SEC Moves to End Mandatory Quarterly Reporting After 50 Years

6 hrs ago

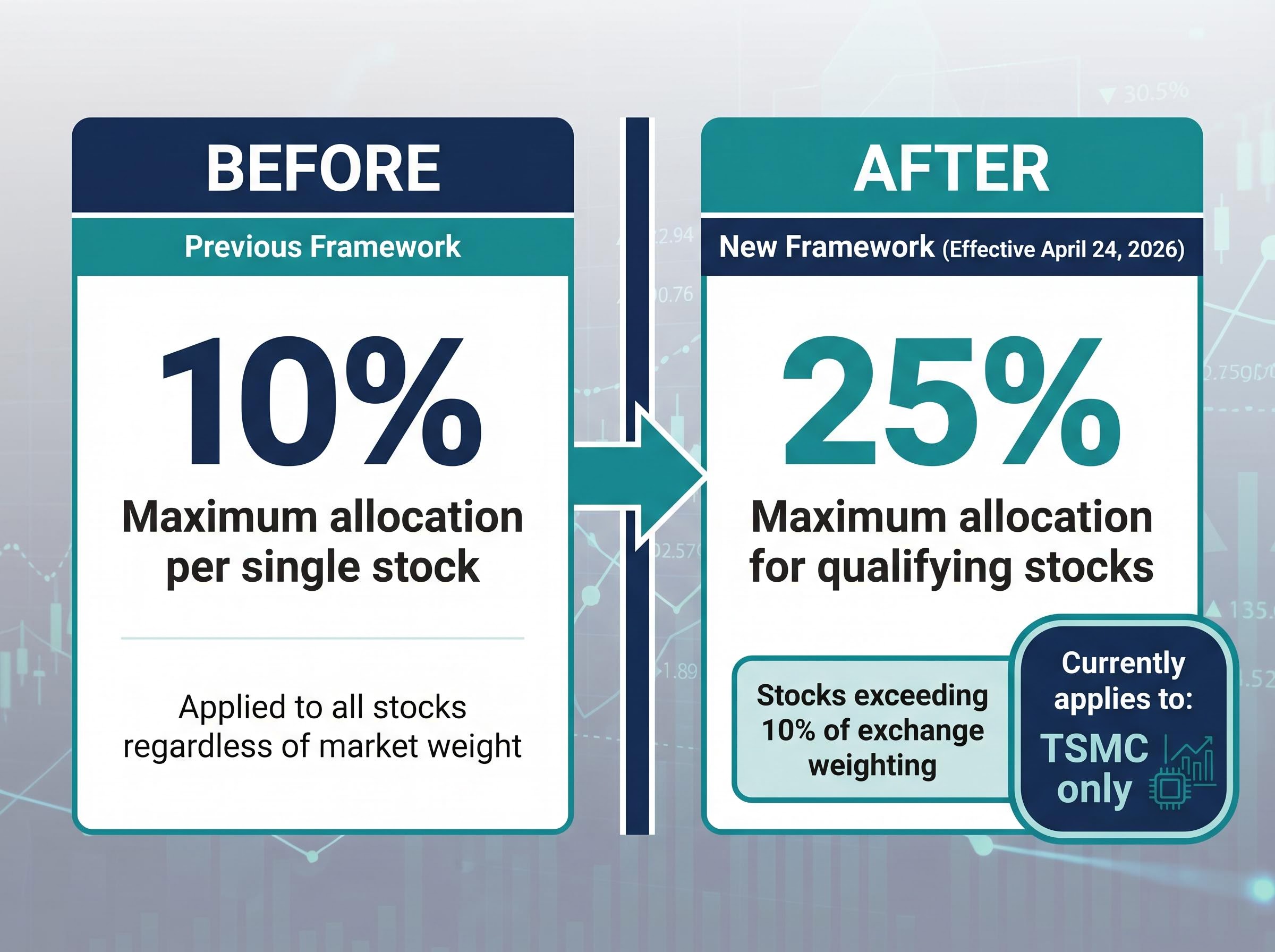

Taiwan’s financial regulator just handed fund managers a new playbook: domestic equity funds can now allocate up to 25% of assets to a single stock, provided that company represents more than 10% of the Taiwan Stock Exchange’s weighting.

