$1.5M Forex Scheme Hid Ponzi Structure, WA Director Admits

24 mins ago

A financial firm with a valid ASIC licence was using a fake Macquarie Bank bond prospectus to take money from retail investors. That licence no longer exists.

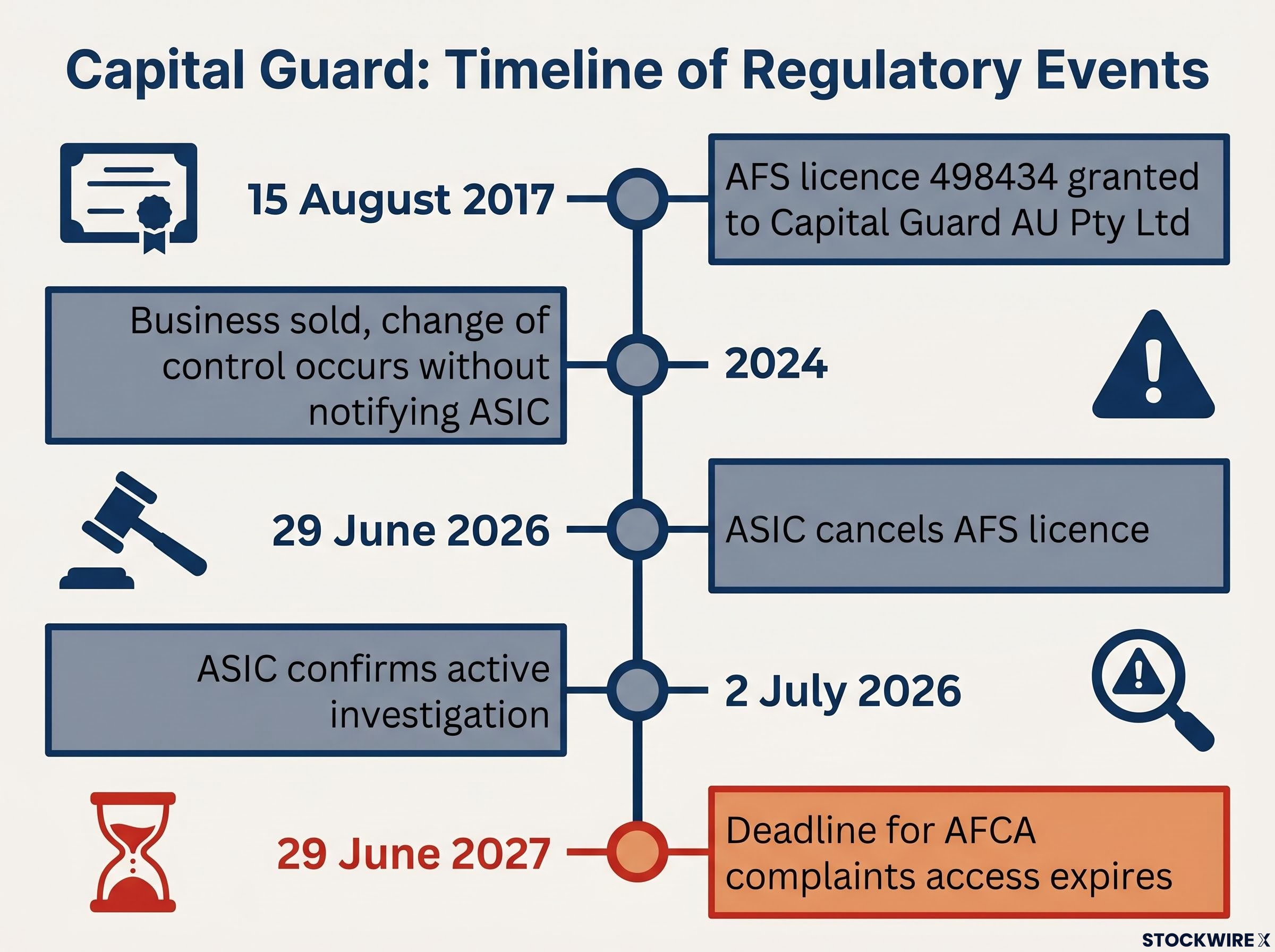

The Australian Securities and Investments Commission (ASIC) cancelled Capital Guard AU Pty Ltd’s Australian Financial Services (AFS) licence on 29 June 2026, three days ago. The cancellation followed findings of deliberate fraud across multiple fronts: a fabricated bond product, falsified documents submitted to an auditor, misleading website claims, and altered scam warnings. Retail investors handed over a combined total of no less than $100,000 to acquire a Macquarie bond that never existed.

