AI, Railways, and the Case for Surviving the Bubble First

10 hrs ago

South Korean equities sit at the intersection of global technology leadership, structural undervaluation, and active government reform. Companies such as Samsung Electronics and Hyundai Motor dominate their industries worldwide, yet the broader market has traded at a persistent discount to regional peers for decades. The reason is not weak business performance but a specific set of governance and ownership structures that have suppressed shareholder returns and kept international capital at arm’s length. That discount is now the target of the Corporate Value-Up programme, launched in early 2024 and still evolving as of mid-2026, which is pressing listed companies to improve capital efficiency, raise dividends, and strengthen governance. For investors willing to learn the mechanics of this market, the setup combines value with a live catalyst. For those who enter without preparation, the governance complexity, unfamiliar trading rules, and currency exposure can produce unwelcome surprises. This guide covers everything a retail investor needs to understand before placing a first trade in South Korean equities: the origins of the discount, the reform programme, access routes, market structure, currency risk, and portfolio fit.

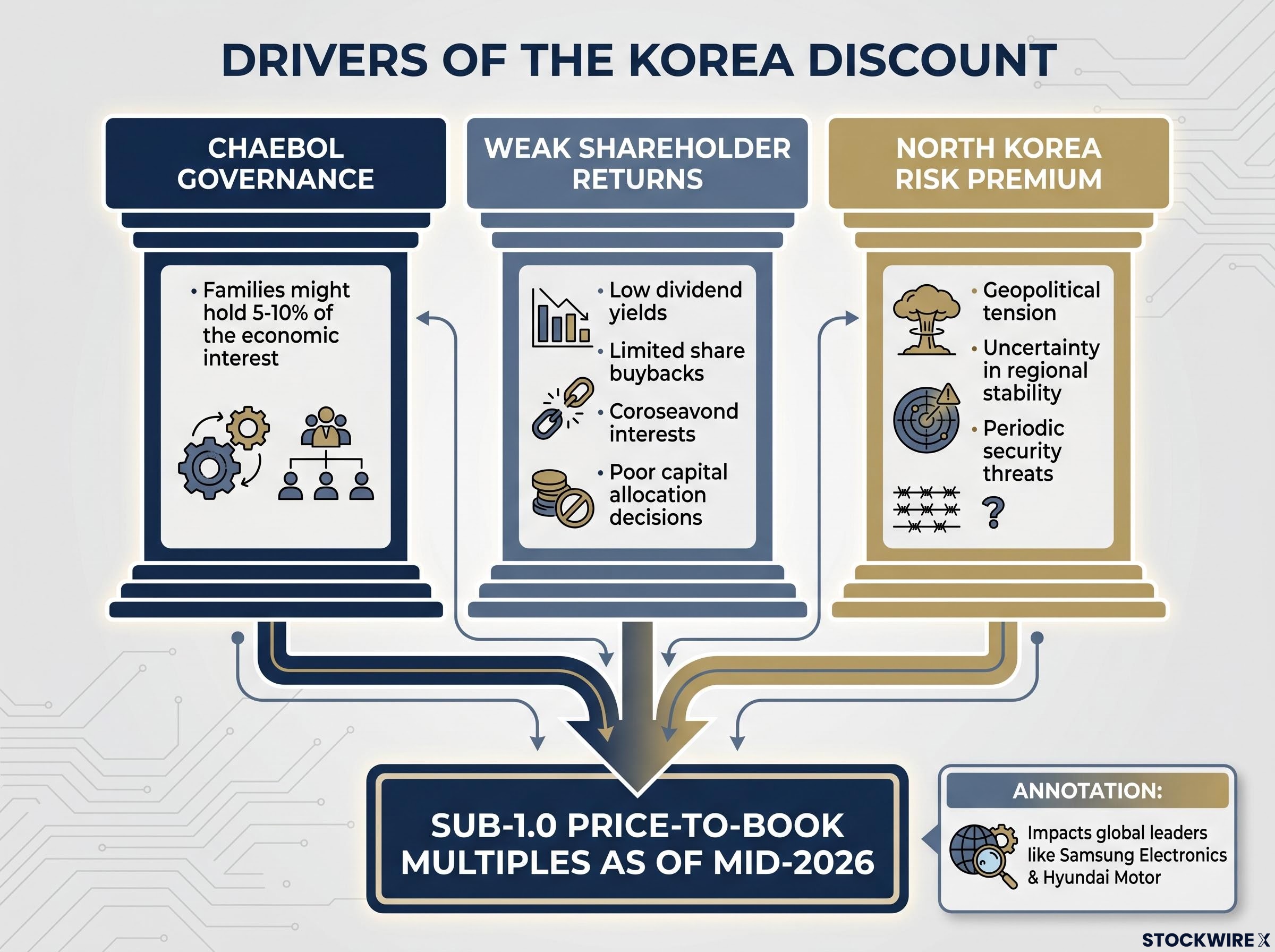

The Korea Discount is not a temporary anomaly or a pricing error waiting to correct itself. It is the predictable output of three structural features that have persisted for years, each reinforcing the others.

