Headline economic data presents a picture of a resilient consumer base, complicating the US economic outlook for financial markets. Aggregate spending metrics continue to point upward, suggesting households are successfully absorbing higher borrowing costs and inflation. This surface-level resilience obscures a financial strain developing across middle and lower-income demographics. Analysts caution that interpreting national data without examining the underlying income divide could lead to significant portfolio misallocations.

Wall Street Complacency Versus Main Street Reality

A severe disconnect has emerged between equity markets reaching near-record highs and the deteriorating fundamentals of the consumer base. Financial market participants appear highly complacent regarding the mounting pressures facing Main Street. Retail consumers are signalling severe distress in their daily spending habits, yet equities continue to price in an uninterrupted growth scenario.

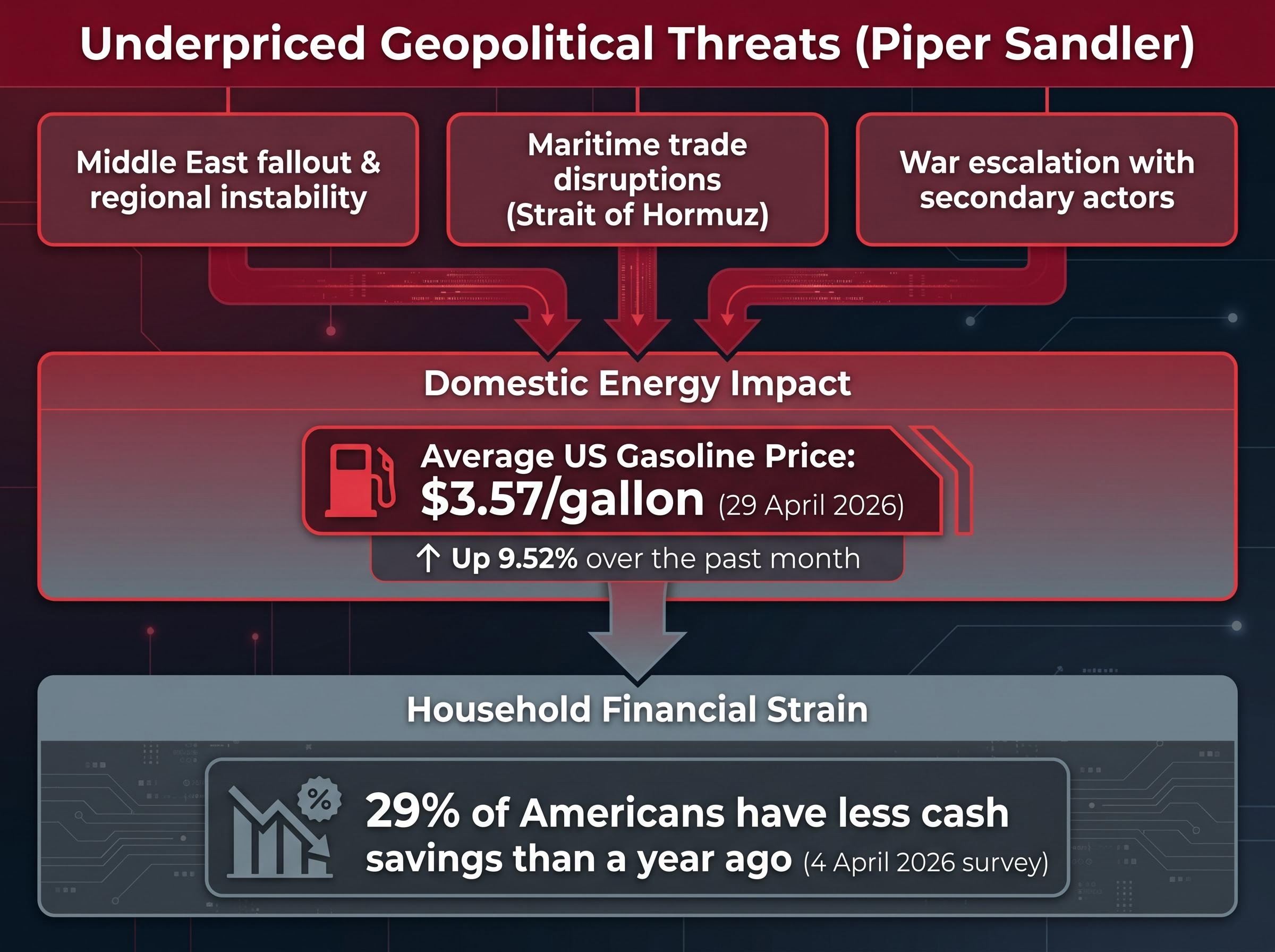

Equity investors are currently ignoring specific geopolitical blind spots that directly threaten global supply chains and domestic energy costs. According to reports, Craig Johnson, Chief Market Technician at Piper Sandler, has repeatedly warned about underpriced geopolitical risks across all major indices. He notes that the current market structure leaves equity portfolios highly vulnerable to a sudden, coordinated consumer pullback.

Johnson outlines several specific near-term threats that equity markets are failing to price accurately.