What this case makes clear is how the architecture of a legitimate-looking firm can be built entirely on fabrication. Capital Guard held a valid AFS licence for nine years while constructing a scheme designed to exploit one of Australia’s most trusted bank names. Here is what ASIC found, how the fraud operated inside a licensed entity, and what affected investors need to do before a hard deadline closes the formal complaints window.

The centrepiece of the scheme was a bond product falsely attributed to Macquarie Bank. Capital Guard promoted and processed investments into this product using a fabricated prospectus bearing Macquarie’s name. Macquarie Bank had no involvement whatsoever. The product did not exist.

That detail matters. This was not a case of a firm misrepresenting the risks of a real investment. The prospectus itself was manufactured, engineered specifically to borrow the trust that Macquarie Bank’s brand carries with Australian retail investors.

The investing mistakes Australian beginners make most frequently include trusting product presentations from firms without independent verification of the underlying product, a vulnerability that fabricated prospectuses like the one at the centre of this case are specifically designed to exploit.

Investor funds totalling no less than $100,000 were channelled into a Macquarie bond product that had been entirely fabricated.

The bond fabrication was not an isolated act. ASIC identified four distinct categories of deceptive conduct:

ASIC’s assessment characterised the conduct as falling within both the misleading or deceptive and the dishonest categories under the Corporations Act 2001, findings that go well beyond a compliance failure and point to a deliberately constructed scheme.

The firm’s AFS licence, numbered 498434, was first granted on 15 August 2017 and remained in continuous force for nine years. The firm’s ACN is 168 216 742, and its registered address sits at Level 36, 1 Macquarie Place, Sydney. On paper, it looked like any other licensed financial services provider.

The licence remained active for nine years. But the people running the firm when the fraud occurred may not have been the people who originally obtained it.

In 2024, the financial services business then trading under the Capital Guard name was sold and passed into the hands of new operators. This was a change of control, and AFS licence conditions require licensees to notify ASIC when controlling ownership changes hands.

Capital Guard did not notify ASIC.

That failure created a regulatory blind spot. New operators were running a licensed entity without the regulator knowing who they were, what their intentions were, or whether they met the competency standards required of a licensee. The compliance failures that followed were consistent with this gap:

These were not isolated administrative oversights. They formed the operational environment in which the fraud operated, a licensed shell with none of the internal controls that a licence is supposed to guarantee.

The AFS licence cancellation took effect on 29 June 2026. Capital Guard has the option of challenging this decision before the Administrative Review Tribunal (ART) if it chooses to do so.

The cancellation does not, however, immediately sever every connection between the firm and its former clients. Certain licence obligations remain in force through to 29 June 2027, preserved by sections 912A(1)(g), 912A(2)(c), and 912B of the Corporations Act 2001. These provisions serve two specific protective purposes, and two only.

AFS licence cancellation is not a suspension or a conditional restriction; it is the immediate termination of a firm’s legal authority to provide financial services, which is why the residual provisions preserving AFCA access and compensation arrangements represent a narrowly constructed carve-out rather than business as usual.

| Licence status | Effective date | Permitted activity | Expiry |

|---|---|---|---|

| AFS licence cancelled | 29 June 2026 | No new financial services permitted | N/A |

| Residual provisions active | 29 June 2026 | AFCA complaints and compensation arrangements only | 29 June 2027 |

Under these continuing obligations, Capital Guard must keep its membership of the Australian Financial Complaints Authority (AFCA) active and must hold compensation arrangements in place for retail clients, including professional indemnity insurance cover.