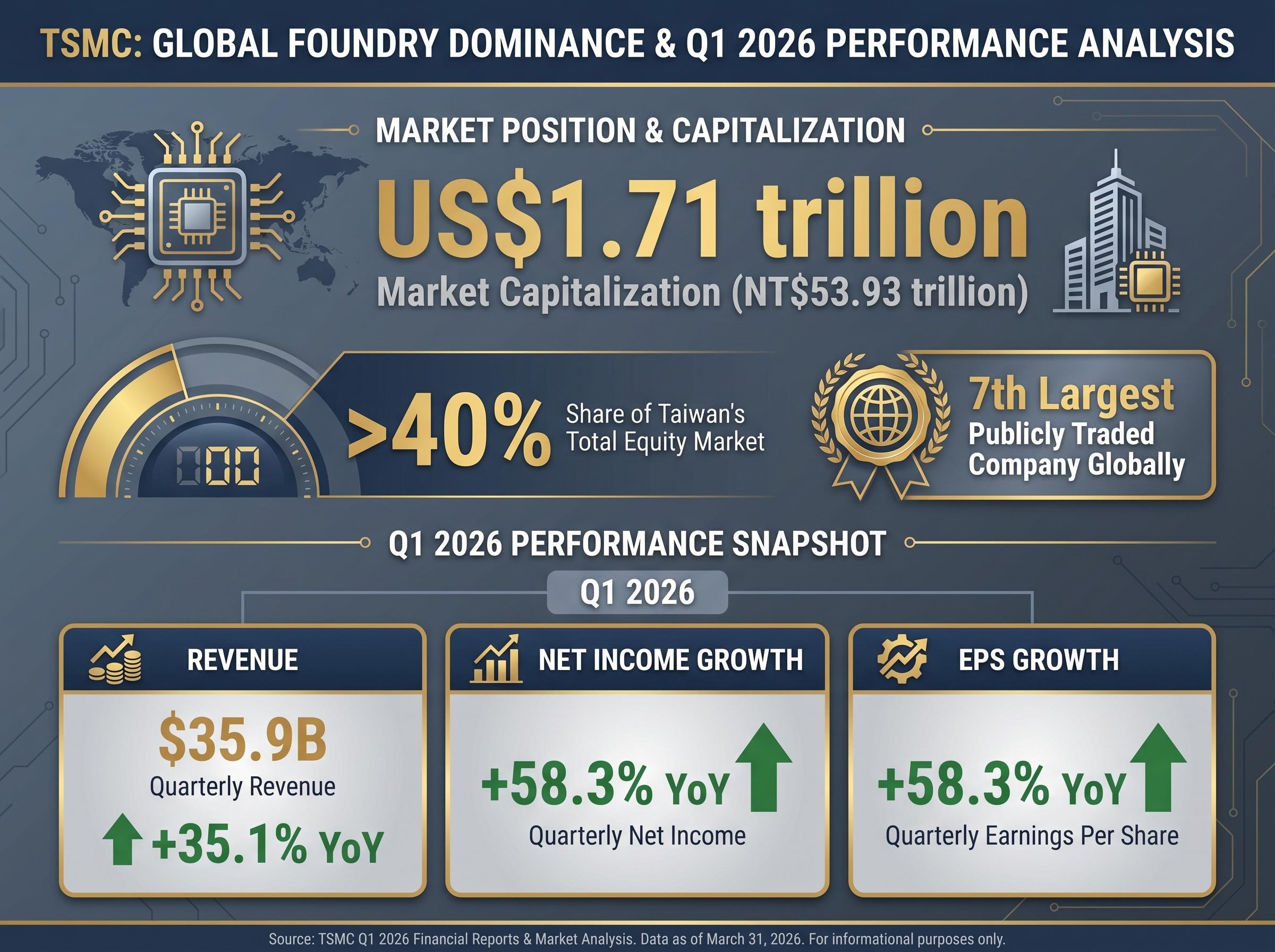

The policy change, effective Friday, 24 April 2026, applies to exactly one company today: Taiwan Semiconductor Manufacturing Company (TSMC), whose market capitalisation of NT$53.93 trillion (approximately US$1.71 trillion) represents over 40% of Taiwan’s entire equity market. The shift reflects regulators grappling with a challenge few developed markets have faced: a single company so dominant that traditional diversification rules force fund managers into structural underperformance.

This analysis examines what the regulatory adjustment signals about Taiwan’s semiconductor sector dynamics, how it reshapes exposure options for investors seeking semiconductor allocation, and what the broader competitive and geopolitical context means for positioning in Taiwan chip stocks.

Taiwan’s Financial Supervisory Commission has altered the mechanics of how domestic equity funds navigate TSMC’s overwhelming market presence. The previous regulatory cap limited any single stock to 10% of fund net asset value, a constraint that forced active fund managers to structurally underweight TSMC relative to its index presence.

The adjustment became necessary because TSMC’s weight in Taiwan’s market had grown so large that adhering to the 10% rule meant missing the dominant driver of index returns. Fund managers faced a structural dilemma: underweight TSMC and underperform the benchmark, or breach regulatory limits.

