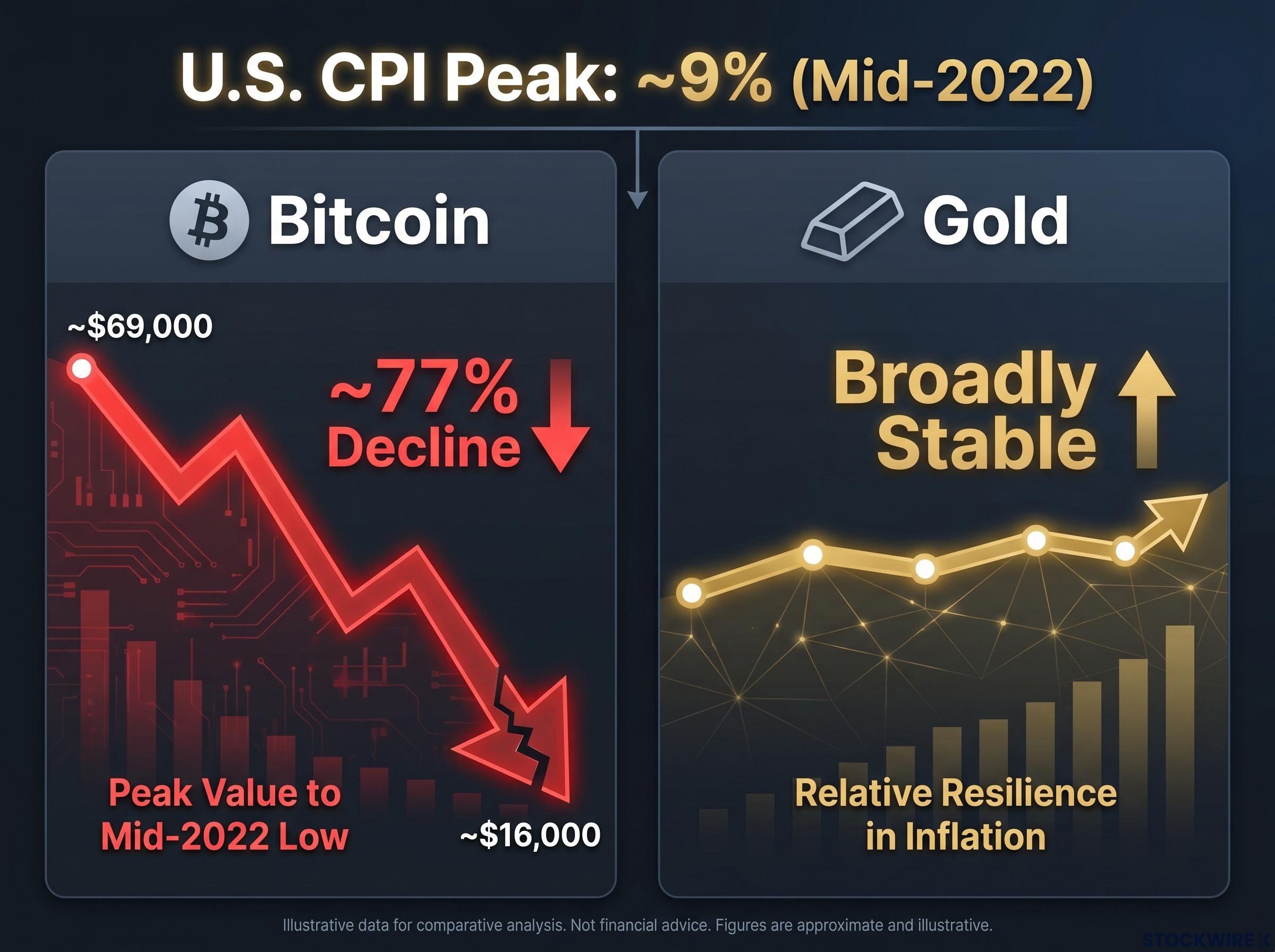

In 2022, when U.S. inflation reached approximately 9%, investors holding Bitcoin as an inflation hedge watched the asset lose roughly 77% of its value. Gold, over the same period, held broadly stable. One asset performed as advertised. The other did the opposite of what its narrative promised.