- Middle East fallout spilling into broader regional instability

- Physical disruptions to maritime trade through the Strait of Hormuz

- Potential war escalation drawing in secondary global actors

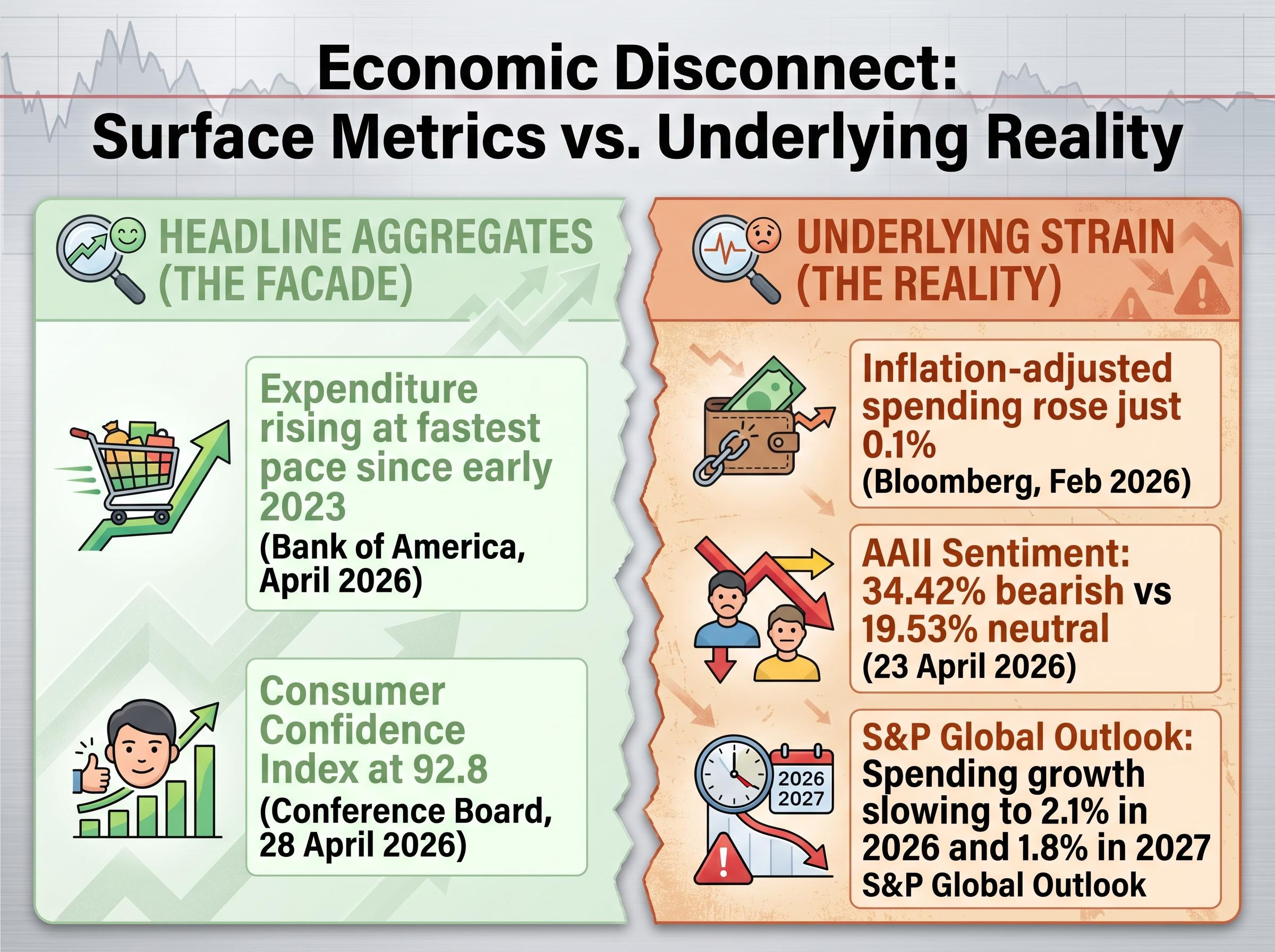

Sentiment metrics clearly capture the growing divergence between Wall Street and everyday consumers. The American Association of Individual Investors sentiment survey for the week ending 23 April 2026 registered 34.42% bearish and 19.53% neutral. This highly cautious outlook contrasts sharply with the bullish positioning seen just before the Iran conflict escalated earlier this month.

For investors looking to contextualise this sudden shift in sentiment, our deep dive into historical stock market warning signals examines how previous energy spikes above four dollars per gallon have reliably preceded significant equity declines.

When big ASX news breaks, our subscribers know first

The Facade of Record Aggregate Spending

The April 2026 economic environment acts as a period of delayed reckoning for financial markets. According to reports, a Bank of America report from April 2026 shows aggregate consumer expenditure rising at its fastest pace since early 2023. These headline figures suggest a population spending comfortably above inflation, reinforcing a highly optimistic narrative on Wall Street. Market strategists point to this data as evidence of structural economic strength.

This optimistic interpretation often ignores the reality of dropping personal savings rates across the broader population, a critical indicator that recent surges in retail volume are being funded by finite reserves rather than genuine wage growth.

Underneath these aggregates, the purchasing power of the average household is eroding steadily. Bloomberg data reveals that inflation-adjusted consumer spending rose by a meagre 0.1% in February 2026. This marginal volume increase highlights a population paying more to consume the same amount of goods, a clear signal of underlying distress.

