United Slashes 2026 Profit Outlook 40% as Iran War Hits Fuel

3 hrs ago

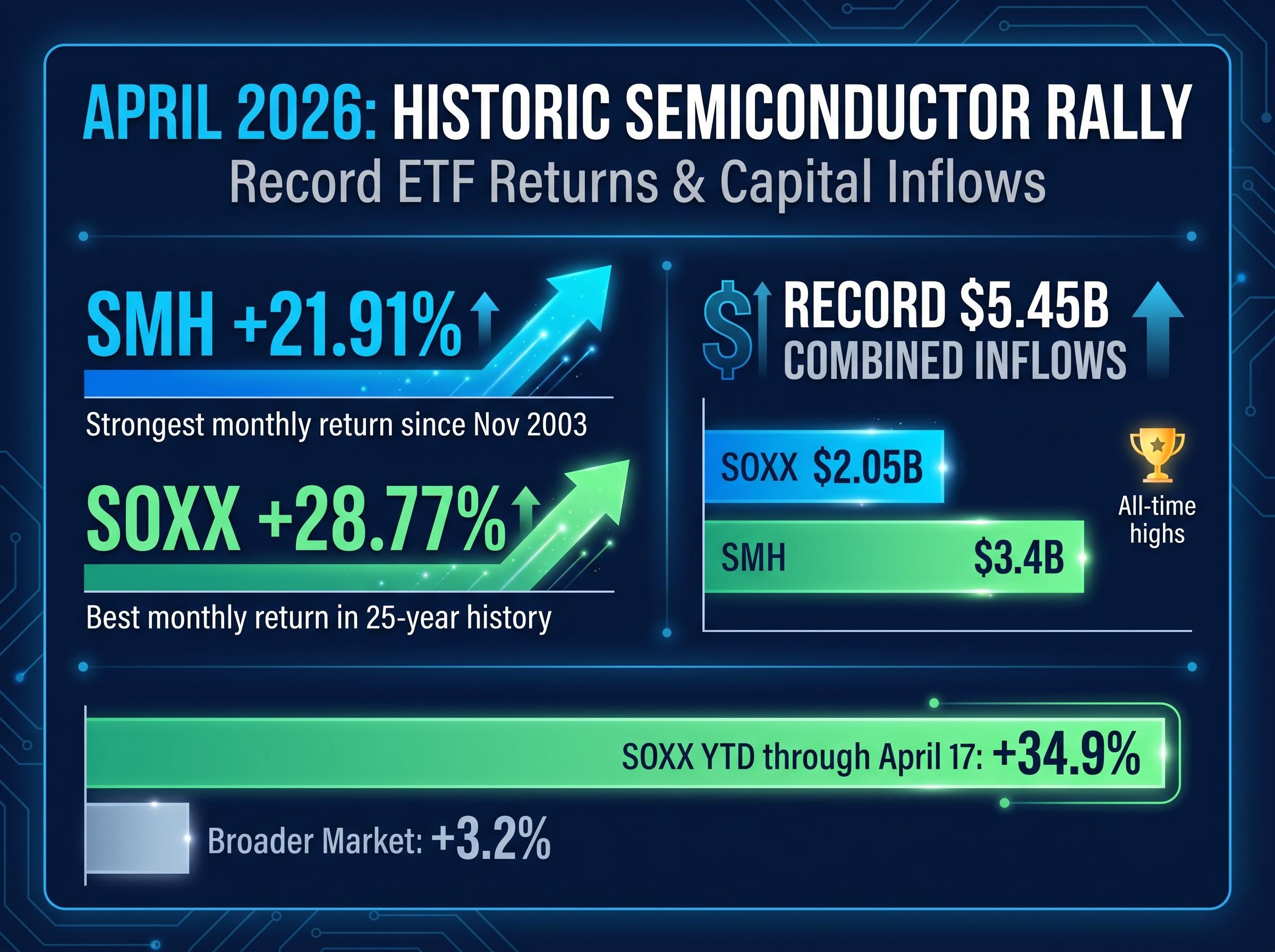

The VanEck Semiconductor ETF delivered 28.77% gains in April 2026, shattering every monthly record in its 25-year history, while the iShares Semiconductor ETF posted its strongest monthly return since November 2003 at 21.91%. Combined capital inflows of $5.45 billion, the largest single-month flow ever recorded for the semiconductor ETF category, signal institutional conviction that the artificial intelligence infrastructure buildout represents a structural multi-year supercycle rather than a speculative trade.

