A striking paradox defines the late April 2026 economy, presenting a complex challenge for accurate stock market analysis. National gasoline prices have pushed past $4.25 per gallon, yet major credit networks are reporting double-digit consumer transaction growth across multiple retail categories.

This contradiction frames the Federal Reserve policy decision concluding today, 29 April 2026. Policymakers are navigating a uniquely fractured macroeconomic environment where traditional leading indicators offer conflicting directions for future growth.

The gap between macroeconomic anxiety and actual consumer behaviour requires careful examination. Investors require a clear, evidence-based dissection of how resilient retail spending, sticky inflation, and a booming artificial intelligence sector are collectively reshaping investment strategies across the remainder of the year.

The Federal Reserve Cements a Higher Floor for Borrowing Costs

The economic data released throughout the first quarter gave central bank policymakers no viable alternative. During its two-day meeting concluding today, the Federal Reserve officially maintained the target federal funds rate at 3.50% to 3.75%.

The official FOMC monetary policy statement confirms this constraint will persist, indicating that policymakers need more definitive evidence of cooling prices before adjusting their current framework.

Wall Street had already entirely priced in this exact outcome, reflecting a broader acceptance of prolonged constraint. The CME FedWatch Tool recorded a 99% to 100% probability of a hold leading into the announcement.

Futures markets indicate no anticipated easing actions, marking a significant recalibration of monetary expectations from just six months ago.

Market Recalibration Futures markets have entirely removed 2026 easing from their pricing models, accepting that structural pressures will force the central bank to maintain elevated borrowing costs.

This establishes the foundational baseline for all capital allocation decisions over the next year and a half. Relief from high borrowing costs is indefinitely delayed, fundamentally altering the calculus for corporate expansion and debt refinancing.

Investors must properly evaluate corporate debt loads and fixed-income yields against this immovable rate floor. Companies carrying significant floating-rate debt will face sustained margin pressure through the end of the calendar year.

