ASIC Fines Three ASX Companies $1.17m for Missing Annual Reports

11 hrs ago

Three companies delivered three completely different outcomes within 72 hours of each other during the week of 4-5 May 2026: an AI software firm that nearly doubled its US revenue, a major airline that shut down and stranded 600,000 passengers, and a meme-stock retailer that attempted to buy one of the world’s largest e-commerce platforms with roughly a fifth of the capital required. The stock market today reflected the tension between these competing signals. The ASX 200 closed at 8,729.80 on 4 May, up 0.74%, while the S&P 500 slipped 0.41% to 7,201 overnight. Brent crude surged to US$113.62 per barrel on Iran-related supply disruptions, and markets priced an approximately approximately 86% probability of the RBA lifting the cash rate to 4.35% at its 5 May meeting. What follows breaks down each of the three stories, explains the financial mechanics behind them, and identifies the investor lesson embedded in each.

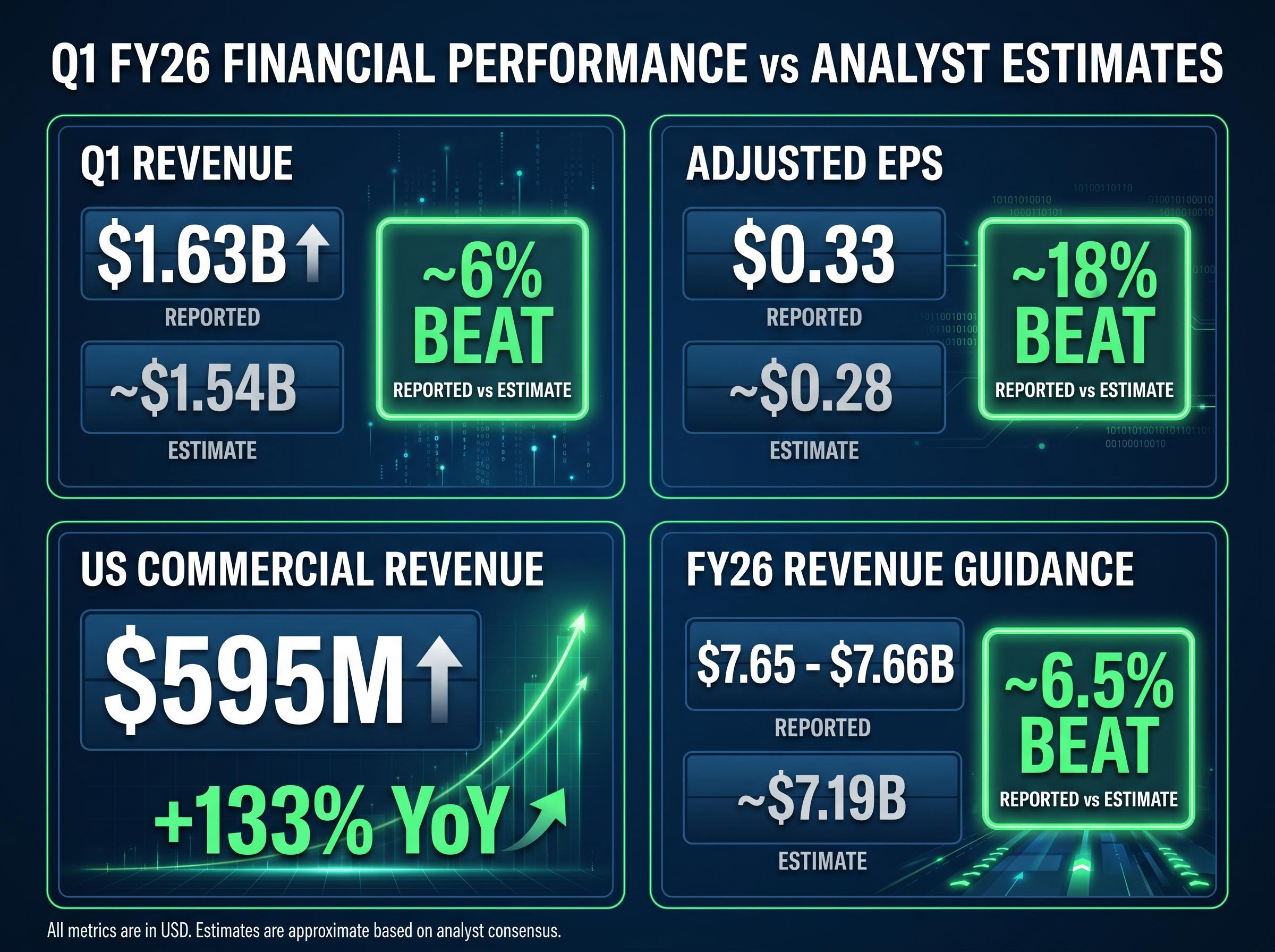

The numbers arrived first, and they were large enough to carry their own argument. Palantir posted Q1 FY26 revenue of $1.63 billion, an 85% increase year-over-year and approximately 6% above analyst consensus. Adjusted earnings per share came in at $0.33, beating estimates by roughly 18%.

