WTI Jumps 1.6% as Iran Strikes Shatter Hormuz Deal Hopes

1 hr ago

Cisco shares surged 16.5% on 14 May 2026, marking one of the largest single-session moves in the company’s recent history. The catalyst was a combination that would normally seem contradictory: nearly 4,000 job cuts announced alongside the strongest guidance upgrade the company has issued in recent quarters. The announcement arrived as U.S. equity markets were already trading at all-time highs, with AI-linked technology names leading a multi-week advance. For investors tracking the AI infrastructure buildout, Cisco’s move offered a specific, concrete data point about how legacy enterprise technology companies are converting hyperscaler spending into revenue growth, and what restructuring costs that transition requires. What follows breaks down the quarterly results, the guidance raise, the restructuring mechanics, the broader sector context, and what the combined signals mean for investors watching this space.

The quarterly numbers arrived first, and they did the heavy lifting. Cisco reported Q3 FY2026 revenue of $15.8 billion, representing 12% year-on-year growth, a figure that stands out for a company of this scale operating in mature enterprise networking markets.

Q3 FY2026 revenue: $15.8 billion, up 12% year-on-year.

Earnings told a more layered story. GAAP earnings per share came in at $0.85, up 37% year-on-year, while non-GAAP EPS reached $1.06, up 10% over the same period. The gap between those two figures is worth flagging: the GAAP number includes accounting items that can distort the underlying profitability picture, while the non-GAAP figure strips those out. Investors tracking operating performance should consider both.

| Metric | Q3 FY2026 Result |

|---|---|

| Revenue | $15.8B (12% YoY growth) |

| GAAP EPS | $0.85 (up 37% YoY) |

| Non-GAAP EPS | $1.06 (up 10% YoY) |

The company cited surging orders from hyperscale data centre operators as the primary demand driver, and outlined four investment pillars shaping its forward positioning:

These results set the stage for what came next. The guidance raise was not a hope; it was built on reported numbers.

