KOSPI Drops 10% as Crowded AI Trade Unwinds Across Global Markets

1 hr ago

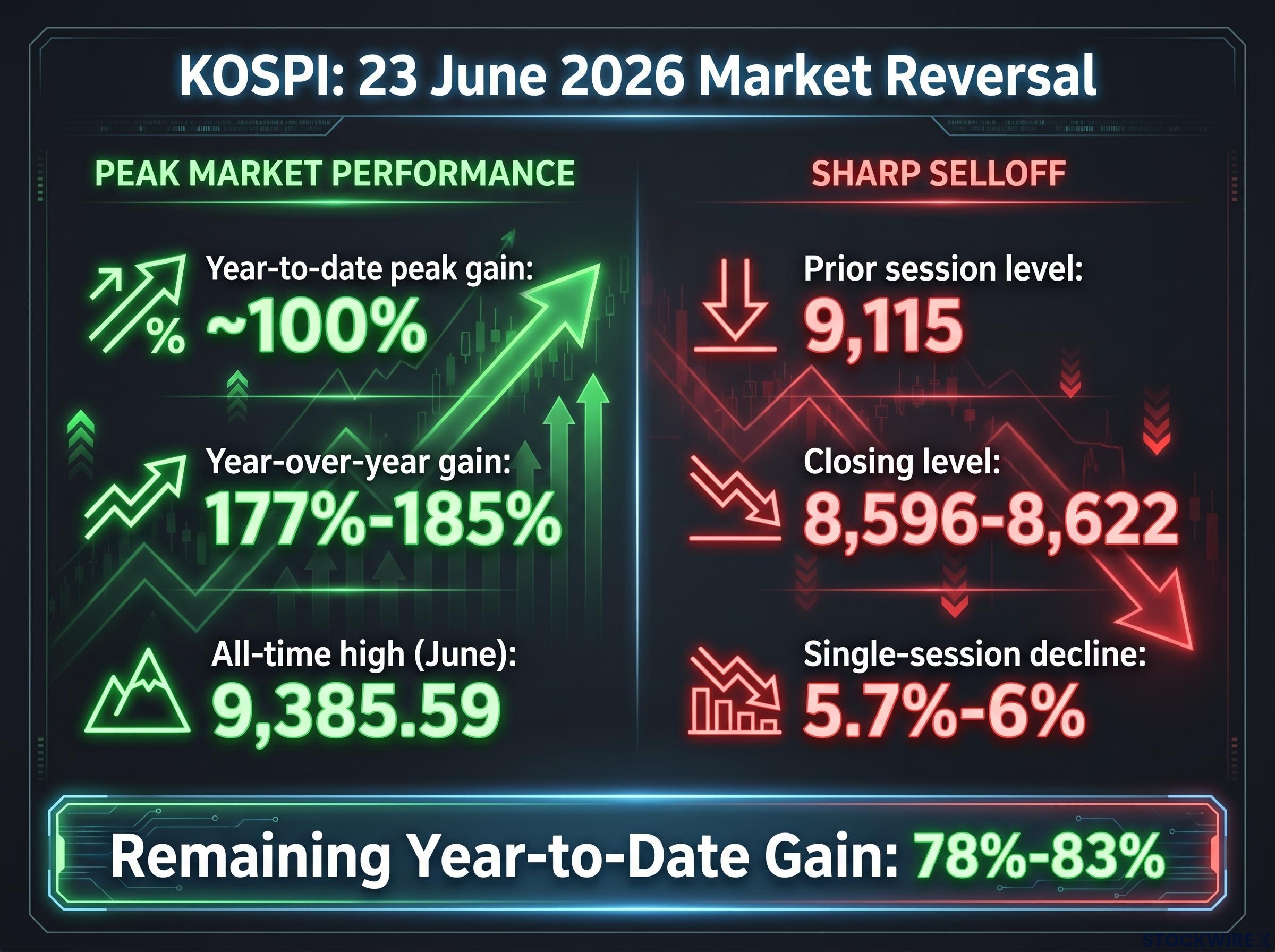

The KOSPI shed nearly 6% in a single session on 23 June 2026, making it the most violent single-day reversal in a bull run that had already delivered roughly 80% gains this year alone. When an index nearly doubles in under six months and then drops 6% in one day, two questions follow immediately: is the thesis broken, and is this the start of something worse?

