Why Taiwan Just Rewrote Fund Rules for Semiconductor Stocks

5 hrs ago

The Securities and Exchange Commission submitted a proposal to the White House’s Office of Management and Budget on 27 March 2026 that could end five decades of mandatory quarterly reporting for U.S. public companies. If finalised, the rule would establish semiannual reporting as the regulatory floor whilst preserving company discretion to continue quarterly filings, a shift SEC Chairman Paul Atkins has framed as removing “the agency’s thumb from the scales” to let market forces determine optimal frequency. President Trump first floated this idea during his initial administration in 2018, though it never advanced to formal rulemaking. This time, with political momentum and imminent OIRA clearance, the proposal is positioned to reshape disclosure rules that have governed American capital markets since 1970.

This analysis examines what the shift from mandatory quarterly to optional semiannual reporting would mean for market efficiency, corporate strategy, and investor access to timely financial information. The stakes are specific: institutional investors including Ken Griffin’s Citadel have signalled they may flag companies adopting semiannual reporting for position reduction, whilst the SEC estimates the change could reduce annual compliance burdens by $2.7 billion. Understanding the proposal’s mechanics, the opposition it faces, and the international precedents that inform the debate helps readers assess likely market responses before the regulatory comment period intensifies.

The proposal establishes semiannual reporting as the regulatory floor whilst preserving company discretion to continue quarterly filing. This is not an elimination of disclosure obligations. It is a shift in who decides reporting frequency.

Three disclosure obligations would remain mandatory regardless of reporting frequency choice:

Quarterly reporting has been mandatory since 1970. The proposal submitted to OIRA on 27 March 2026 would change the regulatory mandate but not prevent companies from voluntarily maintaining quarterly updates. SEC spokesperson Ben Watson characterised this as a market-driven approach: allowing “the market to dictate the optimal reporting frequency based on factors such as the company’s industry, size, and investor expectations.”

Public companies face specific compliance timelines when exchange listing standards are breached. The Nasdaq equity deficiency procedures require companies to submit credible remediation plans within approximately 45 days of notification, with potential extensions to allow time for capital raises or asset restructuring before delisting proceedings commence.

Quarterly reporting has been mandatory since 1970, following the SEC’s transition from semiannual reporting requirements instituted in 1955. The SEC Division of Corporation Finance analysis of quarterly reporting requirements provides the regulatory history showing how the Securities Exchange Act of 1934 evolved to mandate quarterly Form 10-Q filings, a framework later reinforced by Sarbanes-Oxley management certification requirements.

The distinction between regulatory floor and market practice becomes critical for assessing how companies and investors will actually respond. A company adopting semiannual reporting would still face real-time disclosure obligations for material events and annual comprehensive filings. What changes is the cadence of interim financial updates.

