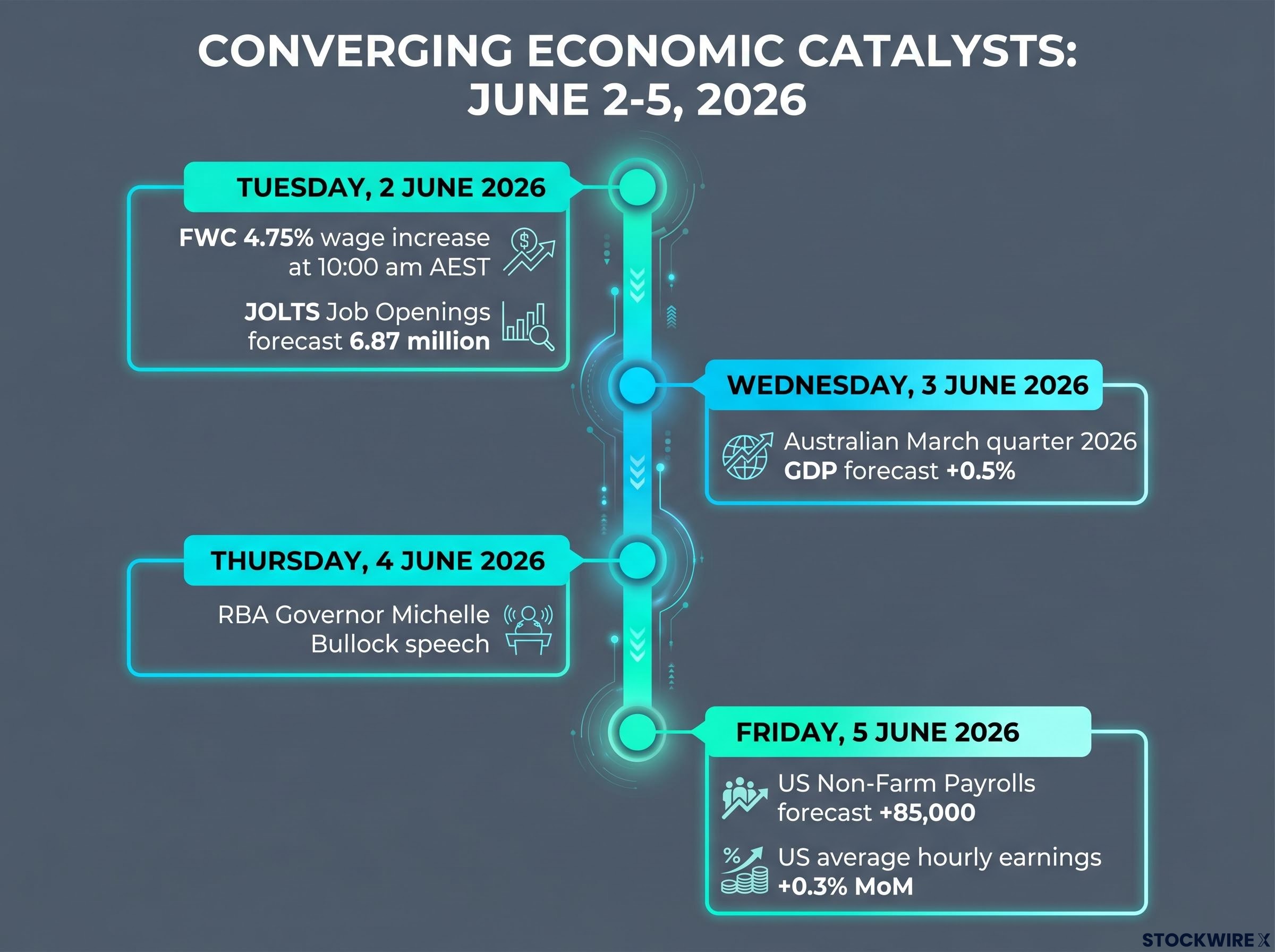

The Fair Work Commission delivered its 2026 Annual Wage Review at 10:00 am AEST on Tuesday, 2 June 2026, and the ASX responded within minutes. A 4.75% increase to modern award minimum wages, effective from the first full pay period on or after 1 July 2026, sent selling pressure rippling across sectors that share almost nothing in common except sensitivity to interest rate expectations. Real estate trusts, consumer discretionary retailers, major banks, and healthcare stocks all fell in the same session, driven by a single regulatory decision that immediately repriced the probability of a Reserve Bank of Australia (RBA) rate hike in August.