Together, these drivers explain why many Korean blue chips still trade at sub-1.0 price-to-book multiples as of mid-2026, despite operating businesses with global scale and competitive advantages.

South Korea’s largest conglomerates, known as chaebols, use complex cross-shareholding pyramids that allow founding families to retain strategic control with relatively small economic stakes. A family might hold 5-10% of the economic interest in a group yet exercise effective control over capital allocation across dozens of subsidiaries.

The consequences for minority shareholders are direct. Capital tends to be hoarded on balance sheets rather than returned. Acquisitions are sometimes made to expand the family’s influence rather than to maximise returns. Return on equity remains lower than it would be if capital allocation were optimised for all shareholders equally.

Korean companies have historically paid lower dividends and conducted fewer buybacks than regional peers with similar earnings profiles. The payout gap has compounded over years into a persistent valuation discount, as income-oriented and total-return-focused investors allocate capital elsewhere.

The North Korea factor operates differently. It is not a constant drag but a periodic shock risk. Escalations on the Korean Peninsula can trigger sharp drawdowns unrelated to company fundamentals, and international investors price that tail risk into valuations at all times. The discount, in other words, is not mysterious. It is logical.

The investment thesis for Korean equities has shifted. The question is no longer simply whether the market is cheap; it is whether an active policy programme can compress the structural discount that has persisted for years. The Corporate Value-Up initiative, launched in early 2024 and still evolving as of mid-2026, represents the most concerted official effort to date.

The programme rests on three reinforcing pillars:

The FSC Corporate Value-Up programme establishes the official policy framework underpinning these reforms, setting out the regulatory expectations for listed companies to publish capital efficiency plans and the incentive structures tied to compliance.

Evidence of behavioural change is emerging. Rising dividend payout ratios and more frequent buyback announcements have appeared at large and mid-cap firms, particularly those with high foreign ownership. More companies are explicitly referencing capital efficiency in their medium-term plans.

Global asset managers increasingly frame South Korea alongside Japan as a governance-reform story, where policy pressure is attempting to unlock value trapped inside listed companies by decades of structural underinvestment in shareholder returns.

Japan’s governance reform offers the closest historical parallel to what Korea’s Value-Up programme is attempting, with the Tokyo Stock Exchange’s capital efficiency push lifting average TOPIX price-to-book from 1.1x to 1.5x since 2023 and demonstrating that policy-driven multiple expansion is achievable when corporate behaviour actually shifts.

If valuations move even part of the way toward regional averages, the upside comes not from earnings growth alone but from multiple expansion, the compression of governance and capital-return risk premia that have weighed on Korean multiples for years. The reform programme does not guarantee that outcome, but it provides the most credible catalyst the market has had.

Three routes exist, each suited to a different level of commitment and complexity. Presented here in ascending order, investors can self-select the entry point that matches their resources and objectives.

| Access Route | Complexity | Cost | Flexibility |

|---|---|---|---|

| ETFs and funds | Low | Fund management fees; no direct FX costs | Broad market exposure only; no single-stock selection |

| International broker (direct KRX) | Moderate | Brokerage commissions plus FX conversion spreads | Full KOSPI and KOSDAQ access; single-stock selection |

| Domestic Korean broker | High | Potentially lower local commissions; higher setup cost | Deepest access; best for specialised or larger investors |

Most global retail investors assume Korean stocks are difficult to access. In practice, the simplest route requires nothing beyond an existing brokerage account or a single ETF purchase.

