Global energy transition investment reached a record USD $2.3 trillion in 2025, yet the ASX-listed fund designed to capture that structural shift spent much of the prior year under significant price pressure before staging a recovery. That tension, between the macro tailwind and the product’s own volatility, is exactly what investors considering the Betashares ERTH ETF need to understand. The fund sits at the intersection of one of the largest capital deployment themes in modern investment history and the practical realities of thematic ETF investing, where structural stories can coexist with sharp near-term drawdowns. As of late May 2026, the fund holds approximately $90.3 million in assets and trades at around $11.32-$11.34 on the ASX, a price that reflects both the recovery from 2025 lows and the cumulative weight of interest rate and policy headwinds. This analysis unpacks what ERTH actually holds, how it has performed and why, what risks the fund carries beyond a management fee disclosure, and how investors should think about its role in a portfolio.

Inside ERTH’s portfolio and why it is built differently from a typical clean energy fund

Most investors approach a “clean energy ETF” expecting solar panels, wind turbines, and pure-play renewable generators. ERTH’s actual composition tells a different story.

The fund targets up to 100 global companies that derive at least half their revenues from products or services aimed at reducing or eliminating carbon emissions. That eligibility rule pulls in companies across nine distinct industry segments:

- Clean energy generation

- Green transportation

- Energy efficiency

- Waste management

- Sustainable food production

- Energy storage

- Smart grids and grid modernisation

- Power electronics and enabling semiconductors

- Industrial automation

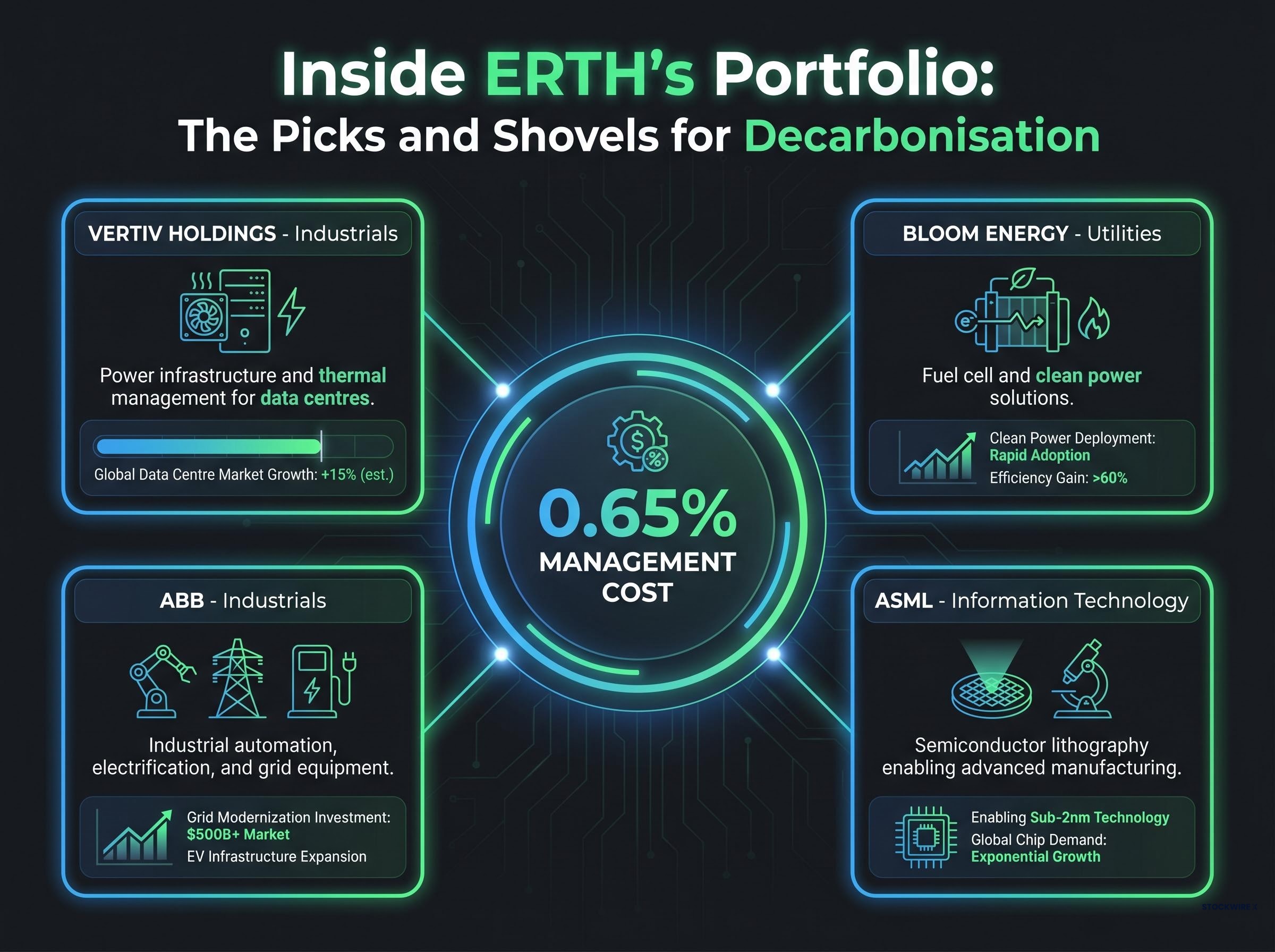

BetaShares has characterised ERTH as providing “the picks and shovels for decarbonisation,” a framing that shifts the lens from renewable energy output to the industrial and technology infrastructure enabling it.

The top holdings confirm this. Names such as Vertiv Holdings, ABB, and ASML are best understood as electrification and manufacturing-infrastructure companies, not renewable energy generators. The management cost sits at 0.65% per annum.

| Holding | Primary Business | Sector |

|---|---|---|

| Vertiv Holdings | Power infrastructure and thermal management for data centres | Industrials |

| Bloom Energy | Fuel cell and clean power solutions | Utilities |

| ABB | Industrial automation, electrification, and grid equipment | Industrials |

| ASML | Semiconductor lithography enabling advanced manufacturing | Information Technology |

Investors who miscategorise ERTH as a pure-play renewables fund will misread both its volatility and its recovery drivers.

The distinction between a concentrated pure-play mandate and ERTH’s broader industrial approach is sharpest when comparing CLNE versus ERTH directly: CLNE’s 30-stock pure-play structure returned approximately 78% in the 12 months to May 2026, while ERTH’s 100-stock diversified approach posted approximately 26%, with the gap reflecting the higher single-theme risk embedded in the more concentrated fund.

When big ASX news breaks, our subscribers know first

The macro case: why USD $2.3 trillion in annual investment is not just a headline number

