How Hormuz Closure at $104 Oil Is Reshaping Every Asset Class

6 hrs ago

After a turbulent Thursday session that saw the Nasdaq drop nearly 1% while Intel soared over 20% after hours, Friday’s earnings slate arrives at a pivotal moment for market sentiment. Investors face a crowded pre-market earnings calendar just as crude oil has breached $100 per barrel and geopolitical tensions continue to shape risk appetite. This analysis breaks down the key reports scheduled before Friday’s opening bell, identifies the metrics that will move markets, and explains how Thursday’s developments set the stage for what comes next.

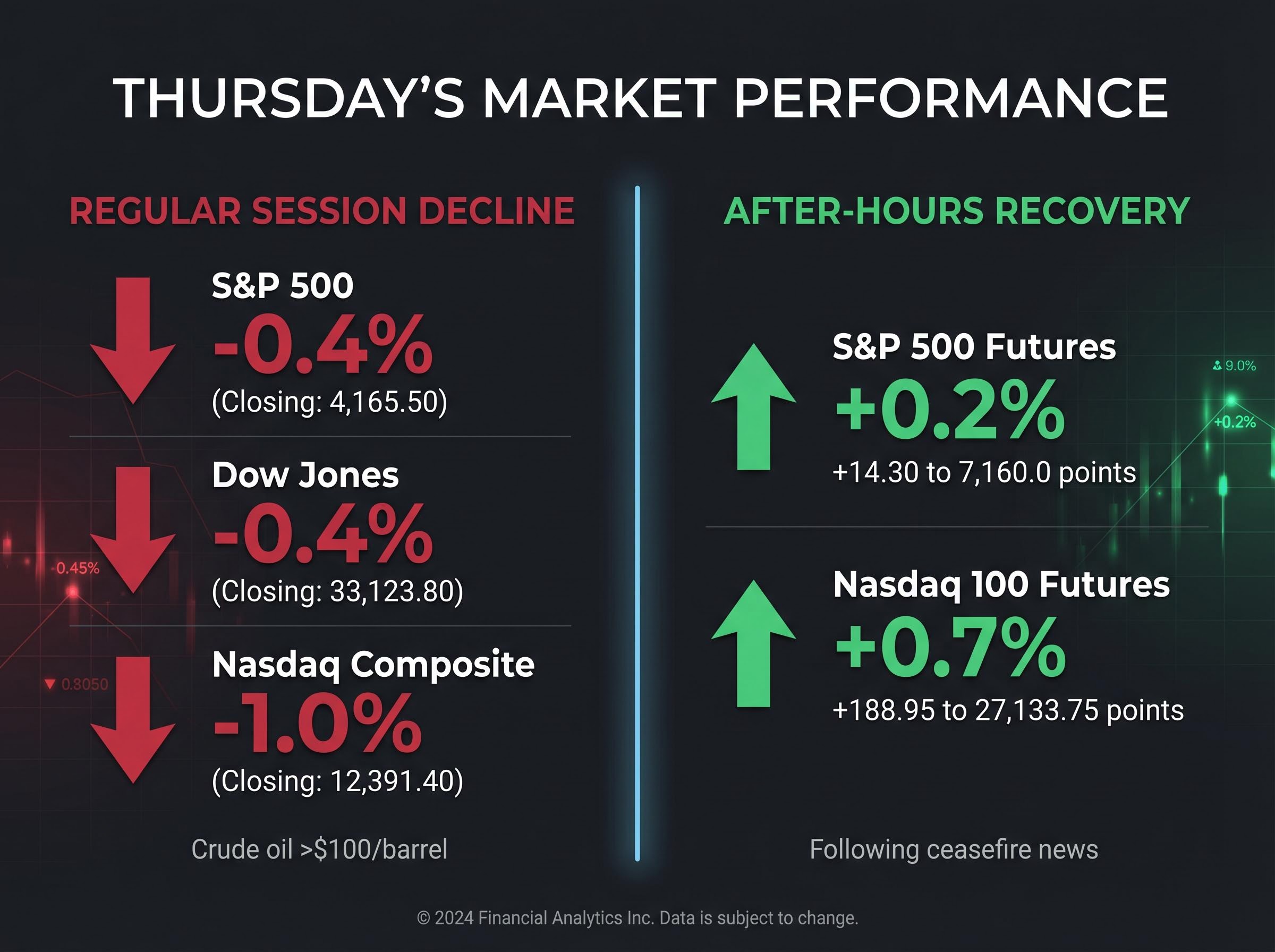

Thursday’s regular session delivered losses across all major indices, with the pullback coming from near-record levels that had defined the previous week’s trading. The S&P 500 and Dow Jones Industrial Average both fell approximately 0.4%, while the Nasdaq Composite led declines with a drop of nearly 1%. Rising energy costs acted as the primary headwind during trading hours, with crude oil prices climbing above $100 per barrel for the first time since the geopolitical crisis intensified.