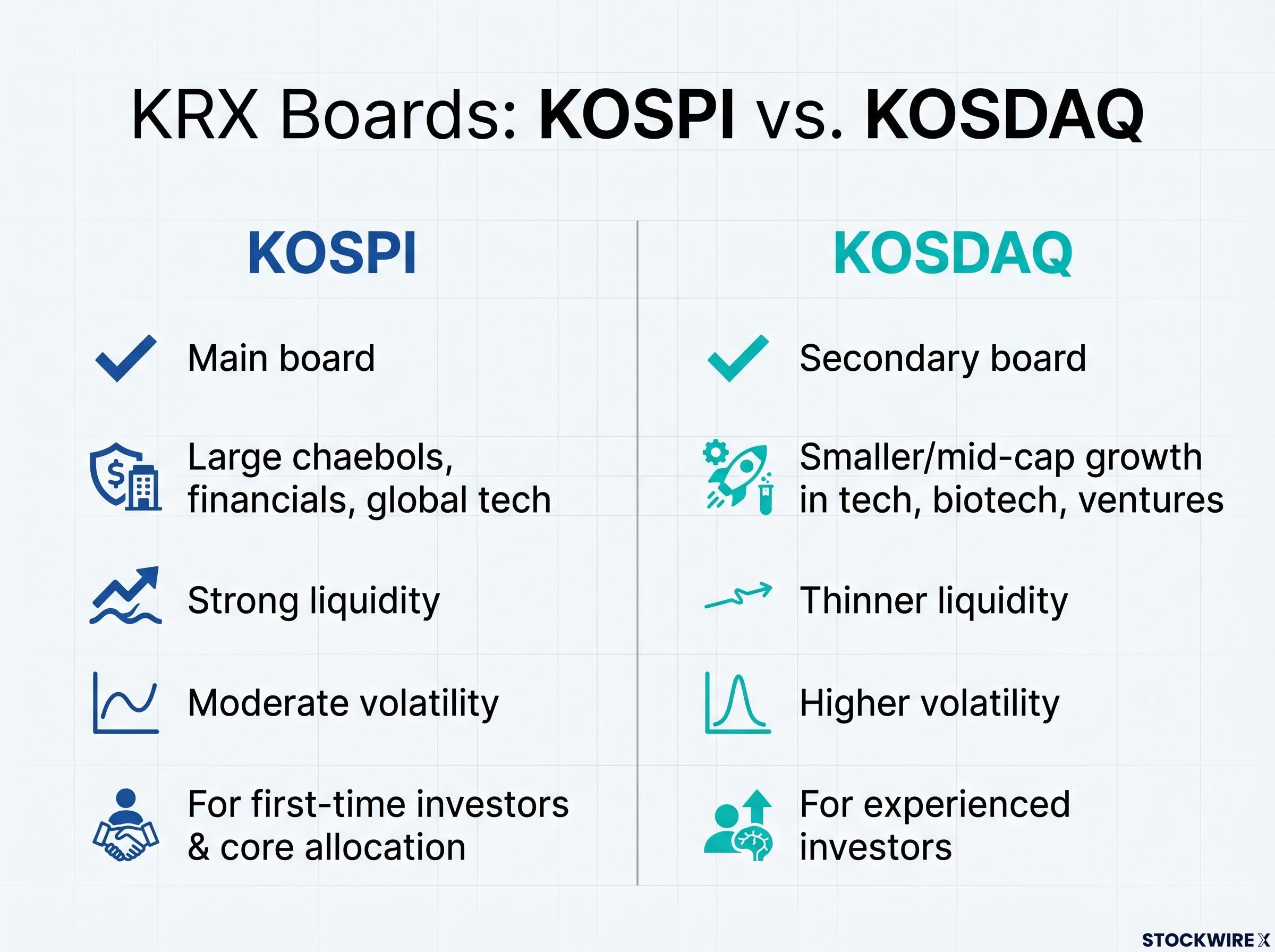

The Korea Exchange operates differently from the US, European, or Australian markets most retail investors are familiar with. Understanding three specific features, the dual-board structure, trading hours, and daily price limits, removes the operational surprises that catch unprepared investors.

The KRX runs two distinct boards, each with a different character.

| Attribute | KOSPI | KOSDAQ |

|---|---|---|

| Board type | Main board | Secondary board |

| Company profile | Large, established chaebol names, financials, global tech leaders | Smaller and mid-cap growth companies in tech, biotech, ventures |

| Typical liquidity | Strong; tight bid-ask spreads for index heavyweights | Thinner; larger price impact when trading in size |

| Volatility level | Moderate | Higher; prone to sharp moves on news flow |

| Suitable for | First-time Korea investors; core allocation | Experienced investors comfortable with higher risk |

For a first position, KOSPI large caps or diversified vehicles offer the most manageable entry point. KOSDAQ names can offer higher upside but demand greater comfort with volatility and thinner liquidity.

The practical implications of the dual-board structure go deeper than the summary comparison above; KOSPI vs KOSDAQ allocation requires understanding how Samsung Electronics and SK Hynix together can represent over 40% of the main board benchmark, meaning a sell-off in either name transmits as a broad market decline through passive ETF redemption mechanics.

The Korea Exchange operates Monday through Friday, 9:00 AM to 3:30 PM Korean Standard Time (KST), corresponding to 8:00 AM to 2:30 PM Singapore Time (SGT). The full session falls within a normal Asian business day, making Korean equities particularly convenient for Southeast Asian-based investors who can monitor positions in real time during standard working hours.

The daily price movement limit is the mechanic most likely to surprise investors from Western markets. KRX imposes a limit of plus or minus 30% around the previous close on individual stocks, confirmed current as of mid-2026. Market-wide circuit breakers also exist during episodes of extreme volatility.

