Software vs Semiconductor Stocks: Momentum or Value in 2026?

Key Takeaways

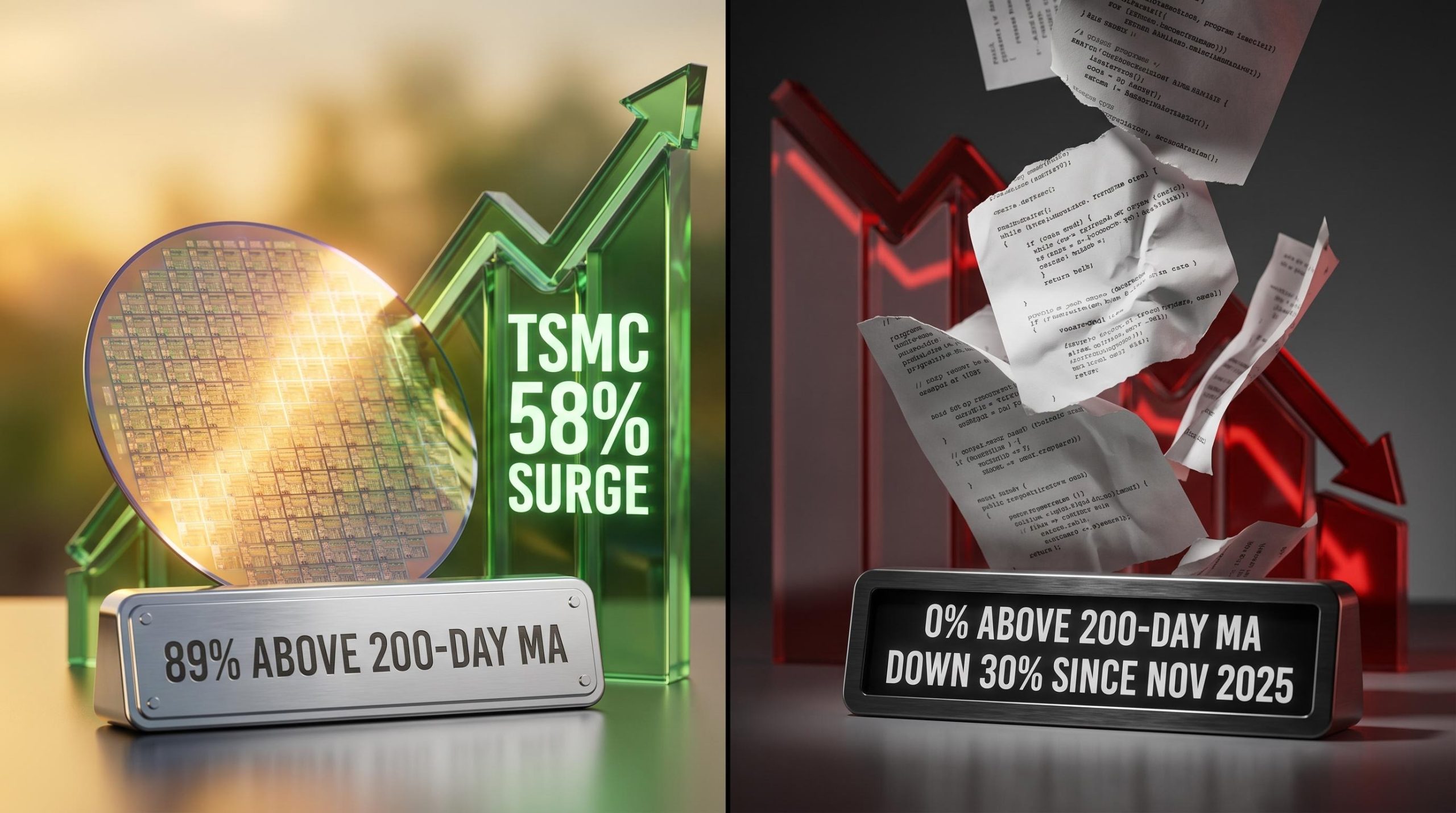

- Semiconductors and software stocks have reached a historic technical divergence, with 89% of semiconductor stocks above their 200-day moving averages versus 0% for S&P 500 software stocks in April 2026.

- TSMC's 58% Q1 2026 profit surge validates the AI infrastructure demand thesis underpinning semiconductor momentum, though a subsequent 3% share price decline highlights valuation risk at elevated levels.

