S&P 500 Breaks 7,200 as Markets Shrug Off $126 Oil Spike

44 mins ago

U.S. digital health startups raised $14.2 billion in 2025, yet most of that capital flowed to a handful of AI-branded mega-deals where clinical documentation platforms and pharma AI companies commanded nine-figure rounds. The companies attracting attention at the earliest stages often tell a more revealing story about where the next generation of health innovation is headed. The AI Health Fund’s Treehub accelerator, backed by Tim Draper and Anne Wojcicki and led by founding partner Mary Minno, operates with a $10 million target fund and has already invested in 12 startups. Its April 2026 launch signals a deliberate bet on pre-commercial, academically rooted founders in four underserved health categories: hormone monitoring, autism behavioural tracking, environmental home health, and predictive patient outcomes.

This piece profiles the four portfolio companies at the core of that thesis, maps each against current market gaps and funding dynamics, and draws out what the portfolio’s composition signals for investors watching early-stage health tech capital flows.

The Treehub accelerator runs quarterly cohorts through six-month programmes, injecting $100,000 in early capital per participant and recruiting explicitly from academic and scientific founder pools. That model is unusual. Most health tech accelerators cast a wider net; Treehub’s constraint is deliberate, filtering for founders whose work originates in peer-reviewed research rather than product-market intuition alone.

Pre-incorporation funding models like Treehub are designed specifically to capture scientific intellectual property before formal corporate structures exist, securing equity at valuations that would be unavailable to investors entering at the seed or Series A stage; the logic is that academic founders rarely have the commercial infrastructure to incorporate quickly, and the fund that moves earliest sets the ownership terms.

The fund closed its initial $1.5 million against a $10 million target. Mary Minno, a former Google executive, leads the fund’s thesis development alongside backing from Tim Draper and Anne Wojcicki. The size of the fund itself is part of the signal: a $10 million vehicle operating inside a $14.2 billion ecosystem is not trying to index the market. It is making concentrated category bets.

The scale gap between the AI Health Fund and the broader digital health ecosystem is worth sitting with. AI-enabled companies captured approximately 54% of total digital health funding in 2025, and the capital premium for AI branding is measurable at every stage.

