JPMorgan Flags $165 Billion in Quarter-End Equity Selling Pressure

11 hrs ago

A comprehensive investment analysis of AB Latour in early 2026 reveals a stark divergence in market pricing versus operational reality. The firm’s share price remained relatively stable, yet its wholly owned operations achieved steady organic growth and record profitability across key segments.

As of late April 2026, the global industrial sector is facing mixed signals, defined by actively easing supply chain constraints but persistent currency volatility. This specific macroeconomic environment makes operational resilience an absolute priority for institutional capital assessing European equities.

The following assessment provides a detailed breakdown of the firm’s recent consolidation strategy and its direct impact on long-term shareholder value. The analysis examines the structural growth mechanics of the new Innovalift business area, evaluates recent targeted acquisitions, and maps the evolving margin profile against current exchange rate headwinds.

By isolating the performance of core subsidiaries from the volatility of the listed portfolio, investors gain a clearer perspective on the firm’s valuation. This analytical division is necessary to accurately evaluate the underlying viability and forward capital allocation capacity of the overarching holding structure.

The financial results for Q1 2026 present a clear split between the temporary struggles of the listed portfolio and the structural resilience of the wholly owned subsidiaries. Investment AB Latour reported an adjusted net asset value of SEK 1,125 per share at the end of the first quarter, representing a 3 percent increase from Q4 2025. This underlying growth occurred despite the listed equities portfolio delivering a 5 percent total return, significantly trailing the 1.2 percent decline of the SIXRX benchmark.

The severity of the listed investment portfolio underperformance mechanically depressed the overarching valuation, obscuring the fact that unlisted industrial operations maintained robust operating margins during the same period.

Investors assessing the headline share price decline must look directly at the operational health of the core business units. Wholly owned operations successfully counterbalanced the listed equities drag, achieving 5 percent organic order intake growth and 4 percent organic net sales growth. The adjusted operating margin for these wholly owned operations held steady at 30.2 percent, providing concrete proof of management execution during a complex trading period.

Adding further context, the Patricia Industries segment generated a 4 percent total return for the quarter. This division achieved 3 percent organic constant currency growth, which was ultimately offset by a 7 percent reported sales decline due to negative exchange rate effects.

These currency headwinds acted as a temporary 6 percent drag on overall reported sales rather than indicating a fundamental structural failure. The underlying organic momentum dictates future dividend stability and capital allocation capacity, making the operational performance highly relevant for long-term equity holders.

| Segment | Organic Growth | Margin or Return | Key Drivers |

|---|---|---|---|

| Wholly Owned Operations | 4% Net Sales, 5% Order Intake | 30.2% Adjusted Operating Margin | Pricing power, structural resilience, acquisition integration |

| Listed Portfolio | N/A | 5% Total Return Q1 2026 | Market volatility, benchmark underperformance |

