UBS projects global equities could gain a further 10% by mid-2027, a forecast that cuts against the growing view among market participants that the current bull run is approaching its limits. The firm’s chief investment officer published the forecast today, 17 July 2026, and it comes with specific earnings targets, regional upgrades, and a reframing of where the AI trade goes next.

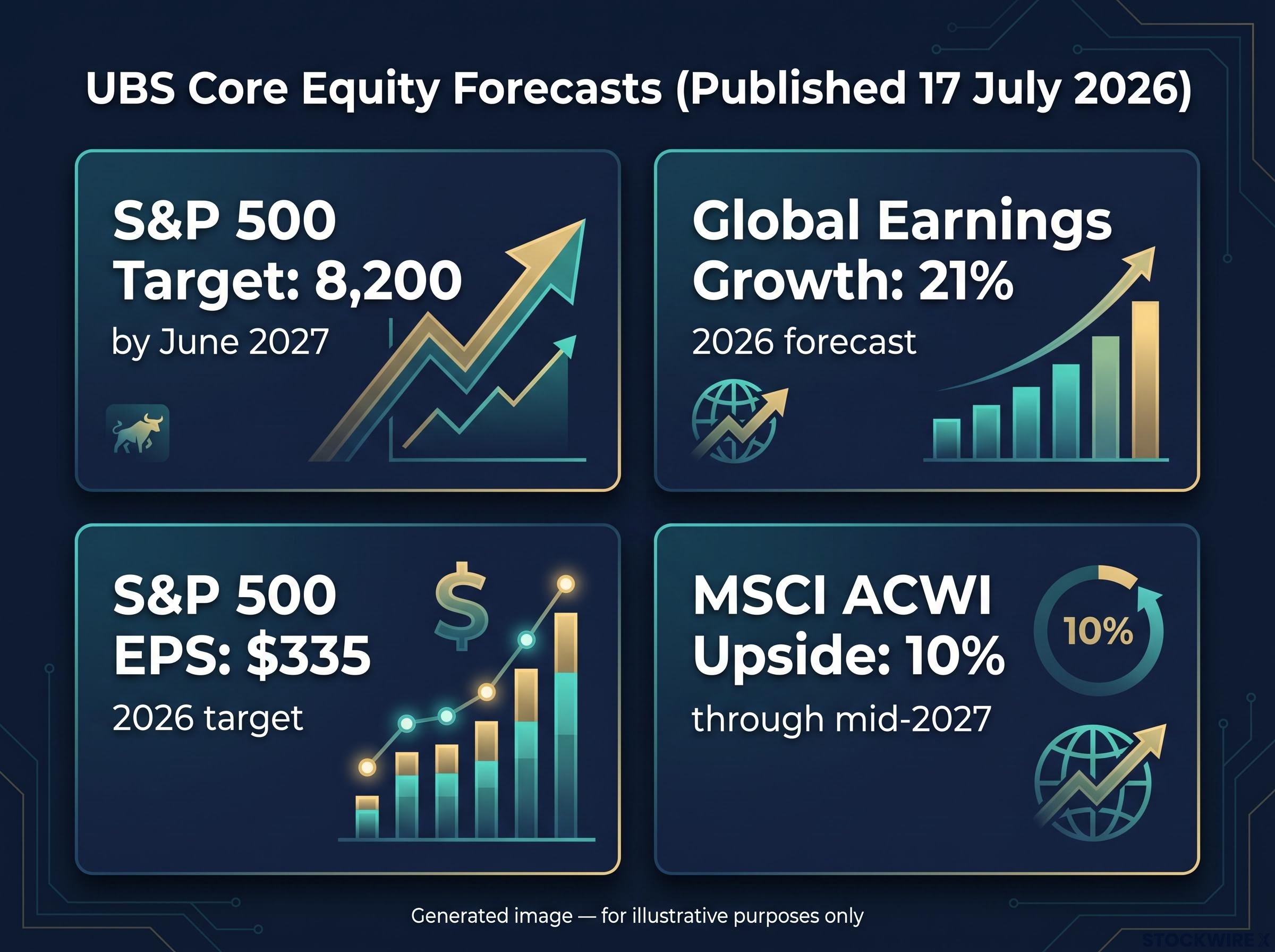

This is not a vague directional lean. UBS is putting a named destination on the rally, backed by a 21% global earnings growth forecast for 2026 and an S&P 500 target of 8,200 by June 2027. The institutional view has shifted: the next leg is no longer a concentrated U.S. tech story.