The sentiment data reflects this mixed and complex reality. The Conference Board Consumer Confidence Index edged up slightly to 92.8 as of 28 April 2026, driven almost entirely by high-income optimism rather than broad-based relief. The full economic weight of the Middle East conflict has not yet filtered through to these trailing sentiment indicators.

Chief Global Economist Commentary “Developed economies have not yet absorbed the full economic weight of the Middle East conflict, with current spending patterns reflecting past confidence rather than future reality,” said Paul Donovan, economist at UBS.

Decoding the K-Shaped Consumer Divide

A K-shaped consumer environment occurs when different income groups experience divergent financial trajectories following an economic shock. High-income households see their financial stability improve and continue spending freely, representing the upward arm of the letter. Lower-income households face mounting budget pressures and reduce their consumption, forming the downward arm.

This structural divide explains how aggregate data currently hides the painful budget realities of the bottom 50%. According to Upside research published on 13 April 2026, a strict spending split exists at the $75,000 household income threshold. Higher-income consumers are single-handedly sustaining national spending averages through premium purchases, while those below the threshold are aggressively cutting discretionary spending.

Recent Federal Reserve Bank of Minneapolis research confirms this divergence by highlighting how elevated borrowing costs disproportionately accelerate the depletion of cash buffers for lower income brackets while leaving wealthier households largely unaffected.

| Household Income Bracket | Current Spending Behaviour | Retailer Preference Shifts |

|---|---|---|

| Above $75,000 | Increased discretionary spending | Premium brands, selective deal hunting |

| Below $75,000 | Reduced discretionary volume | Discount retailers, private-label goods |

Expectations for the future remain sharply polarised across the population. A YouGov report from March 2026 indicates that 34% of adults expect their finances to improve over the year, versus 28% expecting a worsening situation. To survive current budget pressures, cost-conscious consumers are fundamentally altering where and how they allocate their capital.