When big ASX news breaks, our subscribers know first

Understanding Sticky Inflation in a Geopolitically Fractured World

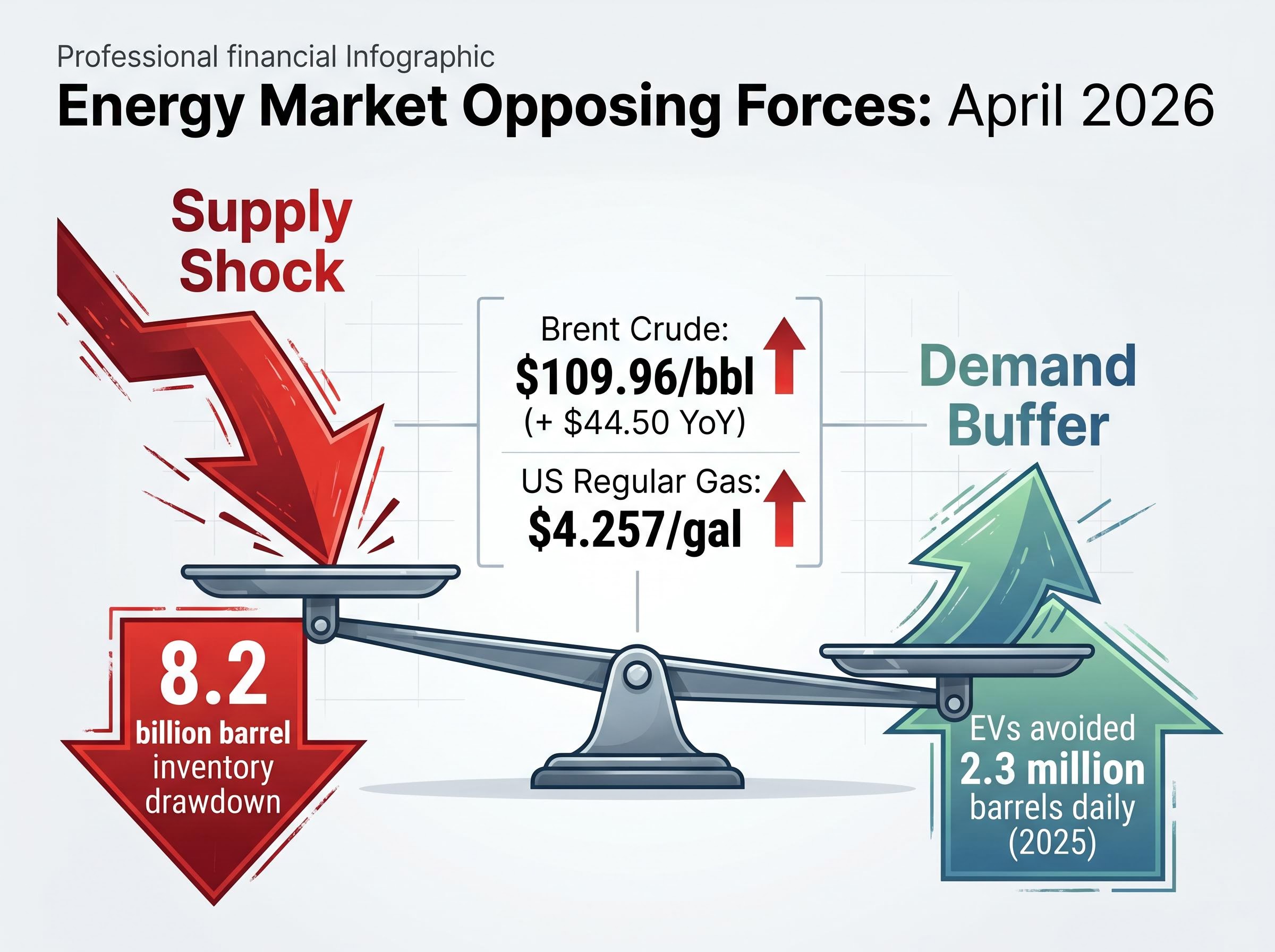

Structural price pressures refuse to moderate despite the sustained presence of elevated borrowing costs. The ongoing conflict in the Middle East has directly constrained global oil supplies, pushing Brent crude to $109.96 per barrel. This represents a substantial price increase of approximately $44.50 year over year.

These international disruptions immediately impact domestic wallets and retail budgets. The average US regular gas price reached $4.257 this week, crossing a psychological threshold for many households.

This dynamic creates what economists call sticky inflation. Sticky inflation refers to price increases that remain stubbornly high and resist dropping, even when central banks raise interest rates to slow the overall economy. When geopolitical shocks disrupt physical supply chains, prices stay elevated regardless of domestic consumer demand levels.

The current energy shock stems directly from an 8.2 billion barrel inventory drawdown linked to Strait of Hormuz disruptions. Competing forces are currently battling in energy markets, complicating the forward outlook for petroleum producers.

Institutional models warn that an extended closure could push benchmark crude even higher, creating adverse tail risk scenarios that substantially increase domestic recession probability.

Geopolitical supply constraints are fighting against demand destruction driven by the global adoption of electric vehicles. Electric vehicle adoption successfully avoided 2.3 million barrels of oil demand daily in 2025, providing a slight buffer against the current supply shock.

Investors must grasp that current inflation is being driven by supply-side geopolitical shocks rather than overheated demand. This distinction helps evaluate which sectors have the pricing power to survive prolonged supply chain constraints. Energy costs bleed into the broader consumer economy through three distinct pathways:

- Primary transportation and logistics surcharges for all physical goods requiring heavy freight.

- Secondary increases in manufacturing input costs, particularly for plastics and petroleum-based industrial products.

- Tertiary reductions in discretionary income as households allocate more capital to basic commuting.

The American Consumer Defies Macroeconomic Gravity

Retail buyers are ignoring conventional expectations and continuing to transact at remarkably high volumes. High energy prices typically compress household spending rapidly, but payment processing data released this week shows unexpected resilience.

