Markets Hit Records as Oil Nears $100: Resilience or Denial?

Key Takeaways

- The S&P 500 has recovered to record highs despite the Iran conflict, but gains are driven by hedge fund short-covering and technical repositioning rather than fundamental risk resolution.

- Crude oil remains just below $100 per barrel — a 45% year-to-date surge — as the Strait of Hormuz closure continues with no clear reopening timeline as of mid-April 2026.

- Bond markets are signalling greater concern than equities, with yields remaining elevated and all prior rate cut expectations erased as energy-driven inflation hits a 25-year high.

- The IMF has warned that sustained elevated energy prices could reduce global economic growth to levels comparable to the Covid-19 pandemic period.

- HSBC's multi-asset strategy team flagged a critical meta-risk: resilient markets may embolden further geopolitical risk-taking, creating a feedback loop that could ultimately overwhelm market stability.

The worst-case scenario materialised. A widening Middle East conflagration, the Strait of Hormuz shuttered, oil prices surging towards $100 per barrel. Yet seven weeks into the crisis, the S&P 500 stands at record highs, having fully erased March losses.

This counterintuitive market response raises a fundamental question: has investor resilience displaced genuine risk assessment, or do markets see pathways to normalisation that remain invisible in diplomatic channels? The Iran conflict market impact has unfolded through three distinct phases since early March 2026. Initial panic drove sharp risk-off moves and energy price spikes. A tentative stabilisation followed as markets absorbed the shock. Recent ceasefire developments sparked rallies driven by hedge fund repositioning rather than fundamental resolution.

Crude oil remains just below $100 per barrel, representing a 45% year-to-date increase. Government bond yields have stabilised at elevated levels, reflecting sustained inflation concerns. The recovery, however, rests on fragile foundations: temporary truce arrangements, short-covering by leveraged funds, and hope rather than evidence of supply normalisation.

Understanding Market Response to Geopolitical Shocks

Markets respond to geopolitical events through mechanisms that often appear counterintuitive to observers expecting linear cause-and-effect relationships. The recent rallies reflect technical repositioning by hedge funds unwinding bearish bets, rather than conviction that fundamental risks have been resolved.

Three concepts help explain current market dynamics:

- Backwardation: When near-term oil futures trade at higher prices than longer-dated contracts, signalling tight immediate supply. The current steep backwardation in crude futures indicates physical demand exceeds available barrels, despite prices approaching $100.

- Safe-haven flows: Capital movements to perceived safe assets during uncertainty. Typically, the US dollar and gold attract inflows during crises. This time, the dollar underperformed during peak hostilities, whilst gold has attracted renewed speculative interest.

- Short-covering rallies: Price increases driven by traders closing bearish positions rather than new buying conviction. Recent equity gains largely reflect this dynamic, creating upward momentum that may not withstand renewed geopolitical setbacks.

The safe-haven demand for gold has intensified globally during the crisis, with investors in major markets shifting toward investment-oriented products as geopolitical uncertainty persists.

The distinction between positioning-driven moves and fundamentally-driven trends becomes critical when assessing rally durability. Current price action suggests the former dominates.

When big ASX news breaks, our subscribers know first

The Oil Price Shock: Strait of Hormuz and Energy Market Turmoil

The Strait of Hormuz closure represents the most significant supply disruption to global energy markets in decades. This narrow waterway, through which approximately one-fifth of global oil supply typically transits, remains closed with no clear reopening timeline as of mid-April 2026.

According to the U.S. Energy Information Administration’s chokepoint analysis, one-fifth of global oil supply typically transits this strategic waterway, making it the world’s most critical energy infrastructure point.

| Metric | Current Level | Change |

|---|---|---|

| Brent/WTI Crude | Just below $100/barrel | +45% YTD |

| Energy Price Inflation | 25-year high | Per UBS calculations |

| Futures Curve | Steep backwardation | Signals sustained supply stress |

| Strait Status | Closed | No reopening timeline |

The International Monetary Fund has warned that sustained conditions at current levels could reduce global economic growth to rates comparable to the Covid-19 pandemic period. This is not merely a financial market event but an economic shock with transmission mechanisms extending far beyond petrol prices. Energy-intensive manufacturing faces margin compression. Transport costs elevate consumer goods prices globally. Households confront the steepest energy price inflation in 25 years, according to UBS calculations.

