ASX Healthcare’s 50-Day Break: Recovery Signal or Bear Bounce?

3 mins ago

For the first time on record, central banks declaring intentions to reduce their U.S. dollar allocations now outnumber those planning to increase them. That finding, from the OMFIF Global Public Investor survey released 30 June 2026, is not a forecast or a theoretical concern. It is a declared intention from institutions that collectively manage the architecture of global reserves.

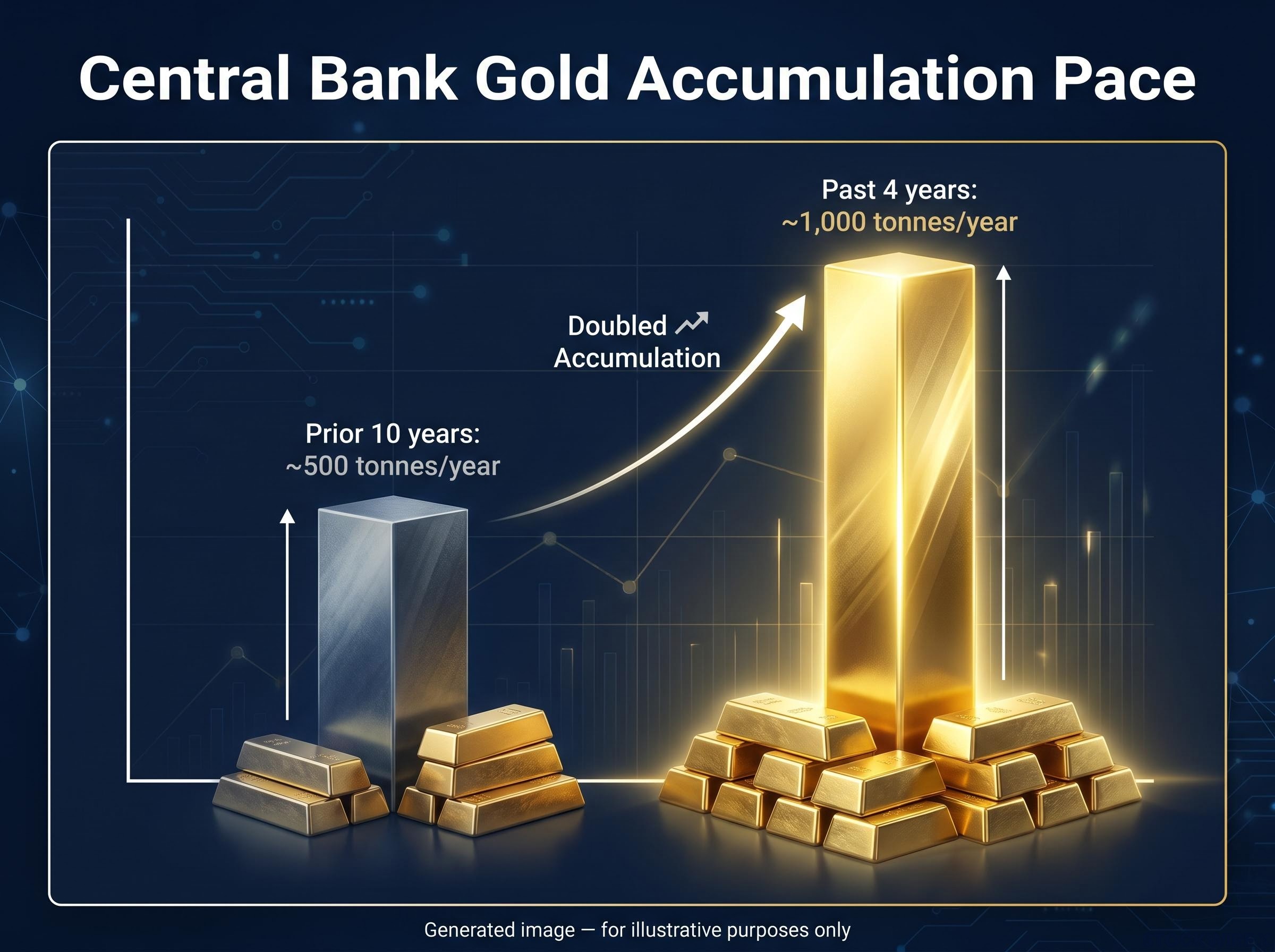

The scale behind that intention matters. The OMFIF survey drew on 90 sovereign institutions overseeing more than $7 trillion in assets. Gold is the primary beneficiary of the reallocation now underway, with central banks accumulating roughly 1,000 tonnes per year over the past four years, double the pace of the preceding decade.

Here is what the institutional data actually tells you about the forces driving this shift, what the survey findings reveal beneath the headlines, and what they mean for how gold should be understood as an asset class going forward. The goal is to equip you with an institutional lens for interpreting gold’s next move, rather than reacting to price noise.

Start with the survey’s credibility. The OMFIF Global Public Investor survey, released 30 June 2026, covered 90 central banks, sovereign wealth funds, and public pension funds whose combined reserves surpass $7 trillion in total assets. This is not a sentiment poll. It is a documented snapshot of how institutions that shape global capital flows are positioning their reserves.

The findings, taken in sequence:

Each of those findings is directionally significant. Together, they describe a structural reorientation in reserve management that is already being acted on.

OMFIF senior economist Yara Aziz observed that the longstanding assumption that public investors could simply wait for conditions to stabilise before acting now appears increasingly untenable. The implication: institutions are not sitting on the sideline waiting for a better entry point. They are building positions now.

That shift in institutional patience is where the demand signal originates. The dollar-reduction finding is not a preference expressed in a conference panel. It is a declared intention from the institutions whose allocation decisions collectively shape the global reserve system, and it tells you where the structural bid for gold is coming from.

In 2022, Western governments froze approximately $300 billion in Russian sovereign assets. Those reserves were held in legitimate foreign currency instruments, in jurisdictions Russia had treated as safe. Overnight, they became inaccessible, removed from Russia’s control without any legal proceeding specific to those assets.

