Hormuz Shipping Collapses 52% as US-Iran Clash Sends Oil Surging

4 hrs ago

The ASX 200 surged 138.8 points on Friday 29 May 2026, delivering its strongest single-session gain in weeks as reports of a tentative 60-day US-Iran ceasefire extension swept through commodity and equity markets. The move nearly reversed the prior session’s losses in a single afternoon, with the benchmark closing at 8,731.7 and finishing the week at its intraweek high.

Advancing stocks in the S&P/ASX 300 outnumbered decliners by a ratio of 233 to 50. The Emerging Companies index surged 3.05%, while the Small Ordinaries and All Technology indices each added 2.28%, signalling broad-based participation rather than a narrow large-cap rally.

What follows breaks down the geopolitical catalyst behind Friday’s move, which sectors captured the rotation and which were left behind, the individual stocks that posted the session’s largest gains and losses, and what the week’s closing shape may signal for ASX investors heading into the weekend.

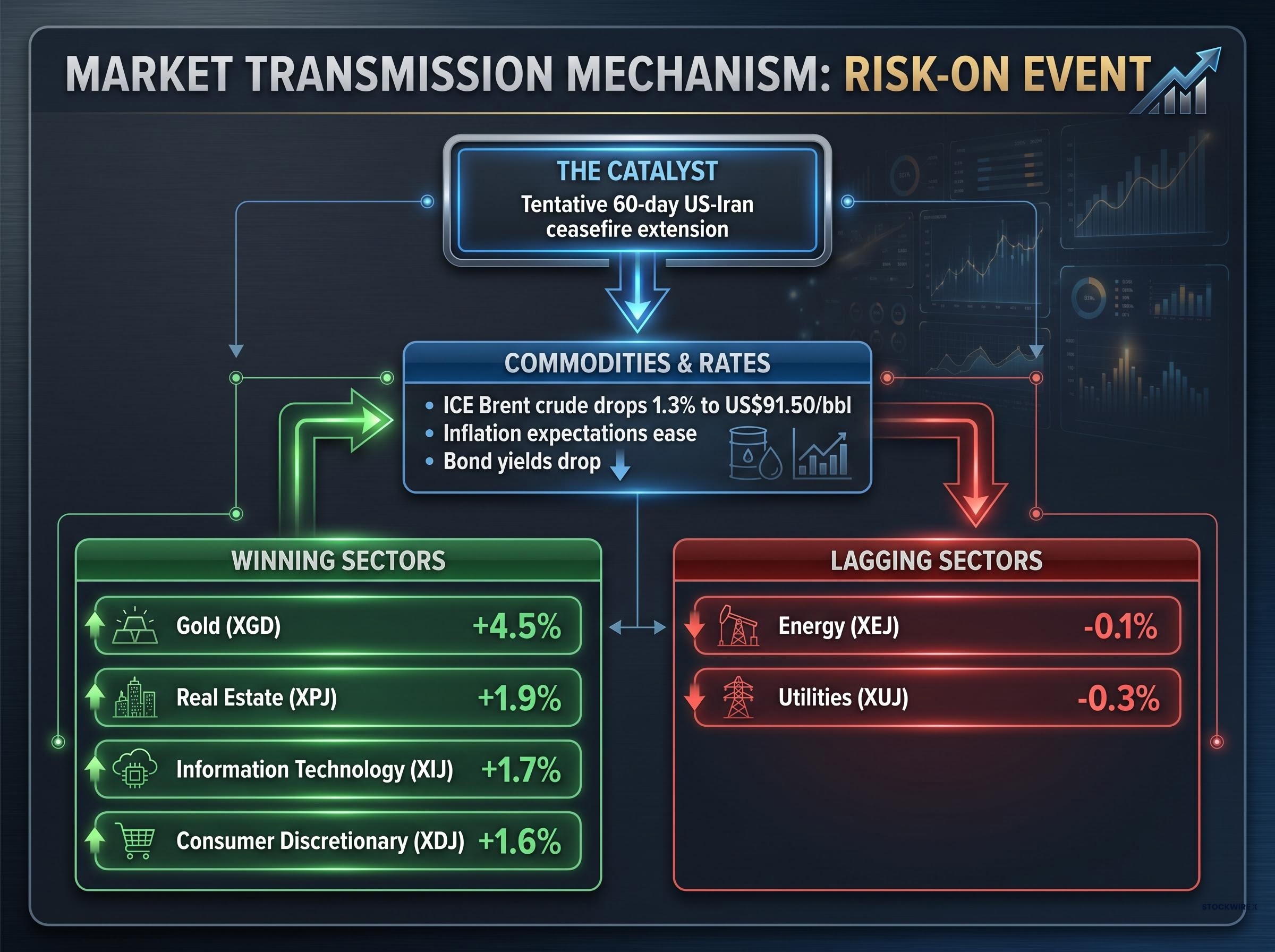

Reports of a tentative 60-day US-Iran ceasefire extension provided the session’s primary catalyst. The ceasefire was described as a market-moving report rather than a formally verified diplomatic outcome, and no official confirmation had been issued as of Friday’s close.

Reuters reporting on oil futures confirmed that crude prices fell on hopes for a potential deal to extend the US-Iran ceasefire, providing direct market context for the commodity-led transmission that drove Friday’s broad ASX rally.

The transmission mechanism from geopolitics to equity prices followed a clear sequence. Falling crude prices eased near-term inflation expectations, which pushed bond yields lower. Lower yields, in turn, reduced the opportunity cost of holding non-yielding assets like gold and compressed the discount rate applied to growth equities, lifting technology, real estate, and small-cap names simultaneously.