The wage outcome did not arrive in isolation. It landed on a market already absorbing weak building approvals data and bracing for a quarter of GDP figures, an RBA governor’s speech, and US labour market releases. What follows is a framework for understanding how a scheduled wage decision transmits through bond yields, discount rates, and sector valuations to reprice an entire index in a single morning.

The policy catalyst and the immediate rate repricing

The numbers were precise. The FWC mandated a 4.75% increase to modern award minimum wages, lifting the National Minimum Wage to $26.44 per hour, or $1,004.90 per week. That weekly figure represents an approximate 6% increase overall, reflecting the compounding effect across different award classifications. The new rates take effect from the first full pay period on or after 1 July 2026.

Markets did not treat this as a labour story. They treated it as a monetary policy signal. The wage figure marginally exceeded expectations, and the immediate interpretation was that the RBA’s case for holding rates steady had weakened. Sticky wage growth feeds directly into the services inflation readings that the central bank has repeatedly flagged as its primary concern.

Services inflation readings have been the RBA’s stated primary concern throughout the 2026 tightening cycle, with trimmed mean CPI holding at 3.3% even as volatile fuel costs drove the headline figure to 4.6% in March 2026, a divergence that gave the Board the evidence it needed to maintain a tightening bias.

A Citi note released following the announcement indicated the wage outcome kept an August RBA rate hike firmly in prospect, contributing to upward pressure on benchmark bond yields across the session.

Bond yields moved first. Equity valuations followed. The ASX 200 broad-based sell-off was not panic; it was repricing. Every sector with duration sensitivity, leverage exposure, or margin vulnerability to labour costs absorbed the shift simultaneously. The speed of the reaction reflected how tightly Australian equities are now tethered to the RBA’s next move.

