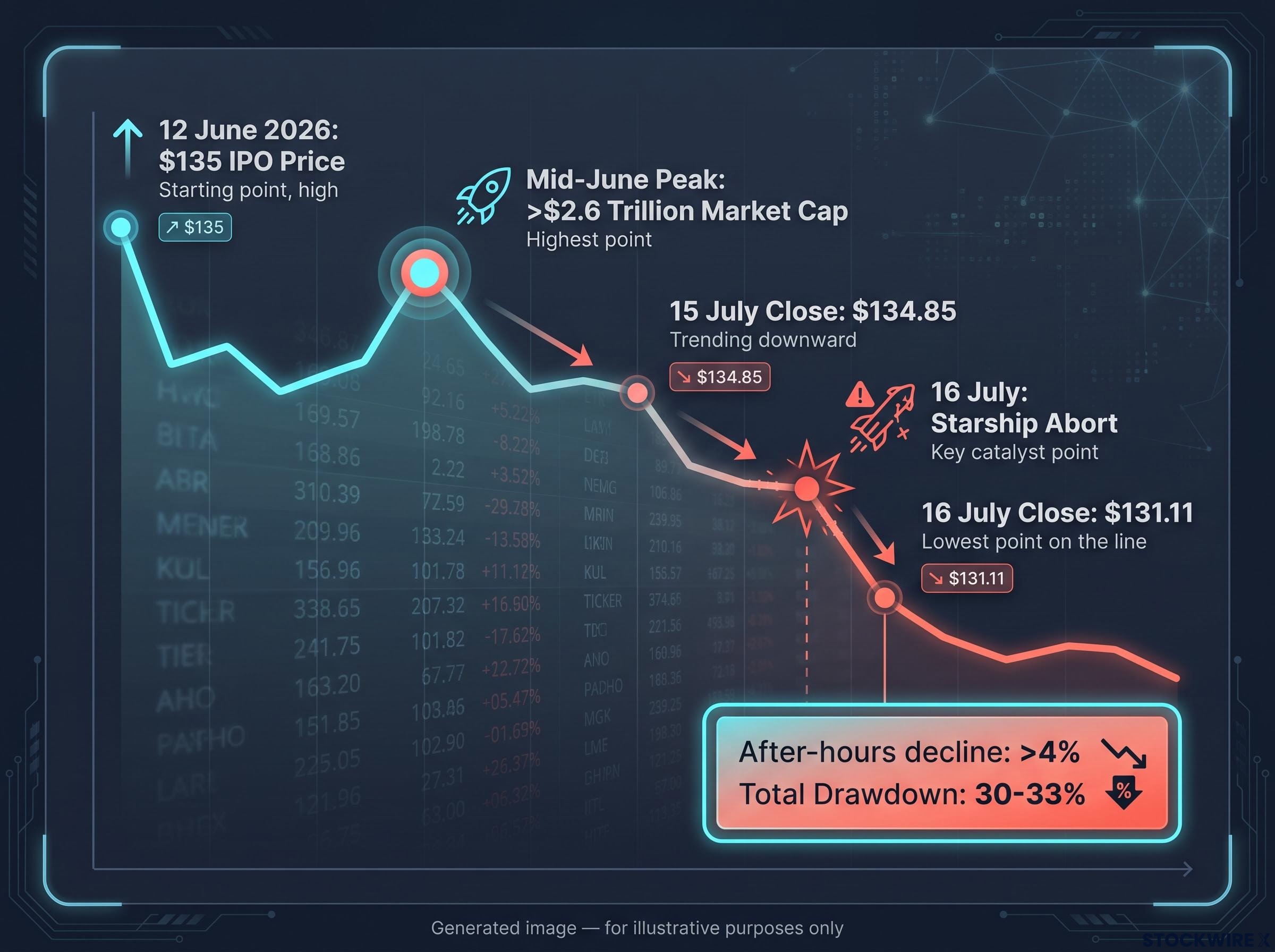

SpaceX shares fell beneath their $135 IPO price for the first time on Wednesday 16 July 2026, after the company’s Starship rocket failed to lift off during a scheduled test. The stock finished the session at $131.11, and extended losses of more than 4% once the abort news spread through after-hours trading.