The standout line was US commercial revenue: $595 million, up 133% year-over-year. That figure matters because it distinguishes Palantir from the government-contract-dependent business it was five years ago. US total revenue grew 104% year-over-year, with the commercial segment now the primary growth engine.

The raised guidance carried more weight than the beat itself. Palantir lifted its FY26 revenue outlook to $7.65-$7.66 billion, up from approximately $7.19 billion, and guided Q2 revenue to a midpoint of $1.80 billion versus consensus of $1.68 billion.

CEO Alex Karp signalled that the US business is expected to roughly double again in 2027, framing the current trajectory as an acceleration rather than a peak.

Broader demand signals corroborated the result. US factory orders for computers and electronics rose 3.6% to $29.6 billion in March 2026, the largest monthly total since 2001, reinforcing that AI infrastructure spending is translating into enterprise purchasing at scale.

| Metric | Reported Result | Analyst Estimate | Beat (%) |

|---|---|---|---|

| Q1 Revenue | $1.63B | ~$1.54B | ~6% |

| Adjusted EPS | $0.33 | ~$0.28 | ~18% |

| US Commercial Revenue | $595M | N/A | +133% YoY |

| FY26 Revenue Guidance | $7.65-$7.66B | ~$7.19B | ~6.5% |

Palantir sells data analytics and AI-powered decision software to enterprises and government agencies. Its revenue reflects clients paying for AI outputs, not Palantir investing in AI infrastructure. That distinction is worth pausing on, because most AI headlines in financial media describe spending, not earning.

When a hyperscaler announces a $30 billion data centre buildout, that is AI capital expenditure. It represents cost. When Palantir reports $595 million in US commercial revenue from AI-integrated software, that is AI-generated income. One category consumes capital in anticipation of future returns; the other has already converted AI capability into recurring revenue.

The scale of AI capital expenditure now running through the four largest hyperscalers, Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion in Q1 2026 alone, with full-year guidance reaching $725 billion, provides the clearest available benchmark for what Palantir is converting into revenue on the other side of the ledger.

US commercial revenue growing 133% year-over-year signals that private sector enterprises are now actively paying for AI-integrated software at scale. The March 2026 factory orders data (computers and electronics up 3.6%, the largest total since 2001) corroborates the demand pattern from the buyer side.

For Australian retail investors evaluating tech stocks, knowing which category a holding belongs to changes the valuation framework entirely. A company generating revenue because of AI is fundamentally different from one spending heavily on AI and hoping for future returns.

Spirit Airlines ceased operations on 2-3 May 2026. The shutdown stranded approximately 600,000 passengers and resulted in roughly 17,000 job losses, making it the first major US airline failure in approximately 25 years.

Approximately 600,000 passengers were stranded and 17,000 jobs were lost in a single operational shutdown, the largest US airline collapse in a generation.

The proximate cause was the failure of a US$500 million government bailout to sustain the carrier through its bankruptcy proceedings. The underlying causes were structural and had been visible for several quarters:

The investor lesson is direct. Government bailout expectations in distressed airline investing are unreliable, and once bankruptcy proceedings begin, equity holders are typically last in the recovery queue. For Australian investors with exposure to aviation or travel-related equities, the Spirit collapse illustrates why distressed airline stocks often appear cheap for legitimate structural reasons. The current oil price environment reinforces that fuel cost volatility remains an existential variable for low-cost carriers.

The Iran conflict economic cascade connects the fuel cost arithmetic directly to Spirit’s collapse: the Strait of Hormuz blockade removed approximately 10.1 million barrels per day from global supply, pushing Brent crude 48% above its pre-conflict baseline and destroying the recovery economics of any ultra-low-cost carrier still relying on pre-2025 fuel assumptions.

