Washington Charges 38 Entities in $10M AI Crypto Fraud Sweep

4 hrs ago

The KOSPI surged past 6,350 in morning trading on Monday, reaching an all-time high as semiconductor giants SK Hynix and Samsung Electronics extended their 2026 dominance. The breakthrough caps an 18-month rally that has carried the index from approximately 4,200 at the start of 2025, with the latest leg powered by a multibillion dollar Samsung SDI battery supply contract with Mercedes-Benz announced Sunday. The record arrives despite persistent Middle East geopolitical tensions that have rattled global markets in recent weeks, underscoring investor conviction that South Korean technology sector fundamentals outweigh macro risks.

The record arrives despite persistent Middle East geopolitical tensions that have rattled global markets in recent weeks, with the geopolitical risk impact on Asian currency markets creating cross-currents that Korean equity investors must navigate alongside semiconductor fundamentals.

Global investors tracking Asian technology exposure now face a market where the KOSPI has climbed more than 1,500 points in under four months, raising questions about momentum sustainability, market breadth, and whether the rally has room to extend or is pricing in future gains prematurely.

The KOSPI opened Monday morning above 6,350, marking an all-time high for the benchmark index. The move extended a rally that has accelerated through successive milestones this year, each threshold breached with increasing speed.

The 2026 trajectory shows the index climbing from 4,840.74 on 16 January to 5,023.76 by 26 January, then pushing through 5,507.01 on 13 February before reaching the current record. The index crossed 6,000 for the first time only in late February, meaning it has gained another 350-plus points in under two months.

2026 Milestone Progression:

The KOSPI200, which tracks the largest 200 companies, moved in parallel with the broader index. The Korean won strengthened 0.34% to 1,475 per USD, reflecting currency market confidence in the rally’s durability.

Daily Gain: The KOSPI’s intraday surge represents the continuation of momentum that has seen the index climb more than 30% from its early 2026 levels.

For global investors using KOSPI as a proxy for Asian technology exposure, the speed of the advance matters as much as the magnitude. The index has now breached four major psychological thresholds in four months, a pace that raises questions about how much future earnings growth is already embedded in current valuations.

Semiconductor stocks remain the primary engine driving the KOSPI to successive records, with company-specific strength translating directly into index-level gains.

1. SK Hynix

SK Hynix reached a record high of 880,000 won (approximately $595.93) on 13 February, as part of the broader technology rally. The advance extended year-to-date gains that have seen the memory chip manufacturer outpace broader market returns, supported by AI infrastructure buildout and market share gains in advanced memory products.

2. Samsung Electronics

Samsung Electronics hit 181,200 won on 13 February as part of the broader technology rally. The stock’s advance reflects investor confidence in the company’s positioning across multiple semiconductor segments, from memory to logic chips.

Fundamental Catalyst: Estimated Q4 semiconductor profit surge of 147% provides fundamental justification for elevated valuations across the sector.

The 147% profit growth estimate anchors the investment case for Korean semiconductor exposure. For global investors assessing whether the rally has further room to run, this figure represents the dividing line between momentum-driven speculation and earnings-supported valuation expansion. Semiconductor exposure remains the primary reason institutional capital flows toward Korean equities, making these two stocks the critical barometers for whether the “Korea premium” thesis can extend into the second half of 2026.

The 147% profit growth estimate anchors the investment case for Korean semiconductor exposure, though understanding the broader semiconductor sector momentum versus value dynamics helps investors assess whether the rally reflects sustainable earnings expansion or speculative positioning that could reverse if macro conditions deteriorate.

The rally’s second catalyst emerged Sunday when Samsung SDI secured a multibillion dollar electric vehicle battery supply contract with Mercedes-Benz, positioning the Korean manufacturer as a supplier to all three leading German automakers.

The agreement, signed by Samsung SDI CEO Cho Joo-sun and Mercedes-Benz Chief Technology Officer Jörg Bruser in Seoul, expands Samsung SDI’s footprint in the premium automotive segment. The contract follows earlier supply agreements with BMW and Volkswagen Group, cementing Samsung SDI’s role in the European electric vehicle supply chain.

Contract Details:

ETF Market Growth: South Korea’s total exchange-traded fund assets expanded over 30% in 2026 to 400 trillion won (approximately $270 billion), with semiconductor and battery-focused funds driving the growth.