The International Energy Agency has characterized the current situation as the greatest global energy security challenge in history, with implications extending far beyond immediate price movements to fundamental questions about energy infrastructure resilience.

Backwardation in the futures curve, where near-term contracts trade at premiums to longer-dated ones, signals that physical demand continues to exceed available supply despite elevated prices. This market structure typically persists until either demand destruction occurs or new supply routes normalise. Neither development appears imminent.

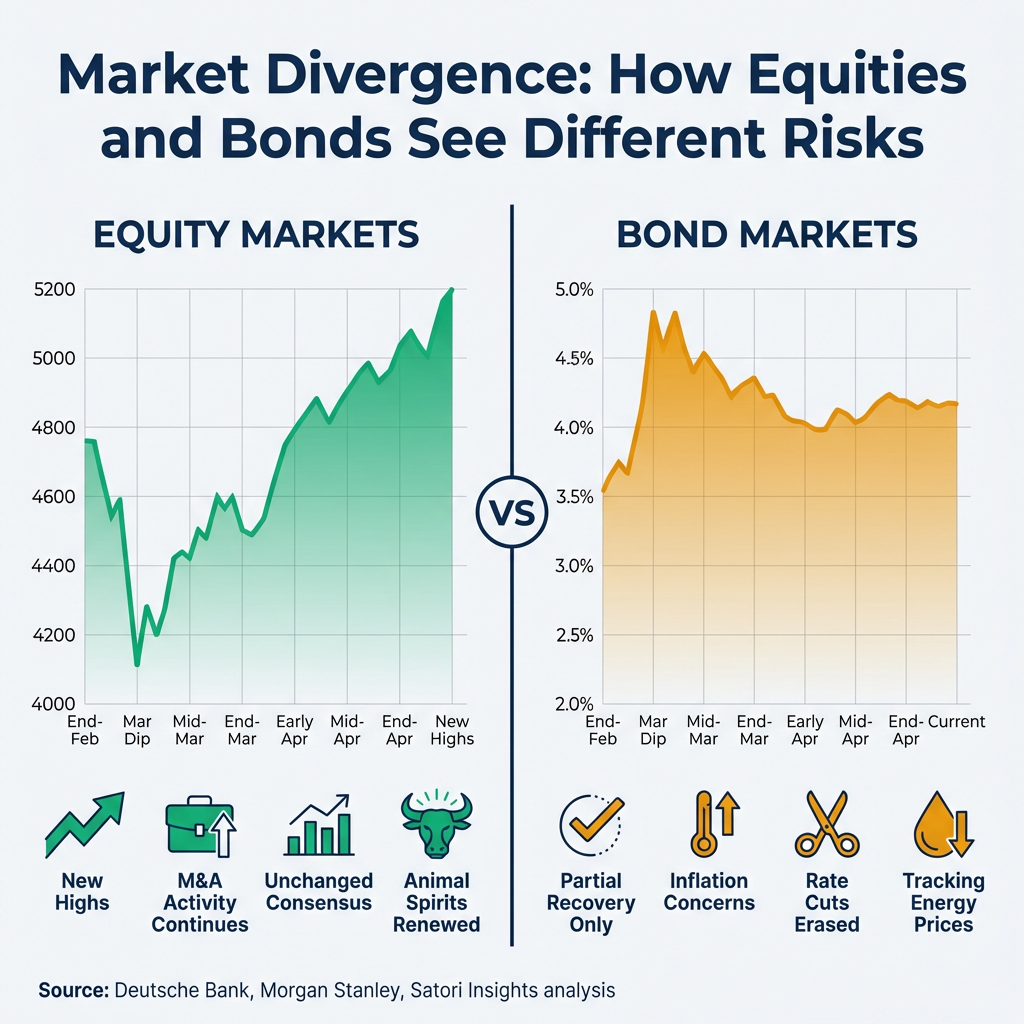

Stock and Bond Markets: A Tale of Divergent Responses

A notable divergence has emerged between equity and fixed income markets’ interpretation of the crisis. The S&P 500 fully recovered March losses and reached record highs. Government bonds, whilst stabilising, have not similarly recovered. Yields remain elevated compared to six weeks ago.

For detailed analysis of how markets absorbed and dismissed the initial shock despite an 8% drawdown, readers can explore the technical and positioning factors that enabled the rapid recovery.

Jim Reid at Deutsche Bank identified bonds as showing greater sensitivity to Iran developments than equities. This divergence reflects multiple underlying dynamics rather than a single explanation.

Equity Markets:

- Full recovery to new highs despite ongoing conflict

- Supported by unchanged corporate earnings consensus

- Hedge fund short-covering driving recent gains

- “Animal spirits” renewed as AI sentiment shifted from failure concerns to success optimism, per Andrew Sheets at Morgan Stanley

- Continued M&A and capital expenditure activity

Bond Markets:

- Partial recovery only, yields elevated versus pre-conflict levels

- Tracking energy prices more closely than equities

- Reflecting inflation concerns and erased rate cut expectations

- Prior AI-driven recession concerns may have caused mispricing

- Supply-shock inflation creating central bank policy uncertainty

Matt King at Satori Insights observed that corporate earnings consensus remains essentially unchanged. Unless the conflict materially impacts corporate performance, this view suggests equities will maintain resilience. Morgan Stanley’s Andrew Sheets noted a critical shift in AI narrative. Market concerns evolved from “AI will fail” to “AI success creates monopolistic winners”. This sentiment shift, combined with what Sheets characterises as renewed animal spirits, helps explain equity market strength despite geopolitical uncertainty.