That episode remains the most significant real-world test of the “digital gold” thesis, and the results were unambiguous. Gold has since set all-time highs above $5,500 per ounce in early 2026, while Bitcoin continues to trade with equity-like volatility and drawdown severity. Retail interest in both assets as inflation protection remains high, and the narrative that Bitcoin functions as a store of value persists in financial media despite the empirical record.

What follows puts the inflation-hedging credentials of both assets under a data lens, establishes what structural characteristics actually qualify an asset as a hedge, and provides a framework for how each should be positioned in a portfolio and why.

The 2022 inflation test and what it revealed about both assets

The 2022 inflationary spike was not a minor stress episode. U.S. CPI reached levels not seen in four decades, and both gold and Bitcoin were simultaneously marketed to retail investors as inflation protection. The test ran. The results were measurable.

The three data points that matter:

- U.S. CPI peaked at approximately 9% in mid-2022, the highest reading since the early 1980s

- Bitcoin fell from roughly $69,000 to approximately $16,000, a drawdown of approximately 77%

- Gold remained broadly stable throughout the same period, delivering modestly positive returns

Bitcoin lost approximately 77% of its value during the precise period it was supposed to protect investors from inflation. The asset did not merely underperform; it moved in the opposite direction of its marketed purpose.

Bitcoin’s subsequent 2025 decline from approximately $126,000 to around $80,000, within what was otherwise a bull cycle, reinforced the pattern. Volatility of this magnitude is not a feature of a hedging instrument. It is the defining characteristic of a speculative asset.

The 2022 episode is not an anomaly to be explained away by citing leverage unwinds or exchange failures. It is the test case, the one period where inflation-hedge credentials were measurable in real time, and the results speak clearly enough to anchor the rest of this analysis.

The 2022 episode is one instance in a pattern: safe haven asset failures during supply-shock crises expose how narrowly these instruments were designed, protecting against financial demand collapses rather than commodity chokepoints or energy-price-driven inflation.

When big ASX news breaks, our subscribers know first

What actually makes an asset a legitimate inflation hedge

Much of the retail discussion around inflation hedging conflates two different things: an asset that tends to rise over time and an asset that protects purchasing power precisely when protection is most needed. These are not the same property.

A legitimate inflation hedge must meet three structural requirements, in order of importance:

- It must retain or gain value when inflation is rising and markets are under stress, not merely during periods of moderate price growth

- It must exhibit low or negative correlation with equities during drawdown periods, so that it counterbalances portfolio losses rather than amplifying them

- It must demonstrate this behaviour repeatedly across multiple stress episodes, not just during favourable windows

The World Gold Council and State Street Global Advisors are consistent on a point that often gets lost in retail commentary: gold’s short-term correlation with headline CPI is weak. Gold does not mechanically rise when a monthly inflation print comes in hot. Its inflation-hedge property operates over longer horizons and is driven by real yields, monetary dynamics, and geopolitical risk rather than nominal CPI readings.

The equity-correlation test: why it matters more than CPI tracking

An asset that adds to portfolio drawdowns during equity bear markets fails the hedge test regardless of its long-term return profile. This is where the structural distinction between gold and Bitcoin becomes sharpest.

Gold’s correlation with equities during stress periods is near zero or negative. It tends to hold value or appreciate when equity portfolios are losing ground, which is the precise behaviour required of a hedge.

Bitcoin’s correlation with the NASDAQ has remained elevated since 2020, with rolling 30-day measures often in the 0.0-0.6 range and strong positive linkage during risk-off episodes. In practice, this means a Bitcoin allocation amplifies existing equity exposure rather than counterbalancing it. Adding Bitcoin to a portfolio that already holds equities increases drawdown severity during bear markets, the exact opposite of what a hedging asset should do.

