Why Micron Stock Crossed $1 Trillion on a Single Analyst Call

48 mins ago

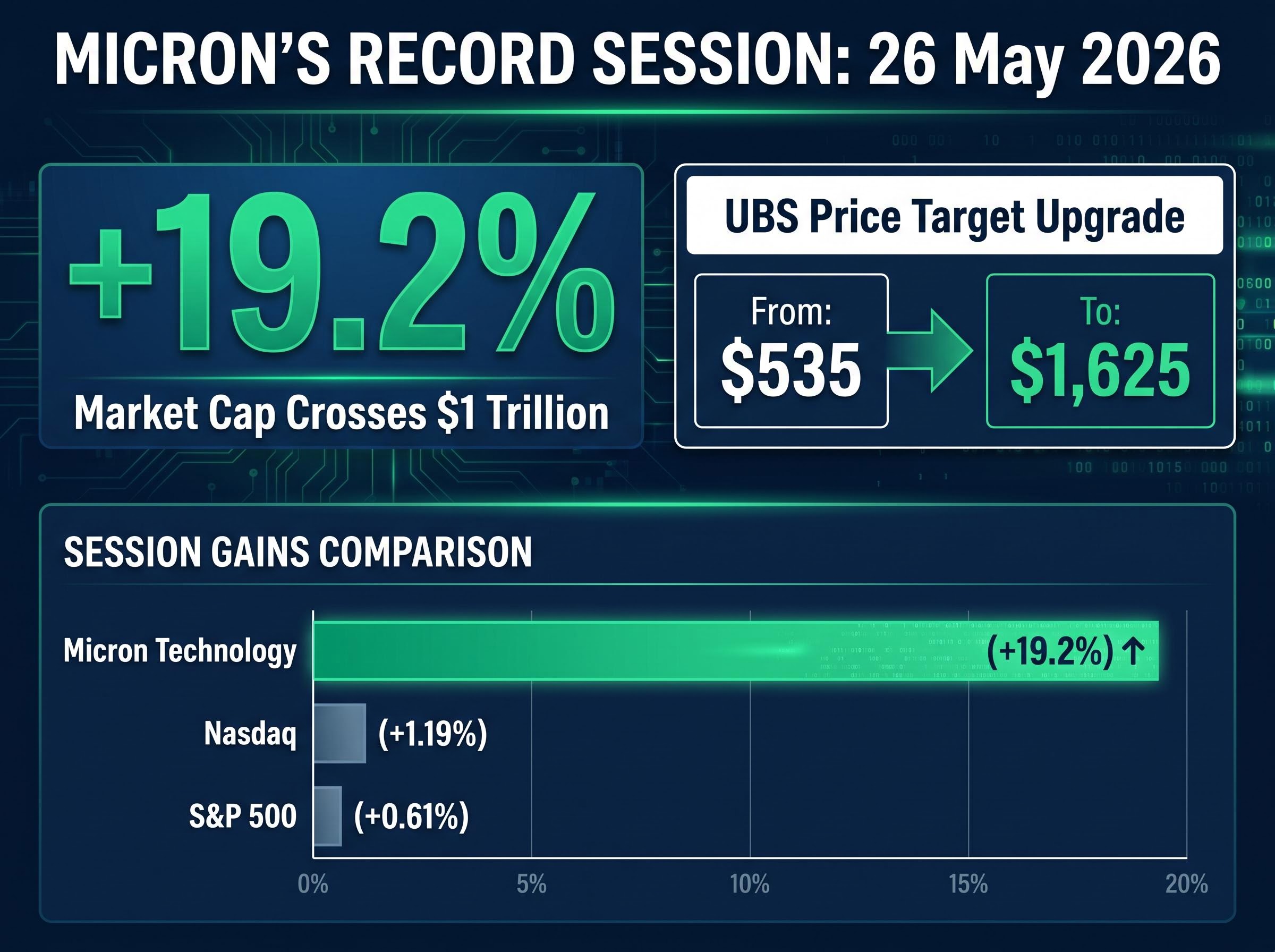

Micron Technology crossed the $1 trillion market capitalisation threshold on Tuesday, 26 May 2026, after UBS tripled its price target to $1,625 from $535, sending the stock up 19.2% in a single session. The move reframes Micron not as a commodity memory maker subject to boom-and-bust cycles, but as a structural beneficiary of artificial intelligence infrastructure buildout. The upgrade arrives as memory supply shortages across high-bandwidth memory (HBM), DRAM, and NAND persist, with demand expected to outpace supply well beyond 2026.

