Magnificent Seven Stocks: Analysing the $2.5T Rally

Key Takeaways

- The Magnificent Seven stocks added a record $2.51 trillion in combined market capitalisation over just eight trading days in April 2026, reversing losses that had exceeded $2 trillion from all-time highs.

- The entire rally has been driven by sentiment shifts and fund flows, with no Q1 2026 earnings confirmed yet, making upcoming earnings season a critical test for current valuations.

- Alphabet offers the cheapest valuation among the group at 17x forward earnings, while Tesla's 145x forward P/E has earned it a Sell rating despite strong retail investor interest.

- Analysts recommend only three of the seven stocks as Buys — Nvidia, Alphabet, and Microsoft — underscoring the need for selective stock picking over broad group exposure via ETFs.

- Within technology, software stocks are considered the value play following sharp sell-offs in early 2026, while memory-related semiconductors are the momentum trade driven by AI infrastructure spending.

The Magnificent Seven stocks added $2.51 trillion in combined market capitalisation over eight trading days in April 2026, marking the largest expansion on record for the group. This dramatic reversal follows losses exceeding $2 trillion from all-time highs, signalling renewed investor confidence after months of sustained declines. The seven companies—Meta, Microsoft, Nvidia, Alphabet, Amazon, Apple, and Tesla—have regained momentum as fund flows shift decisively bullish and technical indicators suggest oversold conditions have corrected.

The rally coincides with broader market strength, with the Nasdaq Composite approaching a 13-day winning streak, its longest since January 1992. The Dow Jones Industrial Average gained over 1,000 points on 17 April alone, positioning major indices for their strongest three-week performance since April 2020. For investors who missed the reversal or are considering entry points, the critical question is whether this rebound represents a sustainable recovery or a technical bounce before further volatility.

For investors who missed the reversal or are considering entry points, the critical question is whether this rebound represents a sustainable recovery or a technical bounce before further volatility. Evaluating contrarian perspectives on rally sustainability helps balance the bullish sentiment evident in fund flows and price action.

The rally coincides with broader market strength, with the Nasdaq’s historic 13-day winning streak, its longest since January 1992. This sustained momentum reflects the technical reversal from oversold conditions that had created attractive entry points across technology indices.

What Are the Magnificent Seven Stocks?

