Deutsche Bank Warns Oil Could Hit $150 on Hormuz Closure

9 hrs ago

Broadcom just posted its strongest AI revenue quarter on record, grew AI chip sales 143% year-over-year to $10.8 billion, beat on both revenue and earnings per share, and guided fiscal Q3 total revenue above consensus. The stock fell more than 13% in premarket trading on 4 June 2026. The paradox is real, but it has a precise explanation: the selloff was not triggered by what management reported but by what it declined to do. Broadcom held its fiscal year 2027 AI revenue target at $100 billion rather than raising it, and guided Q3 AI chip revenue below the most optimistic analyst projections. What follows is a breakdown of the gap between the headline results and the market reaction, what management said about the $100 billion target, and why Bernstein and BofA Securities independently raised their price targets anyway.

The selloff looks irrational on the surface. A 143% AI revenue growth rate, a revenue beat, and an earnings beat do not typically produce double-digit declines. The reaction makes sense only when narrowed to three specific disappointments.

Broadcom shares fell more than 13% in premarket trading on 4 June 2026, despite reporting record AI semiconductor revenue.

The first and largest trigger was Q3 AI chip revenue guidance. Management guided $16 billion for the current quarter; analysts had projected $17.2 billion. That $1.2 billion gap between guidance and expectation carried the weight of a market that had priced in acceleration, not steadiness.

The second trigger was the decision to leave the FY2027 AI revenue target at $100 billion unchanged. Investors had widely anticipated an upward revision following consecutive quarters of above-guidance AI results. That revision did not come.

The three selloff triggers, in summary:

Each of these is a forward-expectations issue. None reflects a deterioration in trailing performance.

The selloff was not limited to Broadcom: CrowdStrike and Palo Alto Networks also declined after reporting positive results on the same evening, a pattern consistent with a sector-wide positioning unwind rather than a verdict on any individual company’s fundamentals.

The actual fiscal Q2 results tell a different story from the one the share price is telling.

Revenue came in at $22.2 billion, up approximately 48% year-over-year, marginally above the Wall Street consensus of $22.1 billion. Adjusted earnings per share of $2.44 exceeded the consensus range of $2.39-$2.40. AI semiconductor revenue of $10.8 billion surpassed Broadcom’s own prior guidance of approximately $10.7 billion.

The forward picture was similarly constructive. Q3 total revenue guidance of approximately $29.4 billion exceeded the consensus forecast of $28.6 billion, representing approximately 84% year-over-year growth.

| Metric | Actual | Consensus |

|---|---|---|

| Q2 Revenue | $22.2B | $22.1B |

| Q2 Adjusted EPS | $2.44 | $2.39-$2.40 |

| Q2 AI Semiconductor Revenue | $10.8B (up 143% YoY) | ~$10.7B (company guidance) |

| Q3 Revenue Guidance | $29.4B | $28.6B |

The table makes the picture plain. Broadcom beat or matched every trailing metric and guided total revenue above expectations. The selloff is entirely about forward AI-specific expectations, not about what the company delivered in Q2. That distinction matters for anyone evaluating whether the drop represents a buying signal or a warning.

The FY2027 $100 billion AI revenue target is not quarterly guidance. It is a longer-horizon management forecast covering Broadcom’s custom AI accelerator and networking chip business across the full fiscal year ending in late 2027. It represents management’s view of where the sum of hyperscaler custom chip programmes and AI networking revenue will land over a multi-year ramp.

Broadcom occupies a distinct and non-interchangeable layer of the AI semiconductor supply chain, sitting between the hyperscalers that commission custom chip designs and the foundries such as TSMC that manufacture them, a structural position that underpins the multi-year revenue visibility management cited on the earnings call.

On the 3 June earnings call, CEO Hock Tan characterised hyperscaler demand as insatiable and highlighted continued momentum in custom chip programmes. The decision to hold the target flat was attributed not to weakening demand but to supply constraints at customer sites, a logistics limitation rather than a commercial one.

Broadcom’s AI revenue has shown quarter-to-quarter fluctuation in prior periods, and management’s conservative posture on near-term guidance has been a recurring pattern. The company beat its own Q2 AI guidance by approximately $100 million, suggesting the conservative approach has consistently produced results at or above the stated outlook.

Both management and analysts drew a clear line between demand-driven caution and logistics-driven caution. The supply constraints cited are at customer sites, not within Broadcom’s own fabrication or design pipeline.

