Software Stocks Fell 16% on AI Fears With No Disruption Evidence

Key Takeaways

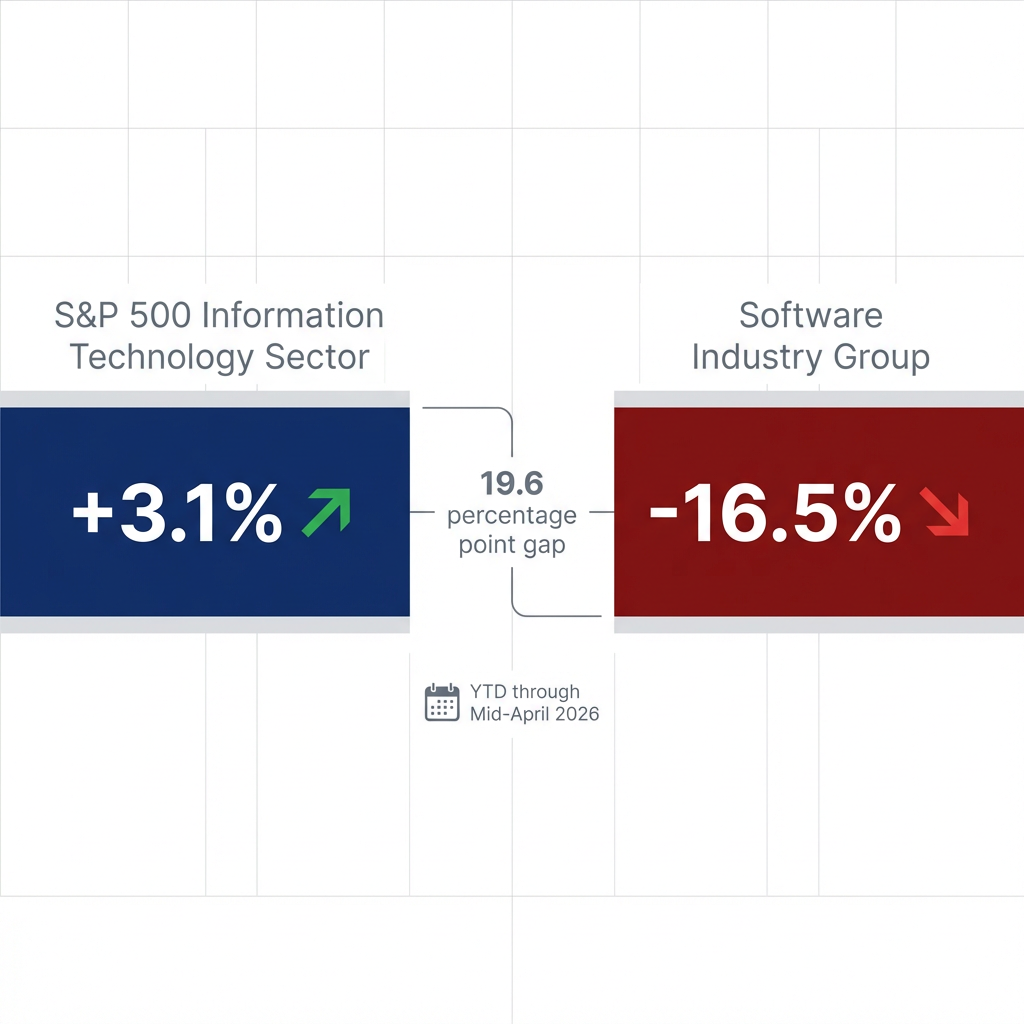

- The software sector fell 16.5% year-to-date through mid-April 2026, dramatically underperforming the broader S&P 500 IT sector's 3.1% gain, despite an absence of concrete AI disruption evidence in corporate earnings or analyst reports.