The triggers are specific and identifiable. Profit-taking after an extraordinary rally collided with a negative catalyst from MSCI, which declined to place South Korea on the watchlist for Developed Market status. The result was a broad, indiscriminate selloff that activated the Korea Exchange’s sidecar mechanism and sent smaller-cap stocks down by double digits. By the end of this article, you will understand exactly what drove the selling, what the MSCI decision means for foreign capital flows into Korean equities, and why the available evidence still points to a correction within a structural rally rather than its end.

The numbers are severe by any measure. The KOSPI closed at approximately 8,596-8,622, down from a prior session level of approximately 9,115. That translates to a decline of roughly 5.7%-6% in a single trading day. Over the preceding seven sessions, the index had finished lower on just two occasions, which makes the abruptness of the reversal even more striking.

Here are the key figures from the session:

Despite shedding nearly 6% in a single day, the KOSPI still stood roughly 78%-83% ahead for the year, a return that ranks it among the top-performing major equity indices globally in 2026.

That context matters. This is a story about the ferocity of a repricing inside an extraordinary bull market, not the collapse of one.

The scale of the preceding rally explains why a single session of profit-taking could produce such a dramatic headline. The KOSPI had gained approximately 100% year-to-date at its peak, driven overwhelmingly by enthusiasm for AI and semiconductor stocks. Year-over-year, the index was showing gains of approximately 177%-185% in recent readings.

The AI semiconductor supercycle that drove the KOSPI’s extraordinary gains is backed by real earnings: Micron posted record quarterly net income of $13.79 billion, Microsoft and Meta alone committed over $160 billion in AI infrastructure capital expenditure for 2026, and Bank of America projected approximately $975 billion in global chip sales for the year, figures that distinguish this rally from purely speculative episodes.

A 177%-185% year-over-year gain is not a normal market. It is the kind of move that compresses the gap between routine profit-taking and a dramatic market event into almost nothing.

When an index gains 100% in under six months, every investor holding those gains faces rational pressure to sell. The selloff on 23 June was not a random shock. It was the mathematical consequence of a market that had moved too far, too fast, for a single catalyst to hold sentiment in place once that catalyst failed to arrive.

Anticipation of MSCI Developed Market inclusion had been building for months, attracting overseas capital seeking to position ahead of an expected upgrade. Foreign investor participation contributed meaningfully to the benchmark reaching record levels. This created a feedback loop: MSCI expectations amplified inflows, which amplified the rally, which amplified the eventual correction when those expectations went unmet.