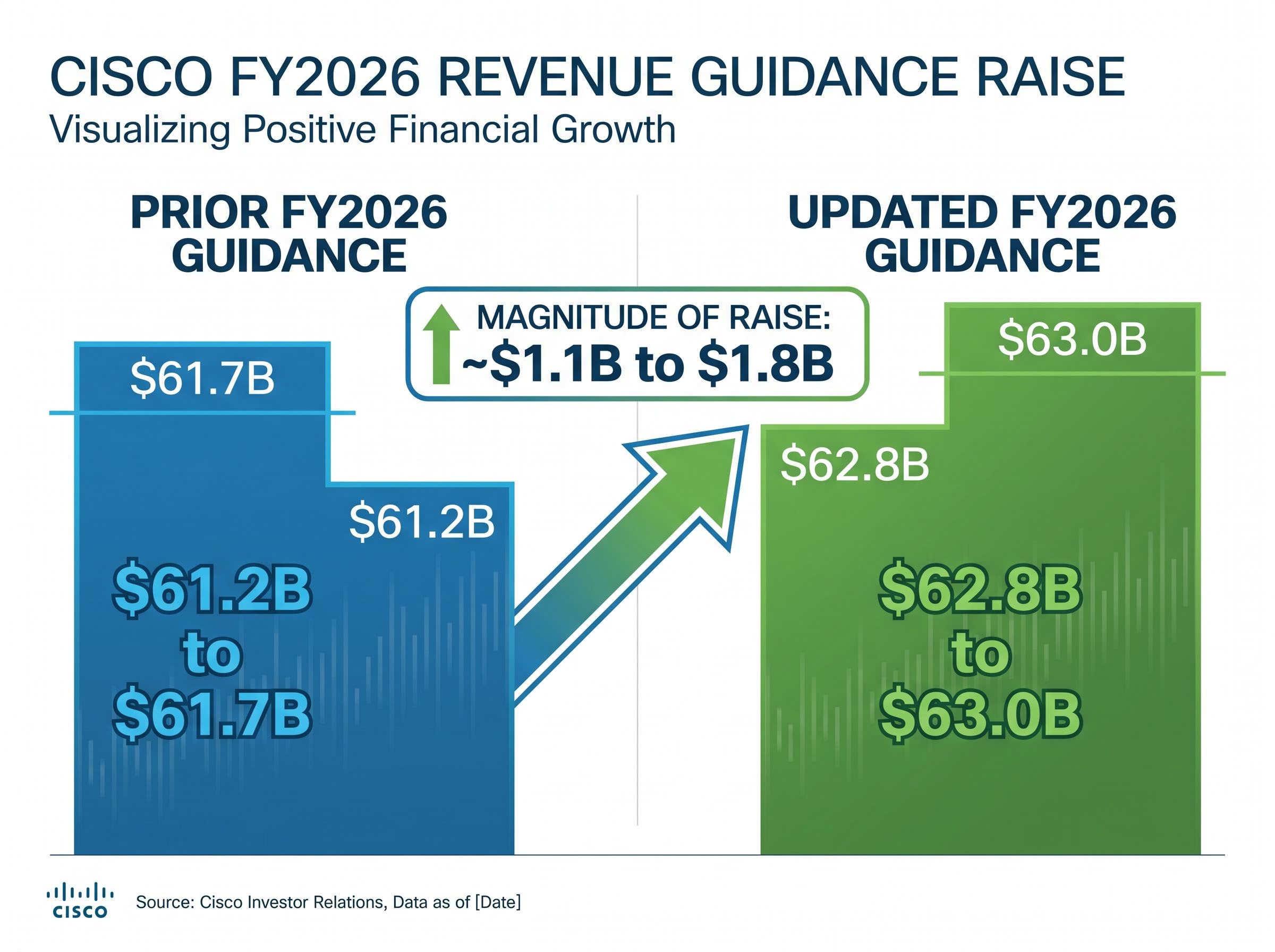

Cisco raised its full-year FY2026 revenue guidance from a prior range of $61.2 billion to $61.7 billion to an updated range of $62.8 billion to $63.0 billion. The arithmetic matters: that is an upgrade of approximately $1.1 billion to $1.8 billion, depending on where within the old and new ranges the comparison is drawn.

| Prior Guidance | Updated Guidance | Magnitude of Raise |

|---|---|---|

| $61.2B – $61.7B | $62.8B – $63.0B | ~$1.1B – $1.8B |

At a company generating more than $60 billion in annual revenue, a raise of this scale typically reflects more than routine quarter-end optimism. Upgrades at this magnitude suggest management has order backlog visibility or confirmed demand commitments that justify resetting both the floor and the ceiling. Cisco cited hyperscaler demand as the explicit basis for the revision. Specific customer names and contract values were not disclosed, which is standard practice at this stage of earnings reporting.

The AI order growth numbers behind the guidance raise are more specific than the headline revenue figure suggests: Cisco booked $2.1 billion in AI orders during Q3 alone and nearly doubled its full-year FY2026 AI order forecast to $9 billion, with networking products growing more than 50% and data-centre switching growing more than 40% year on year.

The market’s immediate verdict: Cisco shares rose approximately 17% in after-hours trading on 13 May 2026.

That after-hours move preceded the 16.5% regular-session gain the following day, signalling that institutional buyers were responding to the guidance revision as a substantive demand signal, not a cosmetic adjustment.

Hyperscale data centre operators are the large cloud platform companies building AI training and inference infrastructure at massive scale. These firms are constructing facilities that house thousands of specialised processors, and every one of those processors needs to communicate with the others at extraordinary speed. That communication layer, the networking fabric connecting AI chips across a data centre, is where Cisco competes.

Hyperscaler AI capital expenditure reached $130 billion in Q1 2026 alone across Amazon, Microsoft, Alphabet, and Meta, with full-year 2026 combined projections approaching $725 billion; that spending base is the demand pool Cisco is drawing from when it cites surging data centre orders as the driver behind its guidance revision.

The company’s four investment pillars map directly onto what hyperscalers need:

This is not an opportunistic pivot. Cisco has spent decades building enterprise networking infrastructure; the hyperscaler AI buildout is creating demand for higher-performance versions of the same product categories the company already manufactures.

The broader context reinforces the pattern. Across the technology sector, approximately 135,724 jobs have been cut across 308 layoff events year-to-date through mid-May 2026, per TrueUp tracking, with AI prioritisation cited as a common restructuring driver at Microsoft, Oracle, Meta, and Amazon. The spending is shifting, and companies are reshaping their workforces to match.

