Marvell Technology Surges 22% on Nvidia CEO’s Trillion-Dollar Call

4 hrs ago

WTI crude surged 5.86% to settle at US$92.47 on 2 June 2026, while Brent crude spiked as much as 6.4% intraday, after Iran announced it was suspending diplomatic communications with the United States and threatening to seal the Strait of Hormuz. This is not a routine oil price swing. The Iran escalation is now transmitting directly into Federal Reserve rate expectations, bond markets, and financial conditions across the US economy, at a moment when incoming Fed Chair Kevin Warsh is preparing to lead his first FOMC meeting. What follows explains the diplomatic break that triggered the move, why the Strait of Hormuz threat carries outsized market weight, how the oil shock is repricing monetary policy on both sides of the Atlantic, and what the cascade means for investors holding rate-sensitive assets.

Iran’s state-affiliated Tasnim news agency reported that Iranian negotiators would cease communications with US counterparts, giving the announcement its official weight. Tehran cited Israeli military operations in Lebanon as the proximate justification, with Foreign Minister Araghchi specifically naming the inclusion of Lebanon in US ceasefire framing as a point of contention.

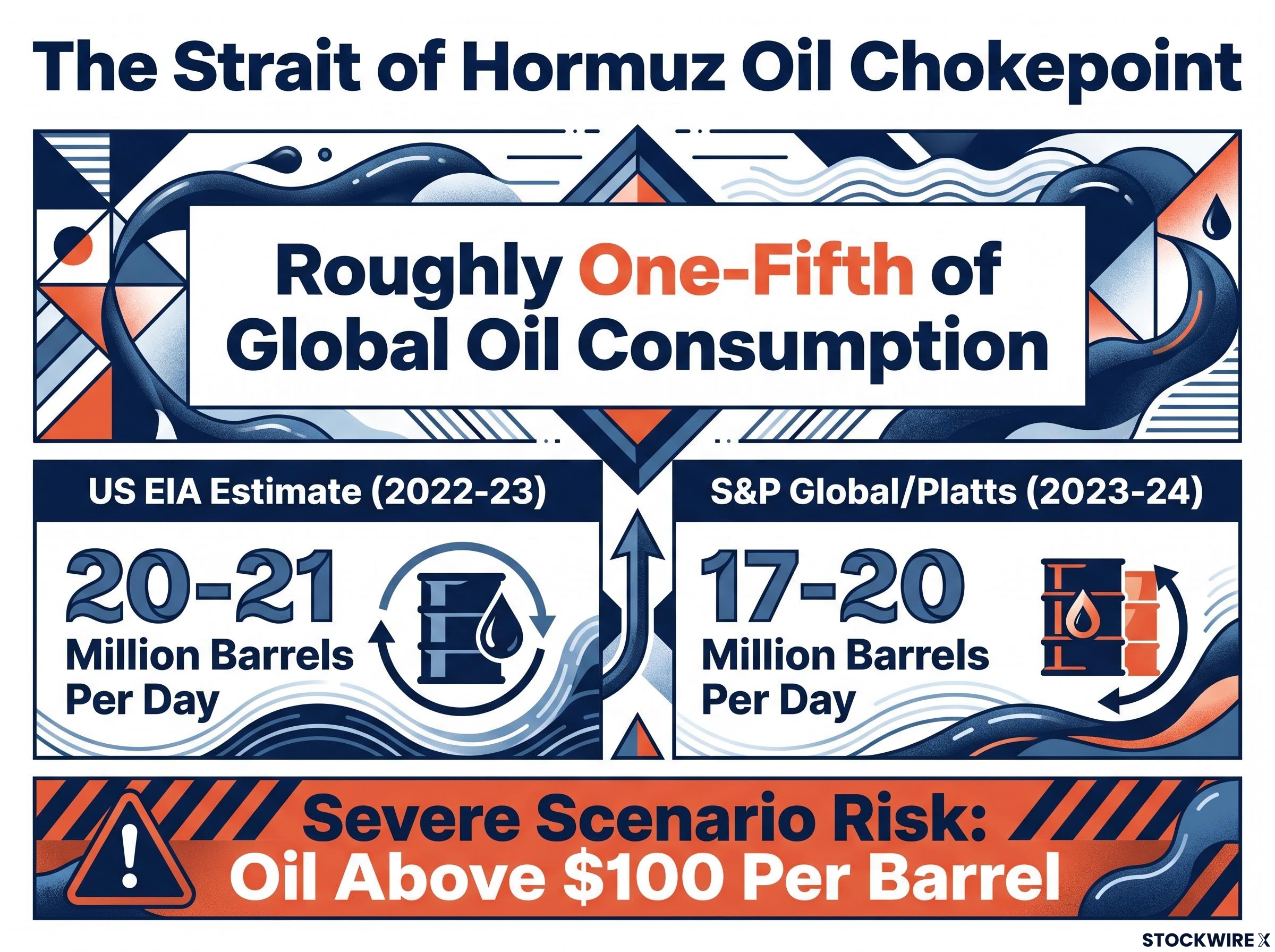

The diplomatic halt alone would have registered as geopolitical noise. What transformed it into a market event was the simultaneous threat to fully close the Strait of Hormuz, the narrow waterway through which roughly one-fifth of the world’s oil supply transits daily.

President Trump responded publicly by stating he was indifferent to the collapse of talks and accused Iran of deliberately prolonging negotiations, a signal that Washington has no immediate de-escalation path in play. Iran and allied parties also raised the possibility of activating the Bab el-Mandeb Strait as an additional pressure front.

Iran’s demand for permanent Hormuz authority represents the structural sticking point beneath the current escalation cycle: previous negotiation rounds collapsed specifically because Tehran refused to cede sovereign control over transit rights, a sovereignty framing that makes any interim diplomatic arrangement inherently fragile.

President Trump stated he was indifferent to the collapse of talks and accused Iran of deliberately prolonging negotiations, according to CNBC reporting.

With both chokepoints now explicitly on the table and no diplomatic off-ramp visible, the oil market’s response was swift.