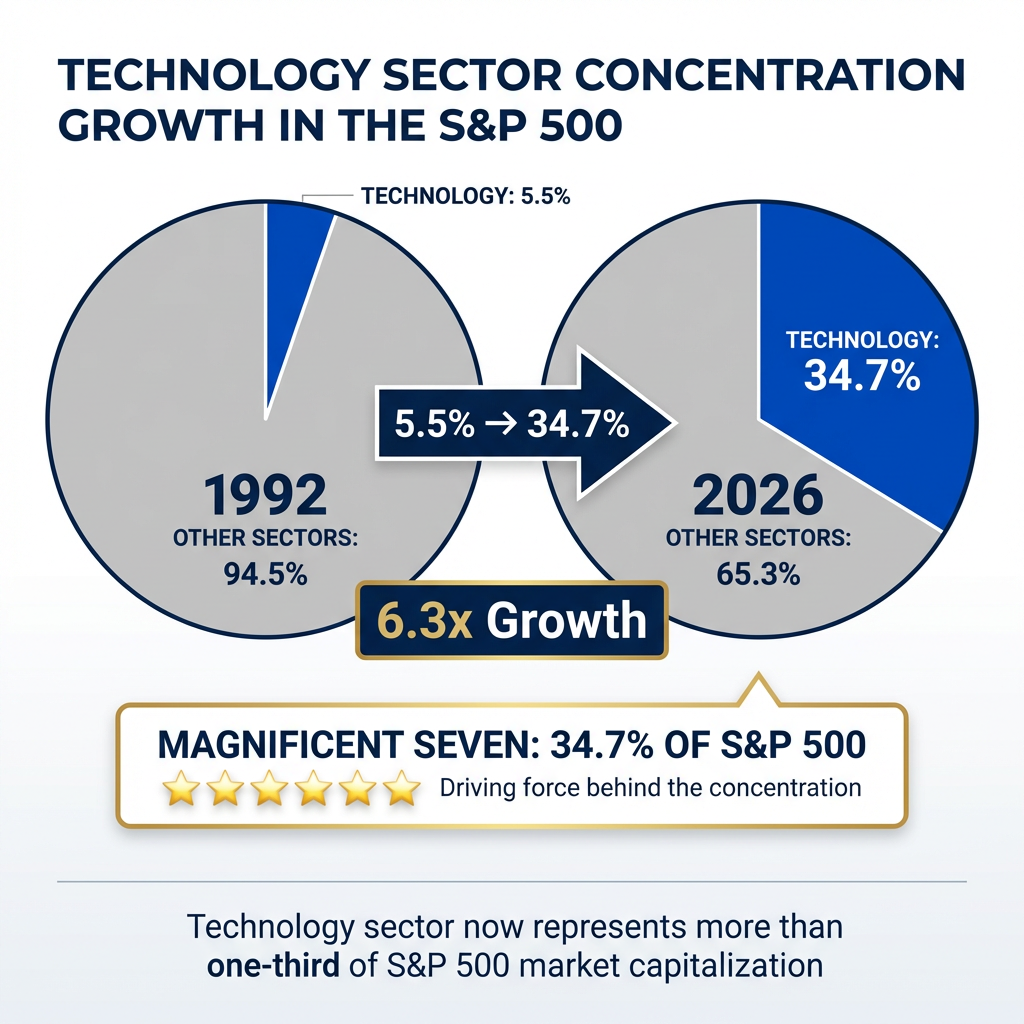

The Magnificent Seven refers to the seven largest technology-focused companies in the S&P 500, collectively representing 34.7% of the index as of April 2026. Their performance disproportionately affects overall market returns due to their scale and concentration. The nickname emerged during the artificial intelligence (AI) investment boom that began in 2023, referencing the classic film to emphasise their dominance.

The seven companies are:

- Apple (consumer electronics and services)

- Microsoft (enterprise software and cloud computing)

- Nvidia (AI semiconductors and graphics processing)

- Alphabet/Google (search, advertising, and cloud infrastructure)

- Amazon (e-commerce and cloud services)

- Meta (social media and metaverse development)

- Tesla (electric vehicles and energy solutions)

The technology sector now represents 34.7% of the S&P 500, compared to just 5.5% in 1992. This concentration means collective movements within the Magnificent Seven can swing the entire market, as demonstrated by the $870 billion loss in a single week ending 27 March 2026. When these companies rally or decline in unison, passive index investors and active fund managers alike feel the impact across portfolios.

The technology sector now represents 34.7% of the S&P 500, compared to just 5.5% in 1992. Federal Reserve research on S&P 500 concentration confirms current market leadership represents historically elevated concentration using the Herfindahl-Hirschman Index, raising questions about systemic risk and passive investing dynamics.

When big ASX news breaks, our subscribers know first

Fund Flows Reverse as Retail Investors Return

Institutional and retail capital flows have shifted decisively bullish during April 2026. The Invesco QQQ Trust recorded a $3 billion inflow on 16 April, the largest single-day intake since $3.1 billion on 19 December 2025. This signals renewed appetite among institutional investors for concentrated technology exposure after months of outflows and defensive positioning.

> “Big Tech had become substantially oversold.”

> Dave Mazza, CEO, Roundhill Investments

The Roundhill Magnificent Seven ETF provides further evidence of the sentiment shift. After experiencing year-to-date outflows through March, fund flows turned positive on 1 April 2026 and accelerated through mid-month. According to Vanda Research, retail investors have returned to popular names, with Tesla emerging as a particular beneficiary despite its 145x forward price-to-earnings ratio and Sell rating from analysts. Earlier guidance warned against blind exposure to MAGS ETF products due to overvaluation in individual holdings, emphasising the need for selective stock picking rather than group-wide investment.