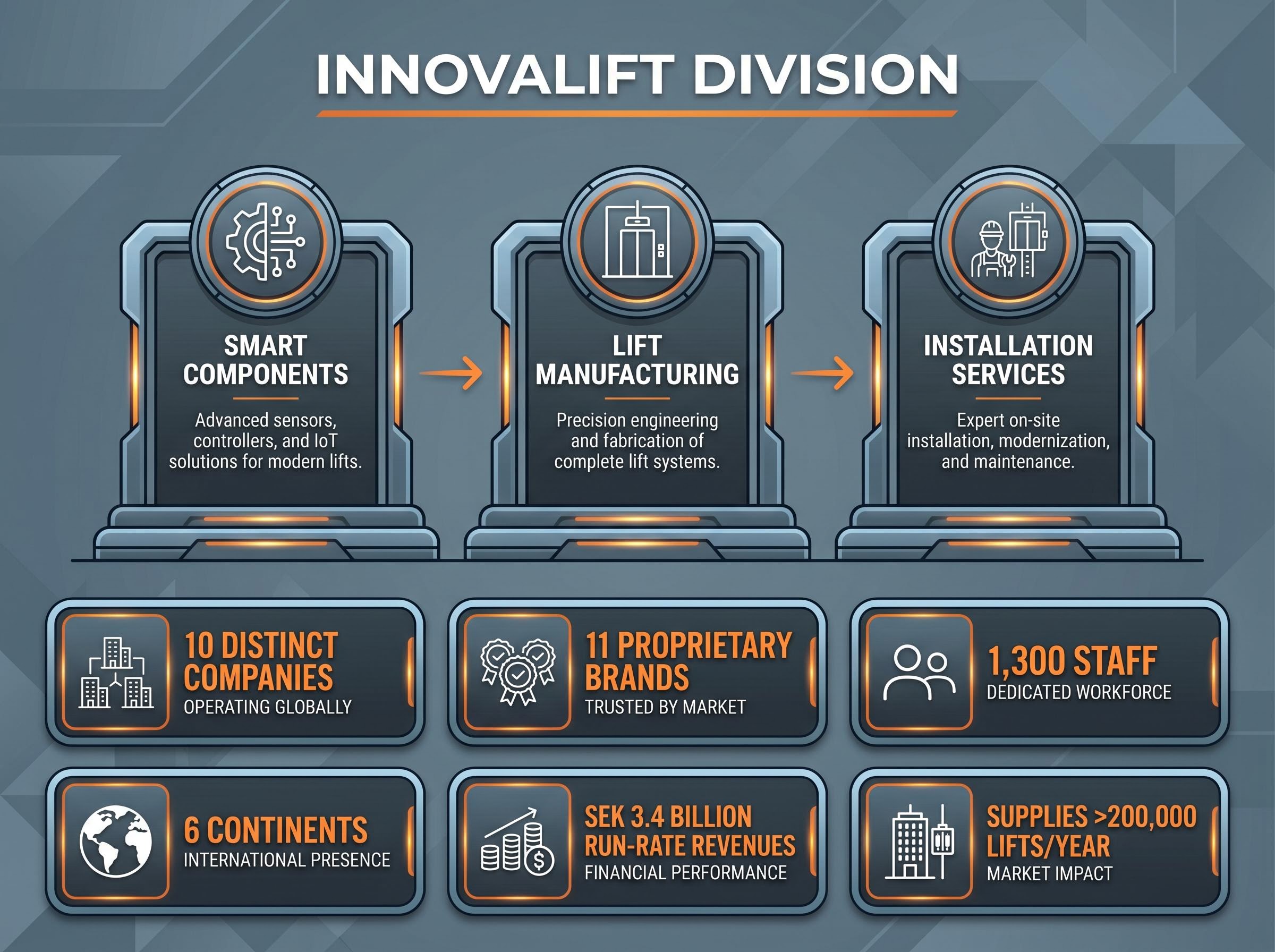

To properly evaluate the long-term growth potential of the holding structure, investors must understand the operational mechanics of the Innovalift division. This newly formed independent business unit is structured specifically to act as a global consolidator in the highly fragmented lift industry. The division operates through a three-cluster business model encompassing smart components, lift manufacturing, and installation services.

Innovalift currently manages 10 distinct companies and 11 proprietary brands, employing 1,300 staff across six continents. The unit generates an unconfirmed, previously rumored run-rate of SEK 3.4 billion in annual revenues and supplies critical components to over 200,000 lifts per year. This massive scale provides immediate operational leverage in a market where smaller regional operators struggle with rising compliance requirements and component costs.

Despite regional market softness in the Middle East and Asia, the segment delivered highly resilient financial performance. Adjusted operating profit remained positive in Q1 2026, maintaining a stable operating margin. This educational breakdown clarifies exactly why the lift sector now represents the third-largest wholly owned unit within the parent company.

Industry consolidation is actively accelerating globally, highlighted by macro trends such as ongoing Otis-Kone merger activities. The operational structure of the Innovalift division connects directly to specific macroeconomic tailwinds driving long-term global demand:

Recent global elevator market growth projections highlight how rapid urbanisation and smart city development are structurally expanding the addressable market for lift component manufacturers. This sector expansion provides a clear rationale for allocating capital toward fragmented but high-margin smart vertical transportation systems.

Aging population demographics requiring increased accessibility infrastructure in residential sectors. Accelerating urbanisation driving high-density vertical construction across developing markets. Sustainability modernisation initiatives forcing building owners to upgrade legacy energy systems. Digitalisation of building management through Internet of Things component integration.

Management initiated a deliberate and highly targeted acquisition phase during and immediately following the first quarter of 2026. This concentrated merger and acquisition activity reveals a clear strategic pattern focused on building new platforms and reinforcing existing geographic dominance. Rather than pausing capital deployment due to the 15 percent Net Asset Value discount, the firm used its strong balance sheet to accelerate structural growth initiatives.

