Netflix Earnings Beat Targets Yet Shares Drop 12% on Outlook

Key Takeaways

- Netflix Q1 2026 revenue grew 16% year-over-year to approximately $12.2 billion, beating internal guidance, with operating margins exceeding 32%.

- Shares fell nearly 12% to around $97.31 as full-year 2026 revenue growth guidance of 12-14% and margin guidance of 31.5% disappointed investors expecting acceleration at a 39x earnings multiple.

- Netflix's advertising revenue is projected to double to approximately $3 billion in 2026, with over 4,000 advertisers on the platform and programmatic penetration approaching 50% of non-live ad business.

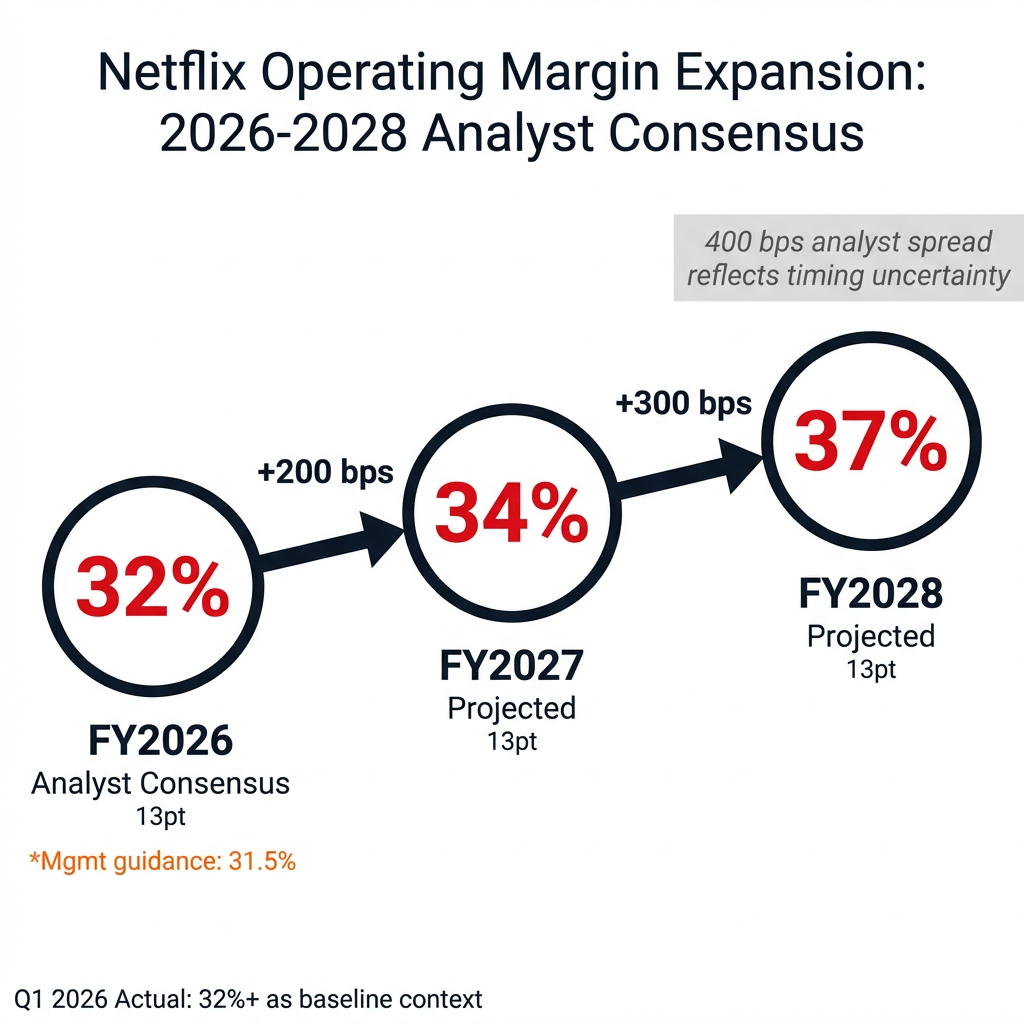

- Consensus projects operating margins expanding from 32% in 2026 to 37% by 2028, though a 400 basis point spread in analyst estimates reflects uncertainty around content expense timing.

- Netflix captures only about 5% of global TV viewing time and has reached fewer than 45% of broadband-connected households, pointing to substantial theoretical growth runway despite near-term deceleration.

Netflix delivered Q1 2026 results that beat internal guidance on 17 April, yet shares plunged nearly 12% to close around $97.31. Revenue climbed 16% year-over-year to approximately $12.2 billion, operating income reached $4 billion with margins exceeding 32%, and user growth hit 31% year-over-year. The selloff wasn’t about quarterly execution. It was about what comes next.