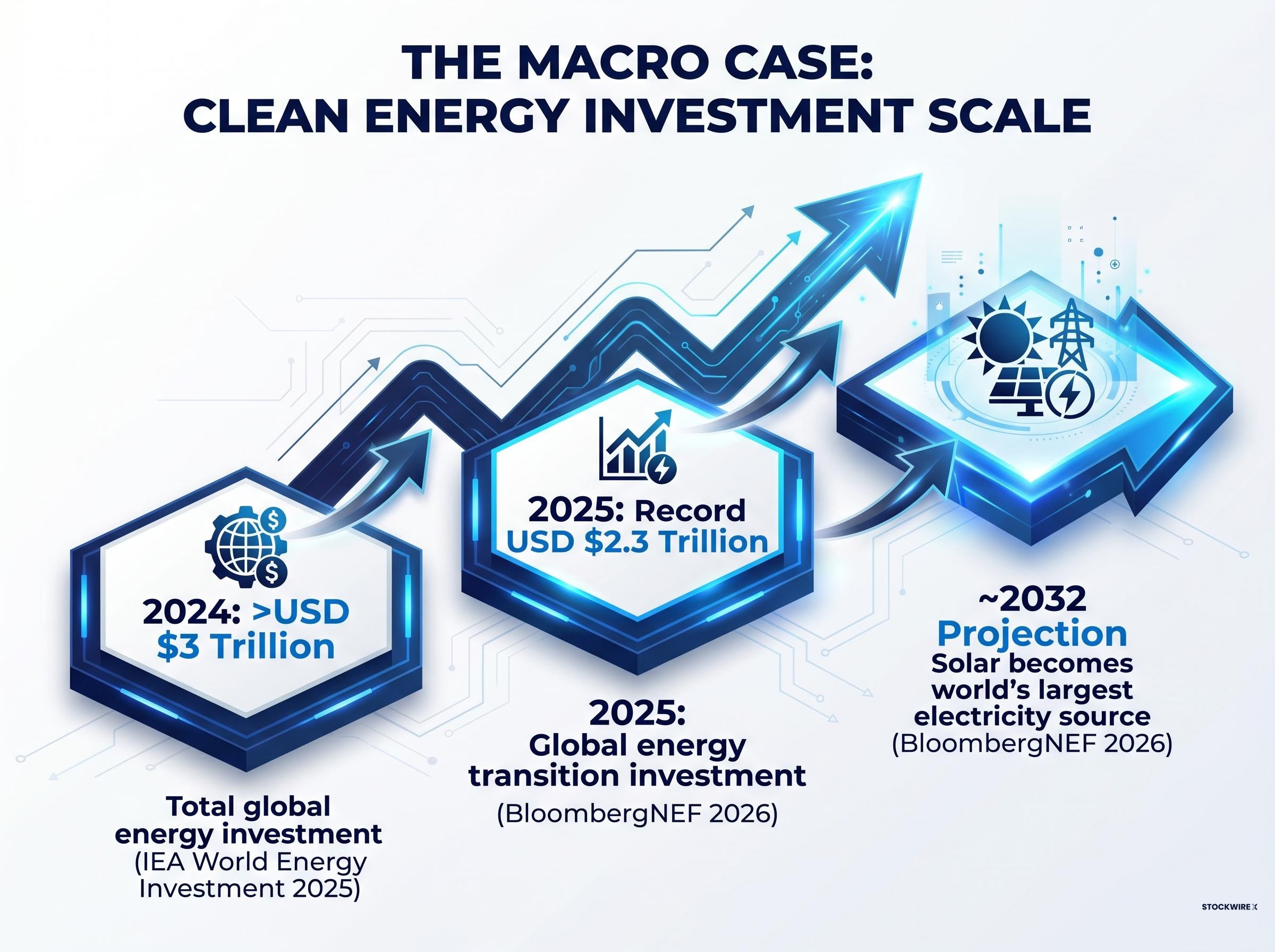

The scale of global clean energy investment provides the structural foundation for ERTH’s long-term thesis. Three data points, progressing from recent actual figures to forward projections, frame the trajectory:

- IEA World Energy Investment 2025: Total global energy investment exceeded USD $3 trillion in 2024, with roughly two-thirds directed toward clean energy, electrification, grid infrastructure, and storage.

- BloombergNEF Energy Transition Investment Trends 2026: Global energy transition investment reached a record USD $2.3 trillion in 2025, with grid and storage investment outpacing some segments of pure-play renewables.

- BloombergNEF New Energy Outlook 2026: Solar is projected to become the world’s largest electricity source by approximately 2032, requiring substantial ongoing grid, storage, and flexibility investment to integrate variable generation.

BetaShares has characterised the energy transition as driven by energy system economics rather than solely by environmental policy frameworks, a distinction that matters for assessing how durable the capital deployment trend is likely to be.

The scale of that number reflects a broader shift in how institutional capital now classifies the energy transition: not as a speculative venture theme but as an infrastructure-grade capital cycle, where predictable long-duration demand from grid build-out and electrification attracts pension funds, sovereign wealth vehicles, and strategic corporate allocators that would not have touched early-stage clean energy a decade ago.

Where within the transition ERTH’s holdings sit

The aggregate investment numbers are large, but what matters for ERTH is where the capital is flowing at the sub-segment level. IEA and BloombergNEF analysis identifies grid modernisation, power electronics, and electrification infrastructure as the specific areas attracting the strongest capital growth. These are precisely the segments where holdings such as Vertiv, ABB, and ASML operate.

On the policy side, US FERC Order No. 2023 interconnection reforms and IRA transferability final rules (published April 2025) create a more predictable project pipeline for equipment suppliers in ERTH’s portfolio.

How ERTH has actually performed, and what drove the moves