Capital Guard cannot offer any new financial services or products under this residual status. It exists solely to keep the complaints and compensation pathway open.

The deadline that matters: AFCA access expires on 29 June 2027. Complaints lodged after that date lose the benefit of AFCA’s jurisdiction over this firm. That is twelve months from now.

If you placed funds with Capital Guard, particularly in connection with the “Macquarie bond” product, treat this as a fraud event and act in this order:

The existence of the professional indemnity insurance requirement in the residual provisions tells you something important: a formal compensation pathway may be available. That changes the situation from “this money is gone” to “there is a structured process worth pursuing.”

Scam warning: Fraud victims are frequently targeted by secondary “recovery” scam operators who contact them unsolicited and charge upfront fees to retrieve lost funds. AFCA and ASIC do not charge fees to investigate complaints. If someone asks you for money to get your money back, that is a second fraud.

Capital Guard was first granted AFS licence 498434 on 15 August 2017 and remained an authorised licensee throughout the period when the fraudulent conduct took place. A licence check would have returned a clean result.

That is the uncomfortable fact at the centre of this case. Licence verification is necessary, but it is not sufficient. A valid licence number confirmed that Capital Guard was authorised to provide financial services. It said nothing about whether the products being sold actually existed.

Investment scam losses across Australia reached $837.7 million in 2025 even as ASIC removed nearly 12,000 fraudulent websites, a scale that contextualises why fabricated prospectuses bearing trusted bank names remain an effective vehicle for fraud against retail investors.

The specific tactic of altering scam warnings tells you that a firm’s own reassurances about its regulatory standing are not a reliable source. When Capital Guard modified third-party warnings issued against it, the firm was actively managing the information environment around its own trustworthiness. Relying on the firm’s version of events was exactly what the scheme required.

Three verification habits would have changed the outcome here:

As of 2 July 2026, ASIC has confirmed that its investigation into Capital Guard continues to be active. Further regulatory or legal action may follow the licence cancellation.

ASIC’s Capital Guard licence cancellation release, published on 1 July 2026, confirms that the regulator classified the firm’s conduct as both misleading or deceptive and dishonest under the Corporations Act 2001, with investor funds of no less than $100,000 directed into a Macquarie bond product that had never existed.

For affected investors, the next twelve months are an active recovery window, not a waiting period. The 29 June 2027 expiry of AFCA access is the hardest deadline in this process, and every week that passes without a complaint lodged is a week less of the structured pathway that remains available.

Capital Guard retains the right to contest the cancellation before the Administrative Review Tribunal, which means the regulatory picture could shift. Investors should monitor ASIC’s media releases for updates and treat the AFCA complaint as the single most urgent step.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

ASIC found that Capital Guard promoted and sold a bond product falsely attributed to Macquarie Bank using a fabricated prospectus, submitted fraudulent documents to an external auditor, made false claims on its website, and doctored third-party scam warnings to obscure their severity. At least $100,000 in retail investor funds was channelled into a Macquarie bond product that never existed.

An AFS licence cancellation is the immediate termination of a firm's legal authority to provide financial services in Australia. For investors who dealt with Capital Guard, it means the firm can no longer offer any new financial services, but residual provisions keep its AFCA membership and compensation arrangements active until 29 June 2027, preserving a formal complaints and recovery pathway during that period.

The deadline is 29 June 2027. ASIC's residual licence provisions require Capital Guard to maintain AFCA membership and compensation arrangements until that date, after which the formal complaints window closes and AFCA loses jurisdiction over the firm.

The Capital Guard case shows that checking an ASIC licence number is necessary but not sufficient. Investors should also verify any product directly with the named issuer by calling the institution using a phone number sourced independently from its official website, and locate any third-party scam warnings from their original source rather than relying on the selling firm's own characterisation.

Affected investors should report to ASIC with all documentation, lodge a complaint with AFCA before 29 June 2027 (the most time-sensitive step), contact their bank's fraud team about potential fund recalls, and seek independent legal advice on civil recovery options. AFCA and ASIC both investigate complaints at no cost to the investor.