SpaceX submitted its S-1 registration statement to the SEC on 20 May 2026, and the language inside it reaches well beyond rockets. The filing describes the company as “building the infrastructure of the future,” a phrase that gestures toward AI compute capacity as much as satellite connectivity or launch services. Most investors approaching the anticipated approximately $2 trillion IPO still frame SpaceX as a launch and connectivity business. The acquisition of xAI in early 2026, however, introduced a third business arm that management is positioning as the company’s largest long-term opportunity, one rooted in AI infrastructure on the ground and, eventually, in orbit. What follows stress-tests that AI infrastructure narrative against verified source material, separates confirmed strategic milestones from management ambitions that remain unverified in public filings, and draws out the specific investment questions that matter most for investors evaluating the SpaceX IPO.

How the xAI acquisition transformed SpaceX into a three-segment business

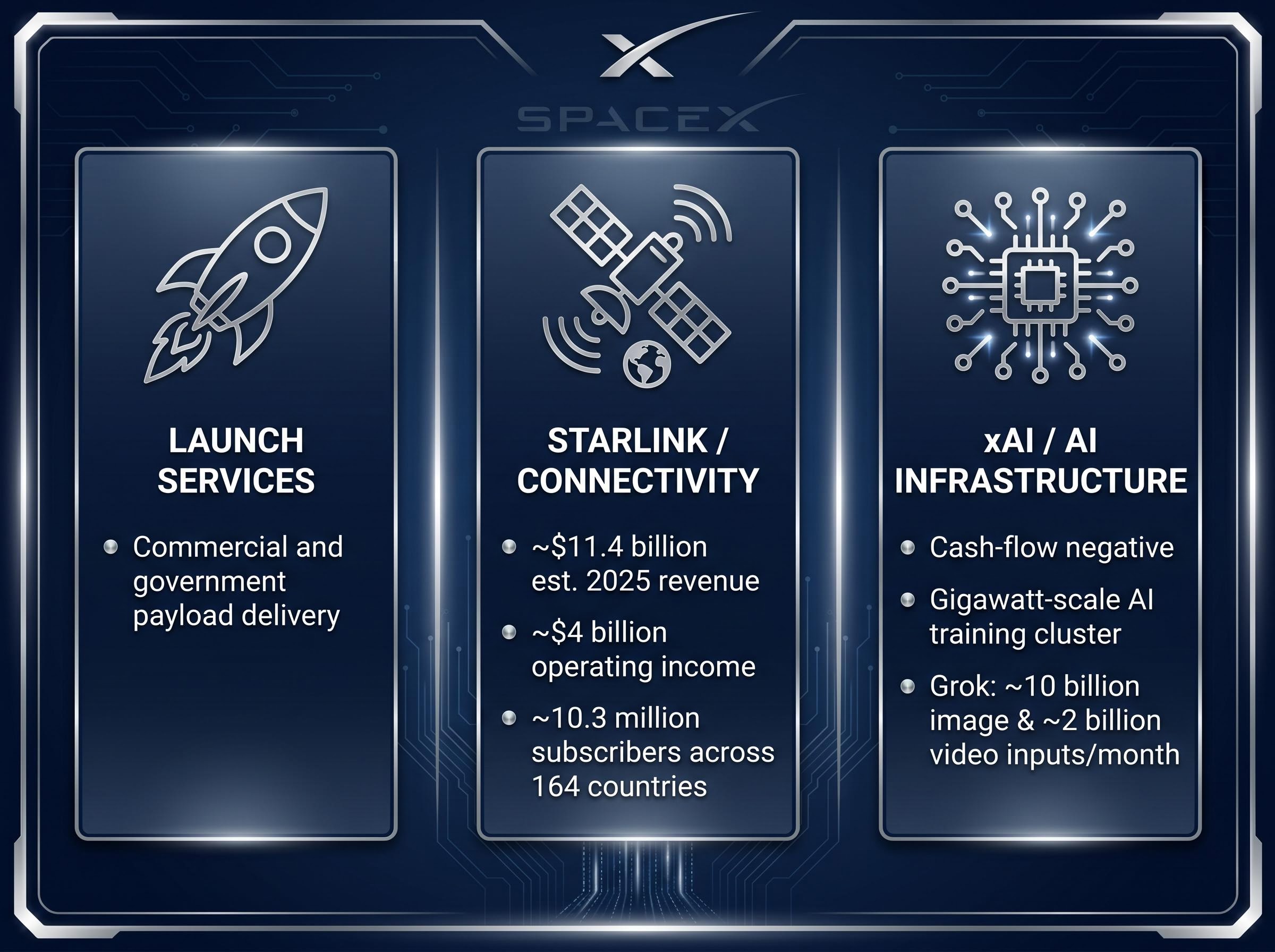

The reverse triangular merger that brought xAI into SpaceX in late January to early February 2026 did not merely add a product line. It restructured the investment case. SpaceX now operates three distinct business arms, each with a different financial profile:

- Launch services: The original business, providing commercial and government payload delivery to orbit.

- Starlink / connectivity: Approximately $11.4 billion in estimated 2025 revenue and roughly $4 billion in operating income, serving approximately 10.3 million subscribers across 164 countries.

- xAI / AI infrastructure: Currently cash-flow negative, with substantial ongoing capital requirements. The S-1 describes xAI as “the first company to build a gigawatt-scale AI training cluster.”

The Grok platform, now part of the combined entity, processes approximately 10 billion image inputs and 2 billion video inputs per month. That volume signals real operational scale, though it does not yet translate into the kind of external revenue that funds the capital expenditure ahead.

SpaceX’s Q1 2026 operating loss of $1.94 billion reflects the combined drag of xAI consolidation and accelerating capital expenditure, with the AI segment generating $818 million in revenue against a cost base that the S-1 does not fully itemise at the segment level.

What the gigawatt-scale cluster actually means