BofA Securities analyst Vivek Arya noted that Broadcom’s customer visibility now reportedly extends to 2028, encompassing Anthropic, Meta, and OpenAI. An unchanged target paired with expanding customer relationships through 2028 can be read as a floor rather than a ceiling. The constraint is on how fast customers can absorb chips, not on whether they want them.

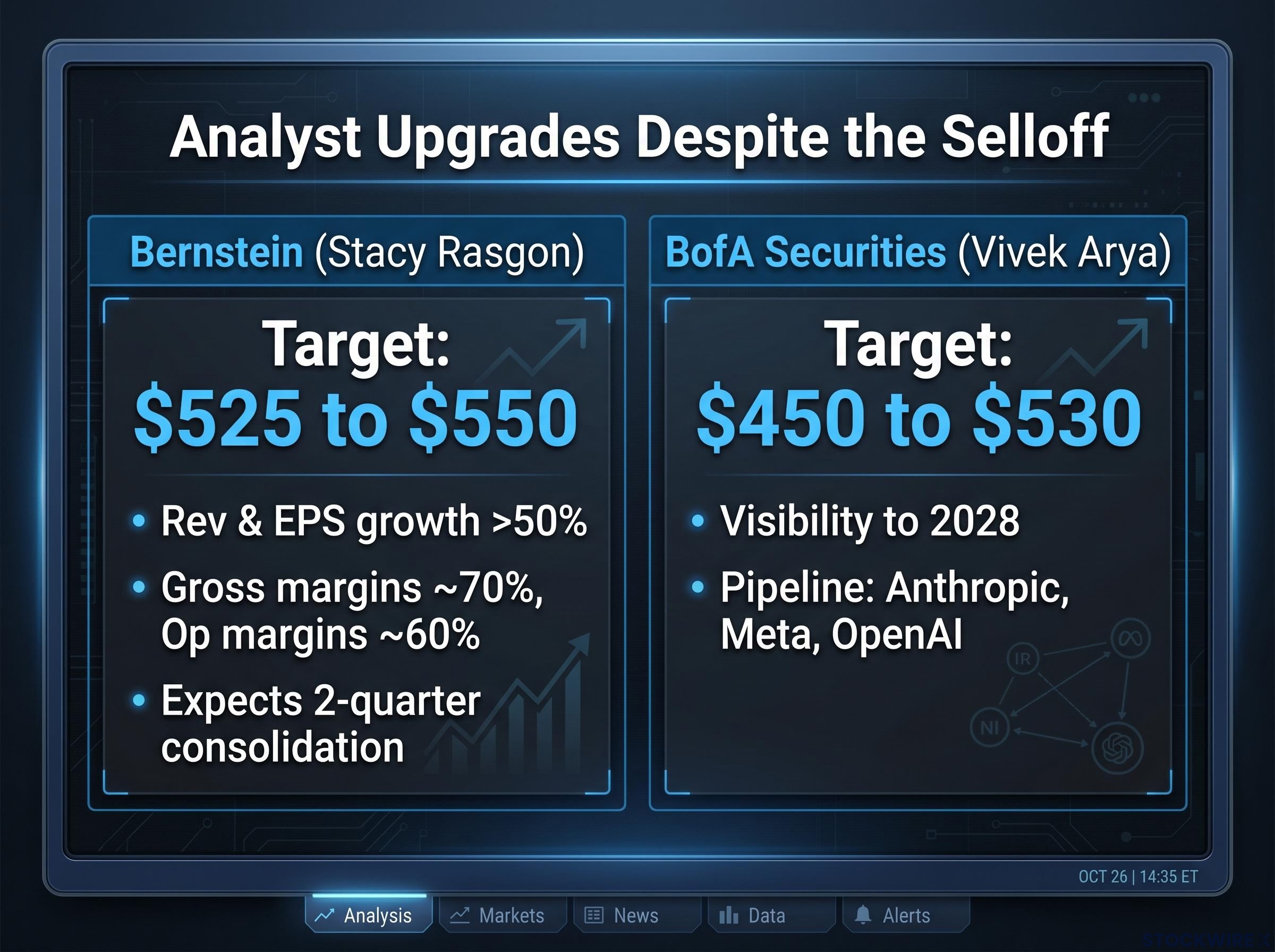

Two of the most closely followed semiconductor analysts responded to the earnings report by raising their price targets on a stock that had just fallen 13%. Their reasoning overlaps on one point and diverges on timing.

Bernstein analyst Stacy Rasgon raised his price target to $550 from $525. His thesis centres on consolidation: Broadcom shares may trade sideways for approximately two quarters before the investment case strengthens heading into 2027. His view is that the underlying business continues to compound at a rate that will reassert itself once forward expectations recalibrate.