With shares trading 26% below their all-time high and valued at 39x earnings, investors are reassessing whether Netflix’s premium multiple still fits a business guiding to 12-14% revenue growth for the full year. This analysis examines the financial results, dissects the market reaction, and frames what the quarter signals for Netflix’s investment case going forward.

Q1 2026 Financial Results: The Numbers Behind the Headlines

Netflix reported Q1 2026 revenue of approximately $12.2 billion, representing 16% year-over-year growth. The figure exceeded the company’s own internal guidance and demonstrated continued execution across its business lines.

Profitability remained robust. Operating income reached $4 billion, an 18% increase from the prior year. Operating margins exceeded 32%, reinforcing the scalable economics of Netflix’s model at this stage of maturity. These are not the metrics of a struggling enterprise.

| Metric | Q1 2026 | Year-over-Year Change | Context |

|---|---|---|---|

| Revenue | $12.2B | +16% | Beat internal guidance |

| Operating Income | $4B | +18% | Margin expansion trajectory intact |

| Operating Margin | 32%+ | — | Above historical averages |

| User Growth | — | +31% | Strong engagement momentum |

Engagement data reinforced the quarter’s strength. Total viewing hours grew during Q1 despite competition from the Winter Olympics for audience attention. This signals portfolio resilience and user loyalty in a fragmented streaming landscape. The core business fundamentals held firm.

When big ASX news breaks, our subscribers know first

Understanding Netflix’s Earnings Reaction: A Primer

Stock prices reflect future expectations, not past performance. When a company reports earnings, investors evaluate whether results and guidance justify the current valuation. A stock trading at 39x earnings, like Netflix, carries high expectations embedded in its price. Meeting those expectations isn’t enough. Exceeding them is the requirement.

Investors assessing whether Netflix’s 39x P/E remains justified can apply the same valuation frameworks for high-multiple technology stocks used to evaluate Apple’s $3.9 trillion market cap, examining how earnings growth trajectories, margin expansion potential, and competitive moat depth interact to support premium multiples.

Forward guidance often matters more than backward-looking results. Analysts had already reduced Netflix price targets from $130 to $119 before the earnings release, signalling pre-existing caution about the growth trajectory. When guidance comes in at or slightly below consensus, it triggers reassessment of whether premium valuations remain warranted.

At elevated multiples, stocks need to not just meet expectations but exceed them to justify their valuations. Netflix’s Q1 results were solid, but “solid” wasn’t enough for a 39x P/E stock. Investors wanted acceleration, not deceleration.

Why Shares Dropped Nearly 12%: Unpacking the Selloff

Netflix released earnings after the market close on 17 April, and shares immediately dropped approximately 8% in after-hours trading. By the close of regular trading on 17 April, the decline had extended to roughly 11.8%, with shares settling near $97.31. This represented one of the steeper post-earnings declines in recent Netflix history.

The divergent performance across major tech stocks on 17 April, with Apple rallying on China strength whilst Netflix dropped sharply on guidance disappointment, illustrates how company-specific catalysts drove sector dispersion despite broader market gains from the Israel-Lebanon ceasefire agreement.

The guidance disappointment drove the selloff. FY2026 revenue growth guidance of 12-14% and operating margin guidance of 31.5% came in below elevated investor expectations. Analysts characterised the outlook as “in line, maybe a little bit bad”. Not catastrophic, but insufficient to justify the premium multiple Netflix commanded heading into the print.

Several factors compounded the negative reaction:

- Growth deceleration: 16% Q1 growth transitioning to 12-14% full-year guidance signals slowing momentum rather than reacceleration

- Margin compression: 31.5% guidance fell below analyst consensus of 32%, raising questions about expense ramp timing

- Valuation reset: 39x P/E becomes increasingly difficult to justify as growth rates moderate toward mid-teens

- Elevated expectations: The stock had gained over 5% year-to-date and 191% over three years, creating a high bar for positive surprises

Despite the sharp one-day decline, Netflix shares remained up year-to-date and dramatically higher over multi-year periods. The selloff may represent a healthy recalibration rather than fundamental business deterioration. Shares now sit 26% below all-time highs, a level that reframes the risk-reward debate.

Netflix’s 12% post-earnings selloff represents a micro-example of the divergence between stock price appreciation and P/E compression observable across the broader S&P 500 in 2026, where earnings growth has outpaced price gains and driven valuation multiples lower even as indices reach new highs.

The Advertising Bright Spot: Netflix’s $3 Billion Opportunity

Netflix’s advertising revenue is projected to double to approximately $3 billion in 2026, representing one of the fastest-growing segments of the business. This diversification carries increasing strategic importance as subscription growth matures in developed markets.