xAI’s ground-based cluster represents confirmed, operational AI compute capacity now absorbed into SpaceX’s balance sheet. It is a physical asset, not a roadmap item. The S-1, however, does not specify a deployment timeline or annual capacity expansion target beyond this gigawatt baseline. Investors pricing in rapid capacity growth are extrapolating from directional intent, not a documented build schedule.

The Colossus cluster hardware that constitutes the gigawatt-scale ground-based compute referenced in the S-1 runs approximately 320,000 Nvidia accelerators across H100, GB200, and GB300 generations, with Nvidia confirmed as the primary supplier in the filing and Wolfe Research framing SpaceX as a top-tier strategic customer with a multi-year procurement roadmap.

When big ASX news breaks, our subscribers know first

Orbital computing as a strategic differentiator: what the evidence confirms and what it does not

The strategic logic behind satellite-based AI inference is genuine. Solar energy is abundant in orbit. The vacuum of space offers natural thermal management advantages that eliminate the cooling constraints facing ground-based data centres. And SpaceX already operates the world’s largest satellite mega-constellation, providing a built-in delivery network for compute outputs.

A Bloomberg TV segment from 18 February 2026 documented internal memos from Elon Musk and SpaceX CFO Brett Johnson describing plans for “satellite form factor data centres” focused on AI inference.

Bloomberg, 18 February 2026: Internal memos describe SpaceX’s plans for “satellite form factor data centers” designed for AI inference workloads, with a regulatory filing to launch as many as one million satellites in support of orbital compute.

The S-1 reinforces this direction, framing “space-based data centers” as part of the combined entity’s roadmap. Management commentary via investor briefings has referenced orbital AI compute infrastructure “potentially deployable as early as 2028,” characterised as a long-term ambition.

What the evidence does not yet support:

- No orbital data-centre satellites have been launched or announced with specific dates.

- No named orbital-compute partners have been publicly identified in any 2025-2026 named-source report.

- The S-1 does not commit to specific orbital compute launch milestones.

The orbital thesis is the most differentiated element of the SpaceX AI story, because no hyperscaler can replicate it. Understanding the gap between confirmed regulatory filings and operational deployment is where the real risk calibration sits.