WTI crude settled at US$92.47, a gain of 5.86% on the session. Brent crude told a slightly more textured story: it spiked as much as 6.4% intraday before pulling back to settle 3.6% higher at US$95.24. The gap between the intraday peak and the closing price suggests markets partially digested the initial fear trade before the bell.

The VIX climbed 4.77% to 16.05, confirming the move as a genuine risk-sentiment event rather than a thin-volume spike. The US 10-year Treasury yield rose approximately 8 basis points intraday but closed only 1 basis point higher at 4.475%, a similar pattern of partial retracement.

| Asset | Intraday Move | Settlement/Close | Level at Close |

|---|---|---|---|

| WTI Crude | +5.86% | +5.86% | US$92.47 |

| Brent Crude | Up to +6.4% | +3.6% | US$95.24 |

| VIX | +4.77% | +4.77% | 16.05 |

| US 10-Year Yield | +8bp | +1bp | 4.475% |

The spread between intraday moves and closing levels across both Brent and the 10-year yield tells readers something worth noting: markets walked back part of the fear trade by session’s end. Where genuine risk pricing now sits is somewhere between the intraday panic and the more measured close.

The Strait of Hormuz is a narrow waterway between Iran and Oman, and it is the single most concentrated oil transit point on earth. When Iran threatens to close it, markets do not treat the statement as rhetoric. They price it as a supply risk with very few short-term substitutes.

The scale explains why:

The Hormuz risk premium is not simply a function of whether the strait is physically open; the near-total withdrawal of commercial war-risk insurance has effectively closed it to standard tanker traffic even during periods when passage was technically possible, a dynamic that the IEA projects will take up to two years to fully unwind regardless of how quickly a diplomatic resolution emerges.

The EIA World Oil Transit Chokepoints data recorded total oil flows through the Strait averaging 20.9 million barrels per day in the first half of 2025, equivalent to approximately 20% of global petroleum liquids consumption and one-quarter of all maritime traded oil, figures that confirm why a credible closure threat registers as a first-order supply shock rather than background noise.

That volume concentration is what makes a Hormuz threat qualitatively different from other geopolitical oil risks. There is no readily available substitute for 20 million barrels per day. The market knows this, and the price action on 2 June reflected it.