Here is what the specific UBS calls mean for how you are positioned: the earnings mechanism behind the forecast, the regions and sectors being upgraded, the AI rotation the firm is flagging, and the four fault lines that could change everything.

Why UBS thinks global equities have 10% further to run by mid-2027

The target represents a 10% gain for global equities as measured by the MSCI All Country World Index (MSCI ACWI), an index tracking equity markets across both developed and emerging economies. UBS CIO Mark Haefele published the call today, and the firm’s June 2026 House View maintains an Attractive stance on global equities.

The MSCI ACWI index factsheet confirms that U.S. mega-cap technology names including NVIDIA, Apple, and Microsoft sit among the top ten constituents, illustrating precisely the concentration dynamic UBS is flagging as a risk for passive global equity holders.

The core forecasts:

- 10% projected upside for MSCI ACWI through mid-2027

- 21% global earnings growth forecast for 2026

- S&P 500 earnings per share target: $335 for 2026

- S&P 500 index target: 8,200 by June 2027

UBS described first-quarter 2026 S&P 500 earnings growth as the strongest recorded in four years, characterising the current rally as justified by genuine profit expansion rather than speculative excess.

Q1 2026 earnings delivered a blended S&P 500 growth rate of 27.1%, nearly double pre-season estimates, with 84% of companies beating EPS forecasts, providing the empirical foundation for UBS’s characterisation of the current rally as driven by genuine profit expansion rather than speculative multiple expansion.

The 21% earnings growth figure is the load-bearing number in this thesis. It tells you UBS is betting on corporate profit delivery, not sentiment or multiple expansion (which is when share prices rise purely because investors are willing to pay more per dollar of earnings, not because earnings themselves are growing). The call lives or dies on whether companies actually produce the numbers. If they do, the upside case holds. If they don’t, the index target is just a number on a page.

When big ASX news breaks, our subscribers know first

What “broadening” actually means, and why it matters for your portfolio

For most of 2023 through mid-2025, global equity returns were dominated by a handful of U.S. mega-cap technology names. AI hype, post-pandemic digital acceleration, and enormous capital flows into a small group of companies meant a cap-weighted global index fund was, in practice, a concentrated bet on five or six stocks.

That is what UBS says is changing. A broadening rally means profits are driving returns from a wider set of companies and geographies. Instead of a single dominant return driver, the earnings contributions are spreading across sectors and regions.

Index concentration in U.S. equities has reached levels with no modern historical precedent, with five mega-cap companies controlling roughly 30% of total market capitalisation, a structural condition that makes the broadening thesis materially more consequential for passive investors than it might initially appear.

UBS expects returns across major markets, the U.S., Europe, Japan, China, and emerging markets, to be “very similar” through the end of 2026. The contrast with what came before is stark:

- Before: Returns concentrated in U.S. mega-cap tech; a handful of names drove most of the index gains

- Now: Earnings growth dispersing across regions and sectors; leadership rotating away from a single theme

Why this matters for concentration risk

If major market returns are converging, a cap-weighted fund still heavily skewed toward U.S. mega-cap tech is carrying concentration risk without a corresponding return advantage. You are taking on the downside exposure of a concentrated portfolio without the upside premium that justified it when those names were the only game in town. Understanding this shift is what makes the regional and sector calls that follow make sense as a coherent portfolio response, not isolated recommendations.

Europe and Asia upgraded: the regional rotation UBS is betting on

The broadening thesis has a specific geographic expression. European equities received an upgrade to Attractive from UBS, on the back of improving cyclical dynamics, a more supportive structural environment, and valuations that remain only modestly above their 10-year averages. The firm continues to hold a favourable view on U.S. and Asian equities alongside this.

The earnings recovery angle is where the European call gets interesting. UBS projects approximately 7% profit growth for European equities in 2026, potentially accelerating to 18% in 2027, according to the firm’s projections (these figures have not been independently confirmed). After several years of earnings stagnation, that kind of acceleration represents a multi-year catch-up trade, and UBS is positioning it as a structural opportunity rather than a short-term tactical call.