The divergence raises questions about which asset class correctly prices underlying risk. Bonds may be signalling inflation persistence that equity markets underestimate. Alternatively, equities may be accurately assessing limited economic damage if diplomatic progress continues.

Inflation Fears and the Central Bank Dilemma

The conflict has fundamentally altered the monetary policy landscape. Rate cut expectations that existed before the war have been completely erased. Bond yields have risen as markets price either sustained inflation or potential rate hikes. This reflects the 25-year energy price inflation surge rippling through global economies.

Understanding why energy prices have become the dominant force driving inflation in 2026 is essential for assessing the central bank policy trade-offs discussed throughout this analysis.

Central banks face a difficult policy dilemma. Supply-shock inflation differs fundamentally from demand-driven inflation. Traditional monetary policy tools (interest rate hikes) address excess demand but prove less effective against supply constraints. Raising rates during a supply shock risks exacerbating economic slowdown without materially addressing the inflation source.

The Bank for International Settlements analysis on central bank dilemmas during stagflationary episodes outlines how supply-shock inflation creates fundamentally different policy challenges than demand-driven price pressures.

The HSBC multi-asset strategy team identified premature aggressive rate hikes as a key risk. Tightening policy too aggressively could tip economies into recession whilst energy prices remain elevated. Conversely, inaction risks inflation expectations becoming unanchored, requiring more painful adjustment later. This trade-off has no clear resolution whilst the Strait of Hormuz remains closed and energy supply uncertain.

The next major ASX story will hit our subscribers first

The Ceasefire Factor: Rally on Thin Ice?

The temporary US-Iran truce sparked the recent market rally. However, this reflects technical positioning rather than fundamental conviction that risks have been resolved. Hedge funds unwound bearish positions. Short-covering drove prices higher. The rally’s foundation rests on hope that conditions will continue improving, not evidence that underlying issues have been addressed.