The practical implications are specific and worth internalising before trading:

Understanding this mechanic in advance prevents panic and misjudged orders during volatile sessions.

Currency is not a footnote in cross-border equity investing. It is a second return driver that can silently amplify or undermine equity gains.

Regardless of what currency a broker uses to settle the trade, the underlying exposure is always to KRW. Total return equals stock performance in KRW, plus or minus the change in KRW against the investor’s home currency over the holding period.

The Korean won is sensitive to global risk sentiment and US dollar moves. Korean equities can deliver strong KRW returns but weak home-currency returns in a risk-off period when the won depreciates against the dollar, euro, or Singapore dollar. The reverse also applies: won strength during risk-on periods can add a tailwind to equity gains.

Practical FX cost considerations deserve attention before committing capital:

Currency risk is the most commonly underestimated variable in cross-border equity investing. Investors who ignore KRW exposure may find their equity returns dramatically altered by won movements in either direction.

Risk assessment done upfront, rather than after an adverse event, allows investors to size positions appropriately and set realistic expectations. The six risks below are ordered from structural to situational, reflecting the distinction between risks that affect the investment thesis itself and risks that create periodic volatility around it.

These are slow-moving risks, but they are foundational. They determine whether the core investment thesis, value plus reform catalyst, ultimately delivers.

Korean regulatory enforcement can move quickly and with significant consequences for listed companies, as illustrated when South Korea revoked Coupang’s corporate group exemption and subjected the U.S.-listed firm to strict antitrust frameworks around cross-shareholding, debt guarantees, and related-party transactions, the same categories of behaviour the Corporate Value-Up programme is pressing all listed groups to reform.

These risks are more event-driven and manageable with appropriate position sizing, broker selection, and awareness. None of them invalidates the investment case, but each requires conscious preparation.

Korean equities are best understood as a satellite allocation sitting around a diversified global or regional core. Global and emerging market indices already include South Korea, but often at a weight that does not fully reflect the potential upside from reform-driven multiple expansion.

The sector concentration reality matters for portfolio construction. Korean equities are heavily weighted toward:

Investors should check for overlap with existing global technology and industrial holdings before adding Korea-specific exposure. A mid-single-digit percentage of total equities serves as a practical starting point, adjusted for individual risk tolerance.

The following checklist converts this guide into an action sequence:

South Korean equities are not simply cheap. They are cheap with a reform catalyst, and the combination of structural discount plus official policy pressure to close it creates a risk-reward profile not easily replicated elsewhere in global equity markets.

The risks are genuine. Governance enforcement will be uneven across companies. Geopolitical noise will create periodic volatility. Currency movements will add a second layer of return uncertainty. None of these risks are trivial, but all of them are manageable with appropriate position sizing, a well-chosen broker setup, and a time horizon that accommodates the multi-year nature of reform.

The Corporate Value-Up programme is still evolving as of mid-2026. Investors who do the structural work now, understanding the discount’s origins, the reform mechanics, the market’s operational features, and the currency dynamics, position themselves to benefit from milestones that have not yet fully materialised.

For investors who have decided to enter Korean equities and want to see how institutional risk management frameworks apply in practice, our deep-dive into Citigroup’s KOSPI position management examines how a major bank weighed overbought signals, record retail margin debt, and tightening global yields to close half a long position while preserving upside exposure through the remaining stake.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements regarding reform outcomes are subject to change based on political, corporate, and market developments.

—

The Korea Discount refers to the persistent gap between the valuations of South Korean listed companies and their regional peers, caused by chaebol governance structures that concentrate family control, historically low dividend payouts, and a geopolitical risk premium tied to North Korea. Many Korean blue chips still trade at sub-1.0 price-to-book multiples despite operating globally competitive businesses.

Launched in early 2024 and still evolving as of mid-2026, the Corporate Value-Up programme is a government initiative that urges listed companies with low valuations to publish capital efficiency plans, increase dividends, and strengthen board governance, supported by Commercial Code amendments and tax incentives designed to make shareholder-friendly behaviour more attractive.

Retail investors can access South Korean equities through three main routes: Korea-focused ETFs tracking indices such as MSCI Korea, direct trading on the Korea Exchange via an international broker using six-digit numeric tickers, or opening an account with a domestic Korean broker for deeper local market access.

The Korea Exchange imposes a daily price movement limit of plus or minus 30% around the previous close on individual stocks, meaning a stock can hit its limit and become effectively illiquid until the next session, a risk that is particularly acute for smaller KOSDAQ names where queued sellers can trap investors for multiple sessions.

All South Korean equity investments carry Korean won (KRW) exposure regardless of the settlement currency a broker uses, so total returns are determined by both the stock's performance in KRW and the movement of KRW against the investor's home currency, which can meaningfully amplify or offset equity gains during risk-off periods when the won typically weakens.