The institutional underweight in European equities is a structural positioning gap confirmed by the June 2026 BofA Global Fund Manager Survey, with Barclays formally upgrading the region on 3 July and Germany’s fiscal expansion programme creating a forward order book for industrials and infrastructure names not captured in standard index allocations.

| Region | UBS Rating | Key Sectors Highlighted | Earnings Growth Forecast |

|---|---|---|---|

| U.S. | Attractive | AI enablers, software, financials | $335 S&P 500 EPS (2026) |

| Europe | Attractive (upgraded) | Industrials, banks, utilities | ~7% (2026), potentially 18% (2027) |

| Asia / Japan | Favourable | Technology, financials | Solid growth expected |

| Emerging Markets | Constructive | Broad exposure | Returns expected similar to developed markets |

Investors outside Europe often underweight the region by default. This table gives you the comparative view: UBS sees similar return potential across geographies, which means deliberate European and Asian exposure is a way to participate in the broadening rally without adding to U.S. mega-cap concentration.

The AI trade is not over, it is just moving

The instinct to equate AI exposure with semiconductor stocks or hyperscaler holdings is understandable. That was the trade for the first phase. According to UBS, the AI investment cycle is now in transition, with the set of companies likely to benefit continuing to evolve as the technology matures.

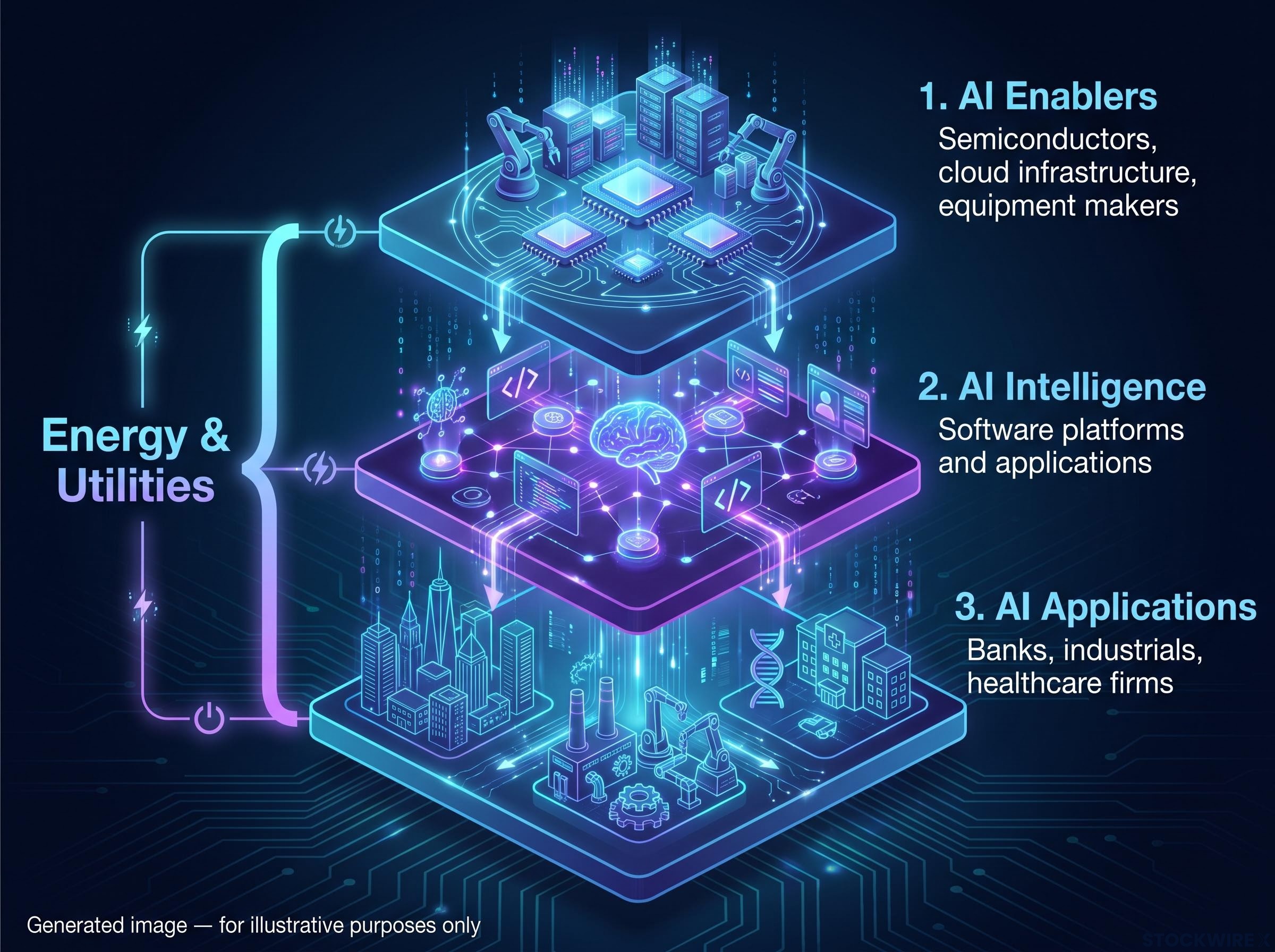

The firm describes three layers of AI exposure:

- AI enablers: semiconductors, cloud infrastructure, and equipment makers. This is the phase that has already delivered substantial returns.