For non-Western central banks, the event posed a question that had previously been theoretical: if reserves held in a foreign sovereign’s currency can be frozen unilaterally, are they truly reserves in the risk-management sense?

Goldman Sachs commodity co-head Samantha Dart, in a note published 29 June 2026, identified the Russian reserve freeze as a lasting catalyst for central bank diversification toward gold. That framing is independently supported by survey data from OMFIF, the World Gold Council (WGC), and HSBC’s Reserve Management Trends research, all of which identify geopolitical risk and sanctions concerns as primary drivers of gold accumulation.

Gold’s distinguishing property is straightforward: it is a physical asset that can be held domestically or in neutral vaults. It is not a claim on another sovereign’s obligations. It carries no counterparty risk from a foreign government’s policy decisions.

That property existed long before 2022. What the Russian freeze did was demonstrate its practical value in a way no theoretical argument had. Central banks did not discover gold’s sovereign independence; they watched a peer institution lose access to $300 billion in reserves that lacked it. The response, a doubling of annual gold accumulation, followed directly.

The case for a structural shift rests on convergence. Multiple independent surveys, using different methodologies and sample populations, are producing consistent signals.

| Survey source | Finding | Timeframe | Direction |

|---|---|---|---|

| World Gold Council (2026) | 89% expect global official gold reserves to rise | Next 12 months | Increase |

| World Gold Council (2026) | 45% plan to increase own holdings (record) | Next 12 months | Increase |

| OMFIF (June 2026) | 32% expect to increase gold holdings | Short term | Increase |

| OMFIF (June 2026) | Net 30% plan to increase gold | 1-2 years | Increase |

| HSBC / Central Banking (2026) | 39% considering increasing gold | Next year | Increase |

| HSBC / Central Banking (2026) | 37% plan more active gold management | Next year | Increase |

| Accumulation pace (recent) | ~1,000 tonnes/year | Past 4 years | Double prior decade |

| Accumulation pace (prior decade) | ~500 tonnes/year | Prior 10 years | Baseline |

The WGC’s 45% figure, a record-high level of intention to increase gold holdings, is the most forward-looking anchor in the dataset. It tells you that nearly half of the world’s reserve managers are not merely maintaining their gold positions; they are actively planning to add.