- The IGV software ETF has dropped 30% since November 2025, driven by the AI ghost trade — institutional fears that AI tools will erode traditional software business models — creating deeply oversold conditions.

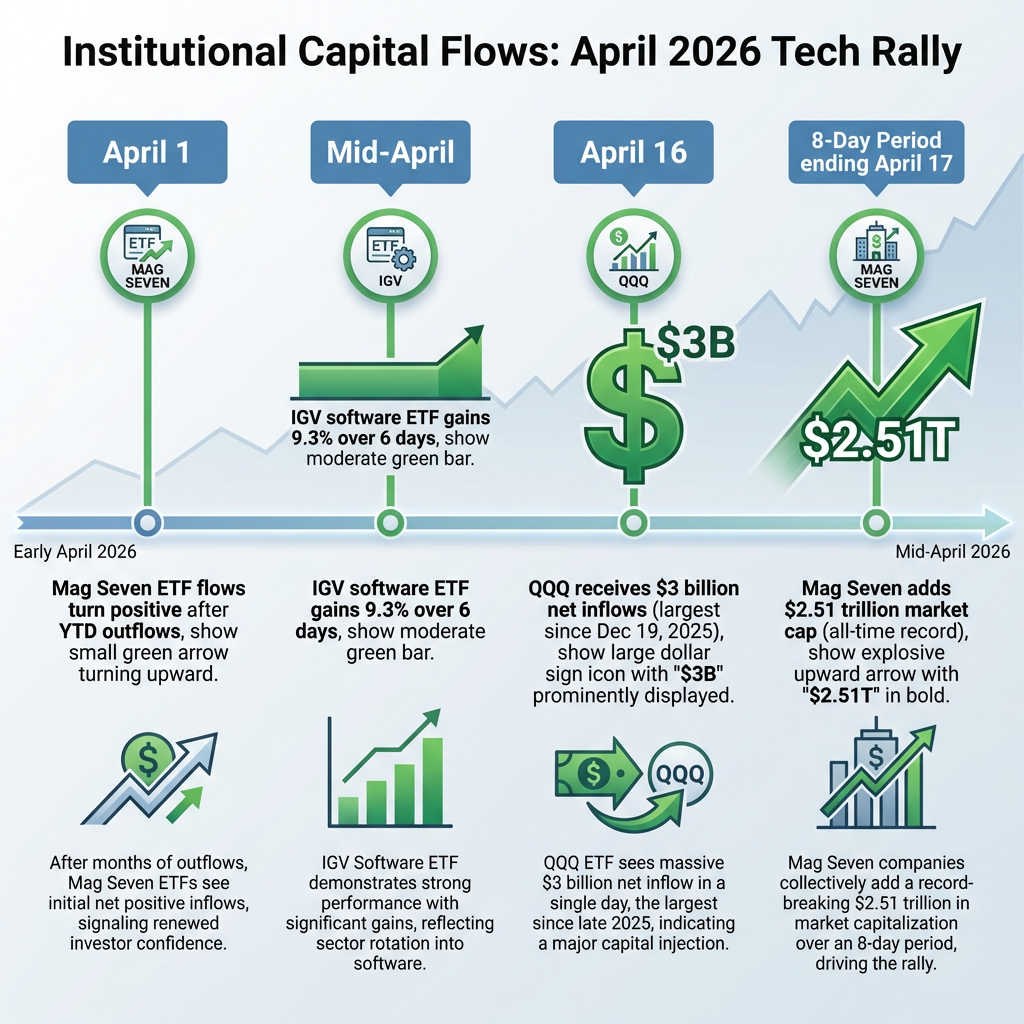

- A mid-April rebound saw IGV gain 9.3% over six days versus SMH's 5.3%, but Jefferies analyst Michael Toomey cautioned the move barely registers in long-term context with no earnings confirmation supporting the bounce.

- QQQ recorded $3 billion in single-day net inflows on 16 April 2026 and the Magnificent Seven added $2.51 trillion in market cap over eight days, signalling institutional capital returning to semiconductor-heavy mega-cap tech names.

Software vs semiconductor stocks have reached a historic divergence in April 2026, creating one of the most compelling momentum versus value debates in recent tech sector history. Semiconductors trade near all-time highs with 89% of stocks above their 200-day moving averages, while every S&P 500 software stock sits below this key technical level after a 30% drop since November 2025.