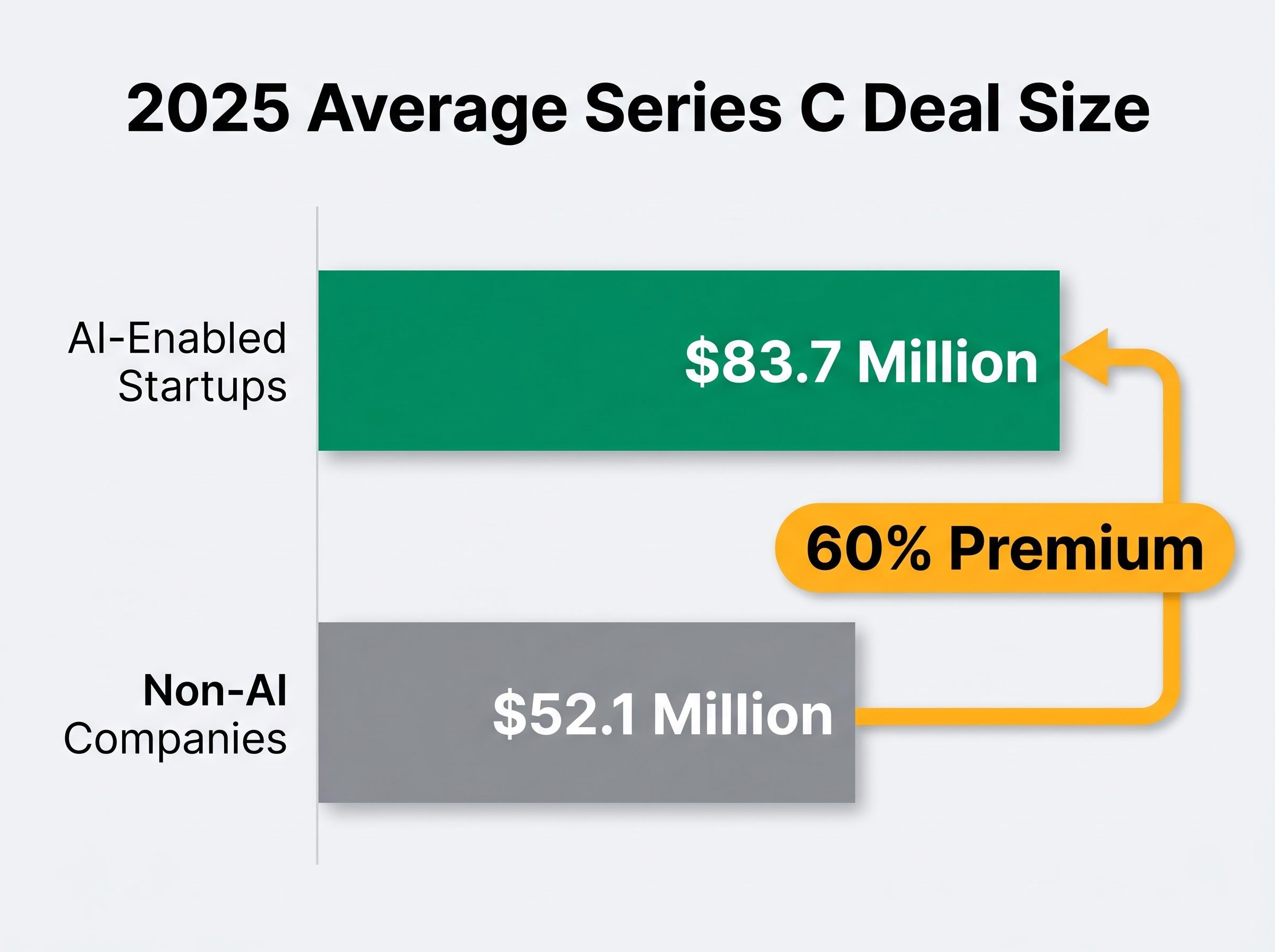

Rock Health’s 2025 funding overview recorded AI-enabled companies capturing approximately 54% of total digital health capital, with the average Series C deal size for AI-branded startups reaching $83.7 million compared with $52.1 million for non-AI companies, a premium that reflects how thoroughly AI positioning has reshaped investor pricing at every stage.

The average Series C deal size for AI-enabled startups reached $83.7 million in 2025, compared with $52.1 million for non-AI companies, a 60% premium that reflects the degree to which investors are paying up for AI positioning.

Rock Health’s 2025 year-end overview flagged the downstream risk: rapid fundraising cycles leave early companies with narrow windows to prove clinical and commercial progress before capital runs out. That dynamic is what makes a small, thesis-driven fund’s portfolio choices legible as signal rather than noise. The categories it chose to back are the ones it believes existing capital flows have systematically missed.

Clair Health has already generated the kind of early commercial traction that shifts the conversation from concept to execution. The Stanford-founded company, launched in 2025 by Jenny Duan and Abhinav Agarwal, is building the first noninvasive continuous hormone monitoring wearable, and its revenue numbers suggest demand arrived before the product did.

The $18 million in B2B contracts is the standout commercial signal. It suggests enterprise buyers, likely fertility clinics, women’s health platforms, or employer benefits programmes, are willing to commit before broad market availability.

That B2B figure is what de-risks the go-to-market question for investors evaluating the round. Consumer wearables live and die by adoption curves; enterprise contracts provide revenue visibility regardless of consumer launch timing.

Enterprise contract dynamics in women’s digital health suggest that institutional buyers are often willing to commit capital ahead of broad consumer availability, a pattern visible in HeraMED’s experience deploying its maternity care platform through partnership agreements with established health systems before achieving full commercial rollout, and one that maps closely to the structure of Clair Health’s $18 million in B2B contracts.

The structural gap Clair Health is targeting remains open. No FDA-approved continuous hormone monitor exists as of April 2026, which means the regulatory pathway is an unresolved variable. The absence of approved comparables also means the company faces no direct competitive pressure from incumbents in the category, a window that will not stay open indefinitely.

The two most clinically complex startups in the portfolio share a common commercial logic: both address populations whose care coordination failures generate outsized downstream healthcare costs. The cost of inaction is not abstract; it is billable.

Diggy originated from clinical autism mitigation research led by Dennis Wall and has since expanded into a comprehensive behavioural tracking system. The platform sits within the autism diagnostics technology category, a space so early that no categorised investment data exists for it as a defined health tech subcategory as of April 2026.

No funding round has been publicly disclosed, which is consistent with the company’s accelerator-stage positioning rather than a signal of weakness. The absence of comparable benchmarks is a feature of underfollowed categories, not a warning sign. Sparse comps data often precedes category formation.

The autism diagnostics FDA pathway is beginning to take shape through companies operating outside the Treehub portfolio: BlinkLab’s pivotal 510(k) validation study, initiated in March 2026 across ten US clinical sites, provides a real-world reference point for the regulatory timeline and evidence standards that any behavioural tracking platform serving the autism population will eventually face.

Korda (formally Koda Health) addresses one of the widest gaps in serious illness care: most patients do not have documented goals-of-care conversations. That absence creates clinical inefficiencies when treatment decisions are made without patient preferences on record, and financial inefficiencies when default aggressive care pathways are followed in the absence of alternatives.

Health Affairs research on advance directive completion found that only around one in three U.S. adults has any documented end-of-life preferences on record, quantifying the scale of the care coordination gap that platforms like Korda are designed to close and illustrating why default aggressive treatment pathways remain the clinical norm in the absence of structured patient guidance.