Gold’s hedging credentials in historical context

Gold’s hedging record is genuine, but it comes with limitations that are worth stating plainly. The most striking illustration of those limitations involves time.

An investor who purchased gold at its January 1980 peak of $850 per ounce waited approximately 45 years in inflation-adjusted terms to recover their purchase price, breaking even around September 2025.

That is not an argument against gold. It is an argument for understanding what gold is: a wealth preservation tool, not a wealth creation vehicle.

From 1971 through 2024, gold delivered annualised returns of approximately 7.9%. Over the same period, the S&P 500 returned roughly 10.7% annually. The gap of nearly 3% per year, compounded over half a century, translates into approximately four times less terminal wealth for gold relative to equities.

| Metric | Gold | S&P 500 |

|---|---|---|

| Annualised return (1971-2024) | ~7.9% | ~10.7% |

| Institutional classification | Store of value / hedge | Growth / total return |

| Equity correlation during stress | Near zero or negative | N/A (is the equity benchmark) |

| Terminal wealth outcome (illustrative, 50 years) | ~4x less than equities | Baseline |

Where gold’s structural credentials hold is in institutional demand and its behaviour during periods of monetary stress. Central bank net purchases totalled 863 tonnes in 2025, with Q1 2026 adding 244 tonnes net (up 3% year-over-year). Poland (31 tonnes) and China (8 tonnes) were among the leading buyers. This sovereign-level accumulation, aimed at reducing dollar exposure over decades, confirms gold’s institutional role as a reserve asset.

The relationship between sovereign debt and gold allocation has shifted materially since 2022: as the BIS documented the stock-bond correlation breakdown, institutions including BlackRock, JPMorgan, and Swiss pension funds responded by increasing gold allocations, effectively replacing bonds as the primary portfolio diversifier.

Gold set all-time highs above $5,500 in early 2026 and traded around $4,330 per ounce as of early June 2026. J.P. Morgan’s commodities team has outlined expectations pushing toward $5,000 per ounce by the end of 2026, with upside scenarios reaching $6,000 or higher. The structural bull case rests on central bank buying, real-rate dynamics, and geopolitical uncertainty rather than short-term CPI tracking.

Bitcoin’s decade of returns versus its moment of reckoning

Bitcoin’s total return over the past decade ranks among the highest of any asset class. That record deserves acknowledgement before the hedge assessment is completed, because the two are often conflated and they should not be.

Over a ten-year window, Bitcoin outperformed most conventional asset classes on a total return basis. Investors who bought and held through the volatility captured returns that equities, gold, and fixed income could not match. That is the growth case, and on its own terms it is strong.

The drawdown record tells a different story:

- Post-2017 rally: Bitcoin lost more than 80% of its value

- 2022 inflation episode: approximately 77% decline, from roughly $69,000 to around $16,000

- 2025 bull-cycle correction: decline from approximately $126,000 to around $80,000

Charles Schwab data indicates Bitcoin’s three-year maximum drawdown remains at 50% or greater. Analyses from the Bank for International Settlements (BIS), the International Monetary Fund (IMF), and central bank working papers classify Bitcoin as a speculative risk asset rather than a hedge, a framing that has held through 2025-2026 updates without meaningful reversal.

The BIS classification of Bitcoin as a speculative asset, published in June 2025, states explicitly that unbacked cryptoassets have established themselves through large price gyrations as speculative instruments rather than stable monetary tools, providing the most current authoritative framing of where Bitcoin sits in the asset taxonomy.

Why strong total returns do not validate the hedge narrative

An asset can generate exceptional returns in a bull cycle while failing as a hedge precisely when hedging is needed. These are separate properties.