The decline marks a concrete inflection point for a company that debuted on Nasdaq just five weeks ago to blockbuster demand and a market capitalisation that briefly exceeded $2.6 trillion. The stock now sits roughly 30% below its mid-June peak, a level that puts many early retail buyers underwater for the first time.

Here is what actually happened, why the IPO price level matters psychologically and practically, and what the compounding risks ahead mean for investors deciding what to do next.

What happened on 16 July and why the stock fell the way it did

The launch pad

During a planned test at the Texas facility, SpaceX’s Starship vehicle came within moments of liftoff before its engines cut out and the attempt was called off. Several of the rocket’s engines fired briefly but failed to sustain ignition, bringing the countdown to a halt before the vehicle cleared the pad. CEO Elon Musk posted on social media that a further attempt could be made as early as next week, though he stopped short of confirming how many engines had malfunctioned.

For SpaceX’s engineering teams, a scrubbed countdown is an iterative step. For the stock, it was a catalyst.

The price action

The sequence of moves told its own story:

- IPO price: $135, listed on Nasdaq 12 June 2026

- 15 July close: $134.85, already drifting below the offering level

- 16 July close: $131.11, down more than 3% during the regular session

- After-hours decline: more than 4% once the abort headlines circulated

- Drawdown from mid-June peak: approximately 30-33%

That gap between how an engineering culture processes a scrubbed test (fixable, expected, part of the iteration loop) and how public markets process the same event (sell first, assess later) is the dynamic new SpaceX shareholders now need to account for every time a launch is scheduled. The company went public five weeks ago. Every visible technical event is now a market event, regardless of how the internal engineering team categorises it.

When big ASX news breaks, our subscribers know first

Why the IPO price acts as a psychological tripwire for investors

The $135 level is not a financial metric in any meaningful analytical sense. It is the boundary between “I am making money” and “I am losing money” for anyone who bought at or near the offering. That distinction is psychological, but it shapes real behaviour.

The pattern is familiar. Early enthusiasm and narrative-driven demand pushed SpaceX well above its offering price within days. Market capitalisation briefly topped $2.6 trillion. Then weeks of price discovery pulled the stock toward a level more consistent with real-world execution risk. That process has now erased roughly $800 billion in market capitalisation from peak to trough (an approximate, unverified estimate), and the stock trades in the low $130s.

Analyst intrinsic value estimates for SpaceX diverge sharply from its peak market capitalisation, with Morningstar placing fair value at roughly $780 billion against a listing price that implied $1.75 trillion, a gap that explains why the stock’s post-IPO re-rating has been steep even before the Starship abort introduced fresh execution risk.

Trading below the IPO price does not tell you whether the business is broken. It tells you the price at listing captured peak optimism, and the market is now doing the slower work of pricing in execution risk.

Retail investors who anchor to $135 as a buy or sell signal are responding to psychology, not fundamentals. The productive question is whether the investment thesis has changed, not whether the number on the screen is red.

The risk landscape facing SpaceX shareholders right now

The launch abort was the immediate catalyst, but it sits on top of a broader set of compounding pressures that make this stock structurally volatile at this stage of its public life.

| Risk Category | What It Is | Concrete Detail | Potential Trigger |

|---|---|---|---|

| Operational Risk | Launch failures or delays shifting revenue timelines | 16 July Starship abort sent shares down more than 4% in hours | Next Starship test attempt (as early as next week) |

| Valuation Risk | Aggressive growth assumptions already embedded in the price | Analyst 12-month targets range from approximately $236-$245 consensus to a $75-$600 bull/bear spread (unverified) | Any disruption to Starlink, Falcon, or Starship revenue timelines |

| Key-Person Risk | Musk’s visibility and multi-company commitments create communication volatility | Social media posts move the stock independently of business performance | Any high-profile Musk statement or controversy |

| Lock-Up / Supply Risk | Employee and early-backer shares entering the tradable float | At least 20% of locked shares released after Q2 results; full expiry by December 2026 (unverified) | Q2 earnings release; December 2026 full lock-up expiry |

One additional amplifier: approximately 28% of the tradable float is currently shorted (unverified), meaning a material fraction of the market is actively positioned for further downside. Elevated short interest both reflects negative sentiment and amplifies it, because short-covering rallies and further shorting on bad news can produce outsized price swings in both directions.

