Micron Hits $1 Trillion After UBS Triples Price Target to $1,625

41 mins ago

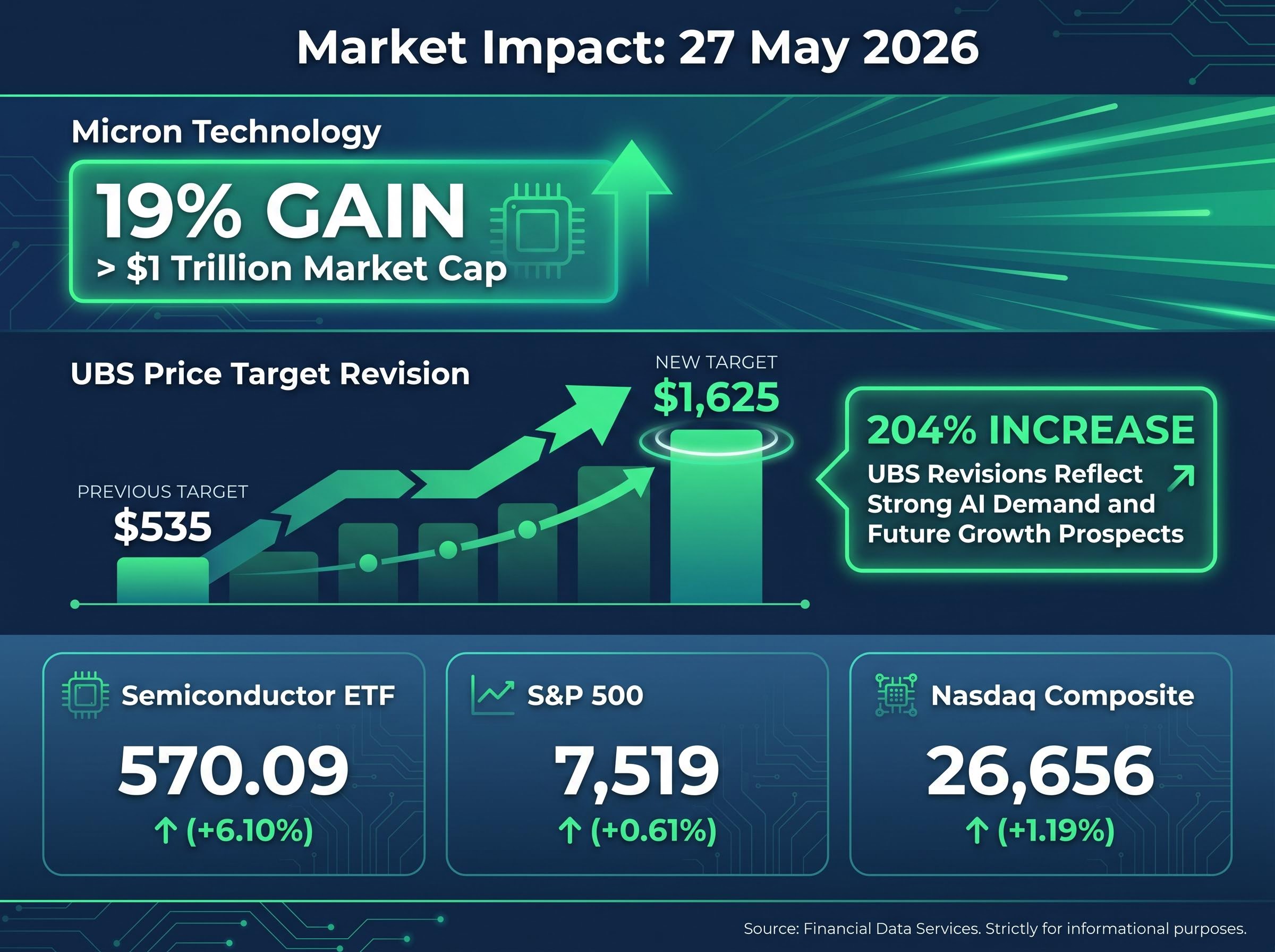

On 27 May 2026, Micron Technology shares surged approximately 19% in a single session after UBS nearly tripled its price target on the memory chipmaker, pushing Micron’s market capitalisation above $1 trillion for the first time. That kind of move does not happen on ordinary analyst upgrades. The catalyst was a UBS note revising its target from $535 to $1,625, a 204% increase that ranks among the most aggressive single-session analyst calls on a mega-cap stock in recent memory. The magnitude of that revision, and what it signals about AI-driven memory demand, is what makes this repricing worth examining carefully. What follows is an analysis of the mechanics behind the UBS call, the AI infrastructure thesis that underpins it, what a $1 trillion-plus Micron valuation means for the broader semiconductor sector, and how investors should weigh the sustainability of this repricing against the structural risks that have defined memory stocks for decades.