Bitcoin’s elevated correlation with equities means its gains and losses tend to occur in the same risk environment as equity gains and losses. During the periods when a portfolio most needs protection, when equities are falling and inflation is eroding purchasing power, Bitcoin has historically fallen alongside them. The decade-long total return does not address this structural shortcoming, because the hedging question is not about average returns. It is about behaviour during stress.

What the structural comparison shows side by side

The evidence assembled across previous sections resolves into a structural comparison that shifts the question from “which asset is better” to a more useful one: these assets serve entirely different portfolio functions.

| Characteristic | Gold | Bitcoin |

|---|---|---|

| Equity correlation during stress | Near zero or negative | Elevated (positive), often 0.0-0.6 on rolling measures |

| 2022 inflation episode behaviour | Broadly stable | -77% drawdown |

| Central bank adoption | 863 tonnes (2025); 244 tonnes net (Q1 2026) | None at central bank level |

| Institutional classification | Store of value / hedge | Speculative risk asset |

| Long-term annualised return (1971-2024) | ~7.9% | N/A (asset too new for comparable data) |

| Appropriate portfolio role | Wealth preservation / inflation hedge | Speculative growth exposure |

Central bank accumulation reinforces the distinction. Sovereign reserve managers buy gold to reduce dollar exposure and stabilise reserves across decades. No central bank holds Bitcoin in its reserves. This is not a retail preference; it reflects an institutional consensus about which asset qualifies as a reserve instrument and which does not.

A portfolio that holds both gold and Bitcoin is not doubling its inflation protection. It is combining a hedge with a growth speculation, and those two positions require different sizing, risk budgets, and time horizons.

The case for separating inflation-hedge and growth allocations also connects to a broader shift in institutional portfolio design: portfolio resilience beyond 60/40 now depends on diversifying across economic environments rather than across asset-class labels, a distinction Bridgewater Co-CIO Bob Prince has argued is more durable than any fixed weighting scheme.

J.P. Morgan’s price target of $5,000 per ounce by end of 2026 (with upside scenarios to $6,000 or higher) reflects the structural demand picture: central bank buying, geopolitical uncertainty, and real-rate dynamics underpinning continued institutional interest. Bitcoin’s price trajectory, by contrast, remains tied to risk sentiment and speculative capital flows.

The evidence has run, and the portfolio implications are clear

The analytical verdict rests on the 2022 test case more than any other data point. Gold held value during the most significant inflationary episode in four decades. Bitcoin lost approximately 77% of its value during the same period. Institutional consensus from the BIS, the IMF, and major asset managers classifies gold as a store of value and hedge; Bitcoin as a speculative risk asset. Central banks accumulate the former and hold none of the latter.

Three portfolio decision principles follow from this evidence:

- Identify the objective first. An inflation-protection allocation and a speculative growth allocation solve different problems and should be evaluated against different benchmarks.

- Match the asset to the objective. If the goal is inflation protection, gold has the structural credentials supported by decades of data and institutional consensus. If the goal is speculative growth exposure, Bitcoin may earn a position, but on growth terms, not hedging terms.

- Size each position according to its actual risk profile. Gold’s 45-year recovery from its 1980 peak is a reminder that even a legitimate hedge can be misused through poor timing and over-allocation. Bitcoin’s three-year maximum drawdown of 50% or greater demands position sizing consistent with its volatility.

Holding Bitcoin as if it were a hedge misunderstands the position and may lead to under-allocation to the assets that actually perform the hedging function. The data has been clear on this point since 2022. The question for investors is whether their portfolios reflect what the evidence shows.

Investors wanting to operationalise the inflation-hedge and growth-exposure distinction across a full portfolio construction will find our comprehensive walkthrough of the All Weather Portfolio framework, which examines the four-quadrant risk-balancing approach, the ALLW ETF launched in March 2025, and where modern practitioners are adjusting the original weights to reflect structurally higher real yields.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions and various risk factors.