Current Valuations and Performance by Stock

Valuations vary dramatically within the Magnificent Seven, creating divergent risk-reward profiles despite the collective rally. The group’s weighting in the S&P 500 contracted from a peak of 35% to 33%, reflecting both price declines and moderating dominance. Investors evaluating entry points must assess individual company metrics rather than treating the group as a monolithic trade.

Valuations vary dramatically within the Magnificent Seven, creating divergent risk-reward profiles despite the collective rally. FactSet’s institutional valuation methodologies provide the industry-standard framework for forward P/E calculations and earnings estimates used by investment professionals to assess mega-cap technology stocks. Investors evaluating entry points must assess individual company metrics rather than treating the group as a monolithic trade.

| Stock | Forward P/E | YTD Performance | Analyst Rating |

|---|---|---|---|

| Alphabet | 17x | N/A | BUY |

| Meta | 18x | -15.2% | HOLD |

| Apple | 29x | -2% to -5% | HOLD |

| Microsoft | N/A | -23.4% | BUY |

| Nvidia | N/A | N/A | BUY |

| Amazon | N/A | N/A | HOLD |

| Tesla | 145x | N/A | SELL |

Alphabet offers the cheapest valuation at 17x forward earnings, supported by over 90% search market share and Google Cloud growing at over 30% year-on-year. Tesla’s 145x multiple represents the opposite extreme, with analysts rating the stock a Sell despite its popularity among retail investors drawn to the April rally. Apple has demonstrated defensive characteristics, posting the best year-to-date performance (-2% to -5%) as its Apple Intelligence product rollout provides a tangible AI catalyst. Microsoft has been the worst performer (-23.4%), though it retains a BUY rating based on enterprise AI adoption and Azure cloud growth.

Software vs. Semiconductors: Two Trades Within Tech

Within the technology sector, software stocks represent a value play whilst semiconductors, particularly memory chips, offer momentum exposure. Software companies were heavily sold off earlier in 2026 on concerns that AI disruption would erode traditional software business models. The sharp reversal in April suggests value-oriented investors identified oversold conditions and re-entered positions.

> “Software is the value play and semiconductors are the momentum trade.”

> Stephanie Link, Chief Investment Strategist, Hightower Advisors

The iShares Expanded Tech-Software Sector ETF (IGV) gained approximately 14% during the week ending 17 April 2026, closing at $84.94. This represents one of the sharpest weekly rallies in the fund’s history, reflecting aggressive buying after prolonged weakness. Memory-related semiconductor stocks drove momentum factor performance during the same period, benefiting from renewed confidence in AI infrastructure spending and data centre expansion. Investors seeking diversified technology exposure beyond the Magnificent Seven can position tactically based on their style preference, with software offering recovery potential from depressed valuations and semiconductors offering participation in continued AI buildout.

The iShares Expanded Tech-Software Sector ETF (IGV) gained approximately 14% during the week ending 17 April 2026, closing at $84.94. This represents one of the sharpest weekly rallies in the fund’s history, reflecting aggressive buying after prolonged weakness. Understanding the technical factors driving the broader tech recovery helps investors distinguish between Magnificent Seven-specific dynamics and sector-wide momentum.

Memory-related semiconductor stocks drove momentum factor performance during the same period, benefiting from renewed confidence in AI infrastructure capital expenditure trends and data centre expansion. Understanding the scale and durability of this spending cycle is critical for assessing whether semiconductor momentum represents cyclical recovery or structural growth.