The cross-asset spillover from geopolitical energy shocks extends beyond equities into bonds and commodities, with US bond yields rising on inflation fears as elevated commodity prices erase Federal Reserve rate cut expectations and tighten financial conditions simultaneously across multiple markets.

The EIA weekly spot price data for WTI crude oil showed March 2026 prices consistently above $90 per barrel, establishing the foundation for the breach of the $100 threshold that occurred in the days following. This pricing trajectory reflects the sustained pressure from geopolitical disruptions rather than a short-term spike.

The after-hours session told a different story. Futures recovered sharply following news of a temporary ceasefire agreement, with S&P 500 Futures gaining approximately 0.2% to 7,160.0 points and Nasdaq 100 Futures advancing 0.7% to 27,133.75 points. The whipsaw between day-session losses and extended-hours optimism reflects a market that remains near highs but is clearly sensitive to new information, whether it arrives from geopolitical developments or corporate earnings.

Market Context ING analysts observed that markets have tolerated rising energy prices while the S&P 500 remains near record levels, a dynamic that suggests investors are pricing the oil surge as a contained disruption rather than a sustained threat to growth.

Understanding Thursday’s split personality, down during the day but recovering after hours, helps investors calibrate their expectations for how Friday’s earnings might be received in a market that has proven resilient yet reactive.

Friday’s pre-market calendar features four major companies whose reports offer a cross-section view of the economy. Procter & Gamble, Norfolk Southern, Charter Communications, and SLB span defensive consumer goods, cyclical transportation, communications infrastructure, and energy services. Each report functions as a window into a different corner of economic activity, with implications that extend beyond the individual companies.

Procter & Gamble represents consumer staples, a sector that typically demonstrates pricing power during inflationary periods but faces margin pressure when input costs surge. Norfolk Southern provides insight into freight volumes and logistics demand, both of which serve as real-time indicators of industrial activity. Charter Communications captures trends in broadband infrastructure spending and subscriber growth, areas that have seen investment accelerate over the past 18 months. SLB, the energy services provider, sits at the intersection of elevated oil prices and increased drilling activity, positioning its results as a direct read on whether the current energy environment is translating to oilfield service demand.

Q1 earnings season had delivered above-expectation results heading into Friday, setting a high bar for these reports. The question is whether the positive momentum can continue into a market that remains near highs but increasingly sensitive to forward guidance.

| Company | Sector | Key Theme to Watch |

|---|---|---|

| Procter & Gamble | Consumer Staples | Pricing power vs margin pressure from input costs |

| Norfolk Southern | Transportation | Freight volumes as industrial activity indicator |

| Charter Communications | Telecommunications | Broadband subscriber growth and infrastructure spend |

| SLB | Energy Services | Oilfield service demand amid elevated crude prices |

Together, these four reports offer a diagnostic for whether different parts of the economy are performing in line with expectations or showing signs of strain.

Earnings beats do not guarantee positive price reactions when valuations are elevated and macro headwinds are present. The market’s response to any given report depends on three factors: results versus expectations, forward guidance tone, and alignment with the macro environment. A company that beats estimates but issues cautious guidance on energy costs or demand visibility can easily sell off, while a company that misses but delivers confidence-building commentary on the quarters ahead can rally.

Netflix’s Q1 2026 results demonstrated this exact dynamic, with shares falling nearly 12% despite revenue growth of 16% and operating margins exceeding 32%, a guidance-driven selloff despite a strong earnings beat that underscores how forward-looking commentary can override backward-looking results when valuations are stretched.

The S&P 500 remains near record levels despite Thursday’s decline, which means valuation multiples have less room to expand from already-stretched positions. In this context, backward-looking results matter less than forward-looking signals. Management commentary on energy costs, consumer demand, and supply chains will be parsed closely, with investors looking for confirmation that companies can navigate the current environment without sacrificing margins or growth.