The Houston-based platform raised a $7 million Series A in October 2025, a round that signals regional health system interest in AI-guided advance care planning tools. The platform facilitates structured goals-of-care conversations and patient decision support, automating a process that currently depends almost entirely on overstretched clinical staff.

| Company | Clinical Focus | Funding Stage | Notable Backer(s) | Commercial Model |

|---|---|---|---|---|

| Diggy | Behavioural tracking for autism populations | Accelerator / Pre-disclosed | AI Health Fund / Treehub | Clinical analytics platform |

| Korda (Koda Health) | AI-guided advance care planning | $7M Series A (October 2025) | AI Health Fund / Treehub | Health system SaaS |

NestWell Health operates as a telehealth platform for aging-in-place, a category that most digital health investors have not yet named as a thesis. The platform underwent a rebrand and expanded its facilities in 2025, positioning around three distinct value propositions:

No defined investment category for environmental wellness platforms currently exists in major funding databases as of April 2026. That absence cuts both ways. It means NestWell has few direct comparables, but it also means institutional investors have not yet built conviction in the category, creating a window for early-stage entrants.

The structural tailwind is demographic. The U.S. aging population is growing faster than the infrastructure designed to serve it, and aging-in-place technology addresses the gap between where older adults want to live and where the healthcare system can currently reach them. Environmental home health is less obscure than overlooked; the clinical need is validated, even if the investment category is not.

Read together, the four companies form a coherent thesis. All four target chronic underservice in diagnostics, behavioural health, end-of-life care, or environmental wellness, categories that sit outside the AI clinical documentation and pharma AI verticals dominating 2025 deal flow. Abridge commands a $5.3 billion valuation in clinical documentation (28.7% of disclosed capital), and Xaira Therapeutics launched with $1 billion in pharma AI (25.5% of disclosed capital). The AI Health Fund’s portfolio deliberately avoids both.

Rock Health’s 2025 data flagged capital concentration and elevated valuations in AI mega-deals, suggesting that early-stage category differentiation is increasingly how smaller funds generate returns in a market where late-stage entry points have compressed.

Flare Capital has been cited as one of few funds specialising in early-stage health technology, but the broader pattern holds: most generalist digital health investors are gravitating toward later-stage AI rounds, leaving pre-commercial categories under-resourced.

For investors tracking this space, three signals over the next 12-18 months will determine whether the AI Health Fund’s thesis converts into category-defining positions:

Medicare reimbursement mechanics represent a downstream milestone that device-based health tech companies must navigate after FDA clearance, and the financial architecture looks materially different from SaaS subscription models: per-patient billing codes, monthly reimbursement cycles, and dual revenue streams combining facility subscriptions with CPT-code-based claims create a commercial structure that rewards clinical deployment scale rather than pure user acquisition.

The AI Health Fund’s portfolio is less a collection of individual bets and more a structured thesis about where early-stage health innovation has been systematically undercapitalised relative to clinical need. The four companies operate in categories where the problems are validated but the investment infrastructure is not, a pattern that either resolves through category formation or stalls at the pre-commercial stage.

The validation events are specific: regulatory movement, enterprise contract announcements, and Series A activity across the portfolio. As AI mega-deals continue to compress returns for late-stage health tech investors, early-stage category conviction funds like the AI Health Fund represent an increasingly distinct risk-return profile.

Whether that profile rewards its backers depends on the question that defines all accelerator-stage investing: can these categories attract the follow-on capital required to move from thesis to proof?

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding company performance, regulatory outcomes, and fundraising activity are speculative and subject to change based on market developments.

Among the most notable early-stage health tech startups are Clair Health (noninvasive hormone monitoring), Diggy (autism behavioural tracking), Korda (AI-guided advance care planning), and NestWell Health (aging-in-place environmental wellness), all backed by the AI Health Fund's Treehub accelerator.

Treehub is a quarterly cohort accelerator backed by Tim Draper and Anne Wojcicki and led by Mary Minno, targeting a $10 million fund that invests $100,000 per participant in pre-commercial, academically rooted health tech founders across four underserved health categories.

Clair Health has generated $800,000 in direct-to-consumer revenue and $18 million in B2B contracts ahead of its broader 2026 launch, with backing from a16z Speedrun, Reach Capital, and the AI Health Fund.

AI-branded companies captured roughly 54% of digital health funding in 2025 and commanded a 60% Series C valuation premium over non-AI peers, compressing returns for late-stage investors and making pre-commercial category bets in underserved areas an increasingly distinct risk-return opportunity.

Key signals to monitor over the next 12-18 months include FDA regulatory movement on noninvasive hormone monitoring for Clair Health, Series A or B announcements for Diggy and NestWell, and expansion of Korda's health system contract pipeline beyond pilot programmes.