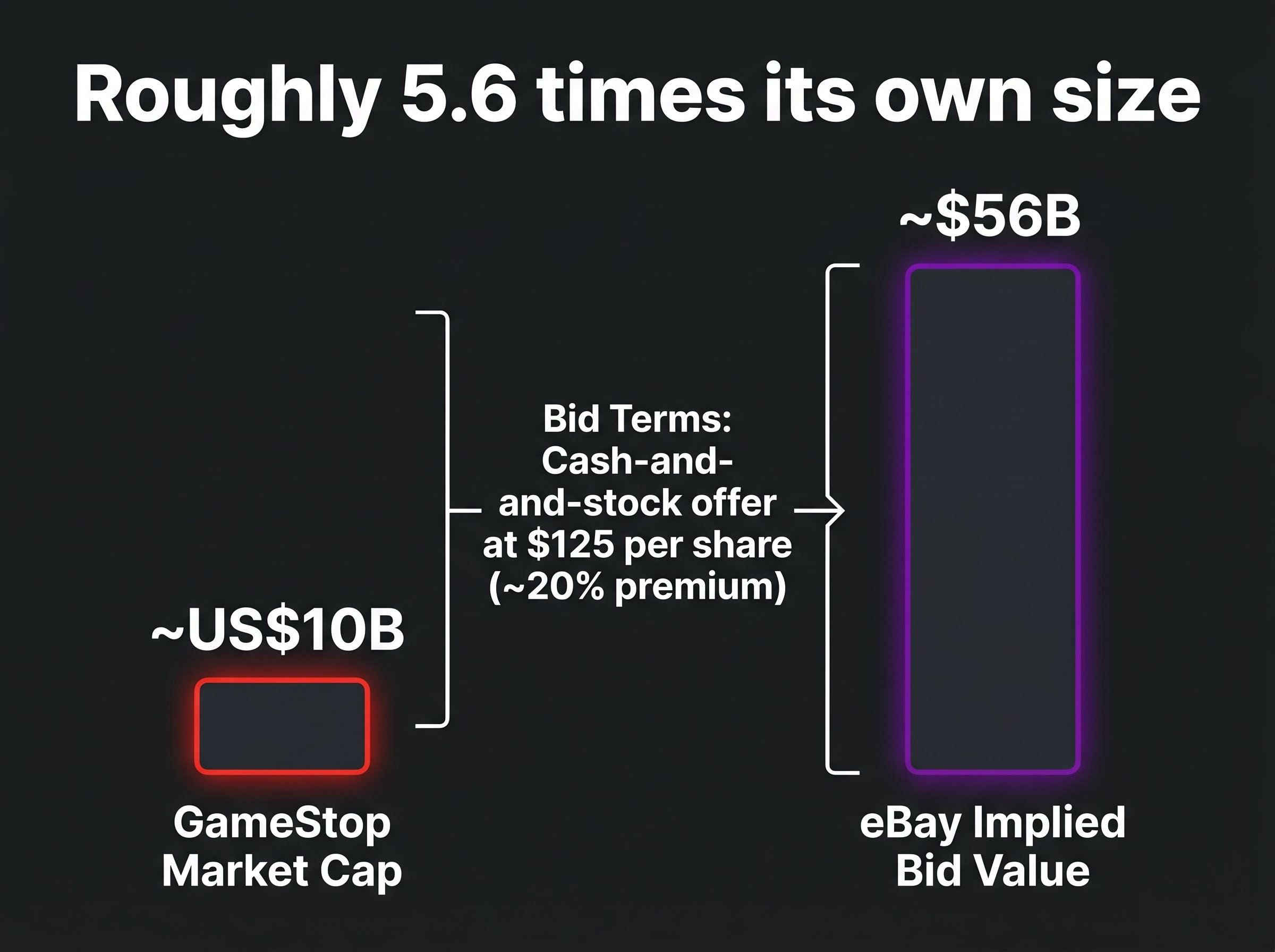

On 3 May 2026, GameStop, led by CEO Ryan Cohen, made an unsolicited cash-and-stock offer valuing eBay at approximately $56 billion ($125 per share), a roughly 20% premium to eBay’s prevailing share price.

GameStop’s own market capitalisation at the time of the bid: approximately US$10 billion.

That arithmetic is the story. GameStop proposed acquiring a company roughly 5.6 times its own size.

| Metric | GameStop | eBay (Target) | Bid Terms |

|---|---|---|---|

| Market Cap | ~US$10B | ~US$47B | Cash-and-stock offer |

| Offer Price Per Share | N/A | N/A | $125 |

| Implied Total Value | N/A | N/A | ~$56B |

| Premium to Market | N/A | N/A | ~20% |

An unsolicited bid is an acquisition offer made without the target company’s board having invited or agreed to it. A “cash-and-stock” structure means the bidder proposes to pay partly in cash and partly by issuing its own shares to the target’s shareholders, effectively diluting existing ownership to fund the deal.

