Washington Charges 38 Entities in $10M AI Crypto Fraud Sweep

7 hrs ago

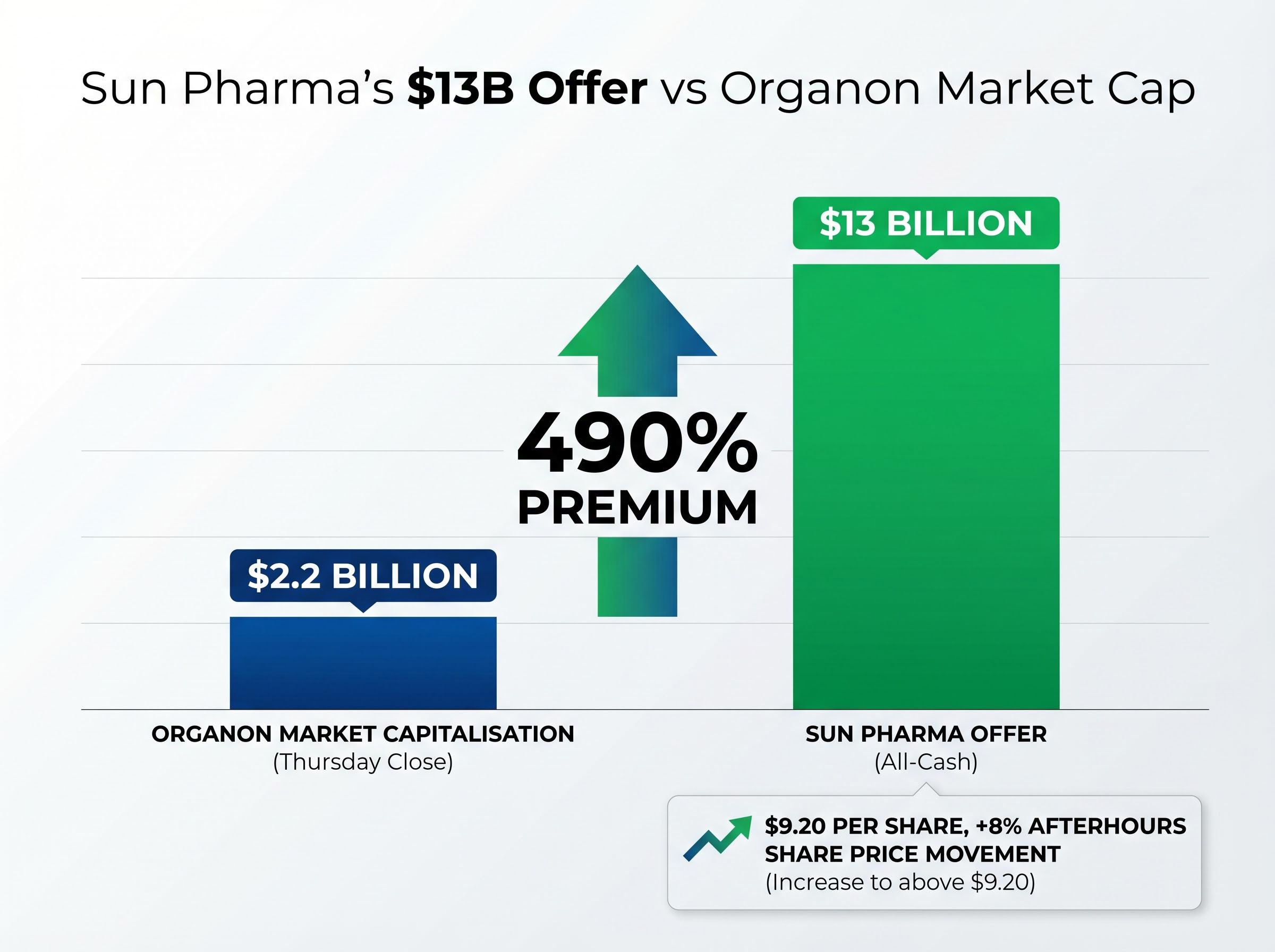

Sun Pharmaceutical Industries has submitted a reported $13 billion all-cash binding offer for Organon & Co (NYSE: OGN), the US-based women’s healthcare company spun from Merck in 2021. The bid represents a premium of approximately 490% to Organon’s $2.2 billion market capitalisation at Thursday’s close, and shares climbed 8% in afterhours trading to above $9.20. Germany’s Gruenthal is also pursuing the target, creating a competitive dynamic that raises both deal value potential and completion uncertainty.