The consistency across surveys matters more than any individual number. And 78% of HSBC survey respondents expect de-dollarisation to be gradual. That does not contradict the accumulation data. It confirms the tempo: this is a sustained, deliberate recalibration, not a panic-driven rush. That measured pace is precisely what makes it durable as a structural tailwind for gold.

The U.S. dollar still accounts for approximately 57% of disclosed global foreign exchange reserves. It remains the world’s primary reserve currency by a wide margin. No survey finding changes that arithmetic today.

The de-dollarisation mechanics underlying this shift are measurable in the reserve data: the dollar’s share of global central bank holdings has fallen from approximately 71% in 2001 to below 57% today, a multi-decade erosion that explains why the OMFIF finding of net dollar-reduction intent registers as a milestone rather than a surprise.

The distinction worth drawing is between directional change and displacement. Central banks are reallocating at the margin, and that marginal reallocation is meaningful and accelerating, but it is not the same as abandoning dollar dominance. The OMFIF finding that more institutions now plan to reduce dollar allocations than increase them is best understood as a shift in net intent, not a declaration of dollar exit.

What the evidence supports:

What the evidence does not support:

Understanding that distinction actually strengthens the gold thesis rather than weakening it. A slow, deliberate reallocation means the structural buying pressure is measured and sustained rather than episodic and reversible. For your positioning, that durability is the signal that matters.

In a note dated 29 June 2026, Goldman Sachs commodity co-head Samantha Dart set out the firm’s end-2026 gold price target of $4,900 per troy ounce. That target was revised upward from $4,300 and revised downward from a prior $5,400 figure, reflecting Goldman’s recognition of near-term headwinds within a structurally bullish view.

Based on gold’s price at the time of publication, the $4,900 forecast represented potential upside in the region of 21% before year-end. Goldman cited two structural drivers: ongoing reserve diversification by emerging market central banks, and eventual cyclical tailwinds from interest rate movements.

| Institution | End-2026 target | Notable caveat |

|---|---|---|

| Goldman Sachs | $4,900/oz | Revised from $4,300; down from prior $5,400 |

| J.P. Morgan, UBS, Wells Fargo, Bank of America, Morgan Stanley | ~$5,200-$6,300/oz | Aggregated range; not independently verified for each institution |

Emerging market central bank diversification away from dollar-dependent reserves sits at the core of Goldman Sachs’ $4,900 gold price case, a view that the survey data from OMFIF, the WGC, and HSBC independently corroborates.

Goldman’s target sits toward the conservative end of the institutional consensus. Peer bank forecasts cluster at higher levels, making the $4,900 figure a floor estimate rather than a ceiling within the professional commodity analyst community. The convergence of multiple major institutions on elevated year-end targets matters more than any single number. It signals that the structural bid from central banks is seen as durable enough to underpin prices well above recent trading ranges.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

For investors wanting to trace how Goldman’s gold thesis has shifted across successive revisions, our full explainer on Goldman’s evolving gold forecast covers the progression from the $5,400 reaffirmation through to the revised $4,900 target, including the liquidation risk caveat that accompanies the firm’s broader structural bull case.

Central bank demand, as characterised across OMFIF and WGC research, is largely price-insensitive. Emerging market institutions in particular are accumulating gold based on reserve diversification objectives and geopolitical hedging considerations, not short-term price movements. The structural bid does not evaporate when prices are elevated.

That structural layer is supported by the data covered above: accumulation pace doubling from 500 to 1,000 tonnes per year, record intention levels in forward-looking surveys, and net dollar-reduction intent crossing into majority territory for the first time.