For global investors seeking diversified Korean technology exposure beyond semiconductors, battery stocks provide access to the multi-decade structural growth theme of electric vehicle adoption. The Mercedes-Benz contract demonstrates how Korean suppliers are capturing share in the global EV supply chain, translating automotive industry electrification into tangible revenue opportunities for ASX-listed Korean equities and their international peers.

The KOSPI’s climb to record highs reflects structural forces beyond single-session momentum, positioning South Korea among the top-performing equity markets globally in 2026.

As of 16 January, the KOSPI had gained 14.9% year-to-date, significantly outpacing most global peers. President Lee referenced a shift from “Korea discount” to “Korea premium” in January remarks, framing the rally as a reassessment of Korean equity valuations relative to developed market peers.

The weak Korean won, trading at 1,475 per USD, provides export competitiveness tailwinds across multiple sectors. Korean manufacturers benefit from currency dynamics that make their products more price-competitive in dollar-denominated markets, supporting order flow growth.

The won’s weakness translates into tangible competitive advantages for Korean exporters, particularly in sectors where pricing power matters and global competition is intense.

Sectors Benefiting from Won Weakness:

Strong order flow in these sectors provides fundamental support for equity valuations, with export-driven revenue growth offsetting domestic demand weakness. For global investors, the won’s position creates a natural hedge within Korean equity exposure, where currency depreciation supports earnings growth for the largest index constituents.

The “Korea premium” thesis rests on whether this combination of sector strength, currency tailwinds, and technology leadership can persist as developed market peers navigate their own economic transitions. Semiconductor profit growth of 147% suggests the fundamental case remains intact, though market breadth concerns (examined in the next section) complicate the sustainability narrative.