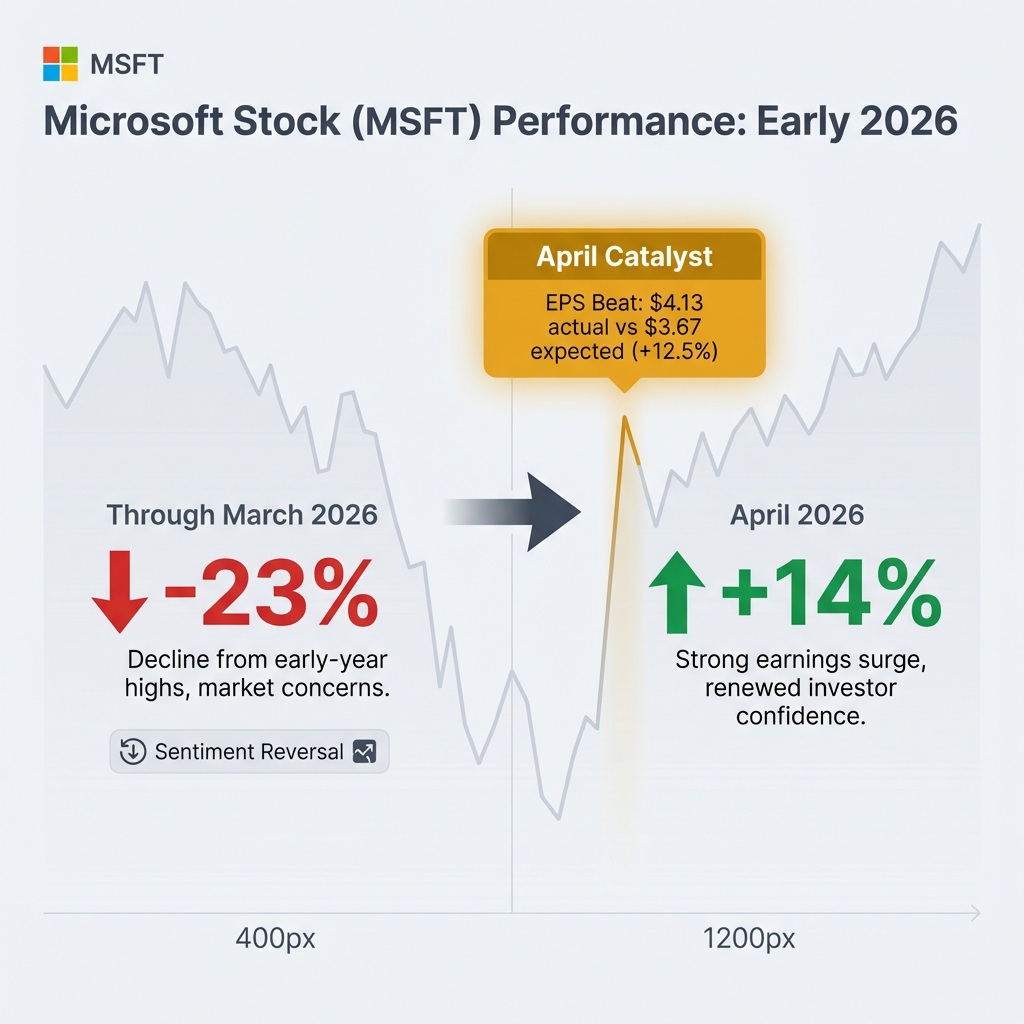

- Microsoft beat Q1 2026 earnings expectations by 12.5%, reporting EPS of $4.13 versus the $3.67 consensus, signalling that the largest software incumbent is benefiting from AI integration rather than being disrupted by it.

- April 2026 saw a significant recovery, with the S&P Software and Services Select Industry Index gaining 6.36% month-to-date and Microsoft rallying 14% after a 23% decline through March, suggesting markets may be recalibrating AI disruption fears.

- No revenue warnings citing AI competition have emerged from major software companies including Salesforce, Adobe, ServiceNow, Oracle, or SAP, making the absence of such SEC-mandated disclosures a materially bullish signal for the sector.

- Investors should monitor specific warning signs including customer retention declines, management commentary on pricing pressure, and AI-native competitors winning enterprise contracts before concluding that disruption fears are materialising.

The software industry is enduring its most severe test since the dot-com bubble. Whilst the broader S&P 500 Information Technology sector advanced 3.1% year-to-date through mid-April 2026, the software industry group plummeted 16.5% over the same period, according to index data. This dramatic divergence has ignited debate over whether artificial intelligence represents an existential threat to traditional software business models or whether fear has driven irrational selling disconnected from fundamental performance.