The Census Bureau advance retail sales data confirms this momentum, showing that household spending across major retail and food service categories continues to grow despite rising borrowing costs.

Fiscal second-quarter network transaction volume metrics for Visa are currently unavailable. American Express volume metrics are currently unavailable over the same period.

The global transition away from physical currency acts as a structural tailwind supporting these electronic commerce networks. This persistent spending complicates the Federal Reserve mandate, as high consumer demand supports further retail price increases.

This payment data directly challenges the assumption that high interest rates have entirely crushed the consumer. Consumer-facing equities still command strong cash flows, particularly digital payment networks capturing the permanent shift toward cashless transactions.

Corporate Divergence Separates Artificial Intelligence from Travel

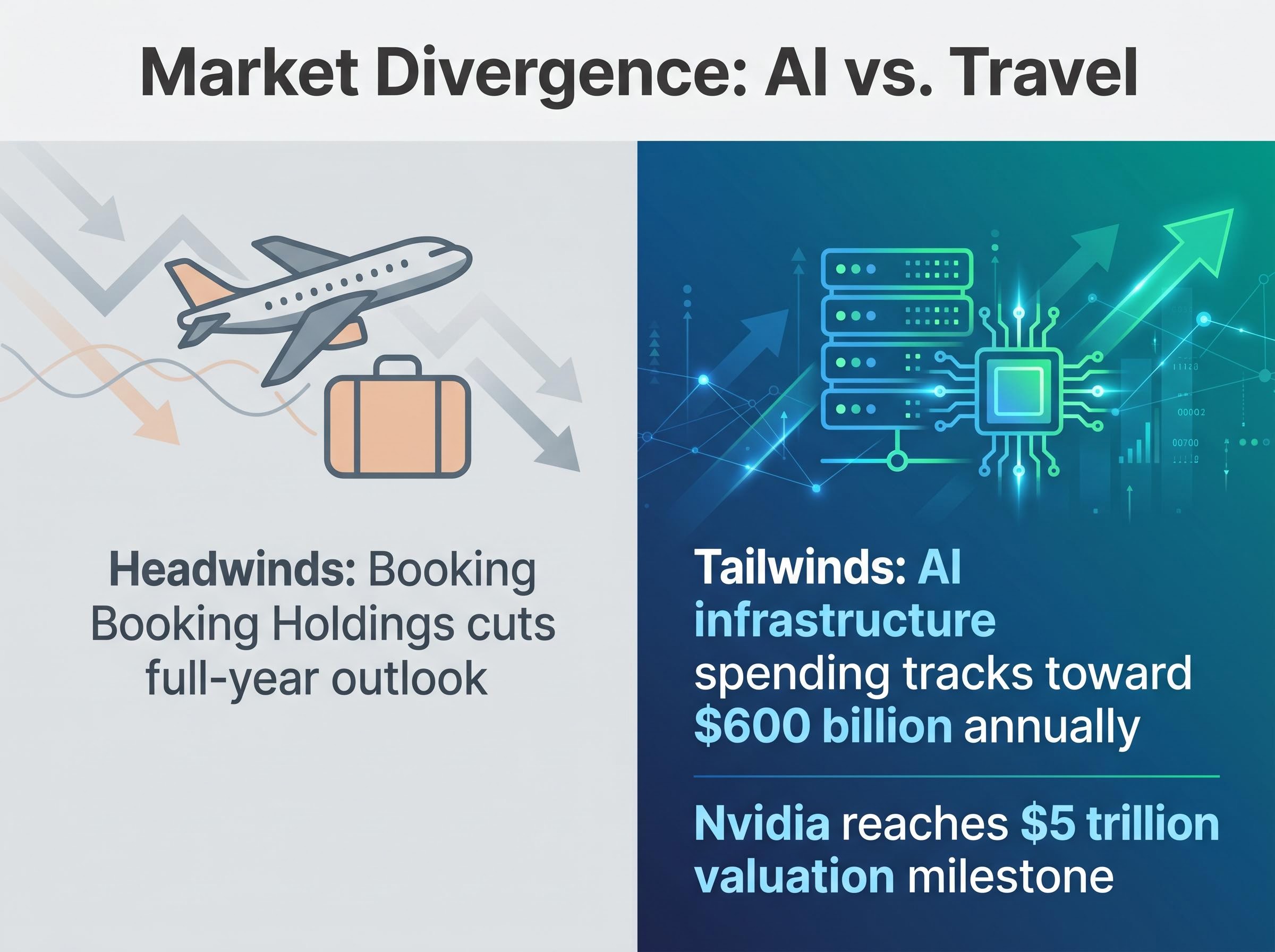

Different corporate sectors are absorbing the current geopolitical shock in starkly contrasting ways. The global tourism sector is experiencing severe demand destruction due to international hostilities and rising aviation fuel costs.

Booking Holdings has cut its full-year outlook due to dampened consumer demand directly tied to regional conflict. This weakness contrasts completely with the massive capital expenditures funneling into alternative power and data infrastructure.

Tech infrastructure spending acts as an independent, insulated economic engine that operates independently of retail consumer health. Artificial intelligence infrastructure spending is currently tracking toward $600 billion annually.

The energy requirements for new server facilities are generating entirely new revenue streams for independent power providers.

Alternative energy companies are emerging as indirect beneficiaries of this expansion, supplying the critical power infrastructure necessary to sustain massive data center operations.

Investors must avoid treating the stock market as a single, unified entity responding to identical pressures. Capital is actively hiding from geopolitical risks by moving away from discretionary hospitality and toward structural technological development.

The divergent factors driving these sectors include:

Geopolitical vulnerability heavily limits international travel bookings and cross-border tourism. Corporate productivity mandates force continuous enterprise investment in machine learning capabilities. Data centre energy requirements create unprecedented new demand for independent power generation. Discretionary consumer budgets prioritise local spending and digital services over overseas holidays.