The S&P 500 valuation dynamics and the split between historical and forward-looking multiples have created a genuinely divided signal for investors, with the Shiller P/E reaching 40.09 in April 2026 (the second-highest reading in 155 years) while the forward P/E compressed to 19.8 times, near its five-year average.

Crude oil above $100 acts as a margin pressure factor for many companies, particularly those in transportation and manufacturing. Whether management teams acknowledge this headwind and quantify its impact, or dismiss it as temporary, will shape how the market prices their guidance.

In periods of elevated uncertainty, forward-looking commentary carries outsized weight. Investors already know Q1 results are largely behind us. What they need is visibility into Q2 and the second half of the year, particularly as geopolitical risks persist and energy prices remain volatile.

Management tone on energy costs, consumer demand, and supply chains will determine whether Friday’s reports reinforce the positive earnings season momentum or introduce new concerns. Three key factors determine post-earnings price movement:

Companies that deliver on all three can cut through a negative session. Those that falter on guidance, even with strong results, risk being sold.

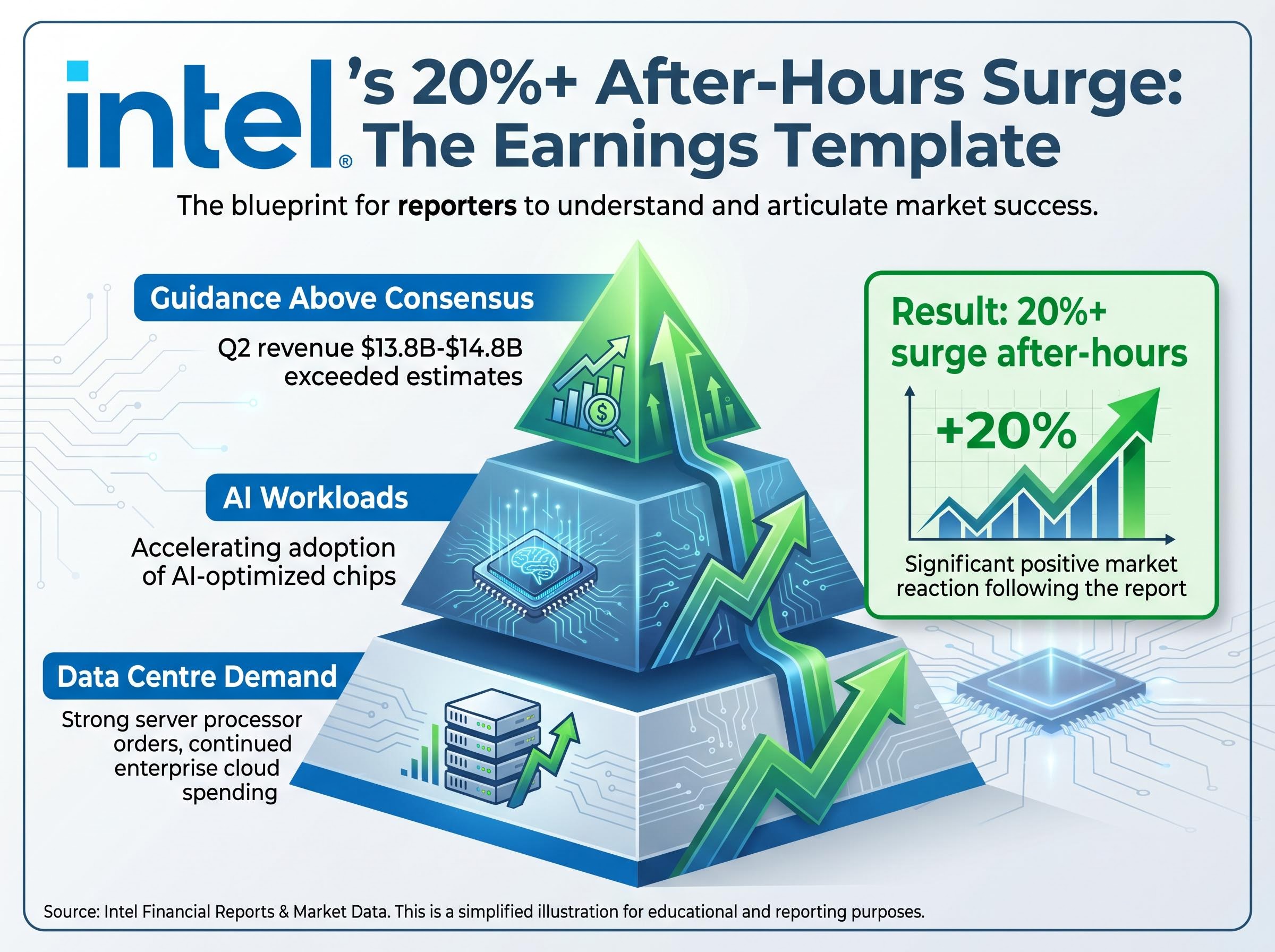

Intel’s Q1 beat and subsequent 20%+ surge in extended trading demonstrates exactly how a strong report paired with confident guidance can cut through a negative session. The semiconductor company delivered results that exceeded analyst expectations, but the real catalyst was its Q2 revenue guidance of $13.8 billion to $14.8 billion, which surpassed consensus estimates and signalled that the company’s turnaround strategy is gaining traction.

Intel’s official Q1 2026 financial results press release confirms the company’s Q2 revenue guidance of $13.8 billion to $14.8 billion, a range that exceeded consensus estimates by approximately 7% at the midpoint and provided the visibility that drove the extended-hours rally. This primary source documents the specific figures that demonstrate how confident forward guidance can override a negative day-session backdrop.

Three drivers fuelled Intel’s beat and the market’s enthusiastic response:

Intel Q2 Guidance Revenue guidance of $13.8 billion to $14.8 billion surpassed analyst estimates, providing the confidence-building signal that drove the extended-hours rally.

Intel’s performance shows that companies with clear growth catalysts can deliver outsized moves even in a choppy market. The lesson for Friday’s reports is straightforward: investors will reward companies that pair solid results with forward guidance that demonstrates visibility and conviction. Management teams that hedge, qualify, or introduce new uncertainties risk being punished, regardless of how strong their backward-looking numbers appear.