Friday’s session shares its structural template with the Iran relief rally of 19 May, when the ASX 200 gained 99.4 points on Trump stepping back from strikes; that session, however, was led by Consumer Staples and Financials rather than gold and materials, illustrating how the same geopolitical catalyst can produce different sector winners depending on which transmission channel dominates.

The ceasefire extension was described as tentative as of 29 May 2026, with no formal diplomatic announcement confirmed. Market pricing reflected the report’s implications, not a verified diplomatic outcome.

Key commodity and futures moves on the session:

The benchmark did not merely rally. It closed at its absolute session high of 8,731.7, and that high also marked the intraweek peak of the weekly candle. The weekly range spanned approximately 2.0% from low to high, with all of the closing strength concentrated at the top of that range.

For the week, the XJO gained 74.7 points, or 0.86%. Breadth confirmed the signal: 233 advancers versus 50 decliners across the S&P/ASX 300, with smaller names outperforming their large-cap counterparts by a wide margin.

| Index | Close | Change (pts) | Change (%) |

|---|---|---|---|

| S&P/ASX 200 (XJO) | 8,731.7 | +138.8 | +1.62% |

| All Ordinaries | 8,965.0 | — | +1.65% |

| Small Ordinaries | — | — | +2.28% |

| All Technology | — | — | +2.28% |

| Emerging Companies | — | — | +3.05% |

A session that closes at its peak on a weekly candle that also closes at its high is a pattern technically oriented investors treat as constructive for near-term momentum. The breadth data corroborates the signal by showing the move extended well beyond the large-cap benchmark.

Gold was the session’s standout sector story. The ASX Gold Sub-Index (XGD) advanced 4.5%, with the bond yield decline mechanism described above directly supporting non-yielding precious metals. The move recovered just over half of the prior session’s decline.

Top gold movers:

The broader Materials sector (XMJ) followed at +2.9%, with base metals and iron ore names rebounding sharply. Alcoa gained 4.6%, Sims added 3.6%, Sandfire Resources rose 3.4%, South32 climbed 3.0%, BHP added 2.9%, and Fortescue gained 2.4%.