The numbers on 27 May 2026 were striking even by semiconductor standards. Micron Technology gapped higher at the open and never looked back, finishing the session up approximately 19% and crossing the $1 trillion market capitalisation threshold for the first time. The broader market moved with it, but the scale of Micron’s advance dwarfed everything around it.

UBS Price Target Revision Prior target: $535. Revised target: $1,625. That represents a 204% increase, nearly tripling the estimate on a stock that was already valued in the hundreds of billions.

A standard analyst revision on a large-cap name typically adjusts a target by 10-15%. A 204% upward revision signals something structurally different: not a minor earnings model tweak, but a fundamental re-rating of the company’s revenue trajectory and valuation framework. Micron was not a passive beneficiary of a broad risk-on session. It was the engine.

The 27 May session did not emerge from a standing start: memory chip stocks surged a combined 250% across Micron, Sandisk, and SK Hynix in the 30 days ending 12 May 2026, with Micron alone posting approximately 90% gains as sold-out HBM capacity and US-China trade policy shifts converged to reprice the sector ahead of the UBS catalyst.

UBS cited AI-related memory demand and long-term supply agreements as the primary drivers behind the revised valuation, according to coverage from CNBC. Those two elements deserve separate examination, because they address different dimensions of the investment case.

UBS analyst Timothy Arcuri anchored the $1,625 target to approximately 15 times forward earnings and projected cumulative free cash flow exceeding $400 billion across 2027-2029, modelling a moderate 2029 downcycle into those figures, a level of earnings specificity that goes well beyond the headline price target revision.

AI model training and inference workloads require memory architectures that differ from traditional enterprise server demand. Training a large language model requires massive parallel data throughput between processors and memory, which means high-bandwidth memory (HBM) and high-capacity DRAM at volumes that scale with the number of accelerator chips deployed. As AI infrastructure spending accelerates, the memory required per server rack increases at a rate that outpaces historical enterprise refresh cycles.

The second component of the UBS thesis, long-term supply agreements, addresses Micron’s historical vulnerability. Memory pricing has always been cyclical. Demand surges drive overinvestment, which drives oversupply, which compresses margins. Multi-year supply contracts shift a portion of Micron’s revenue from spot-price exposure toward predictable, committed volumes.

The analogy is instructive: TSMC’s long-term customer relationships have historically supported premium valuation multiples relative to more cyclical foundry peers. If Micron’s revenue base shifts meaningfully toward contracted volumes, a similar multiple expansion has structural logic behind it.

The session’s price action was ultimately a bet on one product category: high-bandwidth memory. Understanding what HBM is, and why only three companies make it, explains why a memory stock can now command a $1 trillion valuation.

High-Bandwidth Memory (HBM): A memory architecture in which multiple DRAM dies are stacked vertically and connected via through-silicon vias, enabling data transfer speeds that standard memory modules cannot match.

HBM sits physically closer to the processing unit inside AI accelerators. This proximity, combined with the die-stacking architecture, delivers the bandwidth that GPU-based AI training and inference require. It is a component in Nvidia accelerators (H100, H200 series) and AMD Instinct products, meaning HBM demand tracks directly with AI chip shipments.

| Attribute | Standard DRAM | High-Bandwidth Memory (HBM) |

|---|---|---|

| Bandwidth | Moderate (single-die architecture) | High (stacked-die, through-silicon vias) |

| Primary use case | PCs, servers, mobile devices | AI accelerators, data centre GPUs |

| Margin profile | Cyclical, commodity-like pricing | Premium pricing, higher gross margins |

Only three manufacturers produce HBM at commercial scale: Micron, Samsung, and SK Hynix. That concentrated supply structure supports pricing power in a way that commodity DRAM markets, with their broader competitive dynamics, historically have not.

Micron’s 19% move did not stay contained. The semiconductor sector ETF gained 6.10% to close at 570.09, and Information Technology led all US sectors with a 1.69% advance. The mechanism behind this propagation is straightforward but worth stating explicitly.