BofA Securities analyst Vivek Arya raised his price target to $530 from $450, a more substantial revision. His near-term view is more constructive, anchored to the expanding customer pipeline through 2028 and the addition of Anthropic, Meta, and OpenAI to the design-win funnel.

Broadcom’s margin profile, with gross margins in the 70% range and operating margins in the 60% range, remains among the strongest in the semiconductor industry, according to Bernstein analysis.

The shared conclusion is significant: both analysts independently interpreted the unchanged $100 billion target as management caution tied to supply logistics at customer sites, not a sign of deteriorating demand. Where they disagree is on timing. Rasgon sees a pause; Arya sees the pipeline already doing the work.

Among the six structural risks that semiconductor analysts are monitoring across the AI accelerator market, custom silicon displacement represents the most direct threat to Broadcom’s competitive position, given that Broadcom’s own hyperscaler relationships are deepening at the same time that those hyperscalers are funding in-house chip development programmes.

The gap between the current run-rate and the $100 billion target is the question that will define Broadcom’s stock trajectory over the next 18 months. Q3 guidance of $16 billion in AI chip revenue implies an annualised run-rate approaching $64 billion. Reaching $100 billion in FY2027 requires continued acceleration from that base.

The key milestones and conditions tied to the $100 billion path, in sequence:

The gross margin compression anticipated in Q3, approximately 300 basis points, reflects scaling custom accelerator volumes. Higher volumes of custom chips carry lower margins than Broadcom’s networking products, but they represent programme ramps that feed the revenue acceleration path. This is a sign of scaling, not pricing pressure.

Bernstein’s consolidation view positions the next two quarters as a period where the stock digests the gap between expectations and guidance. The investment case, in Rasgon’s framing, strengthens heading into 2027 as the revenue trajectory narrows toward the target.

The BofA Securities assessment that customer visibility extends to 2028, with Anthropic, Meta, and OpenAI cited as pipeline additions, signals design-win momentum that extends beyond the FY2027 target window. Custom AI accelerator programmes typically involve multi-year design cycles, which means these relationships represent forward commitment from hyperscalers to Broadcom’s chip architecture.

This is pipeline visibility, not confirmed revenue. It serves as an indicator of Broadcom’s competitive position in custom silicon rather than a guaranteed revenue figure. For investors looking past the near-term noise, the durability of these design relationships is arguably more instructive than any single quarter’s guidance.

For readers wanting to situate Broadcom’s FY2028 pipeline visibility within the broader hardware cycle, our full explainer on AI infrastructure demand peak examines Morningstar’s projection that new hardware absorption rates will decelerate around 2028, and what that timeline means for entry timing and position sizing across the AI hardware complex.

Broadcom’s Q2 results were strong by every trailing measure. Revenue, earnings per share, and AI semiconductor revenue all exceeded expectations. The selloff was a forward-expectations reset, a recalibration of when the $100 billion target might be raised and how fast Q3 AI chip revenue would accelerate.

Two analysts from different firms independently raised their price targets. Both read the unchanged $100 billion target as conservative posture tied to supply logistics, not demand deterioration. The question that will resolve the investment debate is specific: whether the Q3 AI chip revenue guidance of $16 billion proves to be a floor or a ceiling when results are reported.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Broadcom stock dropped more than 13% in premarket trading on 4 June 2026 because management guided Q3 AI chip revenue at $16 billion versus analyst projections of $17.2 billion, held the FY2027 $100 billion AI revenue target unchanged, and flagged gross margin compression of approximately 300 basis points for Q3.

Broadcom's $100 billion AI revenue target is a longer-horizon management forecast for the full fiscal year ending in late 2027, covering revenue from custom AI accelerator chip programmes and AI networking products sold to hyperscaler customers.

Bernstein raised its target to $550 and BofA raised its target to $530, with both firms interpreting the unchanged $100 billion forecast as conservative posture tied to supply constraints at customer sites rather than weakening demand, and both citing strong margin profiles and expanding customer pipelines.

Q3 guidance of $16 billion implies an annualised AI chip revenue run-rate approaching $64 billion, meaning Broadcom would need continued acceleration from that base to reach the $100 billion FY2027 target.

According to BofA Securities analyst Vivek Arya, Broadcom's customer visibility reportedly extends to 2028 and includes Anthropic, Meta, and OpenAI as pipeline additions alongside existing hyperscaler relationships.