The new framework allows funds to allocate up to 25% to stocks that exceed 10% of exchange weighting. TSMC is the sole current beneficiary of this threshold.

Regulatory parameters before and after:

Regulator’s stated rationale Taiwan’s Financial Supervisory Commission cited the need to increase flexibility for fund investments given the rapid development of Taiwan’s tech industry and rising market capitalizations of large listed companies.

For investors holding Taiwan-focused active funds, this removes a constraint that systematically diluted their TSMC exposure. Funds can now more accurately reflect market weightings without breaching regulatory thresholds, potentially unlocking capital that was previously forced elsewhere.

The scale of TSMC’s market position made the regulatory adjustment inevitable rather than discretionary. The company’s market capitalisation of NT$53.93 trillion (approximately US$1.71 trillion) positions it as the world’s seventh-largest publicly traded company and accounts for over 40% of Taiwan’s total equity market.

This concentration reflects TSMC’s role as the foundry chipmaker serving Nvidia, Apple, and other artificial intelligence infrastructure leaders. The company reported first-quarter 2026 revenue of $35.9 billion, representing year-over-year growth of 35.1%, with net income and earnings per share both climbing 58.3%.

TSMC’s Q1 2026 earnings results demonstrated the company’s financial strength, with net profit reaching a record $18.2 billion despite shares falling 3% as investors weighed supply chain risks and capacity constraints against the 58% profit surge.

Market dominance by the numbers TSMC market capitalisation: NT$53.93 trillion (approximately US$1.71 trillion) Proportion of Taiwan market: Over 40%

The market reacted immediately to the regulatory shift. TSMC shares gained 4.3% in early Friday trading, while the Taiex benchmark climbed 2.7%, outperforming Asian peers and reaching an intraday high of 38,921.95 before closing at 38,715.47.

The sheer scale of TSMC relative to Taiwan’s market creates a structural reality: owning Taiwan increasingly means owning a single semiconductor company. This concentration is both the opportunity (exposure to the world’s dominant advanced chipmaker) and the risk (single-company vulnerability).

TSMC operates as a pure-play foundry, manufacturing chips designed by other companies rather than competing with its own designs. This business model creates sticky customer relationships because Apple, Nvidia, AMD, and other design houses depend on TSMC’s manufacturing capacity and advanced process nodes.

The foundry model means TSMC does not compete with its customers. Apple designs chips; TSMC manufactures them. Nvidia designs graphics processing units; TSMC fabricates them. This separation of design and manufacturing creates structural dependency.

Three elements anchor TSMC’s competitive moat:

The company’s first-quarter 2026 gross margin reached 66.2%, with operating margin at 58.1%, reflecting both premium pricing power and operational excellence. Management guided second-quarter revenue between $39.0 billion and $40.2 billion, representing sequential growth of approximately 10% and year-over-year expansion of 32%.

TSMC’s SEC-filed Q1 2026 earnings report confirms revenue of $35.9 billion, representing year-over-year growth of 35.1%, with net income and earnings per share both climbing 58.3%, gross margin reaching 66.2%, and second-quarter revenue guidance between $39.0 billion and $40.2 billion.

For investors evaluating Taiwan semiconductor exposure, understanding TSMC’s foundry model clarifies why the company commands such a premium and why concentration risk is not easily diversified away. The company’s competitive position is not a function of regulatory protection but of technological and operational superiority that would take years for competitors to replicate.

Taiwan’s semiconductor industry extends beyond TSMC, though no other company approaches its scale or market weight. MediaTek (chip design), United Microelectronics Corporation (foundry competitor), and ASE Technology (assembly and testing) represent significant players within the ecosystem.

MediaTek has emerged as a notable beneficiary of artificial intelligence demand through custom application-specific integrated circuits for cloud infrastructure operators. The company expects custom AI ASIC revenue to exceed $1 billion in 2026 and to account for up to 20% of total revenue by 2027, according to company disclosures.

MediaTek’s revenue guidance reflects the growing hyperscaler shift toward custom application-specific integrated circuits for cloud infrastructure, a trend exemplified by Broadcom’s $100 billion OpenAI partnership that delivers 30% better power efficiency than merchant GPUs.

United Microelectronics Corporation reached a new 52-week high in late April 2026, trading as high as $12.68 and closing near $12.56, up approximately 8% from the prior session. The company beat quarterly earnings per share estimates, reporting $0.13 versus $0.12 expected, with revenue of $1.80 billion representing 7% year-over-year growth.

ASE Technology set a new 52-week high on 22 April 2026, reaching an intraday high of $29.89. The company slightly beat quarterly earnings per share estimates at $0.21 versus $0.20 expected, though revenue came in below forecasts at $5.22 billion versus $5.47 billion expected.