When big ASX news breaks, our subscribers know first

How wage policy transmits to equity valuations

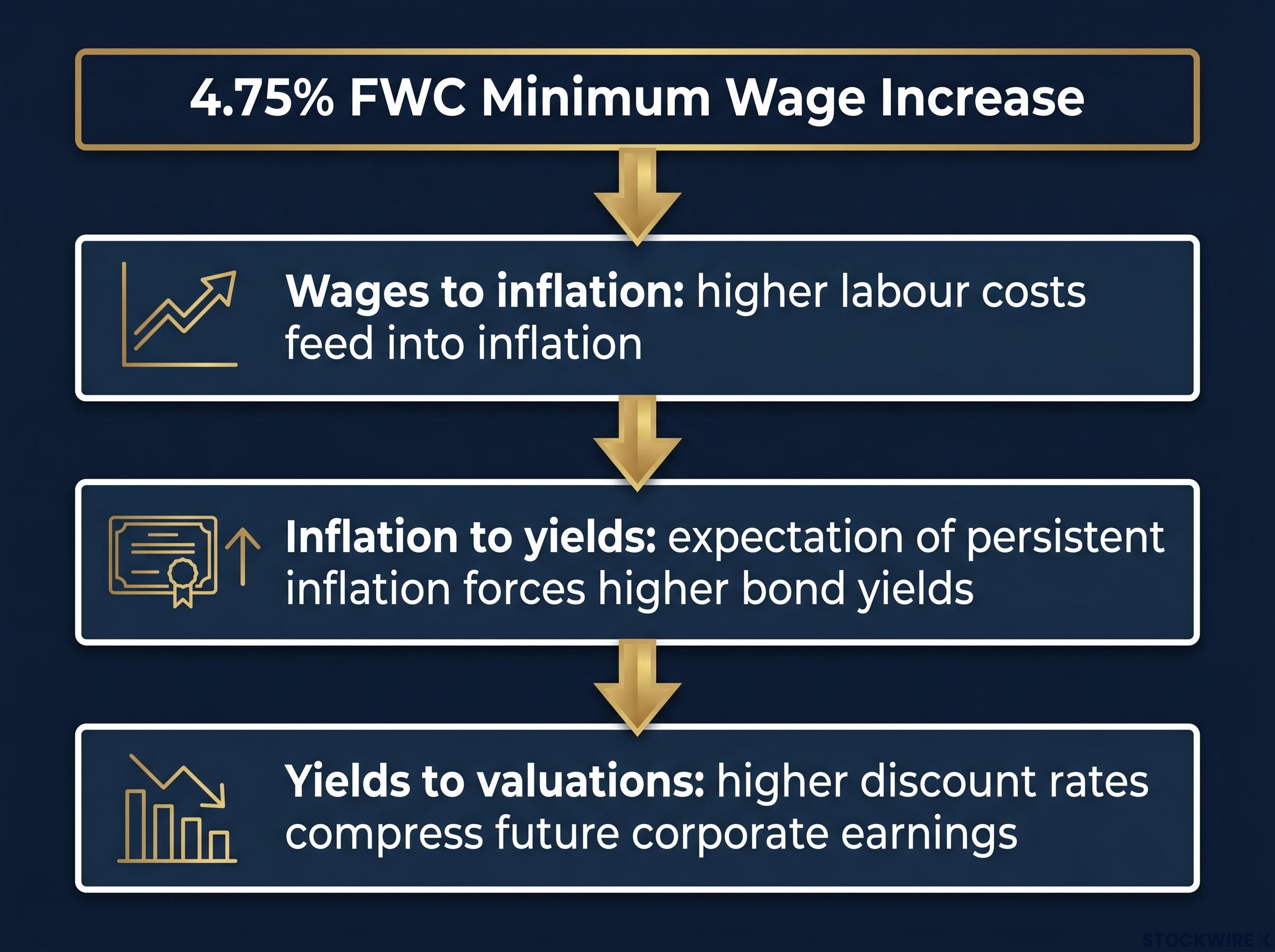

The connection between a minimum wage decision and a falling share price in, say, a healthcare company or a real estate trust is not obvious. It runs through a three-step transmission mechanism that central banks monitor closely.

- Wages to inflation: When minimum wages rise above productivity growth, businesses face higher labour costs. Those costs are either absorbed (compressing margins) or passed on to consumers (pushing up prices). Either path feeds into inflation readings, particularly in services-heavy sectors where labour is the dominant input cost. This dynamic is sometimes referred to as cost-push inflation, where rising production costs rather than rising demand drive price increases.

- Inflation to yields: Persistent inflation, or even the expectation of persistent inflation, forces central banks to keep interest rates higher for longer. Bond markets price this in immediately. Benchmark yields rise as traders demand greater compensation for holding fixed-income instruments in an inflationary environment.

- Yields to valuations: Higher bond yields raise the discount rate applied to future corporate earnings. A company’s projected cash flows five or ten years from now are worth less in today’s dollars when the discount rate increases. Share prices fall to reflect this reduced present value, even before the company reports any actual change in its earnings.

This mechanism explains why ASX valuation multiples have historically contracted during periods of rising bond yields, regardless of whether the underlying companies had direct wage exposure. The discount rate is sector-agnostic; it compresses every future earnings stream equally.

ASX valuation multiples contracted sharply in April 2026 as the CPI print of 4.6% shifted rate expectations, with REITs, discretionary consumer stocks, and high-multiple growth companies absorbing the steepest sector-level derating, a pattern that the FWC wage decision on 2 June reproduced almost identically.

Margin compression across consumer discretionary and staples

Retailers and hospitality operators absorbed the most direct hit. For these businesses, the wage decision was not an abstract rate signal. It was a line item on next quarter’s profit and loss statement.

Discretionary retailers take the immediate brunt

Domino’s Pizza Enterprises fell 5.9% to $16.55. JB Hi-Fi dropped 5.4% to $71.05. Myer declined 4.0%. These are businesses with highly elastic demand, meaning consumers can defer or substitute purchases when budgets tighten. The market priced in a dual threat: higher labour costs eating into operating margins and a potential RBA rate hike squeezing household disposable income further. The combination left discretionary names facing both cost-side and revenue-side pressure simultaneously.

Defensive staples show relative resilience

Consumer staples fell as a sector, with the XSJ index declining 1.31% on the session compared to the XDJ’s 0.60% drop. Yet the individual stock movements told a more nuanced story. Treasury Wine Estates fell 2.6%, while Woolworths dropped 1.9% and Coles declined just 0.7%.

The divergence reflects pricing power. Woolworths and Coles operate massive award-wage workforces, and the 4.75% increase will flow directly into their cost bases. However, supermarket duopolies possess the ability to pass those costs through to consumers via shelf prices, a lever that discretionary retailers cannot pull as easily. The market’s relatively contained reaction to the two grocery giants reflected confidence in that pass-through capacity, even as the sector as a whole traded lower.

| Company | Ticker | Sector Category | Daily Drop |

|---|---|---|---|

| Domino’s Pizza Enterprises | DMP | Discretionary | -5.9% |

| JB Hi-Fi | JBH | Discretionary | -5.4% |

| Myer | MYR | Discretionary | -4.0% |

| Treasury Wine Estates | TWE | Staples | -2.6% |

| Woolworths | WOW | Staples | -1.9% |

| Coles | COL | Staples | -0.7% |

The yield squeeze on real estate, financials, and healthcare

The worst-performing sector on 2 June 2026 had almost no direct exposure to minimum wage labour. The ASX 200 Real Estate sector (XPJ) fell 1.44%, outpacing the declines in consumer-facing sectors. The mechanism was pure yield compression.