The partial unlock after Q2 results represents only one milestone in a far more granular lock-up schedule, with roughly a dozen distinct release events spread across 2026 and a performance trigger that could accelerate earlier tranches if SPCX closes above $175.50 on five of ten consecutive trading days.

The combination of these factors tells you that major price-moving events are still ahead. Position sizing should account for that volatility, not just conviction in the long-term narrative.

Understanding post-IPO price discovery as a structural phase, not a crisis

Post-IPO price discovery is the period during which the broader market, rather than a small group of underwriters and anchor investors, determines a stock’s price through real-world buying and selling with full information access. It is not a crisis. It is a phase, and it behaves in recognisable ways.

Three characteristics define it:

- Short public history: The company has limited reported earnings as a public entity, so future scenarios dominate valuation models more than historical performance

- Sentiment-driven pricing: Shifting expectations, analyst initiations, and headline flow move the stock more than fundamentals in the near term

- Amplified reaction to catalysts: Every launch, earnings release, or executive statement produces larger moves than it would for a company with years of public track record

SpaceX is approximately 30-33% below its mid-June high. Trading volumes remain elevated. Price swings around news events are sharp.

The expectations gap that punishes newly public companies is structural, not incidental: any stock priced at a substantial premium to peers faces near-zero tolerance for execution variance, so a scrubbed launch at current sentiment levels produces a larger price reaction than the same event would for a company with years of public track record behind it.

The lesson is structural, not specific to one company: any newly public business priced at peak optimism will go through a period where price and narrative decouple. Investors who recognise this in advance are far better positioned to hold their thesis through it, or to exit on fundamentals rather than fear.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The next major ASX story will hit our subscribers first

Practical decisions for investors in three different positions right now

The right response to this news depends entirely on where you sit. A framework for each.

If you bought near the IPO price and are now underwater

The productive question is not whether the price is uncomfortable. It is whether the underlying pillars have materially changed. Has Falcon launch cadence deteriorated? Has Starlink’s subscriber trajectory shifted? Has Starship’s contract pipeline weakened?

If those pillars remain intact in your assessment, the move below $135 is part of the volatility inherent in owning a newly public company at this stage. If something has changed in how you assess those pillars, that is a reason to reassess, and the price level is secondary.

If you are considering buying now because the price has fallen

A lower price does not automatically mean better value. The current price already embeds new information: execution risk exposed by the abort, spending and debt load concerns, lock-up supply approaching through December 2026, and elevated short interest. Before buying, the relevant question is whether the long-term scenarios, Starlink at scale, Starship fully commercial, major contract wins, justify owning a stock that can move 4-5% on a single headline.

If you are thinking about trading around the next launch attempt

Markets often partially price in anticipated good news before it arrives. If optimism recovers heading into the next Starship test, a successful launch may produce less upside than you expect. A second abort at current sentiment levels would likely accelerate selling. The risk profile around binary technical events is asymmetric, and unless you have a professional trading setup with strict risk controls, treating these events as trading opportunities rather than long-term data points is hazardous.

Regardless of which position you hold, the most actionable insight from this moment is that SpaceX warrants treatment as a high-volatility position. A 4-5% daily move is manageable if the stock represents 3-5% of a total portfolio. The same move at 15-20% concentration is a different proposition entirely.