April 2026 has emerged as a historic month for chip stocks, with semiconductor returns diverging sharply from broader market performance. The geopolitical relief rally following the Iran-US ceasefire on 8 April, accelerating hyperscaler capital expenditure exceeding $600 billion in 2026, and memory market shortages driving 80-90% quarter-over-quarter price increases have converged to push semiconductor equities to valuations last seen during the sector’s most bullish periods. This article examines the scale of the rally, identifies the biggest beneficiaries across memory, AI accelerators, and equipment suppliers, and evaluates whether fundamentals support further appreciation or whether April’s gains have already priced in the structural demand shift.

The iShares Semiconductor ETF (SMH) closed April at $453, up from $383.40 in March, delivering a 21.91% monthly return that represents its strongest performance since the volatile market conditions of November 2003. The VanEck Semiconductor ETF (SOXX) surged 28.77% during the month, establishing a new benchmark for monthly appreciation in the fund’s entire operational history and eclipsing all prior records across bull and bear cycles dating back to the fund’s 2001 launch.

Capital flows amplified the magnitude of the move. SOXX absorbed $2.05 billion in April inflows alone, more than doubling its previous monthly record. SMH pulled in $3.4 billion, also an all-time high. The combined $5.45 billion in flows represents institutional capital concentration at a scale not previously observed in the semiconductor ETF category, suggesting large asset managers have increased sector exposure rather than merely rebalancing within existing allocations.

Through 17 April, SOXX had delivered a year-to-date return of 34.9%, substantially outpacing the broader market’s 3.2% gain through the same date. This divergence represents a fundamental reallocation of capital within equity markets, with investors concentrating resources in the technology infrastructure layer they expect to underpin the artificial intelligence revolution.

The April rally distributed gains across memory manufacturers, AI accelerators, and equipment suppliers, with performance reflecting which segments investors view as capturing the most durable demand growth.

Micron Technology emerged as the most explosive performer, with shares up 539% over the one-year period through mid-April and trading around $416. The memory specialist benefits directly from structural shortages, with DDR5 chip prices rising from $6.84 in September 2025 to $27.20 by December 2025, a 298% increase. Despite the extraordinary appreciation, Micron trades at a forward price-to-earnings ratio of just 5.5-12x, substantially below the broader market’s 20.1 and the SOXX index’s 22.5, suggesting valuation has not stretched beyond the magnitude of earnings improvement.

Intel delivered one of the sector’s most unexpected comebacks, with shares surging approximately 78-248% year-to-date through 21 April (sources vary, with the higher figure capturing 12-month performance) to trade near $65.83. The recovery reflects strategic partnerships announced in early April: a $14.2 billion repurchase of Apollo’s 49% stake in Intel’s Fab 34 in Ireland on 1 April, participation in Elon Musk’s $20-25 billion Terafab AI chip complex project alongside SpaceX and Tesla announced on 7 April, and a multiyear Google Cloud partnership announced on 9 April committing to Intel Xeon 6 processors.

Broadcom’s market capitalisation expanded to approximately $1.9 trillion as of 22 April, representing a $560 billion increase from the $1.36 trillion valuation the company held in August 2025. Shares climbed 38% in April alone, reflecting investor recognition that Broadcom’s networking and switching products represent essential infrastructure for AI data centre interconnect fabrics.

Broadcom’s April rally, which added $560 billion in market capitalisation, accelerated following the announcement of the company’s 10-gigawatt OpenAI partnership, a custom AI chip deal projected to generate more than $100 billion in revenue and representing the largest single-customer chip partnership in industry history.

| Company | April/YTD Gain | Market Cap | Key Driver |

|---|---|---|---|

| Micron | 539% (1-year), 46% YTD | $200 billion | Memory shortage, HBM premium |

| Intel | 78-248% YTD | $500 billion | Strategic partnerships (Apollo, Terafab, Google) |

| Broadcom | 38% (April) | $1.9 trillion | AI data centre networking infrastructure |

| AMD | 242% (April) | $400 billion | MI400 series ramp, 60% data centre growth guidance |

| TSMC | 34% YTD, 149% (1-year) | $1.76 trillion | 30%-plus 2026 revenue guidance, advanced node leadership |

| Coherent | 448% (1-year) | Not disclosed | Equipment demand for AI infrastructure buildout |