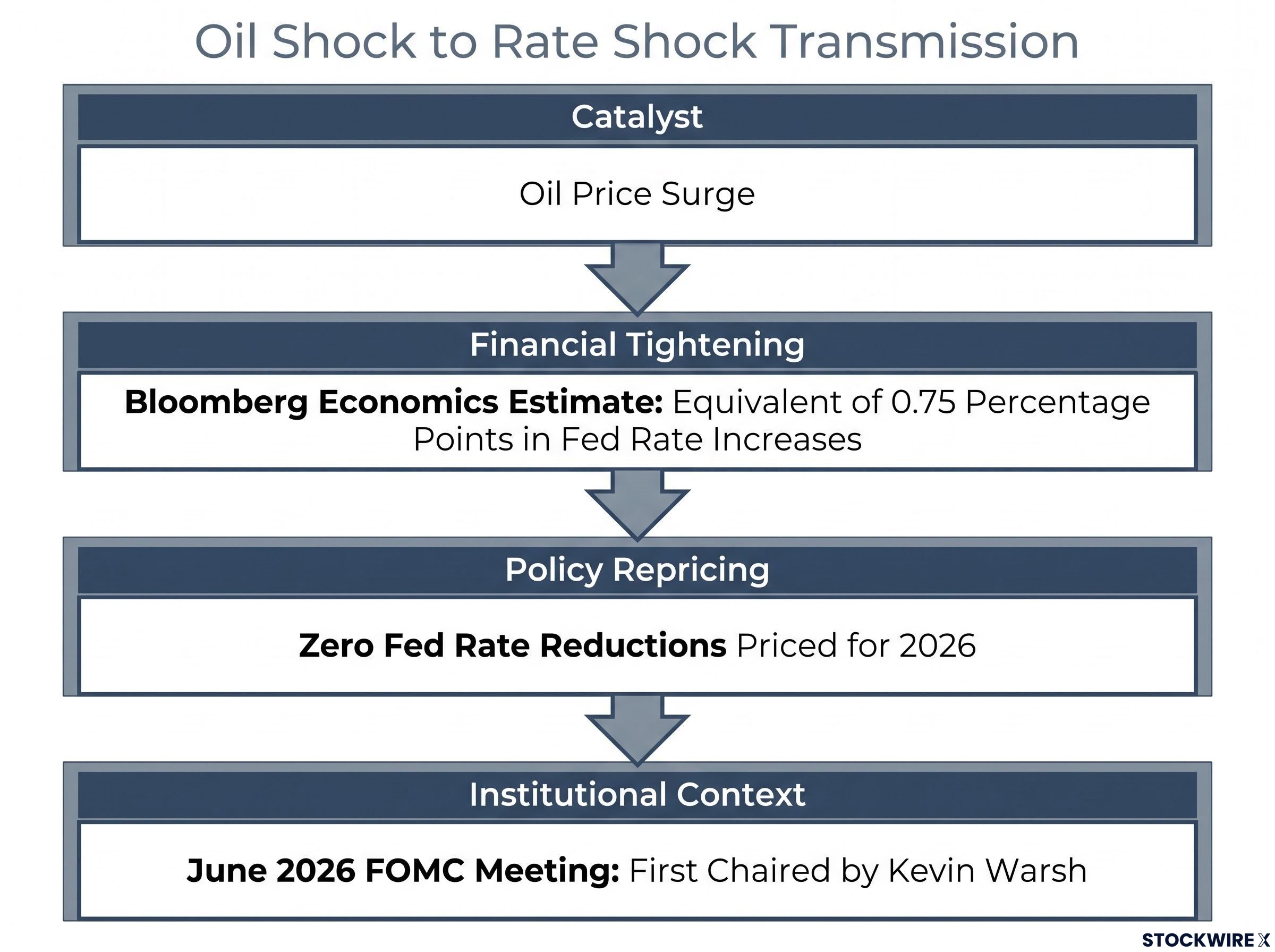

The chain runs in one direction. A sustained oil price shock feeds into headline inflation expectations, which pushes bond yields higher, which tightens financial conditions, which reduces the Federal Reserve’s capacity to cut rates without risking a re-acceleration of inflation. Unlike a technology-driven supply-side deflation, the Fed cannot look through a geopolitical oil shock because it lands directly in consumer energy costs, transportation, and goods pricing.

That transmission is no longer theoretical. It is showing up in the data.

Traders are currently pricing zero Federal Reserve rate reductions in 2026, with positioning tilted toward a potential rate increase. The oil-price surge has been identified as the primary catalyst behind this shift.

Bloomberg Economics estimated that the cumulative rise in bond yields since the onset of the Iran conflict has tightened US financial conditions by the equivalent of roughly 0.75 percentage points in Fed rate increases.

The 10-year Treasury yield closed at 4.475%, with its 8 basis point intraday move partially retracing by close. That intraday volatility reflects a market still calibrating how persistent this shock will prove.