This analysis examines what the bid structure reveals about Sun Pharma’s strategic repositioning, why women’s healthcare assets command premium valuations, and what the competitive bidding signals for investors monitoring cross-border pharmaceutical M&A.

The bid’s scale establishes Sun Pharma’s willingness to deploy significant capital for strategic transformation. At $13 billion against a $2.2 billion market cap, the implied premium is aggressive by any standard. What the structure reveals is equally telling.

Deal Structure $13 billion all-cash offer with no equity consideration, financed through a consortium including JP Morgan, MUFG, and Citi.

The absence of equity signals Sun Pharma’s preference for full operational control rather than a partnership structure. All-cash deals eliminate dilution risk for acquirer shareholders and remove the valuation uncertainty equity consideration introduces. Securing commitments from three major global banks adds credibility to financing capability, addressing a key risk factor in cross-border deals of this magnitude.

The all-cash structures eliminating dilution risk for acquirer shareholders remain attractive in specialty pharma M&A where target shareholders prefer immediate liquidity to equity consideration tied to integration execution.

Financing consortium:

This positions within Sun Pharma’s (NSE: SUN) broader evolution from generic drug manufacturer to specialty pharmaceutical player. The company has historically competed on pricing and volume in off-patent markets. Acquiring Organon’s branded women’s health portfolio shifts that calculus toward margin expansion and therapeutic specialisation, categories where Sun Pharma has limited existing presence.

Women’s healthcare operates with structural characteristics that make portfolios defensible and commercially predictable. Patient loyalty runs higher than in acute-care therapeutics. Prescription continuity persists across product lifecycles. Regulatory barriers to generic entry remain substantial in contraceptive, hormone therapy, and fertility treatment categories where clinical endpoints and safety profiles require extensive validation.

Organon’s portfolio positions as a platform rather than a collection of individual products. The company holds marketed assets across contraception, fertility, biosimilars, and established brands in hormone therapy. Acquirers view this as an integrated commercial infrastructure with existing physician relationships, distribution networks, and regulatory approvals that would take years to replicate independently.

Acquiring a single drug asset requires building commercial infrastructure around it. Acquiring a portfolio delivers that infrastructure already operational. Manufacturing synergies compound the value when production facilities can support pipeline expansion beyond current marketed products. This integration potential explains why platform acquisitions command premiums over sum-of-parts valuations in pharmaceutical M&A.

The broader trend shows branded specialty assets commanding higher multiples than commodity generics. Buyers pay for durability, and women’s health portfolios demonstrate prescription persistence that acute-care categories rarely match.

Key defensibility characteristics:

Germany-based Gruenthal is also reportedly pursuing Organon, creating a competitive bidding situation that introduces both upside potential and completion risk. Both bidders find the same strategic assets attractive: the women’s health portfolio and US manufacturing facilities that provide FDA-compliant production capacity and supply chain positioning.

Competitive bidding typically extends deal timelines as targets evaluate multiple proposals and bidders conduct confirmatory due diligence. Price negotiations intensify when a second credible party validates asset value. Completion probability becomes harder to assess because either bidder withdrawing, regulatory concerns emerging, or financing conditions shifting can derail transactions that appeared certain weeks earlier.

The 8% afterhours price move suggests the market assigns meaningful probability to deal completion, but the gap between current trading levels and the implied offer value per share indicates investors are pricing execution risk and the possibility of bid revisions.

| Bidder | Headquarters | Strategic Focus | Apparent Motivation |

|---|---|---|---|

| Sun Pharma | India | Specialty pharma expansion | US manufacturing, branded portfolio, women’s health platform |

| Gruenthal | Germany | Therapeutic diversification | Women’s health assets, US market access, production facilities |

Manufacturing attraction US production facilities provide FDA-compliant manufacturing capacity, a critical asset for companies seeking to expand American market presence without multi-year facility development timelines.

The pattern of emerging market pharmaceutical companies acquiring Western assets reflects specific economic logic. Indian pharma groups seek market access beyond generics, manufacturing capabilities that meet Western regulatory standards, and branded portfolios that command pricing power. Organon delivers all three.

Cross-border integration carries operational and regulatory complexity that domestic deals avoid. Integrating a US-based company into an Indian parent structure requires navigating different accounting standards, regulatory reporting obligations, and labour market conditions. Sun Pharma has reportedly stated plans for full integration rather than operating Organon as a standalone subsidiary, an approach that maximises cost synergies but increases execution risk.