What follows is a breakdown of the UBS upgrade thesis, the supply mechanics underpinning Micron’s pricing power, why agentic AI workloads are creating durable memory demand, how Wall Street is reassessing the valuation framework applied to the stock, and what positioning data signals about the risks of entering the trade after a 19% single-session move.

The numbers tell the story before any analysis can. Micron Technology advanced 19.2% on 26 May 2026, crossing $1 trillion in market capitalisation for the first time, on the back of a UBS price target revision that tripled the prior figure. That is not a routine upgrade. It is a wholesale reassessment of the earnings framework being applied to the company.

The broader memory chip stocks surge that preceded Micron’s record session had already redrawn the sector’s investor map: HBM capacity across SK Hynix and Micron was sold out through 2026-2027, a Samsung labour strike was threatening a 3-4% reduction in DRAM supply, and US-China trade policy signals were reducing the likelihood of tool-access relief for Chinese memory producers, each factor compressing the already-tight supply outlook before UBS issued its upgrade.

UBS price target revision: $1,625 from $535, implying the share price could more than double from its prior Friday close.

The broader market was constructive but nowhere near proportional. The S&P 500 gained 0.61% and the Nasdaq rose 1.19%, both closing at all-time highs. Micron’s session was not a tide-lifts-all-boats event. It was a single-name re-rating.