The institutional backdrop adds a layer of uncertainty. The upcoming June 2026 FOMC meeting will be the first chaired by Kevin Warsh, while outgoing Chair Powell has cautioned that the central bank is undergoing a stress test due to executive branch pressure on its leadership. The rate-cut narrative that supported valuations in rate-sensitive sectors through early 2026 is now effectively off the table for the year.

The FOMC dissent record from the April meeting, the most divided single vote since 1992, means Warsh inherits a committee already fractured between hawks who formally opposed easing-oriented language and a lone dovish dissenter, an internal fault line that will shape how the June statement is drafted regardless of where the rate decision lands.

ECB board member Isabel Schnabel stated that inflationary spillover from the Iran conflict can no longer be disregarded, according to Bloomberg reporting. That language marks an upgrade from tail risk to a material policy consideration in the ECB’s framing.

ECB board member Schnabel stated that inflationary spillover from the Iran conflict “can no longer be disregarded,” signalling a shift in the ECB’s risk assessment.

For US investors, the ECB signal carries a specific implication. If the ECB tightens or hesitates to cut in response to the oil shock, it tends to strengthen the euro, pressure US export competitiveness, and signal that global rate expectations are moving in the same restrictive direction simultaneously. The Iran shock is repricing central bank behaviour on both sides of the Atlantic at once, which has consequences for international equity exposure and currency-hedged positions.

The asset classes most directly under pressure sit at the intersection of the oil shock and the rate repricing. Rate-sensitive equities, including growth stocks and REITs, face valuation compression as the zero-cuts, lean-toward-hike environment removes the rate relief that underpinned their early 2026 performance. Long-duration bonds carry mark-to-market risk if yields continue climbing. High-yield credit faces spread widening as tightening financial conditions increase default risk at the margin.

Energy equities are positioned as a relative beneficiary. Higher oil prices directly support earnings for upstream producers, though geopolitical risk creates headline volatility in the sector. Strategist guidance from 2023-24 geopolitical episodes advised overweight positioning in energy equities and long-duration Treasuries as hedges during oil spikes; that historical context informs the current environment but does not constitute June 2026-specific advice.

Investors reassessing portfolio positioning in light of the zero-cuts, lean-toward-hike environment will find our dedicated guide to investing during rate hikes, which walks through sector rotation toward high-margin, low-debt equities, the case for energy services exposure, and specific criteria for avoiding highly leveraged names that face acute refinancing risk as financial conditions tighten.

Three variables will determine whether the current repricing deepens or reverses:

2 June 2026 may mark the moment the Iran conflict graduated from a background geopolitical risk into an active driver of US financial conditions. The Bloomberg Economics estimate of 0.75 percentage points of equivalent tightening quantifies how far the transmission has already progressed. Energy market resilience, Fed institutional independence under new leadership, and the market’s capacity to price geopolitical risk accurately are all being tested simultaneously.

Uncertainty remains substantial. The Hormuz threat has not been acted upon. Diplomatic channels have not been permanently severed. The oil price move could partially reverse if de-escalation signals emerge. The forward-looking tension that will define the coming weeks is whether this proves a transient spike that markets reabsorb, or the beginning of a sustained shift in the global oil and rate environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding Fed policy, oil prices, and geopolitical developments are speculative and subject to change based on evolving conditions.

The Strait of Hormuz is a narrow waterway between Iran and Oman through which roughly one-fifth of the world's daily oil supply transits. Any credible threat to close it immediately triggers a supply shock because there are very few viable rerouting alternatives in the short term.

WTI crude surged 5.86% to settle at US$92.47, while Brent crude spiked as much as 6.4% intraday before closing 3.6% higher at US$95.24, marking one of the sharpest single-session oil price moves in months.

A sustained oil shock feeds into headline inflation, which pushes bond yields higher and tightens financial conditions, reducing the Fed's ability to cut rates without risking a re-acceleration of inflation. Traders are currently pricing zero Fed rate cuts in 2026, with positioning tilted toward a potential rate increase.

Rate-sensitive equities such as growth stocks and REITs face valuation compression, long-duration bonds carry mark-to-market risk if yields continue rising, and high-yield credit faces spread widening as financial conditions tighten. Energy equities are positioned as a relative beneficiary given higher oil prices support upstream producer earnings.

Three key variables will determine whether the repricing deepens or reverses: whether Iran acts on the Hormuz closure threat or it remains rhetorical, how the June 2026 FOMC meeting under Kevin Warsh addresses the oil shock in its forward guidance, and whether the 10-year Treasury yield sustains above its intraday highs or retreats toward its session close level.