McKinsey analysis of Asian biopharma cross-border integration challenges identifies policy alignment, capital deployment efficiency, and talent retention as critical success factors when emerging market acquirers pursue Western targets, operational hurdles that Sun Pharma’s full integration approach must navigate to capture the cost synergies the all-cash structure implies.

Key drivers of emerging market pharma acquiring Western assets:

US manufacturing presence matters beyond production capacity. FDA compliance requires continuous process validation, quality systems documentation, and inspection readiness that many emerging market facilities lack. Acquiring operational US plants bypasses a multi-year approval pathway and provides immediate supply chain reliability for American customers.

Acquirers value operational US plants because pre-commercialisation manufacturing agreements with established FDA-compliant facilities bypass multi-year approval pathways and provide immediate supply chain reliability that emerging market manufacturers often lack.

Full integration approaches carry higher execution risk than maintaining acquired companies as standalone units. Operational systems must be harmonised. IT infrastructure consolidated. Workforce policies aligned across jurisdictions with different employment law frameworks. Regulatory filings updated to reflect new corporate structures. Each integration point introduces potential for disruption if execution falters.

The trade-off balances cost synergies against operational complexity. Standalone operation preserves existing workflows but forgoes procurement savings, duplicated overhead reduction, and manufacturing optimisation. Full integration captures those savings but requires flawless coordination across time zones, regulatory regimes, and corporate cultures.

Several concrete developments will determine whether this situation resolves favourably for current Organon shareholders. The gap between the $9.20 afterhours trading level and the implied $13 billion offer value per share represents the market’s assessment of deal completion probability and timing uncertainty.

The gap between Organon’s $9.20 afterhours trading level and the implied $13 billion offer value per share reflects secondary market valuations pricing execution risk, regulatory uncertainty, and the possibility of bid revision or deal collapse.

Catalysts to monitor:

The Hart-Scott-Rodino antitrust filing requirements mandate premerger notification to the FTC and DOJ for transactions exceeding statutory thresholds, with updated rules effective February 2025 imposing expanded disclosure obligations that increase regulatory review timelines for cross-border pharmaceutical acquisitions.

The afterhours price movement to above $9.20 per share prices in acquisition probability but remains well below the per-share value implied by a $13 billion enterprise value offer. That spread quantifies execution risk, regulatory uncertainty, and the possibility of either bid revision or deal collapse.

Investors holding positions or considering entry need to monitor these catalysts as binary events. A formal offer with board support typically compresses the spread between trading price and offer value. Regulatory objections or financing withdrawal can reverse gains rapidly.

For investors examining why strong earnings can coincide with share price declines, our deep-dive into post-earnings price disconnects explores how cash flow quality, valuation multiples, and macroeconomic headwinds influence market reactions independently of reported profit figures.

Sun Pharma’s reported $13 billion binding offer for Organon represents a strategic repositioning toward branded specialty pharmaceuticals, with the competitive dynamic against Gruenthal creating both upside potential through bidding escalation and downside risk through deal uncertainty. The 490% premium to market capitalisation signals aggressive valuation appetite, whilst the all-cash structure and global banking consortium financing demonstrate acquisition seriousness.

The coming weeks will clarify whether this becomes a formal offer with board endorsement, whether Gruenthal counters with a competing bid, and how regulators view a cross-border transaction of this scale in the women’s healthcare sector.

Investors should monitor financing confirmation, regulatory filings with US antitrust authorities, and formal statements from Organon’s board or either bidder as the situation develops.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Sun Pharmaceutical Industries has submitted a reported $13 billion all-cash binding offer for Organon & Co, representing approximately a 490% premium to Organon's $2.2 billion market capitalisation at the time of the bid.

Sun Pharma is seeking to reposition from generic drug manufacturing toward branded specialty pharmaceuticals, and Organon's women's health portfolio, US manufacturing facilities, and established distribution networks provide that platform without requiring years of independent development.

Germany-based Gruenthal is also reportedly pursuing Organon, creating a competitive bidding situation that could escalate the final transaction price but also introduces greater deal uncertainty and timeline delays.

Investors should monitor formal bid confirmation, Gruenthal's response, Hart-Scott-Rodino antitrust filings with US regulators, potential CFIUS review, financing confirmation from the JP Morgan, MUFG, and Citi consortium, and Organon's board recommendation.

The gap between Organon's trading price and the implied per-share value of the $13 billion offer reflects the market pricing in execution risk, regulatory uncertainty, and the possibility of bid revision or deal collapse before a transaction closes.