Iran Conflict Triggers Biggest Energy Crisis in History

Key Takeaways

- The Iran conflict has created what the IEA describes as the greatest global energy security challenge in history, with Brent crude surging past $120 per barrel and WTI futures rising 69% over six weeks.

- Asian LNG spot prices jumped over 140% following Iran's attack on Qatar's Ras Laffan Industrial City, with Qatar's damaged facilities estimated to require 3-5 years to fully repair.

- The conflict extends beyond energy markets, driving an 8% rise in aluminum prices and threatening nitrogen fertilizer supply chains that could push food costs higher through 2026.

- Under the adverse scenario, oil prices could remain in the $100-125 range into the second half of 2026, forcing central banks to delay or reverse expected interest rate cuts due to persistent inflation pressure.

- Investors are advised to avoid reactive portfolio moves driven by daily price swings, as infrastructure damage creates price floors that geopolitical settlements alone cannot quickly eliminate.

The Iran conflict that began on February 28, 2026 has triggered what the International Energy Agency describes as the “greatest global energy security challenge in history”. A temporary ceasefire took effect in mid-April, but uncertainty persists across energy markets, equities, and commodities as infrastructure damage creates lasting supply constraints.

The International Energy Agency’s analysis of unprecedented energy security challenges provides regulatory context for understanding how this conflict compares to previous disruptions including the 1970s oil embargoes and 1990s Gulf conflicts.

Iran Conflict Triggers Historic Market Disruption

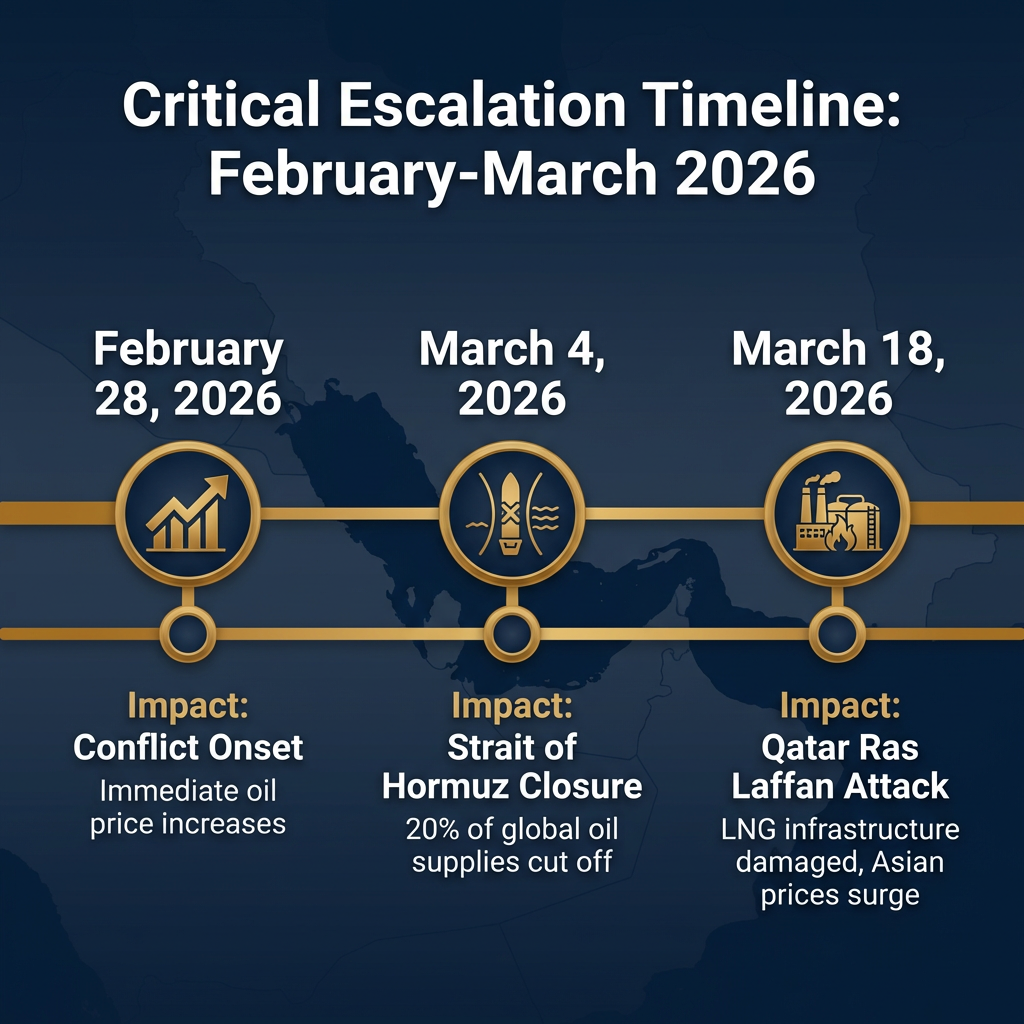

The conflict escalated rapidly through three critical events. Iran closed the Strait of Hormuz on March 4, 2026, disrupting 20% of global oil supplies and significant LNG volumes. On March 18, 2026, Iran attacked Qatar’s Ras Laffan Industrial City complex, one of the world’s largest LNG export hubs. These actions created the largest supply disruption in the history of the global oil market, according to the IEA.