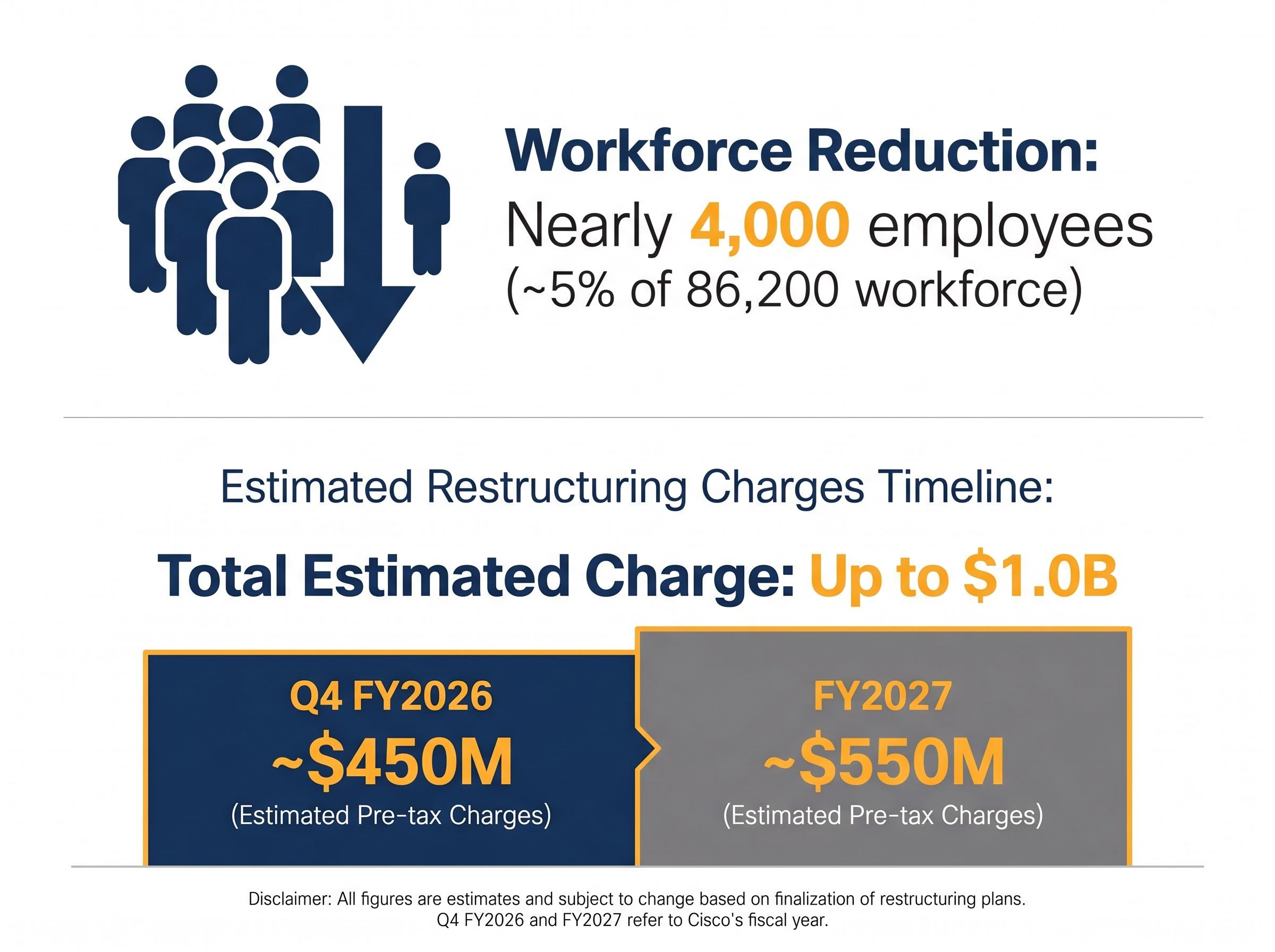

The numbers, stated plainly: Cisco is cutting nearly 4,000 employees, approximately 5% of its roughly 86,200-person workforce as of July 2025. Notifications began on 14 May 2026, with a company-wide meeting scheduled for 21 May 2026.

Approximately 5% of Cisco’s global workforce is being eliminated alongside a quarter of 12% revenue growth.

The total pre-tax restructuring charge is estimated at up to $1.0 billion. The timing of those charges matters for investors tracking reported earnings:

| Period | Estimated Charge |

|---|---|

| Q4 FY2026 | ~$450M |

| FY2027 | ~$550M |

| Total | Up to $1.0B |

The structural logic is straightforward. When a company shifts its revenue mix toward higher-margin AI infrastructure work, the skills and roles that supported legacy product lines no longer match what the business needs. Revenue grows in the new category while headcount shrinks in the old one. Both things are true simultaneously.

Affected employees are reported to receive severance packages that include:

For investors, the separation is clear: the $1.0 billion charge will affect reported GAAP results through FY2027, but it is a discrete restructuring cost. The demand signal driving the guidance raise is a separate and more durable variable.

Pull the lens back and Cisco’s announcement fits a pattern that has been building across 2026.

Year-to-date through mid-May 2026, approximately 135,724 tech sector jobs have been cut across 308 events, per TrueUp tracking.