This extreme positioning presents investors with a critical choice. The semiconductor sector benefits from validated AI infrastructure demand, evidenced by TSMC’s 58% profit surge in Q1 2026. Meanwhile, software companies face existential concerns about AI eroding traditional business models, yet their deeply oversold conditions may offer contrarian value opportunities for patient investors.

A Historic Divergence Between Two Tech Sectors

The technical positioning between software and semiconductor stocks reveals a divergence not seen in decades. 89% of semiconductor and equipment stocks remain above their 200-day moving averages, trading near all-time highs with sustained momentum. In stark contrast, 0% of S&P 500 software stocks hold above this critical technical threshold.

The IGV software ETF has dropped 30% since November 2025, trading near April 2025 lows. This washout signals deep negative sentiment across the entire software sector. Semiconductors, meanwhile, maintain premium valuations driven by AI-related demand, with no signs of technical weakness.

| Metric | Semiconductor Stocks | Software Stocks |

|---|---|---|

| Stocks Above 200-Day MA | 89% | 0% |

| Performance Since November 2025 | Relatively flat, near ATH | Down 30% |

| Current Trading Level | Near all-time highs | Near April 2025 lows |

| Sentiment Indicator | Strong momentum, confidence | Capitulation, pessimism |

A mid-April rebound offered a glimpse of potential software recovery, with IGV gaining 9.3% over six days compared to SMH’s 5.3%. This 14.6-point performance gap favouring software marked a record for the period. However, analysts question whether this signals a sustainable turning point or merely a technical bounce from extremely oversold conditions.

When big ASX news breaks, our subscribers know first

Understanding the Momentum vs Value Divide

The software vs semiconductor stocks comparison exemplifies a classic momentum versus value investing framework. Momentum investors chase assets with strong recent performance and technical strength, favouring semiconductors’ position near highs. Value investors seek beaten-down assets trading below intrinsic worth, viewing software’s 30% decline as potential opportunity.

The empirically validated momentum versus value framework has been rigorously tested across global equity markets in peer-reviewed research published in The Journal of Finance, providing academic support for both strategic approaches in sector rotation decisions.

Stephanie Link of Hightower Advisors explicitly described software as the value play and semiconductors as the momentum trade in recent commentary. Understanding this framework proves essential for interpreting current market dynamics and aligning investment decisions with personal strategy.

What does it mean when 89% of semiconductor stocks are above their 200-day moving average?

This technical indicator signals strong sustained momentum across the semiconductor sector. When nearly nine out of ten stocks maintain positions above this long-term trend line, it demonstrates persistent investor confidence and uptrend durability. Price action above the 200-day moving average typically indicates institutional accumulation and positive sentiment.

The inverse positioning in software, where 0% of stocks hold above this threshold, signals widespread capitulation. Heavy selling has pushed every major software name into technical downtrends, suggesting weak hands have been shaken out and pessimism dominates sentiment.

Why do analysts call software stocks ‘washed out’?

The term ‘washed out’ describes conditions where prolonged, heavy selling has potentially exhausted downward pressure. Software’s 30% decline since November 2025 represents significant value destruction that may have removed speculative holders and weak positioning. This creates potential conditions for mean reversion when sentiment shifts.

Washed-out conditions don’t guarantee recovery. They simply indicate that selling pressure has been extreme, potentially setting up technical bounce opportunities when catalysts emerge or sentiment stabilises.

Neither momentum nor value approaches carry inherent superiority. Each strategy presents distinct risk-reward profiles that depend on investment timeframe, risk tolerance, and market conditions. The following sections examine the specific drivers behind each sector’s positioning.

Why Semiconductors Continue to Lead

Semiconductor momentum stems from sustained AI infrastructure spending showing no signs of abating. These companies occupy ‘picks-and-shovels’ positioning, profiting from foundational AI buildout regardless of which specific applications ultimately succeed. Analyst commentary consistently favours this structural advantage.

Official SIA industry forecasts project sustained double-digit revenue growth through 2025 driven primarily by data center and AI-related chip demand, providing authoritative industry-level validation for the semiconductor momentum thesis beyond individual company results.