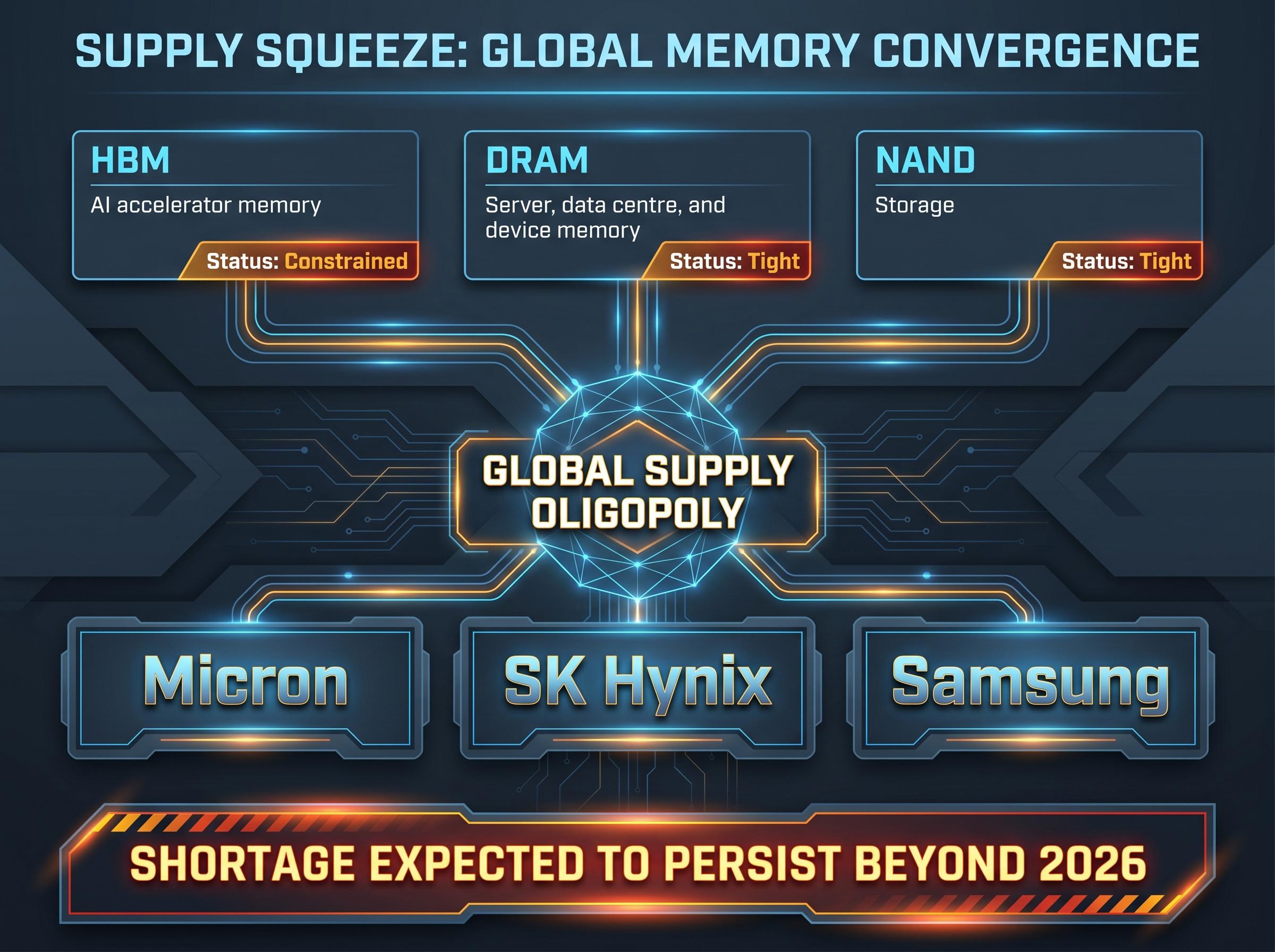

Micron’s pricing power does not rest on a single product line or a temporary inventory draw-down. It rests on a structural floor: demand for HBM, DRAM, and NAND is outpacing supply across all three memory categories, and the company’s own investor relations materials indicate tightness is expected to persist well beyond 2026.

| Memory type | Primary use case | Supply-demand status |

|---|---|---|

| HBM | AI accelerator memory (GPU/TPU stacks) | Constrained |

| DRAM | Server, data centre, and device memory | Tight |

| NAND | Storage (SSDs, enterprise flash) | Tight |

That tightness is the mechanism translating AI demand into revenue. Micron cites pricing as a major driver of revenue and free cash flow growth in the current period, and the company anticipates record free cash flow in fiscal Q3, according to Micron investor relations materials aggregated via Quartr. All three major credit rating agencies have recognised Micron’s balance sheet strength during the current period.

The pricing environment is not proprietary to Micron. A worldwide memory supply shortage has enabled Micron, SK Hynix, and Samsung to raise prices simultaneously. Three companies control the overwhelming majority of global memory production, creating an oligopolistic pricing structure where supply discipline benefits all participants. The UBS upgrade is the immediate catalyst, but the supply thesis is sector-wide in its implications.

Investors wanting the full supply mechanics behind Micron’s pricing environment will find our deep-dive into the memory chip supercycle covers the hyperscaler capex trajectory in detail, including why combined cloud operator spending is projected to surpass $1 trillion in 2027, how AI data centres now account for an estimated 70% of total memory shipment volumes, and why new manufacturing lines cannot reach mass production before 2027, creating a structural supply vacuum that underpins every pricing assumption in the current bull thesis.

Agentic AI refers to the shift from human-centric AI interactions, where a person types a prompt and waits for a response, toward autonomous software agents that operate independently, communicate with other agents, and execute multi-step tasks without human intervention. This distinction matters for memory demand because of how these agents consume hardware resources.

Prior memory upcycles were driven by consumer electronics refresh cycles: new smartphones, new PCs, new gaming consoles. The current cycle is structurally different. Three features distinguish agentic AI memory demand from those prior waves:

Micron’s own investor relations materials characterise the shift toward agentic and machine-to-machine interactions as a secular driver with compounding memory intensity. This framing received indirect corroboration from the broader market session.

Morgan Stanley highlighted demand inelasticity within the AI capital expenditure growth cycle as a constructive market factor, according to reporting via Market Index on the 26 May session.

The distinction between a cyclical and structural demand driver is what separates a one-quarter earnings beat from a multi-year revenue trajectory. If agentic AI adoption scales as Micron’s framing implies, the volume of memory required per unit of AI compute rises with each generation of deployment.

The same earnings figure can command vastly different share prices depending on the valuation framework the market applies to it. For most of its listed history, Micron traded as a commodity memory company. The market assigned trough-adjusted multiples, meaning it discounted the current period’s earnings by the assumed inevitability of the next down-cycle. This produced valuations that compressed during booms and expanded only modestly during busts.

The UBS upgrade thesis argues that framework is now outdated. The distinction between the old and new valuation logic is straightforward:

UBS argued that AI-related structural changes justify a re-rating of Micron’s valuation, with long-term supply agreements offering pricing stability. The bank stated that the market is expected to begin applying a more conventional earnings multiple as further details of AI structural demand become available.

Multi-year pricing agreements convert a portion of Micron’s revenue from spot-market volatility to contracted stability. This narrows the variance in forward earnings estimates, which is the specific mechanism that justifies a lower risk discount in the valuation. If a larger share of revenue is locked in through long-term contracts, the range of plausible earnings outcomes tightens, and the multiple the market is willing to pay expands accordingly.