When a large-cap constituent of a sector ETF surges on a fundamental upgrade, the ETF’s net asset value rises mechanically. Institutional funds benchmarked to the sector rebalance toward the outperformer, creating buying pressure across correlated names. And the narrative itself, that AI memory demand warrants a fundamental re-rating, reprices the expectation set for every company exposed to the same demand cycle.

“Leadership rotation within AI-related equities, with chipmakers taking the lead.”

The Russell 2000 rose 1.79%, breaching 2,900 for the first time, illustrating a broad risk-on tone that extended well beyond the semiconductor sector. Names frequently cited as AI infrastructure co-beneficiaries, including Nvidia, AMD, TSMC, Samsung, and SK Hynix, operate within the same demand narrative that drove the session.

Sector ETF investors holding products like SOXX or SMH gained meaningful exposure to the Micron repricing even without owning the stock directly.

The bull case has internal coherence. If long-term supply agreements reduce Micron’s cyclical earnings volatility, then the historically compressed multiples applied to memory stocks may no longer be appropriate. A re-rating toward infrastructure-like earnings stability has precedent in the TSMC valuation story, where long-term customer commitments and advanced-node pricing power supported a premium multiple for years.

The UBS target of $1,625 implies a sustained AI infrastructure buildout over multiple years with no meaningful supply-side disruption. That is a high-conviction assumption.