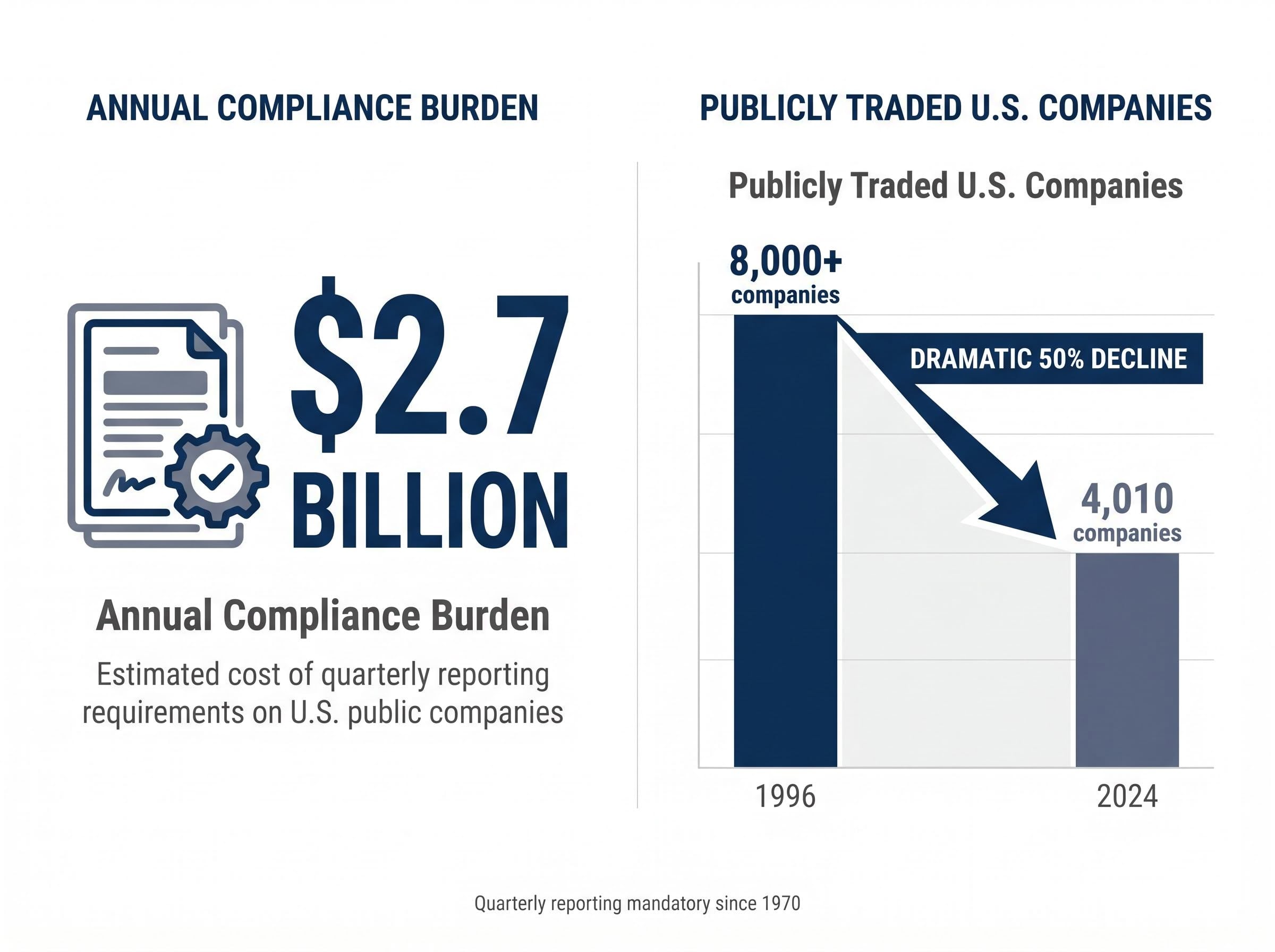

The compliance burden argument rests on specific cost estimates. The SEC has cited a $2.7 billion annual compliance burden that quarterly reporting requirements currently place on public firms.

Annual Compliance Burden The SEC estimates quarterly reporting costs U.S. public companies $2.7 billion annually in direct preparation costs, legal review, audit fees, and opportunity costs from management time diverted to compliance.

This figure encompasses direct costs of financial statement preparation and audit review, costs of maintaining compliant internal control structures, legal review expenses, and opportunity costs represented by management time diverted from strategic business activities to compliance management. For smaller public companies lacking centralised financial control infrastructure, these compliance costs represent a proportionally larger burden relative to total market capitalisation and resources.

Companies with strengthened balance sheets and reduced capital market dependencies increasingly view SEC deregistration as a cost reduction strategy. Westpac’s May 2026 voluntary deregistration demonstrates how firms can preserve US market access through Rule 144A exemptions whilst eliminating Form 20-F compliance costs, a pattern that could accelerate if semiannual reporting becomes the regulatory floor.

The structural argument connects reporting frequency to the declining number of publicly traded U.S. companies. Publicly traded companies peaked at over 8,000 in 1996. Approximately 4,010 trade today as of 2024. This contraction has become a significant concern for policymakers, as fewer public companies may indicate reduced access to public capital markets for growth-stage enterprises.

The structural argument connects reporting frequency to the declining number of publicly traded U.S. companies, which peaked at over 8,000 in 1996 and fell to approximately 4,010 by 2024. Meketa Capital research on declining U.S. public company counts, drawing on World Bank and CRSP data, documents this contraction and analyzes contributing factors including the rise of private equity and regulatory compliance costs.

A Nasdaq white paper argued that quarterly obligations disproportionately burden small and mid-sized companies. Commissioner Hester Pierce has stated that “moving away from mandatory quarterly reporting could allow smaller companies to more effectively allocate their time and resources, both of which are limited.” The policy case frames reduced reporting frequency as addressing a specific barrier that may discourage IPO activity among smaller firms.

The short-termism concern posits that quarterly earnings pressure may distort management decision-making. When companies face pressure to deliver consistent quarterly earnings that meet or exceed analyst expectations, management may optimise near-term reported earnings potentially at the expense of long-term value creation. Academic evidence on this question is complex, with research showing that quarterly reporting contributes to both market stability and potentially short-term thinking by firms.

Institutional investor opposition has emerged before the formal comment period opens. A cohort including billionaire Ken Griffin’s Citadel has been working behind the scenes to convey concerns. Fidelity and other major asset managers have joined this effort. The Managed Funds Association has contended that eliminating quarterly reporting could undermine market efficiency and investor confidence.