Multiple expansion, the process of the market paying more per dollar of earnings, is often a more powerful share price driver than earnings growth itself.

For investors wanting to stress-test the multiple expansion argument with specific numbers, our full explainer on semiconductor stock valuation examines Micron’s current forward P/E of approximately 7.58x-8.9x against historical memory-sector peaks, walks through the three valuation tools that apply to different chip stock types (PEG ratio, EV/EBITDA, and cycle-adjusted forward estimates), and benchmarks Intel’s 101x forward P/E against its dot-com-era peak of 35x to show where genuine bubble conditions exist within the sector and where they do not.

The structural thesis is one side of the equation. The other is how much of that thesis is already reflected in positioning. Several data points from the 26 May session suggest the AI and semiconductor trade is historically crowded:

Goldman Sachs reported that short positioning in US macro products reached a 10-year high during the 26 May session, a signal that forced covering could amplify upside moves but also that positioning is stretched by historical standards.

The US 10-year Treasury yield fell 7 basis points to 4.49% on 26 May, a cumulative 17-basis-point decline over four sessions. That declining yield environment is supportive for growth equity valuations, but it does not resolve the concentration risk.

JPMorgan strategist Mislav Matejka identified a contrarian opportunity in underperforming low-volatility equities including consumer staples, utilities, and insurers. When positioning in a sector reaches the 90th or 93rd percentile, the marginal buyer pool shrinks. Investors evaluating entry into Micron or the broader AI memory trade after a 19% single-session move should weigh the structural thesis against the reality that many institutional participants are already near maximum exposure.

Two interpretations sit side by side. The structural case holds that AI-driven memory demand is secular, supply is constrained through the medium term, and long-term agreements are converting volatile earnings into predictable cash flows. Under that framework, the market is rationally re-rating Micron from a cyclical commodity name to a structural compounder, and the UBS target reflects the new valuation regime rather than speculative excess.

The positioning case holds that technology exposure is at multi-year extremes, momentum tilts are in the 90th percentile, and a 19% single-session move prices in substantial future earnings power in advance of its delivery. Both readings can be simultaneously correct.

The data points that will resolve the tension are identifiable: supply-demand balance updates through the second half of 2026, Micron’s forward guidance on long-term contract coverage as a percentage of revenue, and whether agentic AI adoption translates into verifiable memory volume growth rather than remaining a directional thesis. Until those arrive, the $1 trillion valuation is a statement of conviction, not yet a statement of proof.

AI hardware supply normalisation is the variable that ultimately resolves the tension between the structural bull thesis and the positioning risk: Morningstar projects the rate of new hardware absorption will decelerate around 2028, meaning investors entering the trade in mid-2026 are buying into a cycle with an identifiable horizon, and entry timing and position sizing become the key variables once the structural demand thesis is accepted.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

High-bandwidth memory (HBM) is a specialised type of memory stacked directly on AI accelerator chips like GPUs and TPUs to deliver fast data access at scale. Micron's HBM capacity is sold out through 2026-2027, making it a direct beneficiary of the AI infrastructure buildout and a key driver of the company's current pricing power.

UBS revised its price target from $535 to $1,625, arguing that AI-driven structural demand and long-term supply agreements justify applying a conventional growth multiple to Micron's earnings rather than the trough-adjusted commodity multiple the market had historically used. The bank stated the market is expected to re-rate the stock as further details of AI structural demand become available.

Agentic AI refers to autonomous software agents that operate independently and execute multi-step tasks without human intervention, running continuously rather than responding to occasional prompts. Because these agents run 24/7 and each require dedicated memory allocation, the total memory demand compounds non-linearly as the number of deployed agents grows, creating a durable and scalable source of demand for memory producers like Micron.

Goldman Sachs reported that hedge fund exposure to US technology equities was at five-year highs with momentum factor tilts at the 90th percentile, and Deutsche Bank flagged large-cap technology positioning at the 93rd percentile relative to data back to 2010. When institutional positioning is this crowded, the marginal buyer pool shrinks, meaning a large portion of the structural thesis may already be reflected in the price.

Multi-year pricing agreements convert a portion of Micron's revenue from spot-market volatility to contracted stability, which narrows the variance in forward earnings estimates. A tighter range of plausible earnings outcomes reduces the risk discount applied by the market, allowing investors to pay a higher multiple per dollar of earnings, a process known as multiple expansion that can be a more powerful share price driver than earnings growth alone.