Energy constraints and the power economics of large-scale AI compute

The macro energy picture provides the proportional frame that the S-1’s directional language does not. The EIA’s AEO2025, published in March 2025, projects average U.S. electric load at approximately 480-490 GW in the mid-2020s. McKinsey’s July 2025 analysis projects the entire U.S. data-centre fleet reaching approximately 35 GW by 2030 in its base case. Goldman Sachs research from early 2026 estimates AI-driven data centres could add tens of gigawatts of incremental demand by the end of the decade, with grid permitting identified as a binding constraint.

The EIA AEO2025 electricity projections, published in March 2025, form the baseline against which every gigawatt-scale AI compute claim must be measured, placing the sector’s aggregate demand trajectory in the context of total U.S. grid capacity.

| Entity / Scenario | Power Demand (GW) | Timeframe | Source |

|---|---|---|---|

| Total U.S. average electric load | ~480-490 | Mid-2020s | EIA AEO2025 (March 2025) |

| U.S. data-centre fleet (base case) | ~35 | By 2030 | McKinsey (July 2025) |

| AI-driven incremental demand | Tens of GW | By 2030 | Goldman Sachs (early 2026) |

| Unverified 100 GW/year target | 100 (annual) | Not specified | Not confirmed in any SEC filing or named source |

A 100 GW per year continuous power draw target, which has circulated in some analysis of the IPO, would exceed the entire projected U.S. data-centre fleet by a factor of nearly three. That figure appears nowhere in SpaceX’s S-1 or any named 2025-2026 media source and should be treated as unverified. What the S-1 does confirm is directional intent to “build the infrastructure of the future,” language that establishes ambition without committing to a specific deployment rate.

The grid constraint is not incidental; it is the strategic argument for orbital compute. Energy availability in orbit sidesteps the permitting and grid-connection bottlenecks slowing every hyperscaler’s terrestrial expansion.

AI infrastructure power constraints are not specific to SpaceX; Wall Street projects $530-700 billion in global data-centre IT spending across 2026, and U.S. data centres are on track to consume approximately 9% of domestic electricity by 2030, up from 4% in 2023, a grid pressure that makes the orbital compute thesis structurally attractive to any investor already tracking terrestrial hyperscaler bottlenecks.

What orbital and satellite-based computing actually requires: a primer on the infrastructure stack

Orbital compute is structurally distinct from anything a terrestrial hyperscaler operates. It removes three constraints that define ground-based data-centre economics:

- Starship V3 reduces the cost of putting hardware in orbit. With 100 metric tons of payload capacity per mission and full reusability, anticipated to become operational in H2 2026, Starship V3 makes deploying compute hardware at scale economically feasible for the first time.

- Starlink V3 solves the downlink throughput constraint. Each Starlink V3 satellite is designed to deliver up to 1 terabyte per second of downlink capacity, and a single Starship V3 launch could carry up to 60 Starlink V3 satellites, representing approximately 20 times the downlink capacity per mission compared to Falcon 9.

- Orbital compute then becomes viable for AI inference at commercial scale, with results delivered through the Starlink mega-constellation directly to end users.

Land permitting, grid connection, and cooling water, the three constraints that slow every terrestrial build-out, do not apply in orbit. The two constraints orbit introduces are launch cost per kilogram and on-orbit power density, both of which Starship V3 is engineered to address.

The backhaul problem Starlink V3 solves

Prior generations of satellite-based compute were impractical for AI inference because downlink throughput could not deliver outputs to users fast enough to be commercially useful. Starlink V3’s terabyte-scale per-satellite throughput changes that calculation. This is why the S-1 frames the satellite constellation and AI infrastructure as an integrated stack rather than separate products. The constellation is not just a connectivity business; it is the delivery layer for orbital compute.

How SpaceX compares to AWS, Azure, and Google Cloud, and where the comparison breaks down

The hyperscaler comparison is both useful and misleading. It is useful because both SpaceX and the major cloud providers require massive capital deployment, compete for AI training and inference workloads, and face grid-access constraints. The enterprise customer bases overlap.

It breaks down in a specific way. SpaceX is building proprietary AI infrastructure primarily for its own ecosystem: Starlink, xAI, and Grok. It is not operating a general-purpose public cloud platform. Its competitive moat is vertical integration and launch cost, not data-centre software abstraction layers.