> TSMC’s Q1 2026 profits surged 58% year-over-year on AI chip demand, providing concrete validation of the semiconductor demand thesis and supporting continued strength across Nvidia and peer companies.

While TSMC’s exceptional Q1 results validated the AI chip demand thesis with 58% profit growth, the subsequent 3% share price decline revealed how elevated semiconductor valuations create risk even when fundamentals exceed expectations. This dynamic highlights the complexity facing momentum investors in the sector.

Multiple demand drivers sustain semiconductor momentum beyond AI alone:

- AI compute acceleration across data centres and edge applications

- Cloud infrastructure expansion and capacity upgrades

- Automotive semiconductor content growth per vehicle

- Enterprise and hyperscaler data centre buildout programmes

Recent company performance demonstrates this broad-based strength. Marvell gained nearly 7% in mid-April trading, while AMD closed at $278.26, up 7.8%. Analyst picks including Micron, Sandisk, Applied Materials, and Lam Research are positioned for continued AI compute demand.

Memory chip manufacturers and equipment providers benefit particularly from ‘picks-and-shovels’ economics. These firms supply foundational components required across all AI implementations, insulating them from application-layer competition and providing diversified exposure to AI infrastructure growth.

Software’s Struggles and the AI Ghost Trade

Software faces what analysts term the ‘AI ghost trade’, where investors fear artificial intelligence will erode traditional software business models. This existential concern has driven the sector’s 30% decline since November 2025 and created what some institutional analysts describe as ‘uninvestable’ conditions.

The AI ghost trade concerns driving software weakness represent investor fears that AI will replace traditional software products. However, deeper analysis reveals limited evidence of actual business model disruption materialising across the sector, suggesting current pessimism may be overdone.

> Mizuho analyst Jordan Klein noted buy-side views of software as ‘uninvestable’, capturing the institutional sentiment driving persistent selling pressure across the sector.

The AI ghost trade represents differentiated downside risk compared to semiconductors. Where chip makers benefit from AI infrastructure spending, software companies face potential substitution, where AI tools replace rather than enhance traditional products. This structural uncertainty creates genuine valuation challenges beyond mere sentiment.

Dave Mazza of Roundhill Investments presented a contrarian perspective, noting Big Tech became substantially oversold. IGV’s mid-April gain in recent trading showed some buyers stepping in at deeply depressed levels. However, sustainability remains questionable.

Jefferies analyst Michael Toomey cautioned that mid-April momentum ‘barely registers’ in long-term context. With every S&P 500 software stock still below its 200-day moving average despite the bounce, technical damage remains severe. The rebound may represent temporary relief rather than trend reversal.

No post-mid-April earnings reports or guidance updates from major software firms are available to confirm whether fundamentals support the technical rebound. This data gap limits visibility into whether business performance validates buying at current levels or if further disappointments await.

The next major ASX story will hit our subscribers first

Institutional Flows and Market Positioning

While direct Q2 2026 fund flow data comparing software versus semiconductor exposure remains unavailable, indirect signals from ETF flows and analyst commentary reveal institutional preferences. These indicators suggest positioning favours semiconductors for momentum plays while software attracts primarily contrarian value seekers.

The Magnificent Seven ETF saw flows turn positive on 1 April 2026 after year-to-date outflows, with inflows accelerating through mid-April. This shift indicates institutional money returning to mega-cap tech names, many of which carry significant semiconductor exposure.

| Flow Indicator | Amount/Change | Date | Significance |

|---|---|---|---|

| QQQ net inflows | $3 billion | 16 April 2026 | Largest since 19 December 2025 |

| Mag Seven market cap gain | $2.51 trillion | 8-day period ending 17 April 2026 | All-time record for timeframe |

| Roundhill Mag Seven ETF | Flows turned positive | 1 April 2026 | Reversed year-to-date outflow trend |

QQQ received $3 billion in single-day net inflows on 16 April 2026, marking its largest inflow since $3.1 billion on 19 December 2025. This substantial capital movement suggests institutional conviction in technology broadly, though composition skews toward semiconductor-heavy names.

Retail investors have returned to names like Tesla according to Vanda Research, indicating broadening participation. However, broader market recaps show semiconductors pressing technical breakouts while software lags, implying institutional caution and underweight positioning in software relative to semiconductors.