Advanced Micro Devices surged 242% during April alone, with shares climbing to $274 driven by strategic partnership announcements and accelerating data centre revenue growth. Wall Street maintains 37 Buy or Strong Buy ratings versus only 12 Hold ratings and zero Sell ratings, yielding a consensus price target of $289.35. Equipment suppliers captured substantial gains as well, with Coherent up 448% over one year, Teradyne up 390%, and Lam Research up 295%, demonstrating that the benefits of AI infrastructure buildout have been distributed across the semiconductor supply chain.

The April rally reflects two structural demand pressures converging simultaneously: hyperscaler capital expenditure accelerating to unprecedented levels and memory market shortages that have pushed pricing to multiyear highs.

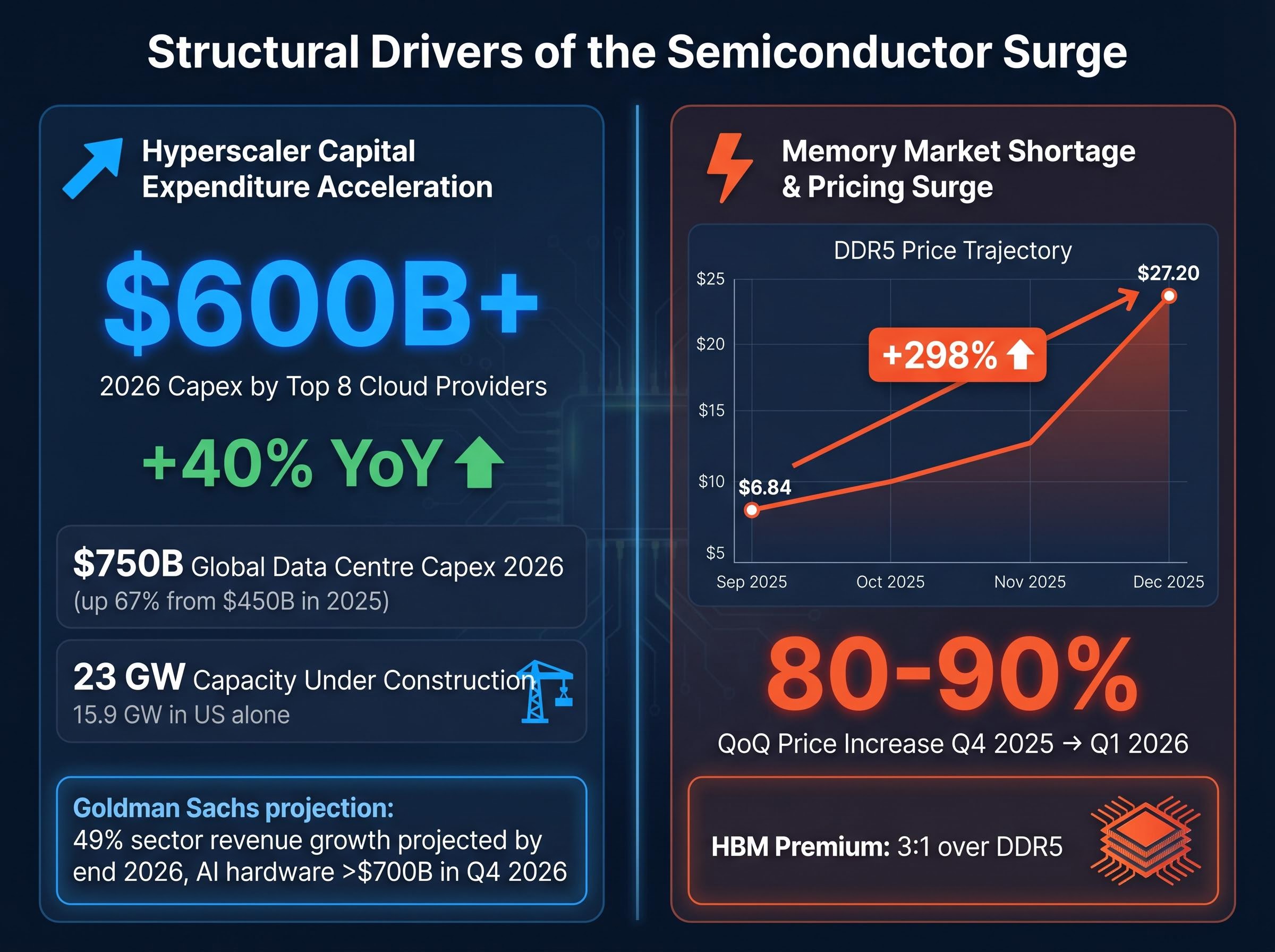

Global data centre capital expenditure is projected to reach approximately $750 billion in 2026, up 67% from $450 billion in 2025. Hyperscaler capital expenditure among the top eight cloud service providers is projected to exceed $600 billion during 2026, representing a 40% year-over-year increase. Over 23 gigawatts of data centre IT capacity was under construction globally as of the end of September 2025, with approximately three-quarters of this capacity being constructed in the United States. The US alone hosts 15.9 gigawatts of data centre capacity under construction, reflecting the extraordinary concentration of infrastructure investment supporting artificial intelligence workloads.

While hyperscalers commit $600 billion-plus in 2026 capital expenditure, physical bottlenecks constraining AI infrastructure deployment, including electrical grid capacity, cooling systems, and advanced packaging equipment shortages, are extending the timeline for when that capacity comes online, creating a potential mismatch between announced spending and operational infrastructure availability.

Dell’Oro Group’s forecast of global data centre capex approaching $1 trillion in 2026 aligns with the $750 billion projection cited widely across semiconductor equity research, reflecting consensus that hyperscaler spending has entered a multiyear expansion phase driven by AI infrastructure requirements.