Intel’s performance aligns with broader semiconductor sector momentum and record institutional inflows, with combined semiconductor ETF inflows hitting $5.45 billion in April 2026 and the VanEck Semiconductor ETF posting its best monthly return in 25 years at 28.77%, driven by hyperscaler capital expenditure projections exceeding $600 billion.

Friday’s earnings slate lands in a market that closed Thursday lower but recovered in futures trading, with energy costs elevated and geopolitical headlines still fluid. The companies reporting, Procter & Gamble, Norfolk Southern, Charter Communications, and SLB, will offer insight into consumer resilience, logistics demand, infrastructure spending, and energy services. Each report serves as a diagnostic for a different sector, with implications that extend beyond the individual names.

Intel’s after-hours surge demonstrates the template: strong results paired with confident guidance can cut through macro noise and deliver meaningful price moves. The focus should be on forward guidance rather than headline beats, with particular attention to management commentary on energy cost impacts and demand visibility. Friday’s reports will test whether the Q1 earnings season’s positive momentum can continue into a market that remains near highs but is increasingly selective about which stories it rewards.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A Friday earnings preview outlines the key companies reporting results before the opening bell, identifies the metrics most likely to move markets, and provides context about the macro environment shaping how those results will be received. For investors, it helps prioritise which reports to watch and what signals to look for in management commentary.

Procter and Gamble, Norfolk Southern, Charter Communications, and SLB are all scheduled to report before Friday's opening bell, spanning consumer staples, transportation, telecommunications, and energy services respectively.

Intel surged over 20% in extended trading after its Q1 results beat analyst expectations and its Q2 revenue guidance of $13.8 billion to $14.8 billion exceeded consensus estimates by approximately 7% at the midpoint, driven by strong data centre demand and accelerating AI chip adoption.

Elevated oil prices act as a margin pressure factor for companies in transportation and manufacturing, meaning investors will pay close attention to whether management teams quantify the impact of higher energy costs on their forward guidance and profitability outlook.

In the current environment, forward guidance carries more weight than headline beats because the S&P 500 remains near record highs with stretched valuations, meaning companies that miss on guidance or introduce new uncertainties can sell off even when their backward-looking results are strong.