Aswath Damodaran, writing on Substack in March 2026, characterised xAI’s AI capability as “nascent” relative to incumbent hyperscalers, framing the AI build-out as important to valuation but still early-stage compared to AWS, Azure, and Google Cloud.

| Dimension | SpaceX / xAI | AWS / Azure / GCP |

|---|---|---|

| Current external cloud revenue | Not established as a public cloud provider | Combined hundreds of billions annually |

| Primary competitive moat | Vertical integration (launch + constellation + AI compute) | Software ecosystem, enterprise relationships, scale |

| Orbital compute capability | Regulatory filings submitted; no hardware deployed | None |

| Primary customer base | Internal ecosystem (Starlink, xAI, Grok) | External enterprise and government clients |

Anthropic’s confirmed major cloud agreements remain with AWS and Google Cloud, not SpaceX. A SpaceX-Anthropic compute agreement of any value has not been confirmed in any named public source. Investors who benchmark SpaceX against AWS on current cloud revenue will systematically underprice the orbital moat and overprice near-term enterprise revenue. The more precise frame is a vertically integrated infrastructure company with a unique pathway to compute that no hyperscaler can replicate, competing in a market it does not yet fully participate in.

Separating confirmed fundamentals from optionality in the SpaceX IPO valuation

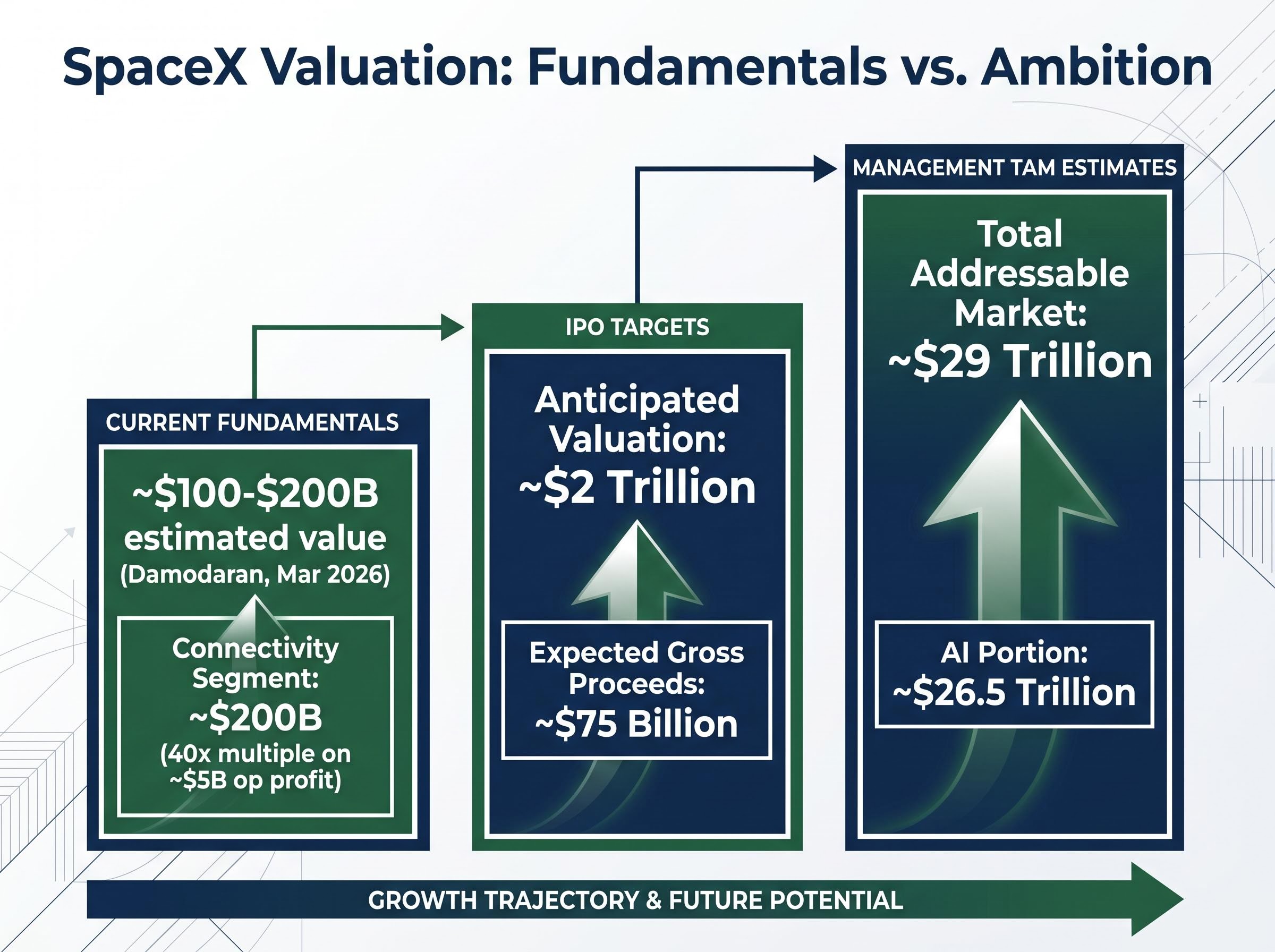

The gap between what SpaceX earns today and what the IPO asks investors to pay is explicit. Aswath Damodaran’s March 2026 framework estimated current fundamental value at approximately $100-$200 billion based on existing financials. The connectivity segment’s estimated operating profit of approximately $5 billion, valued at a 40x multiple, accounts for roughly $200 billion on its own.

Damodaran’s framework for valuing high-optionality growth companies identifies the structural difficulty of separating current cash-flow value from speculative optionality premiums, which is precisely the analytical task the approximately $2 trillion IPO price demands of every investor in the SpaceX offering.

Damodaran, March 2026: Current fundamental value is estimated at approximately $100-$200 billion based on 2025 financials. The approximately $2 trillion IPO valuation requires substantial execution against the AI and orbital roadmap.