Memory market dynamics amplified semiconductor demand pressure. DDR5 chip prices rose from $6.84 in September 2025 to $27.20 in December 2025, a 298% increase in three months. Memory prices surged 80-90% quarter-over-quarter from Q4 2025 into Q1 2026 across most segments, representing the most severe pricing escalation in years. High-bandwidth memory (HBM) used in AI accelerator systems commands a 3-to-1 premium over DDR5, and growing HBM demand has crowded out commodity DRAM capacity as memory manufacturers shifted production toward higher-value products. Micron noted a 3-to-1 conversion ratio between HBM and DDR5 wafer capacity, meaning every unit of HBM production ramp directly compresses general-purpose memory supply.

SK Hynix announced mass production of 192GB SOCAMM2 memory modules for NVIDIA’s Vera Rubin AI processors on 21 April, driving a 3.37% share price jump and illustrating how memory manufacturers are capturing pricing power through product differentiation and advanced packaging rather than commodity DRAM capacity expansion.

Goldman Sachs Semiconductor Revenue Projection

Goldman Sachs projects 49% revenue growth in the semiconductor sector by end of 2026 compared to current levels, with AI-related hardware revenues expected to exceed $700 billion in Q4 2026.

The combination of $600 billion-plus in hyperscaler spending, 23 GW of data centre capacity under construction, and structural memory shortages suggests semiconductor demand has a multi-quarter runway. Industry forecasters project supply tightness will persist through at least the back half of 2026, supporting the durability of memory pricing and the exceptional profitability memory manufacturers have realised.

The Iran-US ceasefire announced on 8 April 2026 provided a relief rally catalyst by reducing investor anxiety about energy disruption and data centre operating costs, but the geopolitical development removed a headwind rather than creating a structural tailwind.

The White House statement confirming the 8 April 2026 Iran ceasefire and Strait of Hormuz reopening provided the primary official confirmation of the geopolitical shift that compressed risk premiums across energy and technology equities, setting the stage for the sector rotation that amplified semiconductor gains through the rest of April.

Prior to the ceasefire announcement, geopolitical tensions in the Middle East had contributed to volatility in oil prices, with approximately a 7% oil price surge reflecting geopolitical risk premiums and approximately 4% of global oil supply affected by Strait of Hormuz disruptions. The Nasdaq Composite had entered correction territory on 26 March 2026, falling more than 10% from its February peak, driven by a combination of renewed tariff anxieties, geopolitical tensions, stubborn inflation concerns, and rotation away from richly valued growth stocks.