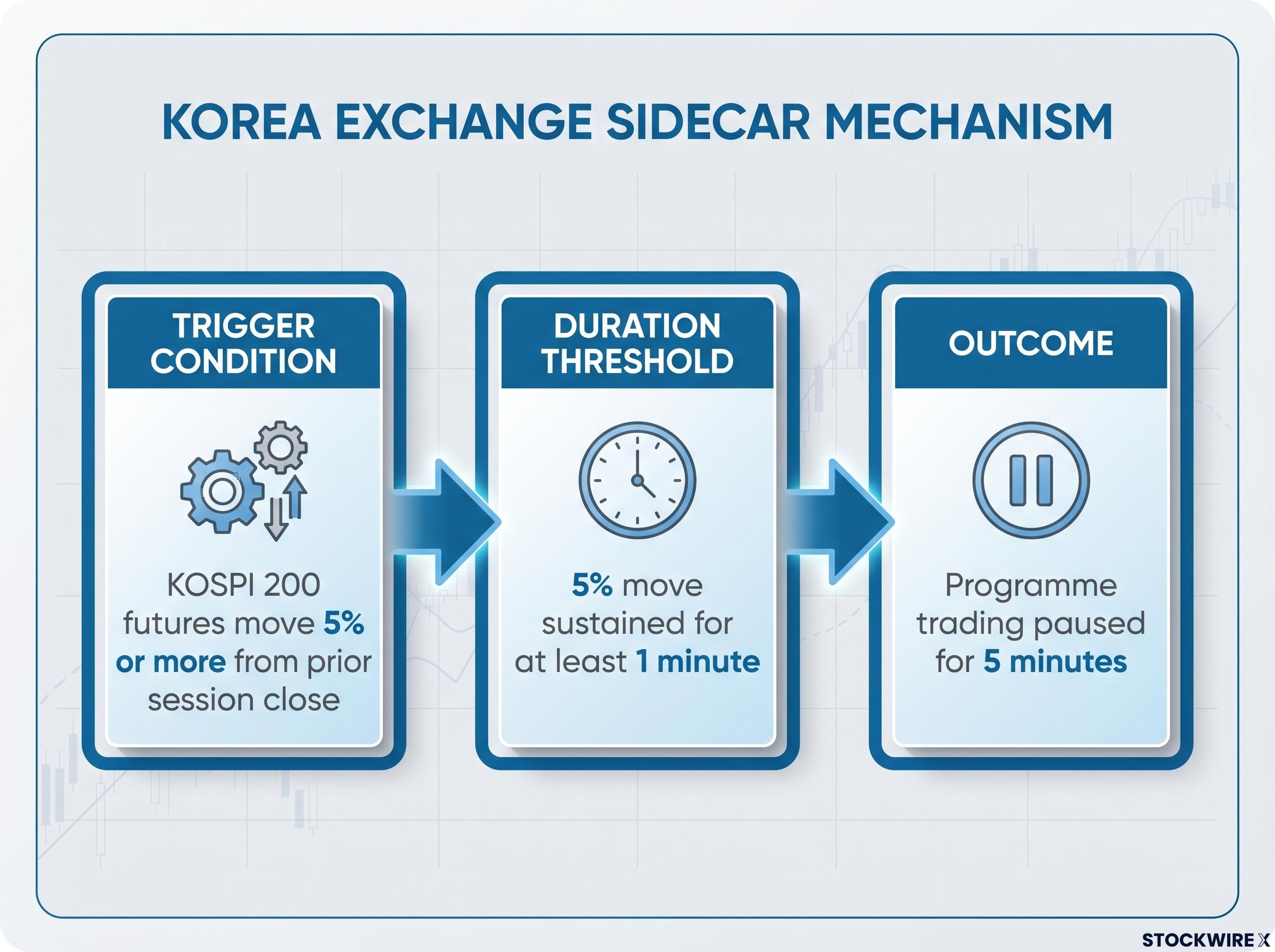

The Korea Exchange activated its sidecar trading restriction during the 23 June session. For investors unfamiliar with Korean market mechanics, the sidecar is a targeted safety mechanism, not an emergency shutdown.

Here is how it works:

The sidecar activated because futures dropped steeply during the selloff, meeting both thresholds. It is a narrower measure than the full circuit breakers that halt all trading across an exchange. Its activation tells you the selling was fast and algorithmic in character, but it also tells you the exchange’s safety architecture functioned exactly as designed. That is a different signal from a market in freefall.

MSCI conducted its market classification review on 23 June and did not place South Korea on the watchlist for Developed Market status. The reason cited: pending reforms on market accessibility. South Korea remains classified as an Emerging Market.

The Korea Discount, the persistent valuation gap driven by chaebol governance structures, historically low capital returns to shareholders, and geopolitical risk premium from North Korea, means Korean equities have long traded below intrinsic value estimates that comparable global peers would command, even before accounting for the market accessibility concerns that MSCI cited in its classification review.