The next major ASX story will hit our subscribers first

What to Watch: Earnings Season and AI Capex

No Q1 2026 earnings reports have been released for any Magnificent Seven companies as of mid-April. The $2.51 trillion rally has been driven entirely by sentiment shifts and fund flows, not confirmed fundamental performance. Earnings season will test whether current valuations are justified by revenue growth, margin expansion, and AI monetisation progress.

Key dates and metrics to monitor:

- Meta earnings (late April 2026)

- Apple earnings (early May 2026)

- Alphabet AI capital expenditure guidance (confirm $75 billion+ commitment)

- Google Cloud growth rate (watch for continuation of 30%+ year-on-year expansion)

- Microsoft Azure performance and enterprise AI adoption metrics

- Nvidia forward demand outlook and data centre GPU shipments

Forward price-to-earnings multiples had compressed to multi-year lows before the April rebound, suggesting valuations had corrected from 2023-2025 peaks. The critical question for investors is whether earnings growth will validate current prices or whether multiples will compress again if AI revenue materialisation disappoints. Alphabet’s $75 billion+ AI capex commitment and Google Cloud’s 30%+ growth will be closely watched as indicators of whether infrastructure spending is translating into commercial returns.

Investor Takeaway: Selectivity Over Group Exposure

Analysts recommend only three of the seven stocks as buys: Nvidia, Alphabet, and Microsoft. These receive BUY ratings based on AI growth potential, enterprise adoption, and reasonable valuations relative to growth prospects. Amazon, Meta, and Apple are rated HOLD due to elevated valuations, antitrust concerns, or moderating growth rates. Tesla is rated SELL on overvaluation, with its 145x forward P/E disconnected from automotive industry fundamentals.

The bull case rests on intact AI fundamentals, $75 billion capex commitments, cloud infrastructure growth exceeding 30% year-on-year, and technical rebounds from oversold conditions. The bear case emphasises the $2 trillion loss that preceded this rally, Tesla’s 145x P/E, and the absence of confirmed Q1 2026 earnings to validate current prices. The Magnificent Seven stocks have been characterised as a “mixed bag” requiring individual stock selection rather than group-wide exposure through ETF products.

Investors should monitor Q1 earnings closely for validation of the rally. Favour BUY-rated names with reasonable valuations (Alphabet at 17x forward P/E, Microsoft and Nvidia with enterprise AI tailwinds). Recognise that the 2023-2025 rally mechanics, driven by indiscriminate AI enthusiasm, may not repeat. The era of broad-based gains across all Magnificent Seven stocks appears to be ending, replaced by a market demanding stock-specific catalysts and fundamental justification for premium valuations.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What are the Magnificent Seven stocks?

The Magnificent Seven stocks are Meta, Microsoft, Nvidia, Alphabet, Amazon, Apple, and Tesla — the seven largest technology-focused companies in the S&P 500, collectively representing approximately 34.7% of the index as of April 2026.

Why did the Magnificent Seven stocks rally in April 2026?

The rally was driven by sentiment shifts and fund flows rather than confirmed earnings, with the Invesco QQQ Trust recording a $3 billion single-day inflow on 16 April and retail investors returning to technology names after oversold conditions created attractive entry points.

Which Magnificent Seven stocks are rated Buy by analysts?

Analysts currently rate Nvidia, Alphabet, and Microsoft as Buys, citing AI growth potential, enterprise cloud adoption, and reasonable valuations, while Tesla carries a Sell rating due to its extreme 145x forward price-to-earnings multiple.

Is Tesla a good buy among the Magnificent Seven right now?

Most analysts rate Tesla a Sell despite its popularity in the April 2026 rally, as its 145x forward price-to-earnings ratio is considered disconnected from automotive industry fundamentals and difficult to justify on earnings alone.

What should investors watch in Magnificent Seven earnings season?

Investors should monitor Q1 2026 earnings for Meta and Apple in late April and early May respectively, along with Alphabet's AI capital expenditure guidance of $75 billion or more and Google Cloud's year-on-year growth rate exceeding 30%.