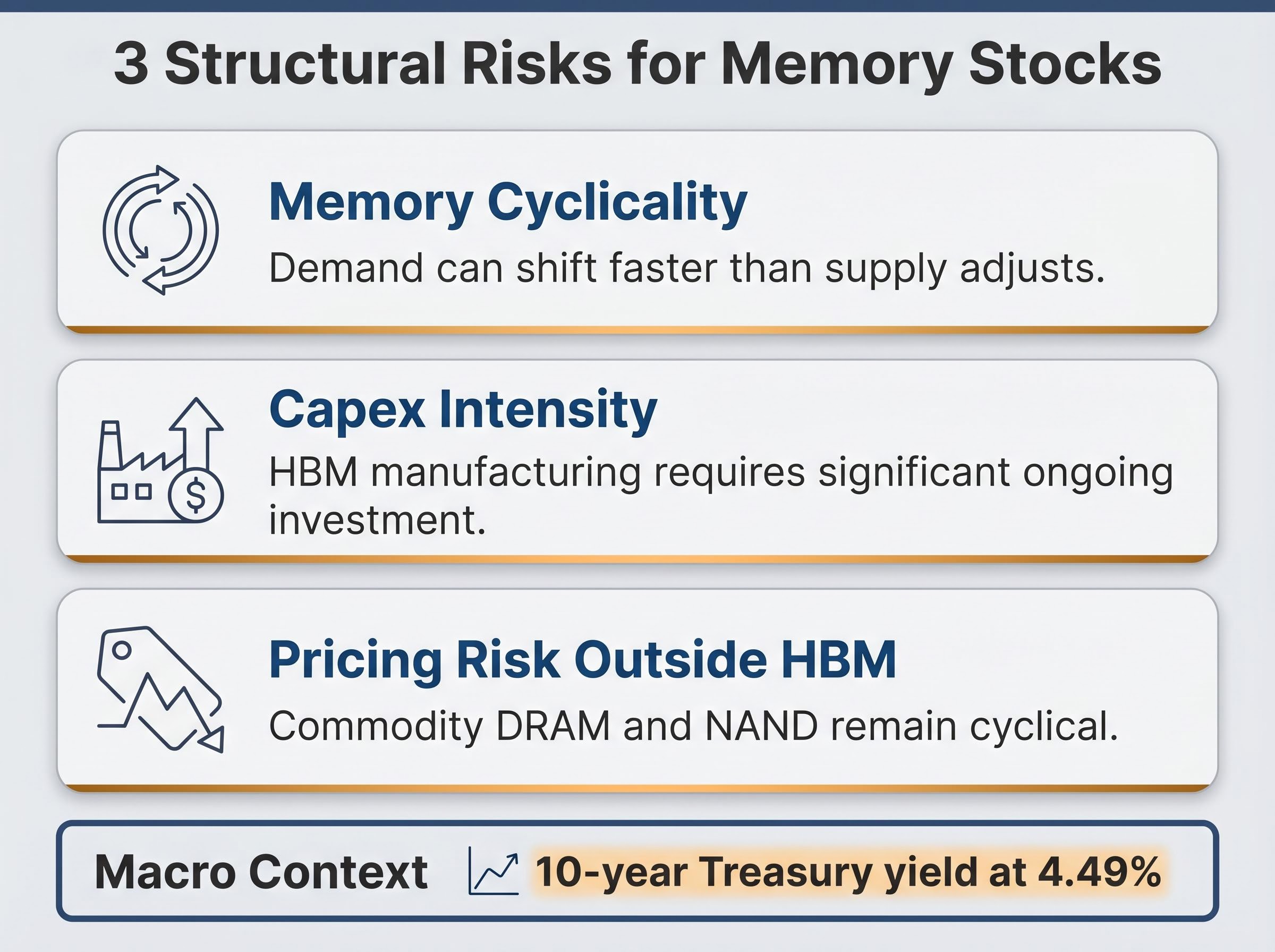

Memory stocks carry structural risks that do not disappear simply because HBM has a stronger demand profile. These are monitoring variables, not dismissals of the thesis.

The 10-year Treasury yield stood at 4.49%, providing the discount rate backdrop against which a $1 trillion growth valuation must be assessed. Higher rates raise the bar for the duration of earnings growth that justifies a premium multiple.

The broader AI investment cycle provides the macroeconomic backdrop against which the UBS $1,625 target must be assessed: US IT hardware and software spending reached 4.9% of GDP in Q1 2026, surpassing both the dot-com era peak and the cloud buildout peak, with combined hyperscaler capex commitments for 2026 running between $600 billion and $805 billion before the Stargate Project’s additional $500 billion is included.

Micron’s crossing of the $1 trillion market capitalisation threshold is a signal that the market has begun re-rating memory infrastructure as a core AI beneficiary category. The session’s record closes, with the S&P 500 at 7,519, the Nasdaq at 26,656, and the Russell 2000 above 2,900, suggest the AI infrastructure repricing has broadened. The equal-weighted S&P 500 also reached an all-time high, signalling breadth rather than concentration in a handful of names.

The forward-looking questions that will determine whether this repricing holds are specific and trackable:

The Micron move is not only about Micron. It is a signal about how the market is pricing the entire AI infrastructure layer, and investors who understand that signal can apply the same analytical framework to future analyst calls across the semiconductor and data centre ecosystem.

UBS’s $1,625 target represents a fully formed, high-conviction view of where AI infrastructure demand takes Micron Technology. The market endorsed it in a single session. Confirmation, however, must come from quarterly results.

The framework developed in this analysis, covering HBM mechanics, supply agreement structure, cyclicality risks, and sector ETF propagation, applies to any future high-conviction semiconductor analyst call, not just this one. Over the next two to four quarters, the signals that will confirm or challenge the thesis are clear: HBM revenue disclosure, gross margin trajectory, and long-term supply agreement commentary in Micron’s earnings releases.

Investors wanting to pressure-test the structural re-rating argument before quarterly earnings provide confirmation will find our deep-dive into the AI memory re-rating thesis, which examines the specific HBM supply constraints across DRAM die capacity, TSV packaging complexity, and CoWoS throughput that make the supply void structurally durable, alongside the starting-point valuation risks that apply even if the bull case is broadly correct.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

High-bandwidth memory (HBM) is a memory architecture where multiple DRAM dies are stacked vertically and connected via through-silicon vias, delivering the data transfer speeds required by AI accelerators. It commands premium pricing and higher gross margins compared to commodity DRAM, making it central to the bull case for Micron's valuation re-rating.

UBS analyst Timothy Arcuri revised the Micron price target from $535 to $1,625, a 204% increase, citing AI-driven memory demand, long-term supply agreements, and projected cumulative free cash flow exceeding $400 billion across 2027-2029. The revision reflected a fundamental re-rating of Micron's revenue trajectory rather than a routine earnings model adjustment.

Long-term supply agreements shift a portion of Micron's revenue away from volatile spot-price exposure toward predictable, committed volumes, reducing the earnings cyclicality that has historically compressed Micron's valuation multiple. This structural shift is analogous to TSMC's premium multiple, which has been supported by long-term customer relationships.

Three key risks persist: memory market cyclicality can cause demand to shift faster than supply adjusts; HBM manufacturing at leading-edge nodes requires heavy capital expenditure that can compress free cash flow; and commodity DRAM and NAND segments remain exposed to pricing pressure regardless of HBM's stronger demand profile.

The semiconductor sector ETF gained 6.10% on the session, and Information Technology led all US sectors with a 1.69% advance, as Micron's fundamental upgrade repriced AI memory demand expectations across correlated names including Nvidia, AMD, TSMC, Samsung, and SK Hynix.