Sovereign debt erosion of the traditional bond diversification role has reinforced the institutional case for gold as a portfolio anchor, with BlackRock, JPMorgan, and Swiss pension funds all explicitly increasing gold allocations to fill the gap left by government bonds whose safe-haven properties deteriorated sharply in the 2022 simultaneous equity and bond selloff.

The tactical layer operates on a different set of inputs entirely:

Rate-driven gold drawdowns can be severe even when the structural bid remains intact, as the Iran conflict period demonstrated: gold fell more than 16% from approximately $4,700 per ounce while central bank accumulation continued at record pace, confirming that the Fed’s real yield and dollar effects can overwhelm sovereign demand signals over a multi-month horizon.

Three conditions would weaken the structural gold bid if they materialised: a sustained reversal in emerging market reserve accumulation, a geopolitical thaw that materially reduces sanctions risk, or a prolonged dollar strengthening cycle that restores confidence in dollar-denominated reserves.

None of those conditions are currently in evidence. But they are the variables worth tracking, rather than reacting to short-term price volatility. If you understand that the institutional buying pressure is driven by reserve management logic rather than sentiment, you are better positioned to hold through cyclical drawdowns without abandoning a thesis that the institutions themselves are acting on.

The current moment is best understood as an early stage in a structural reorientation, not a completed transition. The dollar retains clear dominance at approximately 57% of global reserves. But the directional signals from multiple independent surveys point consistently toward continued gold accumulation and gradual dollar share erosion.

The durability of the trend depends on whether the conditions that created it persist: sanctions risk, geopolitical fragmentation, and institutional distrust of counterparty-dependent reserves. Current geopolitical dynamics do not suggest those conditions are reversing.

The 78% of respondents who expect de-dollarisation to be gradual are describing the tempo. The record 45% who plan to increase their own gold holdings are describing the direction. And the OMFIF survey released 30 June 2026, with its first-ever net dollar-reduction finding, marks where that direction stands today.

The institutional shift in reserve management is slow, deliberate, and already well underway. Accumulation pace has doubled over four years. Net dollar-reduction intent has crossed into majority territory for the first time on record. Investors who read this as structural rather than cyclical are interpreting the same signal that gold-accumulating central banks are acting on.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Central banks are accumulating gold primarily to reduce dependence on reserves held in foreign sovereign currencies, which carry counterparty risk from another government's policy decisions. The 2022 freezing of approximately $300 billion in Russian sovereign assets demonstrated that foreign currency reserves can be made inaccessible overnight, accelerating the shift toward gold, which can be held domestically or in neutral vaults with no counterparty exposure.

The OMFIF survey, released 30 June 2026 and covering 90 sovereign institutions managing over $7 trillion in assets, found that 32% of central banks expect to increase gold holdings in the short term and a net 30% plan to do so over the next one to two years. Critically, it marked the first time on record that more central banks declared intentions to reduce dollar allocations than increase them.

De-dollarisation refers to the gradual reduction by central banks and reserve managers of their holdings in U.S. dollar-denominated assets, reallocating toward alternatives such as gold. The dollar's share of global reserves has already fallen from around 71% in 2001 to below 57% today, and as institutions redirect those allocations, gold benefits from a sustained, price-insensitive structural bid that supports prices across market cycles.

Goldman Sachs set an end-2026 gold price target of $4,900 per troy ounce in a note dated 29 June 2026, revised upward from $4,300 but down from a prior $5,400 figure. The firm's core thesis rests on ongoing reserve diversification by emerging market central banks and eventual tailwinds from interest rate movements, with the $4,900 target sitting toward the conservative end of the broader institutional consensus ranging from approximately $5,200 to $6,300.

Central banks have accumulated roughly 1,000 tonnes of gold per year over the past four years, double the approximately 500 tonnes per year pace of the preceding decade. Multiple independent surveys from the World Gold Council, OMFIF, and HSBC all confirm that forward-looking intentions remain at record highs, with 45% of WGC survey respondents planning to increase their own holdings over the next 12 months.