ERTH’s price history since 2022 follows a pattern with identifiable, structural causes rather than random volatility. The fund suffered a substantial drawdown through 2022-2023, consistent with the broader clean energy sector, as rising interest rates compressed valuations across capital-intensive growth companies. Elevated rates during 2025 applied further pressure.

The recovery, when it arrived, was selective. According to the BetaShares Q1 2025 Fund Update (dated 22 April 2025), the fund posted an approximate 24% recovery from late-2024/early-2025 lows during Q1 2025. That figure represents a rebound from a trough, not a standard annualised return, and the distinction matters for setting expectations.

The Australian Financial Review reported in May 2025 that ERTH had “rebounded strongly in 2025 alongside a re-rating in power-equipment and data-centre related names.”

The internal composition of that recovery is revealing. The sub-segments that led the rebound were:

- Grid infrastructure and power equipment names

- Data-centre power and thermal management companies (led by Vertiv)

Those that lagged included:

- Early-stage clean energy companies

- Hydrogen-related holdings

As at 27 May 2026, the fund’s NAV stood at $11.34 per unit, with funds under management of approximately $90.3 million across 7,964,891 units outstanding. The current price reflects both the partial recovery and the cumulative weight of the prior drawdown period.

The connection between interest rates and ERTH’s performance is not incidental. Capital-intensive growth companies, which dominate the fund, are structurally more sensitive to discount rate changes than mature, cash-generative businesses. Understanding this mechanism is the foundation for assessing whether the recovery reflects a sustainable re-rating or a temporary reprieve.

Specific risks that come with ERTH’s thematic concentration

Interest rate sensitivity is the most demonstrated and quantifiable risk in ERTH’s history. The 2022-2023 drawdown and the 2025 pressure both traced directly to rate cycles, a pattern consistent across commentary from Morningstar (August 2024 and November 2024) and BetaShares own updates. If rates remain elevated or rise further, the same dynamic applies in reverse.