Recent recovery signals complicate the narrative. Microsoft rallied 14% in April after declining 23% through March, whilst the S&P Software & Services Select Industry Index gained 6.36% month-to-date as of 16 April 2026, reaching 13,268.05. These rebounds raise a critical question: does the available evidence support AI disruption fears, or has the market overreacted to theoretical threats that have yet to materialise in corporate earnings and competitive dynamics?

Understanding AI Disruption Fears in the Software Sector

AI disruption concerns centre on the possibility that generative AI and AI-native startups could render traditional software products obsolete or commoditised. The thesis driving software stocks’ 16.5% year-to-date decline rests on several pillars. Generative AI could automate tasks that currently require paid software subscriptions, AI-native competitors might undercut pricing with superior technology, and point solutions could be replaced by versatile AI tools that handle multiple functions.

Investors fear four primary disruption scenarios:

- AI automating workflows that currently require enterprise software licences

- AI-native startups offering cheaper alternatives built on newer architectures

- Generative AI replacing specialised tools with general-purpose capabilities

- Reduced pricing power as AI commoditises features that once commanded premium prices

This theoretical framework has driven significant capital rotation. However, established software companies possess substantial resources to integrate AI into existing products, raising questions about whether incumbents can adapt faster than new entrants can disrupt. The central analytical challenge lies in distinguishing between genuine competitive threats and market overreaction to technological change.

Understanding the theoretical framework for AI disruption and why massive AI investments may not deliver expected returns provides essential context for evaluating whether current software stock fears are justified.

When big ASX news breaks, our subscribers know first

What the Data Actually Shows: Disruption Evidence Is Thin

Despite dramatic stock price declines, concrete evidence of AI-native companies disrupting established software players remains notably absent from Q1-Q2 2026 market data. No major product launches by AI-first startups have displaced incumbents, no revenue warnings from Microsoft, Salesforce, Adobe, ServiceNow, Oracle, or SAP have cited AI competition, and no documented customer defections to AI alternatives have emerged in quarterly reports through mid-April.

Under SEC guidance on AI risk disclosures, publicly traded software companies must clearly articulate material competitive threats from AI in their regulatory filings, making the absence of such warnings in recent quarterly reports particularly significant.

> Microsoft delivered actual earnings per share of $4.13 versus analyst expectations of $3.67, demonstrating that the largest software company is navigating the AI transition successfully rather than facing disruption.

The silence from Wall Street analysts proves equally telling. No April 2026 downgrades or sector reports have specifically warned about AI vulnerability in traditional software companies. When analysts refrain from raising red flags despite significant stock declines, it often signals confidence in companies’ adaptation strategies. The S&P 500 has posted 20 consecutive quarters of revenue growth, with rising net profit margins projected to reach 13.7% through Q2 2026, suggesting underlying business fundamentals remain intact despite AI concerns.

The substantial AI spending supporting market fundamentals suggests that technology infrastructure investments may ultimately benefit established software companies with distribution advantages rather than disrupt them.

Recovery Signals: Why Software Stocks Are Rebounding

April’s sharp recovery suggests markets may be recalibrating AI disruption fears. Microsoft’s dramatic reversal, down 23% through March then rallying 14% in April, represents a significant sentiment shift potentially tied to the company’s earnings beat. The strong quarterly performance demonstrates AI is enhancing rather than threatening Microsoft’s competitive position, validating the company’s substantial investments in AI integration.

The software sector’s April recovery aligns with a broader technology sector rally that has driven major indices to all-time highs, suggesting coordinated sentiment shifts across technology investments.

| Metric | Value | Implication |

|---|---|---|

| Software Index MTD Gain | +6.36% | Strong near-term momentum |

| Microsoft April Rally | +14% | Sentiment reversal for sector leader |

| S&P 500 Forward P/E | 22.4 | Markets pricing in growth |

| 2026 Earnings Growth Forecast | +13.9% | Fundamental support intact |

Institutional stability provides additional support for the recovery thesis. No evidence indicates large-scale rotation from software stocks to AI-native alternatives, whilst the S&P 500’s projected 13.9% earnings growth for calendar year 2026 and forward price-to-earnings ratio of 22.4 suggest investors maintain confidence in technology sector fundamentals. The software index’s 1.41% daily gain on 16 April 2026 reinforces positive momentum across multiple timeframes.