Lithium stocks extended their recent run on rising commodity prices. GFEX lithium carbonate futures added 1.2% to CNY 179,740/tonne, while Australian spodumene concentrate rose 1.8% to US$2,610/tonne. Vulcan Energy surged 9.6%, PMET gained 6.6%, Elevra added 4.4%, Mineral Resources rose 3.8%, IGO climbed 3.6%, and Pilbara Minerals added 2.5%.

The lithium sector re-rating that pushed Liontown Resources, Pilbara Minerals, and Mineral Resources to 52-week highs in early May was driven by lithium carbonate averaging US$15,000 per tonne and 2.1 million Chinese EV sales in Q1 2026, providing the demand backdrop against which Friday’s spodumene and GFEX price moves should be read.

| Sector / Sub-Sector | Best Performer | Gain | Sector Move |

|---|---|---|---|

| Gold (XGD) | St Barbara | +10.6% | +4.5% |

| Materials (XMJ) | Alcoa | +4.6% | +2.9% |

| Lithium | Vulcan Energy | +9.6% | N/A (sub-sector) |

The breadth of named movers across gold, base metals, and lithium indicates a sector-wide re-rating rather than isolated stock-specific bounces.

Travel stocks rallied as ceasefire optimism raised the prospect of eased aviation disruption across the Middle East. Flight Centre surged 8.2% to $10.93, Virgin Australia gained 6.2% to $2.20, and Qantas added 3.2%, lifting the Consumer Discretionary sector (XDJ) by 1.6%.

Real Estate (XPJ) advanced 1.9% as falling bond yields restored the relative attractiveness of property trust distributions. Goodman Group and Abacus Storage King each rose 2.9%.

Information Technology (XIJ) gained 1.7%. Lower yields reduce the discount rate applied to high-growth, long-duration earnings, benefiting names like Siteminder (+6.7%), Megaport (+5.4%), Codan (+3.9%), and Macquarie Technology (+3.5%).

Energy (XEJ) slipped 0.1% as falling crude prices weighed directly on oil producers. Viva Energy dropped 1.9% to $2.12, Yancoal fell 1.7% to $6.77, and Beach Energy declined 1.4%.

Utilities (XUJ) shed 0.3%, with AGL Energy losing 0.8% as capital rotated away from defensive positioning.

The Financials sector recovered in absolute terms but underperformed the benchmark for a sixth consecutive session, a streak that investors monitoring domestic rate sensitivity may wish to note.