Critical questions remain unanswered:

- Durability of the temporary truce arrangement and diplomatic framework supporting it

- Timeline for Strait of Hormuz reopening and normalisation of shipping traffic

- Extent of energy infrastructure damage and requirements for repair

- Risk of renewed escalation if diplomatic progress stalls

- Mechanisms for verifying compliance and managing future disputes

The HSBC multi-asset strategy team noted that conditions only need to become “less bad” rather than fully normalised to sustain market recovery. The rate of change matters more than absolute levels. This observation helps explain recent rallies despite ongoing challenges. However, HSBC also acknowledged that complacency warnings will proliferate. Markets trading on momentum and positioning rather than fundamentals create vulnerability to headline risk.

No clear Strait reopening timeline exists. Progress towards resuming traffic contributed to recent optimism, but normalisation remains incomplete. The coming weeks will prove critical for determining whether tentative stability holds or gives way to renewed volatility.

What Comes Next: Risks, Scenarios, and Market Vulnerabilities

The HSBC multi-asset strategy team identified a meta-risk that may prove more significant than individual threats: buoyant markets could encourage the administration to push geopolitical boundaries further, increasing accident probability. This creates a feedback loop where market resilience enables risk-taking that could eventually overwhelm that same resilience.

Three primary risks dominate the outlook:

- Significant further oil price spike triggering US recession: If crude surges materially above $100 per barrel, demand destruction and economic slowdown become increasingly likely. The IMF has warned that sustained elevated energy prices could reduce global growth to pandemic-era levels.

- Premature aggressive rate hikes by central banks: Policy-makers responding to inflation fears with rate increases risk exacerbating economic weakness from the supply shock. This represents the classic central bank dilemma during stagflationary episodes.

- Ceasefire collapse and renewed escalation: The temporary truce remains fragile. Diplomatic setbacks or renewed hostilities would likely trigger sharp risk-off moves, unwinding recent gains rapidly.

The broader geopolitical context adds complexity. NATO stability has been characterised as under threat. Governments face pressure to increase defence spending, creating fiscal constraints that limit economic policy flexibility. The intersection of these dynamics with energy market stress creates a risk matrix where multiple negative scenarios could reinforce one another.

The coming six weeks will prove critical. Markets have had sufficient time to unwind extreme positioning from the initial shock phase. Whether current price levels prove sustainable depends on concrete progress towards Strait reopening, sustained ceasefire implementation, and evidence that energy supply can normalise without triggering recession.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is the Iran conflict market impact on oil prices in 2026?

The Iran conflict has driven Brent and WTI crude oil prices to just below $100 per barrel, representing a 45% year-to-date increase, as the closure of the Strait of Hormuz — through which roughly one-fifth of global oil supply transits — has created the most significant supply disruption to energy markets in decades.

Why is the S&P 500 at record highs despite the Iran conflict?

The S&P 500's recovery to record highs is largely driven by technical repositioning, with hedge funds unwinding bearish short positions rather than genuine conviction that geopolitical risks have been resolved, alongside a sentiment shift in AI narratives and unchanged corporate earnings consensus.

What is a short-covering rally and why does it matter for investors?

A short-covering rally occurs when traders close their bearish positions by buying back assets, pushing prices higher without new buying conviction — the current equity gains are largely attributed to this dynamic, meaning the rally may not hold if geopolitical conditions deteriorate again.

How does the Strait of Hormuz closure affect inflation and central bank policy?

The closure has triggered the steepest energy price inflation in 25 years according to UBS, completely erasing prior rate cut expectations and forcing central banks into a difficult dilemma between hiking rates to combat inflation or holding steady to avoid worsening an economic slowdown caused by the supply shock.

What are the biggest risks to markets if the Iran ceasefire collapses?

The three primary risks identified are a further oil price spike above $100 per barrel triggering a US recession, premature aggressive rate hikes by central banks worsening a stagflationary episode, and a ceasefire collapse leading to renewed escalation that would rapidly unwind recent market gains.