Key Taiwan semiconductor companies beyond TSMC:

Memory ETF inflows signal investor appetite A memory-focused ETF attracted approximately $1 billion in inflows within 10 days, reflecting investor enthusiasm for AI-related semiconductor plays.

While the new concentration rules apply only to TSMC today, investor enthusiasm for semiconductor exposure extends across the supply chain. Understanding where value accrues beyond TSMC helps investors assess whether Taiwan exposure should be concentrated or spread across the ecosystem.

For investors evaluating whether to concentrate TSMC exposure or diversify across the semiconductor ecosystem, understanding how semiconductor ETF index construction determines performance when rallies broaden beyond mega-caps reveals the structural trade-offs between weighted and capped fund approaches.

Cross-strait tensions between China and Taiwan remain the primary factor constraining TSMC’s valuation multiples. The company’s financial strength and technological leadership would command substantially higher price-to-earnings ratios absent geopolitical risk.

Supply chain diversification efforts reflect this concern. TSMC’s Arizona facility began mass production of four-nanometre chips in early 2025 and continues to ramp production through 2026. The company has committed $165 billion to expand Arizona operations into a cluster of six fabrication plants, two advanced packaging facilities, and a research and development centre.

The United States and Taiwan signed a trade agreement in January 2026 that includes $250 billion in direct investments from Taiwanese semiconductor and technology enterprises and an additional $250 billion in credit guarantees to build and expand chip production capacity in the United States.

TSMC’s strategic decisions ripple through the global semiconductor supply chain. The company indicated it would not purchase ASML’s highest-end lithography equipment due to cost concerns, a decision that contributed to ASML losing close to $17 billion in market value.

ASML’s market value loss illustrates TSMC’s supply chain influence ASML lost close to $17 billion in market value following TSMC’s equipment decision, demonstrating how TSMC’s purchasing choices affect upstream suppliers.

Geopolitical risk represents both risk and opportunity. If cross-strait tensions ease, valuation expansion could supplement earnings growth. Escalation scenarios remain a tail risk that could materially impact returns.

Taiwan’s regulatory adjustment reflects a pragmatic adaptation to the market reality that TSMC has outgrown traditional diversification frameworks. The company’s market capitalisation of approximately $1.71 trillion and dominance of over 40% of Taiwan’s equity market created a structural impossibility: fund managers could not maintain index-relative returns while adhering to the previous 10% concentration limit.

The change unlocks greater flexibility for fund managers but does not eliminate concentration risk. It shifts who bears the risk from the fund structure to the investor.

Geopolitical considerations, supply chain diversification efforts, and the durability of artificial intelligence infrastructure demand will shape whether this concentration proves rewarding or risky. TSMC’s first-quarter 2026 revenue of $35.9 billion and net income growth of 58.3% demonstrate financial strength, but cross-strait tensions and ongoing efforts to diversify semiconductor production away from Taiwan remain material considerations.

Investors considering Taiwan semiconductor exposure should evaluate whether their risk tolerance aligns with concentrated TSMC positioning or whether they prefer broader semiconductor supply chain exposure that includes but is not dominated by a single company.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Taiwan semiconductor stocks include companies like TSMC, MediaTek, United Microelectronics Corporation, and ASE Technology, which together form the backbone of global chip supply. TSMC alone accounts for over 40% of Taiwan's entire equity market and manufactures chips for Nvidia, Apple, and other major technology companies, making Taiwan semiconductor exposure highly relevant to any investor with technology or AI infrastructure allocations.

Taiwan's Financial Supervisory Commission raised the single-stock concentration cap for domestic equity funds from 10% to 25% for any company exceeding 10% of the Taiwan Stock Exchange's weighting, effective 24 April 2026. TSMC is currently the only company that qualifies, allowing fund managers to more accurately reflect its dominant index weight without breaching regulatory thresholds.

TSMC's market capitalisation of approximately NT$53.93 trillion (roughly US$1.71 trillion) accounts for over 40% of Taiwan's total equity market, making it one of the most concentrated single-stock positions in any major developed or emerging market index.

Cross-strait tensions between China and Taiwan are the primary factor constraining TSMC's valuation multiples, and escalation scenarios represent a material tail risk for investors. TSMC is actively diversifying production by committing $165 billion to expand Arizona operations, and a US-Taiwan trade agreement signed in January 2026 includes $250 billion in direct investments to build chip production capacity in the United States.

Investors should assess whether their risk tolerance aligns with the concentrated single-company exposure that comes with TSMC positioning, or whether they prefer spreading Taiwan semiconductor allocation across the supply chain via companies like MediaTek (chip design), United Microelectronics Corporation (foundry), and ASE Technology (assembly and testing). The regulatory change shifts concentration risk from the fund structure to the individual investor.