These strategic moves are projected to add approximately SEK 500 million in annualised net sales to the corporate top line. The company funded these targeted expansions through a complementary strategy of divesting non-core assets, ensuring strict capital efficiency. Latour Industries saw a direct 10 percent acquired growth boost from this capital recycling approach, capitalising on a smart building sector that is expanding at 8 percent year-over-year.

The recent acquisitions demonstrate exactly where management is deploying capital to expand its specific industrial footprint. The most significant transactions include:

The analytical consequence of these strategic acquisitions is clearly visible in the firm’s expanding profit margins despite broader European industrial sluggishness. Strict cost discipline and premium market positioning have effectively insulated the core operating subsidiaries from current market volatility. Investors looking for proof of sustained pricing power will find it within the specialised engineering units.

The official ECB economic bulletin confirms that currency volatility and trade policy shifts have created significant headwinds for the Eurozone manufacturing base over the first quarter of the year. This macro backdrop highlights why strict cost discipline remains crucial for engineering units navigating the current environment.

Nord-Lock Group achieved an all-time high adjusted EBIT margin in Q1 2026, alongside a massive jump in organic order intake. Similarly, logistics automation specialist Caljan recorded organic order intake growth of 34 percent and organic net sales growth of 44 percent. In slower segments like Hultafors, management enacted active cost adjustments to protect profitability, resulting in a stable 14.9 percent operating margin despite entirely flat volume growth.

This operational leverage is absolutely necessary for surviving global supply chain shifts and currency fluctuations without eroding shareholder value. Management expects the currency pressures that compressed reported sales earlier in the year to ease significantly.

Management Outlook on Currency Impacts “While negative currency translation impacted reported growth by up to 6 percent in the first quarter, we anticipate these exchange rate headwinds to moderate significantly heading into Q2 2026, allowing our organic operational strength to fully reflect in top-line results.”

The preceding operational data resolves the current tension between the market discount and the holding company’s long-term growth trajectory. Following the post-earnings drop, the share price stabilised in the SEK 290 to SEK 300 range throughout late April 2026. This pricing represents an approximate 15 percent discount to Net Asset Value, presenting a specific valuation proposition for institutional portfolios evaluating European industrials.

The primary enabler for continued dividend payouts and further consolidation activity is a highly defensive corporate balance sheet. The Net Debt to EBITDA ratio sits comfortably at 1.2x, remaining well within the lower bounds of the firm’s target policy range of 1.0x to 2.5x. This specific financial flexibility secures the firm’s impressive track record of 19 consecutive years of uninterrupted dividend payments.

Institutional sentiment currently balances optimism for the portfolio’s resilience against caution over broader industrial slowdowns. The consensus target price across 12 tracking analysts stands at SEK 340, implying a 19 percent upside from current trading levels.

ABG Sundal Collier issued a Buy rating for the stock, specifically citing the portfolio’s strong structural resilience despite ongoing currency translation effects. Conversely, DNB Markets issued cautionary notes, warning that a broader European industrial sector slowdown could cap near-term multiples, despite acknowledging the firm’s highly secure capital position.

Investors exploring the mechanics of this historical pricing shift will find our full explainer on the Latour NAV discount, which breaks down the specific earnings drivers and subsidiary growth metrics that could ultimately close the valuation gap.

The combination of the Innovalift expansion and the targeted acquisition strategy positions the firm aggressively for the remainder of 2026. While currency effects and listed portfolio underperformance caused short-term volatility, the underlying organic growth engine remains completely intact. The specialised subsidiaries continue to demonstrate the precise pricing power required to defend margins in a complex macroeconomic environment.

For long-term investors, the current valuation discount offers a mathematically compelling entry point into a historically premium industrial holding company. The defensive balance sheet ensures that structural growth initiatives can proceed unhindered by external market pressures.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Innovalift division is a newly formed, independent business unit within AB Latour, structured as a global consolidator in the fragmented lift industry, managing 10 companies and 11 brands across six continents.

In Q1 2026, Investment AB Latour's wholly owned operations achieved 5 percent organic order intake growth and 4 percent organic net sales growth, maintaining a 30.2 percent adjusted operating margin despite listed portfolio struggles.

The investment case for AB Latour centers on its current 15 percent discount to Net Asset Value, strong underlying operational growth, strategic acquisitions, and a defensive balance sheet that supports continued dividends and future consolidation.

Currency headwinds acted as a temporary 6 percent drag on Latour's overall reported sales in Q1 2026, though management anticipates these effects to moderate significantly by Q2 2026.