Synthesising the Conflicting Signals for Equities

Pulling these disparate threads into a cohesive forward-looking framework clarifies the new market paradigm. The heavy concentration of tech giants masks underlying vulnerabilities in the broader stock indices, creating a distorted view of corporate health.

The Illusion of Index Stability

Headline market performance is heavily skewed by a handful of mega-cap technology companies. The four reporting technology giants collectively account for a significant portion of the total S&P 500 index valuation.

Nvidia recently reached a historic $5 trillion valuation milestone, standing as the ultimate symbol of this unprecedented index concentration. This extreme weighting means the broader index can report gains even while the majority of constituent companies suffer margin compression.

Investors must look beneath surface-level index returns to understand the true underlying economic health of standard industrial firms. The equal-weight indices show a much flatter trajectory, reflecting the strain of elevated borrowing costs on mid-sized manufacturers and regional banks.

If consumer spending eventually cracks under the weight of $4.25 gas, corporate profit margins will face severe and immediate compression. Allocators must navigate an environment defined by a 3.50% baseline rate floor and $100 oil through the remainder of 2026.

For allocators reevaluating their portfolio weighting, our full explainer on passive index concentration risk details how heavy reliance on megacap tech fundamentally alters the traditional diversification benefits of broad market funds.

Navigating a Market Defined by Resilience and Constraint

The core tension in late April 2026 lies between consumer transaction strength and the immovable constraints of energy inflation. Retail spending demonstrates surprisingly high volumes, but supply-side shocks keep basic living costs elevated across the board.

The Federal Reserve will remain securely on the sidelines until these competing macroeconomic forces resolve. Investors cannot rely on central bank intervention or immediate rate cuts to boost equity valuations in the near term.

Monitoring specific corporate profitability margins will serve as the ultimate tiebreaker in this prolonged economic standoff. Companies that can successfully defend their margins against higher input costs while servicing debt at 3.50% rates will structurally outperform the broader indices.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.