Several of the largest technology companies have executed similar restructurings, each with its own AI-prioritisation framing:

Cisco was among the top percentage gainers in U.S. markets on 14 May 2026. The broader market context was receptive: the Nasdaq Composite closed at 26,402.34, up approximately 1.20%, while the S&P 500 reached 7,444.25, up approximately 0.58%. AI-linked technology names were leading the advance.

Whether Cisco’s restructuring represents a lagging response to a trend already priced into peers, or a timely repositioning the market is rewarding with a premium, is the question the stock price will answer over the coming quarters.

For investors wanting to understand how the 14 May 2026 session played out across the full hardware stack, our dedicated guide to AI infrastructure stocks on that date covers the Nvidia H200 China clearance that amplified Cisco’s gains, the sympathy moves in Arista, Super Micro, Marvell, and Broadcom, and the regulatory risks that could unwind the Nvidia side of the rally before first shipments arrive.

A 16.5% single-session move on a combination of layoffs and guidance upgrades reveals how the market is currently pricing AI infrastructure exposure in mid-2026. The market read the restructuring not as distress but as allocation, the redeployment of resources from lower-margin legacy lines toward the demand that drove a $1.1 billion-to-$1.8 billion guidance raise.

Three forward-looking variables will determine whether that pricing holds:

The macro overlay: CME FedWatch data as of 14 May 2026 showed a market-implied probability above 28% for a 25-basis-point rate hike by year-end 2026, up from 20.7% one week prior.

The CME FedWatch tool tracks market-implied probabilities for Federal Reserve rate decisions across upcoming FOMC meetings, giving investors a real-time read on how bond markets are pricing monetary policy risk into equity valuations.

The U.S. 10-year Treasury yield stood at 4.455% on 14 May 2026. Enterprise IT budgets are sensitive to borrowing costs, and a tightening rate environment could pressure the very capital expenditure cycle that is fuelling Cisco’s demand story.

The core tension this story resolves is that guidance upgrades and workforce reductions are not contradictory in a business undergoing genuine mix-shift. They are predictable co-occurrences when a company sheds lower-margin legacy exposure and scales higher-margin AI infrastructure work. Cisco’s 14 May 2026 announcement is a case study in reading those combined signals as evidence of where management is placing its bets.

The legacy software repricing underway across the sector provides the broader backdrop for why Cisco’s mix-shift away from traditional enterprise networking lines is strategically rational: AI is actively migrating enterprise value from headcount-dependent platforms toward infrastructure-layer businesses, with $2 trillion in U.S. software market capitalisation eroding from per-user licensing models in the first months of 2026.

Updated FY2026 guidance: $62.8 billion to $63.0 billion, the benchmark the market will hold management against.

The forward watchpoints remain specific. Q4 FY2026 results will show whether order momentum sustained. The approximately $450 million in restructuring charges recognised this quarter and the remaining $550 million flowing into FY2027 will create noise in reported earnings that investors will need to separate from operating performance. And the 12% year-on-year revenue growth that anchored Q3 sets the baseline trajectory.

For investors evaluating enterprise technology companies more broadly, the pattern is reusable: when a company raises forward guidance and cuts headcount simultaneously, the question is not whether the two are contradictory. The question is whether the demand signal is durable enough to justify the cost of reshaping the business to meet it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Cisco shares surged 16.5% after the company reported Q3 FY2026 revenue of $15.8 billion (up 12% year-on-year) and raised its full-year FY2026 revenue guidance by approximately $1.1 billion to $1.8 billion, driven by surging hyperscaler AI infrastructure orders including $2.1 billion in AI orders during Q3 alone.

Cisco is cutting nearly 4,000 employees (roughly 5% of its workforce) to reallocate resources away from legacy enterprise networking lines and toward higher-margin AI infrastructure products such as custom silicon, high-speed optics, and AI-focused security; the restructuring reflects a deliberate mix-shift rather than financial distress.

Cisco raised its full-year FY2026 revenue guidance from a prior range of $61.2 billion to $61.7 billion to an updated range of $62.8 billion to $63.0 billion, representing an upgrade of approximately $1.1 billion to $1.8 billion depending on where within the ranges the comparison is drawn.

Cisco estimates a total pre-tax restructuring charge of up to $1.0 billion, with approximately $450 million expected in Q4 FY2026 and the remaining approximately $550 million flowing into FY2027, which will create noise in reported GAAP earnings that investors will need to separate from underlying operating performance.

Hyperscale cloud operators building large-scale AI training and inference facilities require high-performance networking fabric, custom silicon, optical interconnects, and security layers to connect thousands of AI processors; Cisco supplies these products, and with combined hyperscaler AI capital expenditure approaching $725 billion for full-year 2026, that spending base is the direct demand pool behind Cisco's guidance revision.