| Sector | Change (%) | Notable Mover | Individual Move (%) |

|---|---|---|---|

| Consumer Discretionary (XDJ) | +1.6% | Flight Centre | +8.2% |

| Real Estate (XPJ) | +1.9% | Goodman Group | +2.9% |

| Information Technology (XIJ) | +1.7% | Siteminder | +6.7% |

| Energy (XEJ) | -0.1% | Viva Energy | -1.9% |

| Utilities (XUJ) | -0.3% | AGL Energy | -0.8% |

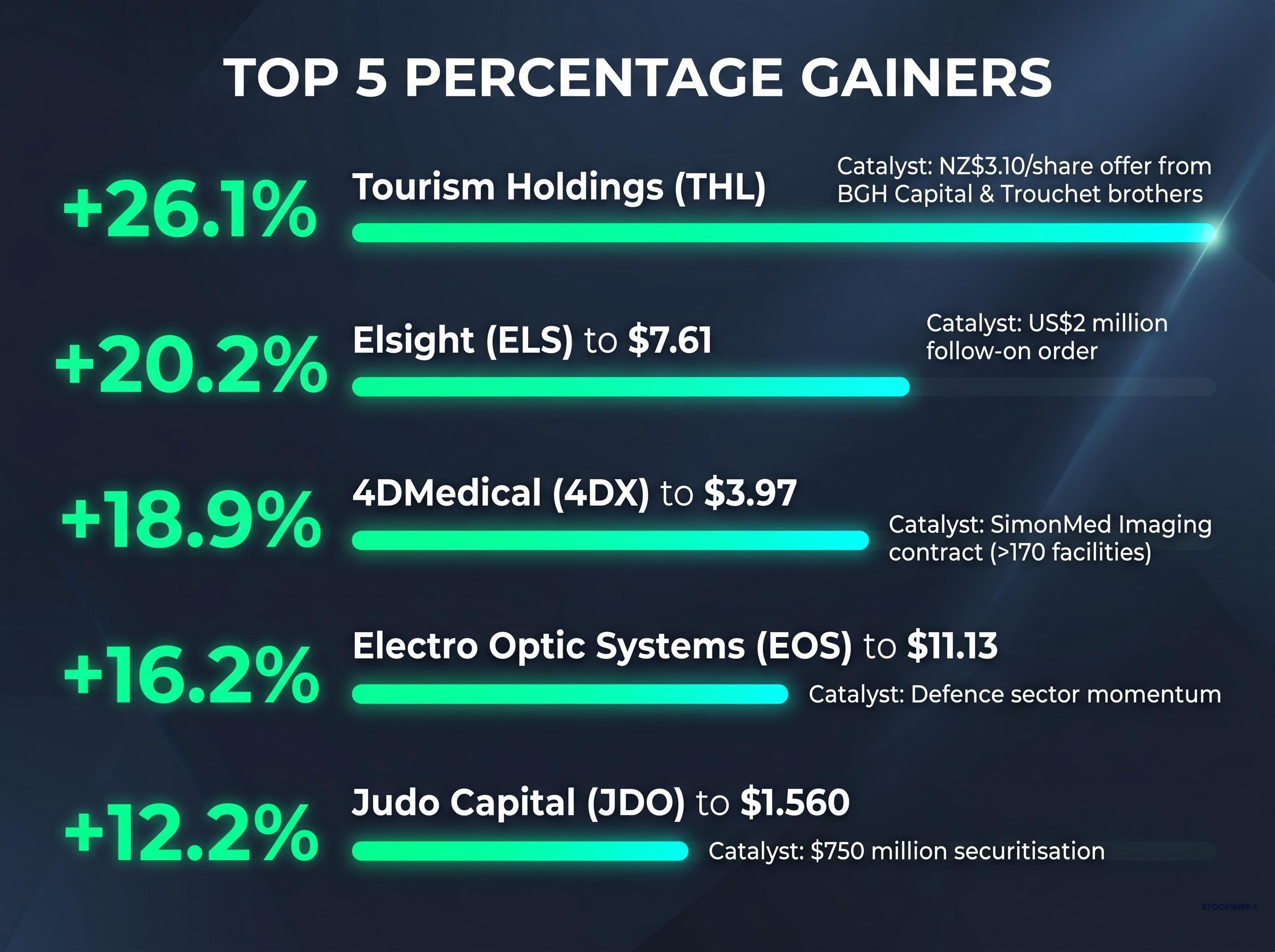

Defence and drone stocks produced some of the day’s largest percentage gains. Elsight led the ASX, surging 20.2% to $7.61 after securing a follow-on US public safety order valued at approximately US$2 million, compared to the initial US$460,000 purchase in January 2026. White House commentary regarding drone-manufacturing funding amplified the broader sub-sector, with Electro Optic Systems jumping 16.2% to $11.13.

The session’s top five gainers by percentage:

Broker upgrades also contributed. Morgans upgraded Tabcorp to Buy (price target $1.07, from $1.20), citing an approximately 40% share price decline. Macquarie upgraded HealthCo Healthcare REIT to Outperform (target $0.83, from $0.67).

Among the session’s notable decliners:

Macquarie cut its price target on IDP Education to $2.35 from $5.45, the starkest single analyst action of the session, as the stock fell to a 52-week low.

A risk-on session occurs when capital rotates from defensive positions (utilities, cash, high-yield bonds) into growth-sensitive assets such as resources, technology, travel, and small caps. The trigger is typically an event that reduces perceived risk in the market, whether a geopolitical de-escalation, a favourable central bank signal, or an economic data release that eases recession fears.