The next major ASX story will hit our subscribers first

Key Risks: What Could Validate Disruption Fears

Whilst current evidence of AI disruption remains thin, significant data limitations prevent definitive conclusions about the software sector’s resilience. No granular performance data exists for individual companies including Salesforce, Adobe, ServiceNow, Oracle, or SAP, meaning Microsoft’s success may not reflect universal sector conditions. Smaller software companies or those in specific subsectors could face material competitive threats not yet visible in aggregate indices.

Investors should monitor specific warning signs that could validate AI disruption concerns:

- Revenue guidance cuts citing AI competition in earnings calls

- Customer retention rate declines indicating switching to AI-native alternatives

- Pricing pressure discussed by management as AI commoditises features

- AI-native competitors gaining enterprise traction with Fortune 500 customers

- Analyst downgrades citing specific AI threats with supporting evidence

The absence of disruption today provides no guarantee it will not materialise. Technology transitions often follow non-linear patterns, with incumbent vulnerability emerging suddenly after extended periods of apparent stability. The theoretical case for AI disruption remains plausible even if Q1-Q2 2026 data has not yet validated investor fears.

NBER research on AI economic impacts by economist Daron Acemoglu examines how technology transitions can follow non-linear disruption patterns, with incumbent vulnerability often emerging suddenly after extended stability periods.

Investment Implications: Positioning for Software’s AI Future

Current evidence suggests software stocks AI disruption fears are more theoretical than realised, though selective positioning favouring companies demonstrating successful AI integration remains prudent. The 16.5% year-to-date decline may have created opportunities in companies where market pessimism exceeds fundamental risk. Microsoft’s April recovery, supported by strong earnings that beat analyst expectations by 12.5%, demonstrates that incumbents with resources and distribution advantages can adapt to AI-driven market changes.

Investors evaluating individual software stocks should apply a rigorous analytical framework:

- Examine AI product integration discussed in quarterly earnings calls

- Monitor customer retention metrics for signs of competitive pressure

- Assess pricing power maintenance despite AI-driven feature commoditisation

- Evaluate competitive positioning versus AI-native alternatives in target markets

- Track institutional positioning changes as signals of informed investor sentiment

The April recovery and thin disruption evidence suggest fears may be overblown. However, the transformative nature of AI demands company-by-company analysis rather than blanket sector bullishness. Software companies demonstrating successful AI integration, like Microsoft, appear positioned to benefit from AI advancement rather than suffer disruption. The broader sector recovery may follow as more companies report earnings that validate adaptation strategies over displacement fears.

Investors considering software positions should also examine contrarian perspectives on technology valuations that question whether current recoveries are sustainable given macroeconomic headwinds.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is AI disruption in the software sector?

AI disruption in the software sector refers to the risk that generative AI tools and AI-native startups could render traditional software products obsolete, undercut pricing, or replace specialised applications with general-purpose AI capabilities, reducing revenue and pricing power for incumbent software companies.

Why have software stocks fallen so much in 2026?

The software industry group declined 16.5% year-to-date through mid-April 2026, significantly underperforming the broader S&P 500 IT sector's 3.1% gain, driven by investor fears that AI competition could commoditise software features and erode the business models of established players.

Is there actual evidence that AI is disrupting traditional software companies?

As of mid-April 2026, concrete evidence of AI disruption remains notably absent — no major software companies including Microsoft, Salesforce, Adobe, or Oracle have issued revenue warnings citing AI competition, and Microsoft actually beat earnings expectations by 12.5%, reporting EPS of $4.13 versus the expected $3.67.

What warning signs should investors watch for that could validate AI disruption fears?

Investors should monitor revenue guidance cuts citing AI competition, declining customer retention rates, management commentary on pricing pressure from AI commoditisation, AI-native competitors winning Fortune 500 enterprise contracts, and analyst downgrades specifically attributing weakness to AI threats.

How should investors position themselves in software stocks given AI uncertainty?

Current evidence suggests selective positioning favouring companies demonstrating successful AI integration is prudent, with the 16.5% sector decline potentially creating opportunities where market pessimism exceeds fundamental risk, though company-by-company analysis is essential rather than blanket sector bullishness.