Key escalation timeline:

- February 28, 2026: Conflict onset, immediate oil price increases as markets priced geopolitical risk premium

- March 4, 2026: Strait of Hormuz closure cut off critical oil and LNG transit route, triggering supply crisis

- March 18, 2026: Qatar Ras Laffan attack damaged irreplaceable LNG infrastructure, sending Asian spot prices surging

The mid-April ceasefire has reduced immediate escalation risks, but physical infrastructure damage and supply chain disruptions continue to affect global markets. Analysts caution that even rapid conflict resolution cannot quickly restore pre-war supply conditions.

When big ASX news breaks, our subscribers know first

Understanding Why the Strait of Hormuz Matters

The Strait of Hormuz functions as the world’s most critical oil chokepoint, with 20% of global oil supplies transiting through this narrow waterway. Unlike pipeline disruptions that can be partially rerouted, maritime chokepoint closures eliminate entire supply routes overnight. Iran’s March 4 closure immediately removed millions of barrels per day from global markets, with no alternative shipping routes available for Gulf producers.

The EIA’s World Oil Transit Chokepoints analysis documents how the Strait handles approximately 21 million barrels per day of petroleum and petroleum products, with no viable alternative maritime routes available when this passage is disrupted.

Qatar’s Ras Laffan Industrial City represents one of the world’s largest LNG export complexes, supplying Asian and European markets with liquefied natural gas. The March 18 attack created immediate global LNG price spikes because this capacity cannot be replaced in the short term. Gulf states also produce approximately 9% of the world’s aluminum supply, adding industrial metals exposure to the region’s energy dominance.

Oil and Natural Gas: Price Surges and Supply Shocks

Oil markets responded in distinct phases as the conflict escalated. In late February and early March, Brent crude rose 10-13% to $80-82 per barrel by March 2, reflecting uncertainty before the worst supply disruptions materialised. Markets were pricing geopolitical risk without yet experiencing physical supply losses.