What this correction changes and what it does not

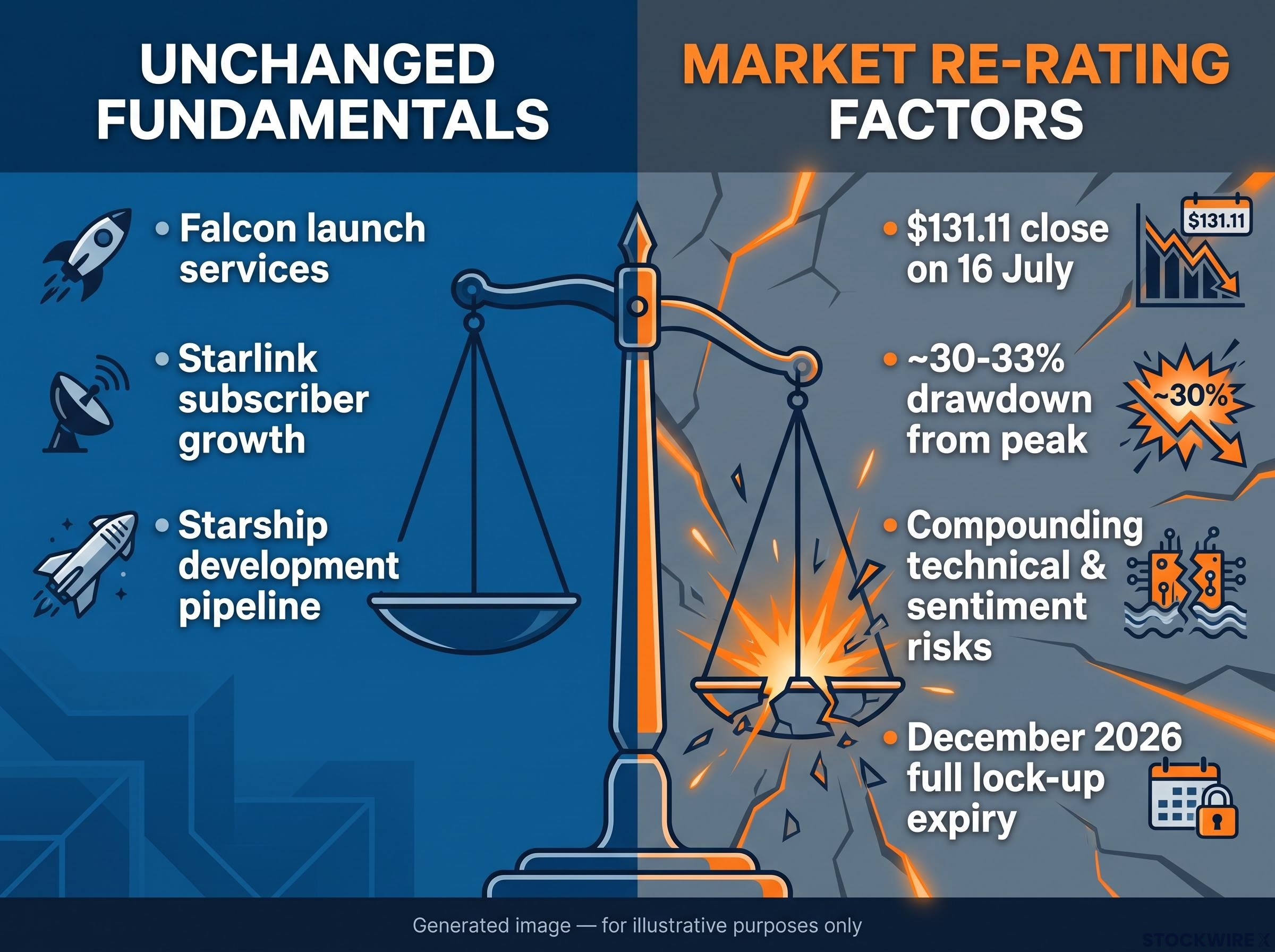

None of the fundamental pillars of the SpaceX business, Falcon launch services, Starlink subscriber growth, Starship’s development pipeline, changed because the stock closed at $131.11 on 16 July. The rocket did not launch. The engineering team will iterate. Musk indicated another attempt could come as early as next week.

What did change is the market’s willingness to pay peak-enthusiasm prices in the face of compounding technical, supply, and sentiment risks. That re-rating is real, and it has further to play out: the partial lock-up release after Q2 results and the full December 2026 expiry are dated events still ahead.

Peak-optimism pricing is not unique to SpaceX, but the scale of the initial surge, a 19.6% single-session gain on Day 2 followed by a further 11.2% after-hours move that briefly pushed market capitalisation toward $3 trillion, set a baseline for subsequent disappointment that is unusually large even by IPO standards.

The move below the IPO price is not a verdict on whether SpaceX‘s businesses will ultimately deliver. It is the market re-rating peak-optimism pricing in real time. Those are different things, and investors are best served by holding both truths simultaneously.

For investors who entered with a clear long-term thesis, this correction is a test of that thesis’s robustness. The ones most likely to navigate it well are those who wrote down why they bought before the stock fell, who sized the position for volatility rather than conviction alone, and who treat the next Starship test, the next earnings release, and the next lock-up expiry as information inputs rather than emotional triggers.

Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions and various risk factors. These forward-looking statements are speculative and subject to change based on market developments and company performance.