When an undercapitalised acquirer makes an unsolicited bid of this kind, three outcomes typically follow:

For retail investors, the pattern matters because unsolicited bids can temporarily lift target stock prices as the premium gets priced in. Chasing those spikes in deals that are structurally unlikely to close has historically been a source of losses when the bid evaporates and the premium unwinds.

Investors wanting to map the specific financing arithmetic behind the offer will find our deep-dive into the GameStop funding gap covers the $9 billion cash position, the $20 billion TD financing commitment, the residual $26.5 billion shortfall, and the proxy contest escalation options GameStop retains ahead of eBay’s 17 June 2026 Annual General Meeting.

Each of the three stories represents a different category of corporate risk currently live in global markets: AI revenue validation, sector structural collapse, and speculative dealmaking. They arrived simultaneously, and collectively they offer a sharper picture than any one of them provides alone.

| Company | Story Type | Investor Lesson |

|---|---|---|

| Palantir | AI revenue validation | Distinguish AI earners from AI spenders; revenue inflection changes the valuation framework |

| Spirit Airlines | Structural collapse | Cheap airline stocks are often cheap for structural reasons; bailout expectations are unreliable |

| GameStop/eBay | Speculative dealmaking | Unsolicited bids by undercapitalised acquirers rarely close; avoid chasing target-stock premium spikes |

The Australian market context is not insulated from these developments. The ASX 200 closed at 8,729.80 on 4 May (up 0.74%), but the S&P 500 slipped 0.41% to 7,201 overnight. Brent crude at US$114 per barrel feeds directly into domestic inflation pressures. The AUD traded at 0.7208 against the US dollar.

Market pricing reflected approximately 80% probability of a 25 basis point RBA rate hike to 4.35% on 5 May 2026, meaning domestic rates are tightening into this offshore turbulence.

The actionable question: for each holding in a portfolio, which of these three risk categories does it belong to, and does its current valuation reflect that?

International ETF allocation among Australian retail investors crossed a structural threshold in Q1 2026, with international funds overtaking domestic ETFs as the most purchased category on record across the Selfwealth by Syfe platform, a shift accelerated by exactly the kind of offshore volatility that Palantir’s earnings result and Spirit’s collapse represent.

The three stories are not isolated incidents. They are indicators of durable market themes: AI monetisation credibility is being tested by real earnings cycles, aviation sector fragility persists under sustained fuel cost pressure, and speculative dealmaking continues even as credit conditions tighten. For Australian investors, the AUD at 0.7208, the imminent RBA decision, and Brent crude at US$114 are the domestic transmission channels through which these offshore stories arrive on local balance sheets. The next corporate earnings cycle will either confirm or complicate the AI revenue inflection story Palantir just evidenced, and investors who understand the distinction between AI spenders and AI earners will be better positioned to read it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—

AI revenue generators are companies that earn income directly from AI-enabled products, like Palantir which reported $595 million in US commercial AI revenue. AI capital spenders, such as hyperscalers, invest billions building AI infrastructure and hope for future returns, meaning their AI exposure shows up as cost before it appears in earnings.

Spirit Airlines ceased operations on 2-3 May 2026 after a US$500 million government bailout failed to sustain the carrier through bankruptcy, stranding approximately 600,000 passengers and eliminating around 17,000 jobs. Structural pressures including high fuel costs with Brent crude near US$114 per barrel, post-pandemic price competition from full-service airlines, and an accumulated debt load had weakened the business for several quarters before the final collapse.

On 4 May 2026, the ASX 200 rose 0.74% to 8,729.80 while the S&P 500 slipped 0.41% to 7,201 overnight, reflecting competing signals from strong AI earnings like Palantir's result against rising oil prices and tightening monetary policy. Markets were also pricing approximately 86% probability of an RBA rate hike to 4.35%, adding domestic pressure to the offshore volatility.

Unsolicited bids from undercapitalised acquirers typically end in one of three ways: the deal collapses when the bidder cannot prove financing capacity, the bidder revises terms significantly by bringing in outside financing, or the target uses the approach to attract better-capitalised competing buyers. Retail investors who chase the temporary premium spike in the target's share price often face losses when the bid evaporates and the premium unwinds.

Palantir reported Q1 FY26 revenue of $1.63 billion, up 85% year-over-year, with US commercial revenue growing 133%, demonstrating that AI-integrated software is generating real recurring income rather than just attracting capital expenditure. For Australian investors, this result illustrates that distinguishing between companies earning revenue because of AI and those spending on AI in anticipation of future returns is essential to applying the correct valuation framework.