The IPO is anticipated to value the company at approximately $2 trillion, with expected gross proceeds of approximately $75 billion. Ron Baron of Baron Capital, holding approximately $15 billion in SpaceX shares, has signalled intent to deploy an additional $1 billion at the IPO. Management’s combined total addressable market estimate reaches approximately $29 trillion, with AI accounting for approximately $26.5 trillion of that figure.

Three specific execution milestones would most directly validate the AI infrastructure premium:

- Starship V3 reaching commercial launch cadence (targeted H2 2026)

- Orbital compute hardware deployment with confirmed throughput metrics

- A verifiable large-scale enterprise compute agreement

Several claims circulating in IPO analysis, including a named SpaceX-Anthropic $15 billion per year compute deal, “Macro Hard” as an enterprise platform, “Colossus 1/2” facility branding, and a 100 GW per year deployment target, have not been confirmed in any SEC filing, Bloomberg, WSJ, Reuters, or named financial press report as of May 2026. Investors should demand primary source confirmation before pricing these into their models.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

What the SpaceX IPO is really asking investors to price: verified assets versus unproven ambitions

The confirmed foundation is real. The xAI acquisition is complete. A gigawatt-scale ground cluster is operational. Orbital compute regulatory filings have been submitted. Starship V3 and Starlink V3 are on track for H2 2026. This is not vapourware.

The discipline required is equally real. Several high-profile AI infrastructure claims attributed to SpaceX management in circulating analysis remain unverified in any primary source as of the 20 May 2026 filing date. Investors who price these in are assuming execution that has not yet been documented.

SpaceX is the only company that simultaneously owns the launch stack, the mega-constellation, and a gigawatt-scale AI cluster. Whether that vertical integration justifies a $2 trillion entry price depends on how much weight investors assign to an orbital compute moat that is architecturally unique but operationally unproven.

For investors who want a structured framework for deciding whether to participate at IPO price rather than waiting for secondary market entry, our deep-dive into the SpaceX IPO valuation walks through the EBITDA multiples, historical IPO underperformance base rates, and the specific execution milestones that analysts say would need to be hit to justify the $2 trillion entry point.

“Building the infrastructure of the future.” — SpaceX S-1, filed 20 May 2026

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.