An Ibotta report from 2026 details a massive shift toward discount retailers like Walmart and Dollar General as buyers seek out everyday value. Even insulated shoppers, who are not severely financially strained, are adopting specific value-focused shopping behaviours to protect their purchasing power against inflation.

Switching from premium national brands to store-owned private-label alternatives Consolidating grocery trips to bulk retailers to maximise unit economics Delaying major appliance and electronics upgrades until promotional periods Trading down from full-service dining to quick-service restaurant formats

Geopolitical Shocks and the Savings Drawdown Mechanism

The ongoing conflict in Iran connects directly to domestic household purchasing power via global energy markets. Rising energy prices function as a regressive tax, consuming a significantly larger percentage of lower-income budgets. As of 29 April 2026, the average US gasoline price sits at $3.57 per gallon, a jump that immediately impacts discretionary income.

Official Bureau of Labor Statistics CPI data validates this pressure, showing substantial monthly surges in the gasoline index that force working families to reallocate funds away from discretionary purchases.

This pricing level represents a 9.52% surge over the past month alone. Consumers are using finite cash reserves to fund these elevated living costs, a dynamic that accelerates the depletion of household savings. This coping mechanism turns an abstract overseas conflict into a highly tangible kitchen-table crisis for the working class.

The rapid drawdown of financial reserves is mathematically unsustainable over the long term. A survey from 4 April 2026 indicates that 29% of Americans currently have less cash savings than they did a year ago. UBS economists have warned about physical supply shortages in energy markets and their direct threat to broader consumer affordability in the coming quarters.

The Hidden Cost of Sustaining Lifestyles

Households are increasingly masking inflation by draining their savings to maintain their previous standard of living. This behaviour temporarily props up the aggregate spending figures seen by market analysts, delaying the inevitable demand destruction. The strategy has an absolute expiration date dictated by the limits of household balance sheets.

The population is currently split between those draining cash and those accumulating it. While 29% are drawing down savings to survive, 25% have managed to grow their reserves through employment rebounds in specific sectors. This stark contrast further reinforces the K-shaped economic divide shaping the underlying fundamentals of the market.

The Inevitable Resolution of Unsustainable Spending

The current divergence between strong aggregate spending and underlying consumer strain must eventually resolve into a downward correction. Consumers cannot fund structural inflation with finite savings indefinitely, regardless of headline employment numbers. When these cash buffers fully deplete, the forced normalisation process will trigger a sudden contraction in retail volumes.

Forecasting models are already plotting the timeline for this impending economic slowdown. The S&P Global Q2 2026 outlook forecasts inflation-adjusted consumer spending growth at 2.1% in 2026. The firm projects this growth will slow even further to a cycle-low of 1.8% in 2027, confirming the expected demand destruction.

Other institutional analysts are adopting an even more cautious stance on future growth, projecting rising recession probabilities if sustained energy inflation prevents the Federal Reserve from delivering its anticipated rate cuts.

Paul Donovan assesses that the gap between current consumer behaviour and economic reality must correct as energy impacts compound over the summer months. This normalisation will likely manifest as a sharp drop in discretionary corporate earnings in late 2026. Financial markets will ultimately be forced to reprice equities to reflect the actual, diminished purchasing power of the average household.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The Reckoning Awaiting the American Consumer

Aggregate spending metrics are currently providing financial markets with a false sense of security. High-income households are generating statistical noise that masks the severe budget pressures facing the broader population. The structural K-shaped divide ensures that headline data cannot be trusted as an accurate indicator of widespread economic health.

The ongoing depletion of savings to fund higher energy and living costs makes a spending contraction inevitable in the near future. Geopolitical shocks continue to accelerate this timeline by inflating the cost of basic necessities at the retail level. Market participants must recognise that current consumption levels are built on finite, rapidly draining household reserves.

Investors should interpret future consumer data releases with extreme scepticism. A reliance on surface-level aggregate metrics will leave equity portfolios highly exposed. When the underlying financial strain finally forces a sudden correction in retail demand, the market recalibration will be swift and significant.

Institutional trading desks are already calculating specific market triggers for impending corrections, preparing for scenarios where sustained blockades force a rapid downward revision of corporate earnings estimates.