The market efficiency argument rests on information asymmetry. Less frequent reporting means investors must extrapolate further into uncertainty. When information is released semiannually rather than quarterly, investors face greater difficulty estimating firm value between disclosure dates. This uncertainty can translate into higher cost of capital as investors demand risk premiums to compensate for information risk, increased volatility at earnings announcement dates as markets incorporate six months of accumulated information adjustments in a single event, and wider bid-ask spreads as uncertainty about firm performance increases.

The SEC investor advisory committee heard warnings from buy-side firms in March 2026. Active managers indicated they would flag companies switching to semiannual reporting as candidates for position reduction or valuation reassessment.

Investor Response Signal “Quarterly reporting may become optional, but for companies aiming to maintain trust, secure stable access to capital, and manage market expectations, it will remain a practical necessity,” according to market commentary from active managers assessing the proposal’s implications.

If major asset managers follow through on reducing positions in companies that adopt semiannual reporting, the cost savings from reduced compliance could be offset by higher capital costs. This creates a practical calculation that corporate boards must weigh.

Index classification changes can trigger billions in passive fund rebalancing within compressed timeframes. Indonesia’s experience with MSCI review procedures demonstrates how index providers evaluate market accessibility, free float liquidity, and governance structures, with classification downgrades often producing concentrated selling pressure during reconstitution windows.

Specific actions investors have signalled include flagging companies for position reduction, removal from certain portfolios, and valuation reassessment that assumes higher information risk. The mechanism is straightforward: if a company reduces reporting frequency, institutional investors may apply a valuation discount to compensate for reduced information flow.

Corporate boards may find cost savings difficult to justify when weighed against higher risk perception from the investor base. A $500,000 annual saving in compliance costs becomes less compelling if it triggers a 2% valuation discount on a $500 million market capitalisation, representing $10 million in shareholder value.

The United Kingdom operates with semiannual reporting as the primary disclosure framework for public companies. This international precedent demonstrates that a major capital market can function with less frequent mandatory disclosures. Canada adopted a pilot programme on 19 March 2026, providing more recent evidence of how semiannual regimes can be structured.

Canada’s pilot programme is voluntary and limited to venture issuers with under $10 million revenue. Eligible issuers must have been reporting for at least 12 months with clean compliance records. The programme exempts first and third quarter reporting obligations in favour of semiannual reporting, reflecting a judgement that smaller companies face disproportionate compliance burdens whilst larger, more actively traded companies should maintain more frequent reporting.

The Canadian framework permits issuers to elect to withdraw from the semiannual reporting pilot and resume full quarterly reporting obligations for subsequent periods. This provides flexibility and an off-ramp for companies that conclude quarterly reporting serves their needs or investor preferences. The comment period, which closed in December 2025, revealed generally supportive sentiment. Many commenters agreed that quarterly reporting imposes a disproportionate burden on smaller venture issuers and may not yield meaningful disclosure benefits for investors.

Hong Kong, Japan, and Australia also operate with semiannual reporting frameworks, though specific regulatory structures vary.

| Jurisdiction | Mandatory Frequency | Key Features |

|---|---|---|

| United States (current) | Quarterly | Form 10-Q quarterly, Form 10-K annual, Form 8-K material events |

| United Kingdom | Semiannual | Interim and annual reports with real-time material event disclosure |

| Canada (pilot) | Semiannual (voluntary) | Limited to venture issuers under $10M revenue with clean compliance history |

| Hong Kong | Semiannual | Interim and annual accounts with prescribed content and timing rules |

International precedents demonstrate that semiannual reporting can function in major markets without catastrophic dysfunction. However, the Canadian model’s targeted, voluntary approach with quality controls suggests that wholesale adoption across all U.S. public companies may not be the only implementation path.

Large, widely followed companies like JPMorgan will likely maintain quarterly reporting as a market norm even without regulatory mandate. JPMorgan has stated it would continue quarterly guidance through analyst and investor conference calls regardless of rule changes. This commitment from one of the largest financial institutions signals that market-driven forces may sustain quarterly reporting for major companies.

Markets react sharply to quarterly guidance updates even when backward-looking results meet expectations. Netflix’s Q1 2026 experience, where shares fell nearly 12% despite a revenue beat, demonstrates how forward-looking commentary in quarterly reports drives valuation adjustments that semiannual reporting would compress into less frequent but potentially more volatile repricing events.

The practical outcome may be a bifurcated market: large caps maintaining quarterly updates whilst smaller companies and certain sectors exercise flexibility. Company characteristics suggesting likely adoption of semiannual reporting include:

Biotechnology companies face specific pressures that make semiannual reporting attractive. Quarterly reports can overemphasise cash burn and near-term clinical trial results in ways that distort investor understanding. Biotech companies face restrictions on commenting about FDA interactions quarterly, as such commentary is generally regarded as prejudicial to regulatory outcomes.