The Magnificent Seven added $2.51 trillion in market capitalisation over an eight-day period ending 17 April 2026, setting an all-time record for such a timeframe. This extraordinary wealth creation concentrated in mega-cap names with significant semiconductor and AI infrastructure exposure reinforces the momentum trade thesis.

This record-setting $2.51 trillion market cap expansion over just eight days concentrated wealth creation in mega-cap names with significant semiconductor exposure. Analysis of which specific Magnificent Seven stocks drove this historic rally reveals important insights about concentration risks and the sustainability of the momentum trade.

Key Considerations for Investors

The choice between software vs semiconductor stocks depends fundamentally on investment timeframe and risk tolerance. Neither sector presents a clear consensus trade. Semiconductors offer validated momentum but carry elevated valuation risk and crowded positioning. Software presents contrarian value opportunity but faces structural uncertainty from AI disruption.

Understanding frameworks for managing volatility across different investment approaches helps investors align sector decisions with their broader portfolio objectives and risk parameters, particularly important when choosing between momentum and value strategies in uncertain markets.

Semiconductor Stocks

Pros:

- Strong momentum with 89% of stocks above 200-day moving averages

- Validated AI demand evidenced by TSMC’s 58% profit growth

- ‘Picks-and-shovels’ positioning benefiting from AI infrastructure buildout

- Multiple demand drivers including cloud, automotive, and data centres

Cons:

- Elevated valuations following sustained rally to all-time highs

- Potential flush-out risk from crowded positioning at premium levels

- Limited upside if current pricing already reflects optimistic scenarios

- Vulnerability to any signs of AI spending deceleration

Software Stocks

Pros:

- Deeply oversold conditions with 0% of stocks above 200-day moving averages

- Potential mean-reversion opportunity after 30% decline since November 2025

- Heavy selling may have removed weak hands and speculative positioning

- Long-term value case supported by analyst commentary on washed-out levels

Cons:

- AI ghost trade structural concerns about business model erosion

- ‘Uninvestable’ institutional view limiting near-term capital inflows

- No fundamental confirmation from earnings supporting mid-April rebound

- Recovery sustainability questioned by analysts including Jefferies’ Michael Toomey

Momentum-oriented investors may favour semiconductors for continued AI infrastructure exposure and technical strength. Value-oriented investors may eye software for mean-reversion potential from extremely oversold conditions. The key distinction lies in time horizon and conviction around structural versus cyclical factors.

Monitoring upcoming earnings reports will prove critical for software fundamental confirmation. Any signs of AI spending pullback or demand deceleration could affect semiconductor momentum. Both sectors require active position management given the historic nature of their current divergence.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is the difference between software stocks and semiconductor stocks as investments?

Semiconductor stocks represent companies that design and manufacture chips used in AI, data centres, and devices, while software stocks represent companies selling applications and platforms. In April 2026, semiconductors are trading near all-time highs driven by AI infrastructure demand, while software stocks have fallen 30% since November 2025 amid fears AI will erode traditional business models.

Why have software stocks fallen so much in 2025 and 2026?

Software stocks declined 30% from November 2025, driven by the so-called AI ghost trade — investor fears that artificial intelligence tools will replace or substitute traditional software products, eroding revenue and business models. Mizuho analyst Jordan Klein noted that buy-side institutions have begun viewing software as 'uninvestable', contributing to persistent selling pressure.

Are semiconductor stocks still a good buy after their rally to all-time highs?

Semiconductor stocks retain strong momentum with 89% of stocks above their 200-day moving averages, supported by TSMC's 58% Q1 2026 profit surge and sustained AI infrastructure spending. However, elevated valuations and crowded positioning mean any signs of AI spending deceleration could expose downside risk even when fundamentals remain strong.

What does it mean when 0% of software stocks are above their 200-day moving average?

When no S&P 500 software stock holds above its 200-day moving average, it signals that the entire sector is in a technical downtrend, reflecting widespread capitulation and deeply negative investor sentiment. While this historically oversold condition can set up mean-reversion opportunities, it does not guarantee a recovery without fundamental catalysts.

Should I invest in software or semiconductor stocks right now?

The choice depends on your investment strategy: momentum-oriented investors may favour semiconductors for their validated AI demand and technical strength, while value-oriented investors may view software's 30% decline as a contrarian opportunity. Analysts caution that software's mid-April rebound lacks fundamental earnings confirmation, while semiconductors carry elevated valuation risk at current levels.