US policy risk requires more nuanced treatment. The Motley Fool (published 30 May 2026) reported that rollbacks of certain US clean energy incentives during 2025 had a negative impact on portions of ERTH’s portfolio, with further US policy headwinds identified as ongoing risk. At the same time, no enacted federal law between January 2025 and May 2026 has been verified as repealing or materially rolling back the core IRA clean energy tax credits. IRA transferability final rules (April 2025) and energy communities guidance (February 2025) provided partial offsetting support. The distinction between programmatic or executive actions and legislative repeal is one investors should track closely.

Morningstar (August 2024) identified high sector and factor concentration as a source of elevated volatility relative to broad global equity benchmarks.

The behaviour gap in thematic ETFs, where investors pile in near peak valuations and experience money-weighted returns well below the fund’s reported time-weighted figure, is one of the most consistent findings in ETF research and applies with particular force to clean energy funds given their demonstrated pattern of sharp rallies followed by multi-year drawdowns.

ASIC MoneySmart guidance on ETF risks advises Australian retail investors to examine what index or sector an ETF targets and to assess concentration carefully, a consideration that is especially relevant for thematic funds where sector exposure is deliberately narrow.

| Risk Factor | How It Affects ERTH | Current Status |

|---|---|---|

| Interest rate sensitivity | Capital-intensive growth holdings compress under higher discount rates | Demonstrated driver of 2022-2025 drawdowns; rate outlook remains uncertain |

| US policy risk | Sub-IRA regulatory or programmatic changes affect equipment demand pipelines | Core IRA tax credits intact; executive-level headwinds ongoing |

| Concentration and thematic risk | Heavy industrials, IT, and clean energy exposure amplifies sector-specific moves | Higher volatility than broad global equity benchmarks (Morningstar) |

| Currency exposure | AUD/USD movements affect returns independently of underlying stock performance | Structural feature of the fund’s global mandate |

Currency exposure as a structural condition

Because ERTH’s underlying holdings are denominated primarily in USD and other non-Australian currencies, movements in the AUD/USD exchange rate affect returns independently of how the underlying stocks perform. This is not a hidden risk but a function of the fund’s global mandate. Investors should factor it into their broader portfolio currency exposure rather than treating it as a temporary condition that will resolve.

Portfolio fit: where ERTH belongs and how much is enough

The consensus across Morningstar, Livewire Markets, the Australian Financial Review, and BetaShares own commentary is unusually consistent: ERTH is a satellite holding, not a core equity allocation.

The Australian Financial Review described ERTH as a “high-beta thematic ETF” that should sit “at the edges of a portfolio.”

The investor profile for whom this fund is appropriate has four defining characteristics:

- Long investment horizon: the energy transition is a multi-decade structural theme, not a near-term trade

- Tolerance for significant short-term volatility: drawdowns of the magnitude seen in 2022-2025 must be absorbable

- Existing core global equity exposure: ERTH should layer on top of a lower-cost broad market fund, not replace one

- Genuine conviction in the decarbonisation structural trend: without this, the volatility will be difficult to hold through

The 0.65% per annum management cost is high relative to broad global equity ETFs. In context, however, it buys access to active thematic selection across a global universe of decarbonisation-linked companies that most Australian investors could not replicate through direct stock picking. Morningstar (August 2024) noted the fee is comparable with other niche thematic strategies.

Position sizing matters. Morningstar (November 2024) recommended small allocations, warning explicitly against replacing core global equity exposure. Livewire Markets (March 2025) described the fund as appropriate for long-term, higher-risk investors. BetaShares (June 2025) positioned ERTH as a satellite allocation with explicit warnings about concentration risk.

The energy transition is structural, but this fund is not for everyone

The macro case for clean energy and grid infrastructure investment is well-supported by independent data from the IEA and BloombergNEF, and ERTH provides genuine diversified access to that theme through a single ASX transaction. The fund’s actual composition, spanning power electronics, grid equipment, industrial automation, and enabling semiconductors, is broader and more industrial than many investors expect.

The costs of accessing that theme are real. Volatility, a 0.65% fee, concentration risk, currency exposure, and policy sensitivity have all already affected this fund’s returns, not as theoretical risks but as demonstrated performance drivers. Investors who match the satellite-holding profile should assess ERTH against their existing global equity exposure and determine a specific allocation size they can hold through rate cycles and policy uncertainty, rather than treating the fund as a speculative trade on near-term clean energy sentiment.

Investors building a satellite sleeve beyond ERTH should compare other ASX thematic satellite positions across multiple dimensions before allocating, since return dispersion within the thematic category is substantial: two funds with similar ‘technology’ labels can produce return gaps exceeding 30 percentage points in a single year depending on their underlying mandate construction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions and various risk factors.