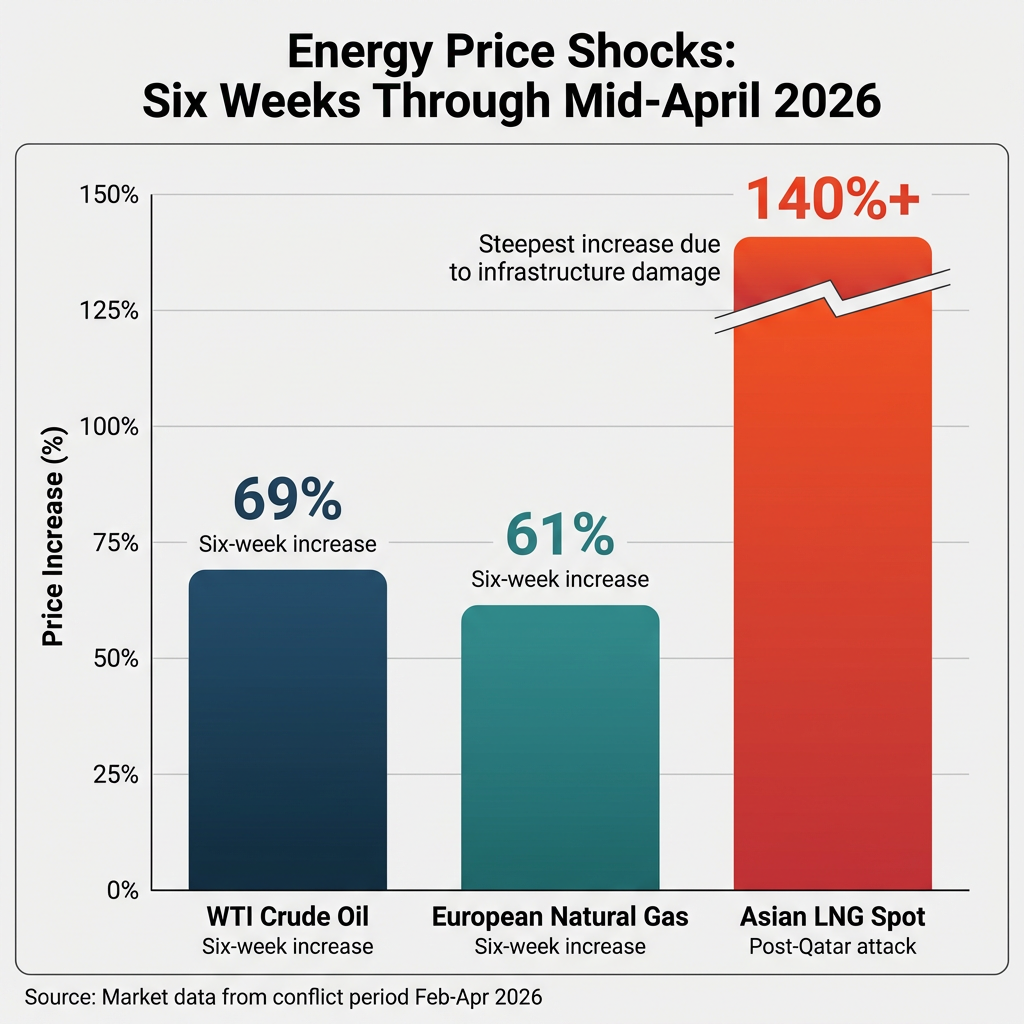

Following the Strait of Hormuz closure on March 4, Brent crude surged past $120 per barrel as physical supply shortages became reality. Over the six-week period through mid-April, WTI crude oil futures increased 69%. The overall price impact attributed to the war reached approximately 50%, fundamentally altering global energy economics. Analysts revised 2026 Brent forecasts upward by 30% to $82.85 per barrel, shifting market expectations from comfortable surplus to supply deficit.

| Energy Type | Price Change | Timeframe/Trigger |

|---|---|---|

| Brent Crude | 10-13% to $80-82 | Late Feb – March 2 (initial response) |

| Brent Crude | Surged past $120 | Post-Hormuz closure (March 4) |

| WTI Crude | 69% increase | Six weeks through mid-April |

| European Natural Gas | 61% rally | Six weeks through mid-April |

| Asian LNG Spot | 140%+ increase | Post-Qatar attack (March 18) |

LNG markets experienced even sharper disruptions given infrastructure dependencies. Following the March 18 attack on Qatar’s Ras Laffan complex, Asian LNG spot prices increased by over 140%, whilst European natural gas rallied 61% over the same six-week period. These represent steeper price shocks than oil markets because LNG infrastructure cannot be quickly substituted or rerouted when major export facilities sustain damage.

Stock Markets, Bonds, and Currency Volatility

Global stock markets experienced declines from the conflict’s onset, with a broader selloff extending through late March as the scale of energy supply disruptions became apparent. The equity decline reflected not just regional exposure but worldwide growth concerns as energy-dependent sectors faced margin compression and demand destruction risks.

On news of the mid-April temporary ceasefire, global stock markets rallied, led by energy-reliant sectors and countries most exposed to supply disruption risks. However, the rally reflected rapid unwinds of hedges and speculative repositioning rather than fundamental resolution. Energy-reliant sectors led the recovery, but analysts caution this represents technical relief rather than conviction that supply constraints have ended.

Bond yields surged as commodity prices rose, quickly erasing expectations for rate cuts that preceded the war. The yield increases reflected inflation concerns driven by energy price spikes and shifting monetary policy expectations away from accommodation. Currency markets experienced volatility particularly affecting energy-importing nations and emerging markets exposed to commodity price shocks, whilst safe-haven flows influenced major currency pairs.

Geopolitical conflicts historically drive safe-haven asset demand during geopolitical uncertainty, with precious metals experiencing structural shifts in investor allocation patterns when traditional risk assets face sustained volatility.

Beyond Energy: Aluminum, Fertilizers, and Inflation Pressure

On March 28, 2026, Iran hit Emirates Global Aluminum, causing massive production disruptions. Gulf states produce approximately 9% of the world’s aluminum supply, and aluminum prices increased 8% in March as the attack’s implications for industrial metals supply chains became clear.

Industries directly affected by aluminum supply disruptions include:

- Automotive manufacturing (body panels, engines, structural components)

- Aerospace production (airframes, engine parts)

- Electronics manufacturing (casings, heat sinks, circuit boards)

- Construction materials (window frames, cladding, structural elements)

- Consumer goods packaging (beverage cans, food containers)

Prolonged conflict could trigger shortages of nitrogen fertilizers, potentially driving up food costs through agricultural input price inflation and food supply chain disruptions. Energy prices directly affect fertilizer production costs, creating a transmission mechanism from energy markets to agricultural commodities and ultimately consumer food prices.