Real Estate Investment Trusts (REITs) carry substantial debt. Higher bond yields raise the cost of servicing that debt while simultaneously narrowing the spread between property yields and risk-free rates, making REITs less attractive as income investments. Stockland dropped 4.3% to $3.79. Vicinity Centres fell 4.0%. GPT Group declined 2.7%. For retail-exposed REITs specifically, the wage decision carried a secondary concern: if labour costs pressure retail tenant margins, the ability of those tenants to service lease obligations weakens.

Bond yield and dividend yield compression was also the primary driver of the ASX’s 2.04% decline on 8 May 2026, when a Strait of Hormuz military exchange triggered an overnight rise in government bond yields and erased an estimated $100 billion in Australian market capitalisation, with financials and real estate again absorbing the heaviest losses.

The Financials sector (XFJ) lost 1.00%, with credit quality concerns at the centre. A potential August rate hike raises the risk that mortgage holders already under stress could tip into default. AMP fell 4.4% to $1.53, ANZ dropped 3.0%, and Westpac declined 1.5%.

Healthcare continued its position as one of the weakest major sectors on the ASX. The XHJ fell 1.21%, with Cochlear dropping 4.3% to $96.74 and Telix Pharmaceuticals falling 3.0%. These are long-duration growth stocks whose valuations depend heavily on earnings projected years into the future. When discount rates rise, those distant earnings compress in present-value terms more than any other sector category.

| Company | Ticker | Sector | Daily Drop |

|---|---|---|---|

| Stockland | SGP | Real Estate | -4.3% |

| Vicinity Centres | VCX | Real Estate | -4.0% |

| GPT Group | GPT | Real Estate | -2.7% |

| AMP | AMP | Financials | -4.4% |

| ANZ | ANZ | Financials | -3.0% |

| Westpac | WBC | Financials | -1.5% |

| Cochlear | COH | Healthcare | -4.3% |

| Telix Pharmaceuticals | TLX | Healthcare | -3.0% |

The next major ASX story will hit our subscribers first

Converging economic catalysts beyond the wage decision

The FWC ruling did not land on a clean slate. Australian May 2026 building approvals had already fallen 3.4% month-on-month earlier in the week, significantly worse than the forecast 1.5% decline and following a 10.5% contraction the prior month. The housing construction pipeline is weakening at precisely the moment the market is pricing in higher borrowing costs.

The remainder of the week presents a series of data releases capable of either reinforcing or unwinding the rate hike fears triggered on Tuesday.

- Wednesday, 3 June 2026: Australian March quarter 2026 GDP, forecast at +0.5% quarter-on-quarter, a slower pace of expansion relative to the +0.8% result in the December quarter.

- Thursday, 4 June 2026: RBA Governor Michelle Bullock delivers a scheduled speech, the first public remarks since the FWC decision and a likely focal point for forward guidance on the August meeting.

- Friday, 5 June 2026: US Non-Farm Payrolls for May, forecast at +85,000 (down from +115,000 in April), alongside US average hourly earnings forecast at +0.3% month-on-month.

The US data matters because global bond yields move in tandem. If American wage growth accelerates alongside Australian wage growth, the combined signal could harden expectations of tighter monetary policy in both economies. The JOLTS Job Openings release (forecast at 6.87 million) on Tuesday evening provides an early read on US labour demand before Friday’s payrolls figure.

Navigating the pathway to the August RBA meeting

The 4.75% Fair Work wage rise has shifted the market’s posture from cautious optimism about rate relief to active defence against a potential August hike. The RBA’s inflation calculus now includes a confirmed wage input that exceeds productivity growth, feeding directly into the services inflation readings the central bank has identified as the binding constraint on rate cuts.

Governor Bullock’s speech on Thursday, 4 June 2026 is the next inflection point. The tone of those remarks will signal whether the RBA views the FWC decision as confirmation of sticky inflation or as a manageable one-off within a broader disinflationary trend.

Until then, the repricing that began on Tuesday morning remains the market’s working assumption. Investors holding duration-sensitive positions, leveraged REITs, or margin-exposed consumer names face a week where every data point either confirms or challenges the higher-for-longer thesis.

Investors wanting to model the full RBA policy pathway will find our full explainer on Australia’s labour market cooling, which covers the April 2026 unemployment rise to 4.5%, the trend versus seasonally adjusted divergence, and why all four major banks still see any rate cut as a late-2026 event despite the headline softening.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.