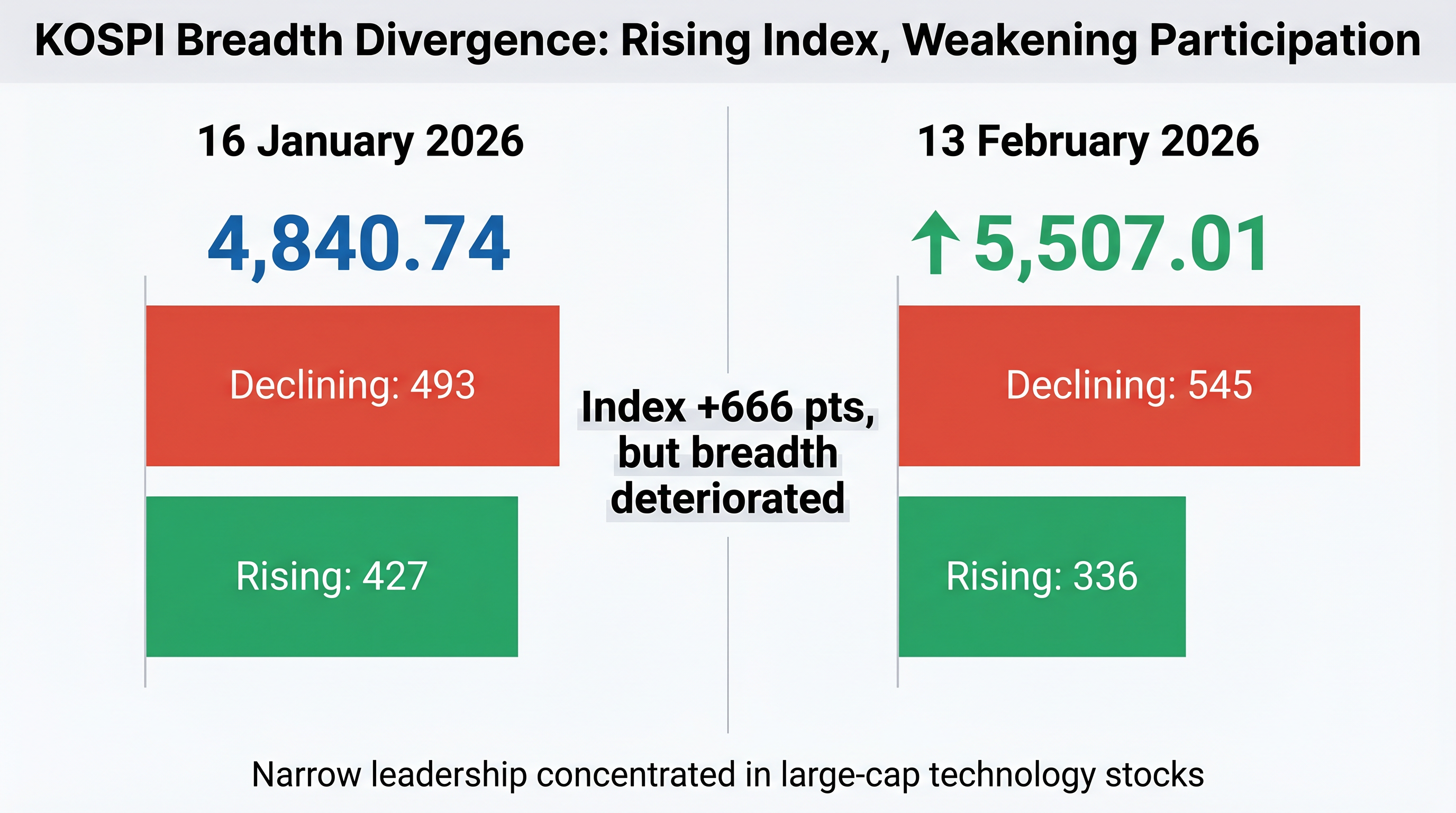

The KOSPI’s record high masks narrower participation beneath the surface, with market internals revealing concentration risks that could matter if sentiment shifts.

| Date | KOSPI Level | Declining Stocks | Rising Stocks |

|---|---|---|---|

| 16 January | 4,840.74 | 493 | 427 |

| 13 February | 5,507.01 | 545 | 336 |

On 13 February, 545 stocks declined versus only 336 rising despite the index reaching then-record levels. The divergence between index performance and underlying stock participation indicates large-cap dominance, particularly in semiconductor and battery sectors, while mid-cap and small-cap names lag.

The divergence between index performance and underlying stock participation mirrors market breadth and sentiment divergence patterns in late-stage rallies, where headline indices climb on narrowing leadership while broader market internals deteriorate, creating vulnerability to sharp reversals if catalysts shift.

Foreign investors have been net sellers in recent sessions, with domestic retail investors driving the advance. Individual investors appear to be using Middle East-related pullbacks as buying opportunities, with fear-of-missing-out behaviour evident in trading patterns. On 24 March, the KOSPI gained 2.7% to 5,553.92 as retail capital flowed into technology stocks during a broader market dip.

Risk Factors:

For global investors, these dynamics present a classic late-cycle rally pattern where headline indices climb on narrowing leadership. Record highs driven by retail euphoria while foreign institutions sell represent a risk that monitoring systems should flag. The sustainability of the rally depends on whether semiconductor earnings can justify current valuations and whether market participation broadens beyond the current narrow leadership group.

The KOSPI’s record above 6,350 confirms South Korea’s position as a standout performer in 2026, powered by semiconductor profit growth of 147% and expanding battery sector contracts such as Samsung SDI’s multibillion dollar Mercedes-Benz agreement. The rally’s speed, climbing more than 1,500 points in four months, reflects investor conviction that Korean technology sector fundamentals outweigh geopolitical risks.

Narrow market breadth and foreign selling warrant monitoring. On 13 February, 545 stocks declined despite the index reaching then-records, indicating large-cap dominance that could reverse if sentiment shifts. The May 2026 expected debut of single-stock leveraged and inverse exchange-traded funds may add further retail trading activity to an already momentum-driven market.

Global investors should monitor semiconductor earnings releases and foreign investor flows as indicators of whether the Korea premium can extend. The 147% profit growth figure provides fundamental support for current valuations, but the narrow leadership group and retail-driven momentum create vulnerability if macro conditions deteriorate or if earnings disappoint in coming quarters.

The KOSPI surged past 6,350 in morning trading on 21 April 2026, marking an all-time high for the South Korean benchmark index after climbing more than 1,500 points in under four months.

The KOSPI record high is being driven by an estimated 147% surge in Q4 semiconductor profits from SK Hynix and Samsung Electronics, combined with Samsung SDI securing a multibillion dollar EV battery supply contract with Mercedes-Benz announced on 20 April 2026.

The contract positions Samsung SDI as a supplier to all three leading German automakers, adding battery sector momentum alongside semiconductor strength and broadening the fundamental case for Korean equity exposure beyond chips alone.

Yes, on 13 February 2026, 545 stocks declined while only 336 rose despite the index hitting then-record levels, indicating the rally is concentrated in 10-15 large-cap technology names while foreign institutions have been net sellers and retail investors drive the advance.

South Korean semiconductors, shipbuilding, defence, and automotive exporters benefit most from the won trading at 1,475 per USD, as their products become more price-competitive in dollar-denominated markets, supporting earnings growth for the largest KOSPI constituents.