Biotech-Specific Benefits “Quarterly earnings calls are generally a bad idea for biotechs, with rare exceptions,” according to Jordan Stuart’s analysis of biotech investor relations practices. Stuart noted that biotech firms should consider hosting only one quarterly earnings call per year to coincide with full-year results, suggesting the semiannual option could align better with biotech business models.

Some investors note that even smaller firms might prefer quarterly reporting to offset declining analyst coverage of small-cap stocks. When sell-side coverage is thin, voluntary quarterly updates become a mechanism for maintaining investor awareness and market liquidity.

Investors would need to adjust their monitoring and due diligence processes depending on which companies they hold. A portfolio mixing large-cap quarterly reporters with small-cap semiannual reporters would require differentiated information-gathering strategies.

The regulatory process follows established rulemaking procedures. Expected phases include:

The proposal was submitted to OIRA on 27 March 2026. Typical OIRA reviews complete faster than the 90-day maximum, suggesting formal proposal release could occur imminently. If the current timeline holds and the proposal releases for comment in April 2026, the SEC would likely vote on a final rule in late 2026 or early 2027.

Transition periods for major SEC rule changes are typically measured in years, not months. This phased compliance approach would allow companies to modify financial reporting systems, investor relations strategies, and audit procedures in an orderly fashion. Compliance dates could potentially extend into 2027 or beyond, giving companies substantial lead time to assess whether semiannual reporting serves their specific circumstances.

Companies should conduct forward-looking analysis of their specific reporting needs and investor preferences regardless of regulatory outcome. Even if the proposal does not proceed as anticipated, the regulatory debate itself has shifted market expectations. Companies developing strategies for a more flexible reporting environment will be better positioned whether the proposal advances as anticipated, faces substantial revision, or triggers a hybrid approach where light quarterly updates pair with deeper semiannual filings.

The regulatory debate itself has value: forcing companies, investors, and policymakers to articulate what quarterly reporting actually provides and whether its costs justify its benefits.

The proposal represents a shift in decision-making authority from regulator to market, not an elimination of disclosure. Form 8-K material event obligations, annual Form 10-K filings, and semiannual interim reports would persist. What changes is who decides whether quarterly interim updates serve a company’s specific circumstances.

The outcome depends on the intensity of investor opposition during the comment period and whether the SEC incorporates modifications. Institutional investors have signalled specific concerns about information asymmetry and valuation risk. If these concerns translate into formal comment submissions with supporting data, the SEC may revise the proposal to include carve-outs, extended transition periods, or quality controls similar to Canada’s pilot programme structure.

Market forces may sustain quarterly reporting as a norm for large companies even if the regulatory mandate disappears. JPMorgan’s commitment to continue quarterly guidance regardless of rule changes demonstrates that competitive dynamics and investor expectations can enforce disclosure practices independent of regulatory floors. The bifurcation that emerges, with large caps maintaining quarterly updates whilst smaller companies exercise semiannual flexibility, would create a more complex information environment requiring differentiated investor monitoring strategies.

Readers should monitor the SEC’s formal proposal release and public comment period. Stakeholder submissions will shape whether the final rule resembles the current proposal or incorporates significant modifications addressing market efficiency concerns, capital cost implications, and sector-specific considerations that have emerged during the pre-release debate.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Semiannual earnings reporting means companies publish interim financial results every six months rather than every three months. Under the SEC's 2026 proposal, semiannual reporting would become the regulatory floor, meaning companies could choose to continue quarterly filings voluntarily, but would no longer be required to do so.

The SEC estimates that mandatory quarterly reporting currently costs U.S. public companies approximately $2.7 billion annually in preparation costs, legal review, audit fees, and management time, meaning semiannual adoption could substantially reduce that burden, particularly for smaller firms.

Major companies are unlikely to abandon quarterly reporting even if the regulatory mandate is removed. JPMorgan has publicly committed to continuing quarterly guidance through analyst and investor conference calls regardless of any rule changes, signalling that market forces may sustain the quarterly norm for large-cap firms.

Form 8-K real-time material event disclosures and annual Form 10-K filings would remain mandatory, so investors would still receive timely notice of major events like acquisitions or executive changes. However, investors would need to extrapolate further between formal interim updates, which institutional managers warn could increase information asymmetry and valuation risk.

The proposal was submitted to the White House Office of Management and Budget on 27 March 2026, with a formal SEC vote for public comment anticipated in April 2026. Following a comment period and SEC review, a final rule vote could occur in late 2026 or early 2027, with transition periods likely extending compliance dates into 2027 or beyond.