Friday’s ceasefire reports provided that trigger. Reduced Middle East tension pushed crude prices lower, which eased inflation expectations and, in turn, pulled bond yields down. Lower yields then supported asset classes across the board: gold (because the opportunity cost of holding a non-yielding asset falls), real estate (because property trust distributions become relatively more attractive), and technology (because lower discount rates increase the present value of future earnings).

Lower yields reduce the discount rate applied to future earnings, mechanically lifting the present value of long-duration cash flows even when underlying earnings estimates are unchanged, which is why technology and real estate respond so sharply to a single session of bond yield compression.

The same catalyst that lifts most of the ASX simultaneously weighs on the energy sub-sector. Falling crude prices reduce revenue expectations for oil and gas producers, making energy the natural loser in a ceasefire-driven session. Utilities tend to underperform because investors rotate away from defensive holdings when risk appetite rises.

Small caps and emerging companies tend to outperform large caps in strong risk-on sessions because smaller names carry higher sensitivity to shifts in risk appetite. Friday’s data illustrated this clearly: the Emerging Companies index surged 3.05% compared to the XJO’s 1.62% gain. The Financials sector’s sixth consecutive session of underperformance relative to the benchmark serves as a reminder that sector-specific dynamics can persist even within a broadly positive session.

The XJO closed at 8,731.7, at its session peak and at the intraweek high of the weekly candle, approximately 2.0% above the week’s low.

For technically minded investors, a weekly candle that closes at its high is a constructive signal. It suggests buying pressure strengthened into the close rather than fading, and that sellers did not re-emerge at elevated levels. The weekly gain of 74.7 points (+0.86%) was delivered almost entirely in Friday’s session.

The durability of Friday’s rally, however, rests partly on a catalyst that remained unconfirmed. The ceasefire extension was described as tentative as of the close, with no formal diplomatic announcement verified. Weekend news flow will either validate or undercut the positioning that drove the session.

ASX 200 earnings delivery risk is the other side of Friday’s constructive close: with the forward P/E sitting at the upper boundary of the range historically consistent with 5%-6% Australian bond yields and the equity risk premium at roughly 80 basis points, the index has limited valuation buffer if the ceasefire catalyst proves transient and earnings guidance disappoints.

Three variables are likely to shape the open next week: confirmation or denial of the US-Iran ceasefire, follow-through in commodity prices (particularly crude and gold), and any development in the Financials sector’s persistent underperformance relative to the benchmark across six consecutive sessions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A risk-on session occurs when capital rotates out of defensive assets like utilities and cash into growth-sensitive sectors such as resources, technology, and small caps, typically triggered by events that reduce perceived market risk. On 29 May 2026, reports of a US-Iran ceasefire extension drove exactly this rotation, lifting the ASX 200 by 1.62% in a single session.

Falling crude prices eased near-term inflation expectations, which pushed bond yields lower; lower yields reduced the discount rate applied to growth equities and lifted the relative attractiveness of gold and real estate, producing broad gains across materials, technology, and property trusts while only the energy sector declined.

Gold led all sectors with the ASX Gold Sub-Index rising 4.5%, followed by Materials at 2.9%, Real Estate at 1.9%, and Information Technology at 1.7%, while Energy slipped 0.1% and Utilities fell 0.3% as capital rotated away from oil-exposed and defensive holdings.

Tourism Holdings jumped 26.1% after BGH Capital and the Trouchet brothers raised their takeover offer to NZ$3.10 per share, with the consortium already holding 19.9% of the company and a further 16% of shareholders said to be supportive of due diligence.

When the ASX 200 closes at the top of its weekly trading range, it signals that buying pressure strengthened into the close rather than fading, which technically oriented investors treat as a constructive near-term momentum signal; however, Friday's rally rested partly on an unconfirmed ceasefire report, meaning weekend news flow could validate or undercut the move.