The MSCI Developed Market reclassification criteria that South Korea failed to satisfy include foreign exchange market openness, omnibus account usage, foreign investor registration processes, and the availability of investable products, each representing a structural accessibility gap that reforms must close before a watchlist addition becomes possible.

| Category | Current status | Watchlist placement | Next review |

|---|---|---|---|

| MSCI classification | Emerging Market | Not placed on Developed Market watchlist | 2027 or later |

The investor logic is straightforward. Foreign capital had accumulated in Korean equities in anticipation of an upgrade, with investors seeking to get ahead of the substantial passive index-tracking flows that a reclassification would have generated. When the watchlist addition failed to materialise, that near-term catalyst evaporated, and repositioning followed.

The next expected review opportunity is 2027 or later, which means this particular tailwind will not return in the near term.

For investors holding Korean equities, the MSCI decision means the foreign-capital momentum that helped propel the rally will not be amplified by institutional index-tracking flows any time soon. Patience is required before this catalyst can re-emerge.

The index-level figure tells one story. The individual stock wreckage tells another.

| Company | Decline | Context |

|---|---|---|

| DLG Exhibitions and Events Corp Ltd | -17.2% | Touched lowest level since late March 2026 |

| Dae Won Chem | -15.9% | Small-cap industrial stock |

| Enex | -15.6% | Small-cap industrial stock |

| Haesung DS Co Ltd | -15.0% | Small-cap technology stock |

| Hansol Technics | -12.9% | Small-cap technology stock |

These are not AI or semiconductor leaders. They are smaller-cap names spread across events, chemicals, and industrial segments. When non-AI, non-semiconductor small caps fall 15%-17% in a single session, it tells you the selling was indiscriminate and liquidity-driven, not a targeted reassessment of any particular sector thesis. That distinction matters for what happens next.

The case for continued strength rests on specific foundations:

The honest read is that the rally thesis is intact but the near-term risk profile has shifted. A market that can move 6% in a single session in either direction demands that anyone holding Korean equities reconsider whether their investment horizon aligns with that level of volatility.

Fund flow data through late May 2026 had already flagged emerging signs of institutional repositioning, with emerging market equity funds recording six consecutive weeks of net outflows and Bank of America’s Bull and Bear Indicator briefly touching 8.0, a level that has historically preceded 2-3% equity declines, suggesting the conditions for a sharp correction were accumulating before the MSCI decision provided the trigger.

Even accounting for the 23 June selloff, the KOSPI has delivered one of the strongest year-to-date returns of any major index in 2026. That fact has not changed. What has changed is the clarity of the near-term path. The MSCI setback, elevated valuations, and the sheer scale of the preceding move all mean the next few weeks carry more uncertainty than the last few months did.

The variables to watch are specific: MSCI developments heading toward the 2027 review cycle, the durability of AI and semiconductor earnings as they begin reporting in coming quarters, and whether the index stabilises or faces further rounds of profit-taking. The structural story is not broken. The easy phase of the rally may be.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The KOSPI fell roughly 5.7%-6% on 23 June 2026 due to a combination of profit-taking after an extraordinary rally and MSCI declining to place South Korea on the watchlist for Developed Market status, which removed a key near-term catalyst for foreign capital inflows.

The sidecar is a targeted trading restriction that pauses programme trading for five minutes when KOSPI 200 futures move 5% or more from the prior session's closing price for at least one minute; it activated on 23 June because futures dropped steeply during the selloff, signalling fast and algorithmic selling rather than a full market shutdown.

MSCI kept South Korea classified as an Emerging Market due to pending reforms on market accessibility, meaning the large passive index-tracking flows that a Developed Market reclassification would have generated will not materialise until at least the 2027 review cycle.

The KOSPI had gained approximately 100% year-to-date at its peak in June 2026, driven primarily by AI and semiconductor stock enthusiasm, and even after the selloff it retained roughly 78%-83% in year-to-date gains.

Key variables include MSCI developments heading toward the 2027 review cycle, the durability of AI and semiconductor earnings in upcoming quarterly reports, and whether the index stabilises at current levels or faces further rounds of profit-taking driven by elevated valuations.