The conflict’s impact extends beyond energy markets to transport-dependent industries, with the aviation sector’s operational response to fuel price volatility demonstrating how companies navigate sustained commodity price shocks through hedging strategies and network adjustments.

The conflict fundamentally altered central bank policy trajectories. Expected interest rate reductions were postponed or conversely increased in light of higher inflation, shifting monetary policy from anticipated accommodation to a tightening bias. European central banks face particularly acute pressure given energy import dependence, representing a fundamental shift from pre-conflict policy consensus that had anticipated rate cuts through 2026.

The next major ASX story will hit our subscribers first

Scenario Outlook: What Markets May Face Next

> Moderate Scenario

> Military operations wind down sustainably, with gradual energy flow normalisation through the Strait of Hormuz and progressive restoration of damaged infrastructure. Oil prices remain elevated through Q2 2026 in the $75-100 range as supply gradually returns, with differing regional growth impacts and slight U.S. economic impact given lower energy import dependence.

> Adverse Scenario

> Major military operations fade but limited strikes continue, creating ongoing impairment of energy infrastructure and persistent security risks in Strait of Hormuz shipping lanes. Oil prices remain in the $100-125 range into the second half of 2026, with EU and Asia facing economic stagnation due to energy import dependence, whilst the U.S. weakens via financial conditions and global growth spillovers creating sustained inflation pressures requiring prolonged monetary tightening.

Energy prices could remain elevated even if the war ends quickly due to physical infrastructure damage requiring multi-year repairs. Qatar’s LNG facilities are estimated to require 3-5 years to fully repair, whilst oil production restoration will take several months minimum. Insurance premium increases for regional operations, strategic reserve rebuilding by importing nations, and reduced investment in regional energy projects all contribute to persistent price pressure regardless of conflict resolution timing.

While Gulf LNG capacity faces multi-year repair timelines, major LNG infrastructure projects in other regions may benefit from increased strategic importance as importing nations seek supply diversification.

> Critical Insight: Infrastructure damage timelines mean prices could stay elevated for months or years regardless of when fighting stops. The physical constraints of repairing complex energy infrastructure create price floors that geopolitical settlements alone cannot eliminate.

What Investors Should Consider Now

Fidelity professionals advise against hasty portfolio changes during elevated volatility, noting that headline-driven reactions can compromise long-term financial objectives. Market volatility is apt to remain elevated with headline risk driving short-term swings as the durability of the mid-April ceasefire remains uncertain and infrastructure constraints persist.

Key investor considerations include:

- Maintaining international equity diversification despite regional instability, as global exposure remains important for long-term portfolio construction

- Understanding that defense sector tailwinds depend on longer-term budget trends rather than immediate conflict developments

- Recognising that individual risk appetite and investment time horizon should guide portfolio decisions more than short-term headlines

- Avoiding reactive moves driven by daily price swings that may reverse as quickly as they emerge

This conflict represents a watershed moment in global energy security, fundamentally altering market expectations for commodity prices, inflation trajectories, and monetary policy paths. However, historical patterns show markets recover from geopolitical disruptions when structural supply constraints ease. The critical factors for individual investors are income requirements, investment time horizon, and capacity to endure temporary declines rather than attempting to time market movements around headline developments.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Frequently Asked Questions

What is the Iran conflict market impact on oil prices?

The Iran conflict caused Brent crude to surge past $120 per barrel after the Strait of Hormuz was closed on March 4, 2026, with WTI crude futures rising 69% over six weeks — representing approximately a 50% overall price increase attributed to the war.

How did the Iran conflict affect LNG and natural gas prices?

Asian LNG spot prices increased by over 140% following Iran's March 18, 2026 attack on Qatar's Ras Laffan Industrial City, while European natural gas rallied 61% over the same six-week period due to the damage to irreplaceable LNG infrastructure.

How long will energy prices stay high after the Iran conflict ceasefire?

Energy prices could remain elevated for months or years even after fighting stops because Qatar's LNG facilities are estimated to require 3-5 years to fully repair and oil production restoration will take several months minimum.

What should investors do during the Iran conflict market volatility?

Financial professionals advise against hasty portfolio changes during elevated volatility, recommending investors maintain international equity diversification and let their individual risk appetite and investment time horizon guide decisions rather than reacting to short-term headlines.

What sectors beyond energy are affected by the Iran conflict?

Beyond oil and gas, the conflict has disrupted aluminum supply chains after an attack on Emirates Global Aluminum caused prices to rise 8% in March, and prolonged conflict risks driving up fertilizer and food costs through energy-driven agricultural input price inflation.