Operational execution behind the ad tier has been strong. Netflix grew its advertiser base by 70% year-over-year in 2025, reaching over 4,000 advertisers on the platform. Programmatic advertising now approaches 50% of non-live advertising business, indicating infrastructure maturity and scalability that supports the doubling trajectory.

Key advertising metrics for 2026:

- Q1 2026 ad revenue expectation: $598 million

- Full-year 2026 projection: $3 billion (2x 2025 levels)

- Advertiser base: 4,000+ (up 70% year-over-year)

- Programmatic penetration: approaching 50% of non-live ad business

- Strategic investments: continued expansion in go-to-market capabilities and sales infrastructure

The next major ASX story will hit our subscribers first

2026 Outlook and the Path to $51 Billion

Consensus projections place FY2026 revenue at approximately $51.4 billion, implying 13.3% growth and sitting within management’s 12-14% guidance range. Whilst this represents deceleration from recent years, it remains substantial absolute growth for a company of Netflix’s scale approaching annual revenue of over $50 billion.

The margin expansion story unfolds across a multi-year trajectory. Analyst consensus projects operating margins progressing from 32% in 2026 to 34% in 2027 and 37% by 2028. A 400 basis point spread in analyst projections reflects uncertainty about the timing and magnitude of content expense ramps. Management’s 31.5% 2026 margin guidance sits slightly below the 32% consensus, contributing to the April 17 selloff.

Management frames Netflix’s market opportunity as substantial runway remaining. The company captures only about 5% of global TV viewing time and has reached fewer than 45% of broadband-connected households worldwide. With 325 million+ paid members at the end of 2025 and a target of approaching 1 billion total audience, significant theoretical expansion potential persists.

What This Means for Netflix Investors

The bull case centres on core business execution, advertising diversification, massive remaining market opportunity, and a margin expansion trajectory that could deliver 37% operating margins by 2028. Netflix operates at scale, demonstrates pricing power, and continues to capture viewing share in a fragmented streaming landscape. The advertising business provides genuine revenue diversification that could offset subscription maturation in developed markets.

The bear case emphasises growth deceleration as structural rather than cyclical. At 39x P/E, the valuation requires premium growth rates that 12-14% revenue expansion may not support. Increased competition in streaming, maturing subscriber bases in key markets, and execution risk on advertising scale all challenge the premium multiple. If margins expand but revenue growth continues to moderate, the valuation debate intensifies.

Key questions frame the investor decision:

- Is the 12% pullback an opportunity to acquire a quality business at a discount, or the beginning of a sustained valuation reset?

- Does advertising growth provide sufficient diversification to offset subscription maturation, or will the law of large numbers compress total growth regardless?

- With shares at 39x earnings but 26% off highs, where does the risk-reward sit for investors evaluating entry points?

With Netflix shares down 26% from all-time highs but still trading at 39x earnings, investors face the timing debate for technology stock entry points that institutional strategists are navigating across the sector in April 2026, balancing record index levels against valuation compression opportunities in individual names.

The Q1 results didn’t fundamentally alter Netflix’s story. The business continues to execute, margins are expanding, and advertising is scaling. What changed on 17 April was the market’s assessment of what that story is worth at $97.31 per share. That debate will sharpen as the year unfolds and FY2026 guidance either validates or challenges the current valuation framework.

Frequently Asked Questions

What were Netflix Q1 2026 earnings results?

Netflix reported Q1 2026 revenue of approximately $12.2 billion, a 16% year-over-year increase, with operating income of $4 billion and operating margins exceeding 32%, all beating the company's own internal guidance.

Why did Netflix stock drop after Q1 2026 earnings?

Netflix shares fell nearly 12% because full-year 2026 revenue growth guidance of 12-14% and operating margin guidance of 31.5% came in below elevated investor expectations, making it difficult to justify the stock's 39x price-to-earnings multiple.

What is Netflix's advertising revenue outlook for 2026?

Netflix's advertising revenue is projected to approximately double to $3 billion in 2026, supported by a 70% year-over-year increase in its advertiser base to over 4,000 advertisers and programmatic advertising approaching 50% of its non-live ad business.

Is Netflix stock a buy after its post-earnings selloff?

After the selloff, Netflix shares traded 26% below all-time highs at around $97.31, presenting a debated risk-reward; bulls point to margin expansion, advertising growth, and market penetration below 45% of broadband households, while bears argue that 12-14% revenue growth does not support a 39x P/E valuation.

What is Netflix's revenue target for full-year 2026?

Analyst consensus projects Netflix full-year 2026 revenue at approximately $51.4 billion, implying 13.3% growth and sitting within management's guided range of 12-14%.