Timeline: Correction to Rally

26 March 2026: Nasdaq Composite enters correction territory, down 10% from February peak

8 April 2026: Iran-US ceasefire announced, initial two-week truce begins

April 2026: Semiconductor rally delivers record ETF gains as geopolitical risk premium compresses

The ceasefire timing proved particularly beneficial for semiconductor stocks, as it reduced concerns about potential energy supply disruptions that might constrain data centre operations or increase their operating costs at a moment when the sector had already corrected meaningfully. However, lingering effects from the Strait of Hormuz crisis continue to influence shipping costs and material availability, with residual material shortages warranting ongoing attention. The rally’s durability depends on fundamentals, specifically whether hyperscaler capital expenditure plans and memory market conditions sustain demand, rather than whether the geopolitical truce holds.

The earnings calendar through early May will test whether April’s appreciation has captured the sector’s upside or whether fundamentals support further gains.

TSMC raised its full-year 2026 revenue growth guidance to above 30%, substantially exceeding historical norms and reflecting the company’s confidence in sustained demand for advanced semiconductor manufacturing capacity. Global semiconductor revenue is projected to exceed $1.3 trillion in 2026, marking the highest growth in two decades. Morgan Stanley lists NVIDIA ($260 target), Broadcom ($470 target), and Astera Labs as top picks for 2026, emphasising AI spending as the key driver. Wall Street consensus on AMD remains firmly bullish, with 37 Buy or Strong Buy ratings versus 12 Hold and zero Sell, yielding a consensus price target of $289.35.

TSMC’s 30%-plus revenue guidance for 2026, which exceeded analyst expectations and marked the highest growth rate in the foundry’s history, did not prevent a 3% share price decline on 17 April as investors focused on supply chain concentration risk and the sustainability of hyperscaler spending rather than the magnitude of the near-term revenue beat.

Despite strong fundamentals, several risk factors warrant caution:

The upcoming earnings releases from AMD and Intel will reveal whether the rally has room to extend or whether valuations have already captured the structural demand shift. Investors should monitor TSMC and AMD results closely as bellwethers for AI infrastructure demand, with particular attention to commentary on hyperscaler capital expenditure plans, memory pricing trajectories, and forward guidance relative to consensus expectations.

April 2026 has delivered historic gains for semiconductor investors, with record ETF inflows of $5.45 billion and breadth across memory, AI accelerators, and equipment suppliers signalling institutional conviction in the artificial intelligence infrastructure supercycle. The combination of $600 billion-plus in hyperscaler capital expenditure, 23 GW of data centre capacity under construction, and structural memory shortages driving 298% DDR5 price increases suggests demand has a multi-quarter runway.

With AMD and Intel reporting in the coming days and TSMC guiding for 30%-plus revenue growth, the sector’s trajectory through May depends on whether earnings validate the pace of appreciation. Investors should track the upcoming releases for confirmation that fundamentals support the rally, while remaining mindful that 35% year-to-date gains have raised the bar for positive surprises.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Semiconductor stocks are rallying due to three converging forces: hyperscaler capital expenditure exceeding $600 billion in 2026, structural memory shortages that pushed DDR5 prices up 298% in just three months, and the geopolitical relief from the Iran-US ceasefire on 8 April 2026 compressing risk premiums.

SOXX is the VanEck Semiconductor ETF, a fund tracking chip sector equities since 2001. In April 2026, it delivered a 28.77% monthly return, its strongest performance in the fund's 25-year history, while absorbing $2.05 billion in inflows, more than double its previous monthly record.

Micron Technology led with a 539% one-year gain driven by memory shortages, AMD surged 242% in April on data centre growth, Broadcom added $560 billion in market capitalisation to reach $1.9 trillion, and equipment suppliers Coherent and Teradyne rose 448% and 390% respectively over one year.

Sustainability depends on upcoming earnings from AMD (5 May) and Intel, with analysts watching for confirmation of 33% year-over-year EPS growth at AMD and continued hyperscaler spending commitments; risks include SOXX trading at a 22.5x forward P/E, export control uncertainty, and questions about whether 80-90% quarter-over-quarter memory price increases can persist.

AI infrastructure spending is the primary structural driver, with the top eight cloud providers committing more than $600 billion in capital expenditure during 2026 and over 23 gigawatts of data centre capacity under construction globally, creating multi-quarter demand visibility for chips across memory, accelerators, and networking equipment.