- AI intelligence: software platforms and applications that process, deploy, and refine AI capabilities. This layer is beginning to attract capital.

- AI applications: real-economy companies, including banks, industrials, and healthcare firms, that are converting AI into measurable productivity and margin gains. This is where UBS sees the next wave of returns.

Energy and utilities sit alongside all three layers. Rising data-centre power demand is positioning them as structural beneficiaries, not as traditional defensive or commodity plays. UBS identifies AI, power and resources, and longevity as key structural growth themes over the coming 12 months.

Data from recent months supports the rotation thesis. Financials have posted stronger returns than technology, and healthcare has staged a recovery, both consistent with the pattern UBS has outlined. If your AI exposure consists entirely of semiconductor ETFs or hyperscaler holdings, you may already be positioned for the phase that is ending rather than the one beginning.

The next major ASX story will hit our subscribers first

Four risks that could break the thesis

UBS’s base case is constructive, but the firm is explicit about the fault lines that could alter it. Each of the four risk clusters has a specific mechanism and a monitoring signal.

- Inflation and rate-hike fears. A sustained rise in energy costs or stubborn inflationary pressure could upset the expectation of a supportive interest-rate environment. UBS cited the U.S.-Iran situation explicitly as a geopolitical factor that could feed into energy-driven inflation. Watch: inflation breakevens and rate futures for signs that central bank expectations are shifting toward tightening.

- AI monetisation shortfalls. Strong AI-related capital expenditure is currently a major earnings driver. If spending slows or fails to convert into revenue and profit, it undermines a significant portion of the 2026-2027 earnings thesis. Watch: AI capex guidance and monetisation disclosures in quarterly earnings calls.

- Geopolitical instability and energy shocks. Tensions involving major energy producers or key shipping routes remain a source of volatility. UBS pointed to the fragile and uncertain prospect of a lasting settlement between the U.S. and Iran as a specific risk to monitor. Watch: oil price movements, shipping-route disruptions, and diplomatic developments in the Middle East.

- Index concentration risk. The rapid rise of a handful of U.S. tech names has made broad global indices behave like single-theme bets. This risk is not hypothetical or distant; it is already embedded in most passive global equity portfolios today. Watch: the weight of the top 10 holdings in your main equity index funds and ETFs.

Concentration risk stands apart from the other three because you can act on it immediately. The other risks require waiting for external triggers. This one is already in your portfolio.

UBS has published a companion scenario analysis framework that assigns a 60% probability to the base case and maps the specific oil-price and geopolitical triggers that would activate the downside and upside tails, giving investors a structured way to stress-test the 8,200 target against the risks outlined above.

What the UBS call changes about how to be positioned right now

UBS’s mid-2027 outlook does not tell you to buy more equities. It tells you to buy different equities. The composition of winners is changing, and staying in the same positions that worked in 2024-2025 carries a different risk profile than it may appear.

Five questions to ask about your current portfolio:

- Assess concentration. How much of your equity exposure is effectively tied to a small set of U.S. tech names? If you hold cap-weighted global index funds, the answer may be higher than you expect.

- Rebalance across regions. Are you deliberately exposed to European industrials, banks, and utilities, or Asian technology and financials? UBS sees similar returns across geographies, which means underweighting non-U.S. markets is a concentration choice, not a neutral default.

- Refine AI sector exposure. Does your AI allocation extend beyond semiconductors and hyperscalers into energy, software applications, and real-economy adopters? UBS suggests allocating up to 30% of equity portfolios to AI, power and resources, and longevity themes (this figure has not been independently confirmed).

- Build a monitoring routine. Track inflation breakevens, AI capex disclosures, geopolitical developments, and the weight of your top holdings. These are the early-warning signals for the four risks above.

- Set your time horizon. UBS expects volatility and sector rotation within the uptrend. Longer-horizon investors can lean into the broadening rally; shorter-horizon investors should emphasise balanced sector exposure and liquidity.

The bull case is intact, according to UBS’s reading. What has changed is who wins within it. Portfolios built for the concentrated mega-cap phase of this cycle are not automatically positioned for the broadening phase that follows.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—