The Reserve Bank of Australia raised the cash rate to 4.10% on 17 March 2026, and digital trading platforms registered the impact within milliseconds. The contemporary investor reaction to economic news is no longer characterised by reading morning papers and gradually adjusting portfolios over weeks. Today, macroeconomic policy shifts trigger immediate, algorithmic recalibrations across Australian retail platforms.

The technological infrastructure supporting these platforms ensures that retail capital moves with unprecedented velocity. This analysis examines how everyday investors are currently navigating these abrupt portfolio adjustments in a high-speed digital trading environment.

By unpacking the mechanics of recent trading behaviours, market participants can better understand the forces driving modern volatility. The gap between institutional expectations and retail reality has widened substantially. Recognising how platforms process these events provides clarity for those attempting to manage wealth amid rapid domestic policy changes.

Quantifying the Shock of the March 2026 RBA Rate Hike

The 25 basis point rate increase delivered last month created immediate whiplash across Australian retail trading platforms. Historically, markets absorbed central bank decisions over several trading sessions. The current environment prices this external information almost instantaneously.

While major institutional reports from CommBank and Westpac IQ noted a broad increase in investor caution, retail platforms experienced hyper-specific engagement drops. While a 20% drop in trading engagement is rumored, quantitative metrics confirming it are unavailable following the borrowing cost increase. This swift withdrawal highlights how collective behavioural spasms now drive immediate market volatility.

This contraction contrasts sharply with historical retail buying frenzies seen in previous cycles. For context, platform data from April 2025 showed a transaction jump coinciding with American import duty declarations.

The sequential timeline of the March policy shift demonstrates this new acceleration:

- At 2:30 PM AEDT on 17 March 2026, the RBA announced the cash rate increase to 4.10%.

- Within seconds, automated risk-management triggers executed preliminary portfolio adjustments across major retail brokerages.

- By 3:00 PM AEDT, retail platform engagement metrics recorded the sharp contraction in active buy orders.

- Over the following 48 hours, CommBank and Westpac IQ analyses confirmed the broader systemic shift toward investor caution.

The official RBA monetary policy statement cited persistent capacity pressures and a rigid economic outlook as the primary catalysts for this tightening measure.

Understanding the severity of these aggregate adjustments helps individual investors normalise their own trading anxiety during major announcements. It reveals that rapid portfolio fluctuations are a feature of collective digital infrastructure rather than isolated market failures. The speed of the response fundamentally changes how capital operates in the Australian market.

When big ASX news breaks, our subscribers know first

Anatomy of a Digital Sell-Off and Hyper-Reactivity

The mechanics of an accelerated market fundamentally alter how macroeconomic pressure translates into portfolio changes. In a digital trading environment, the friction of traditional transaction delays is eliminated entirely. This lack of friction allows cost-of-living pressures and rising inflation to trigger immediate reductions in retail market participation.

When inflation metrics print higher than expected, retail participants do not wait for quarterly earnings reports to adjust their exposure. They liquidate positions instantly on their mobile devices. This foundational knowledge allows investors to separate the noise of a digital sell-off from actual systemic economic failure.

The Accelerated Market Shift Historical delayed market responses allowed for measured asset reallocation. Modern instantaneous pricing means retail portfolios absorb macroeconomic shocks in real-time, turning subtle policy shifts into immediate liquidity events.

Despite this obvious structural change, major institutional economic outlooks often omit retail hyper-sensitivity metrics. The KPMG Australia Economic Outlook Q1 2026 extensively discusses the impacts of RBA rate hikes but lacks specific analysis regarding everyday retail market movements.

Similarly, historical data from the Australasian Investor Relations Association in November 2024 outlined general retail participation trends without linking them directly to real-time macroeconomic sensitivity. This analytical omission leaves a gap in understanding how everyday investors actually drive intraday volatility. Recognising this gap explains why personal portfolio values can fluctuate wildly minutes after a central bank press release.

For retail participants attempting to neutralise their reactive trading impulses, our full explainer on dollar-cost averaging breaks down how automated periodic investments can mathematically smooth out average entry costs during major macroeconomic events.

Capital Flight and the Rotation Away From Defensive Assets

The underlying mechanics of high-speed trading ultimately manifest in tangible, and sometimes counterintuitive, asset rotations. The most prominent current trend is a measurable retail capital rotation out of traditional defensive positions and into expansionary assets.

Despite the prevailing caution surrounding RBA rate hikes, investors are exhibiting a softening appetite for physical wealth stores. These traditional safe havens previously peaked during periods of international political instability. According to an April 2026 market update from Global X ETFs Australia, retail capital is actively shifting away from gold and rotating into US equities.

Platform trading data shows that precious metal acquisition transactions have fallen as a percentage of overall platform volume. This capital flight highlights the paradox of investors seeking risk assets when domestic monetary policy tightens.

| Asset Class Preference | Late 2025 Volume Trend | Q1 2026 Volume Trend |

|---|---|---|

| Gold & Precious Metals | High acquisition frequency | Declining as a percentage of platform trades |

| US Equities | Moderate retail participation | Material capital rotation and inflow |

| Physical Retail Property | USD 6.5B total investment | Stabilising as an alternative wealth store |

In a distinct but related shift, investors previously sought alternative yields in physical retail property investment. This sector reached USD 6.5 billion (a 39% year-over-year increase) in 2025, driven heavily by private capital seeking tangible wealth stores. Tracking where this highly reactive money flows gives market participants a benchmark for their own asset allocation strategy.

Forward-looking CBRE commercial property investment research tracks this standout volume growth across physical asset classes, confirming that private capital is actively targeting alternative yields.

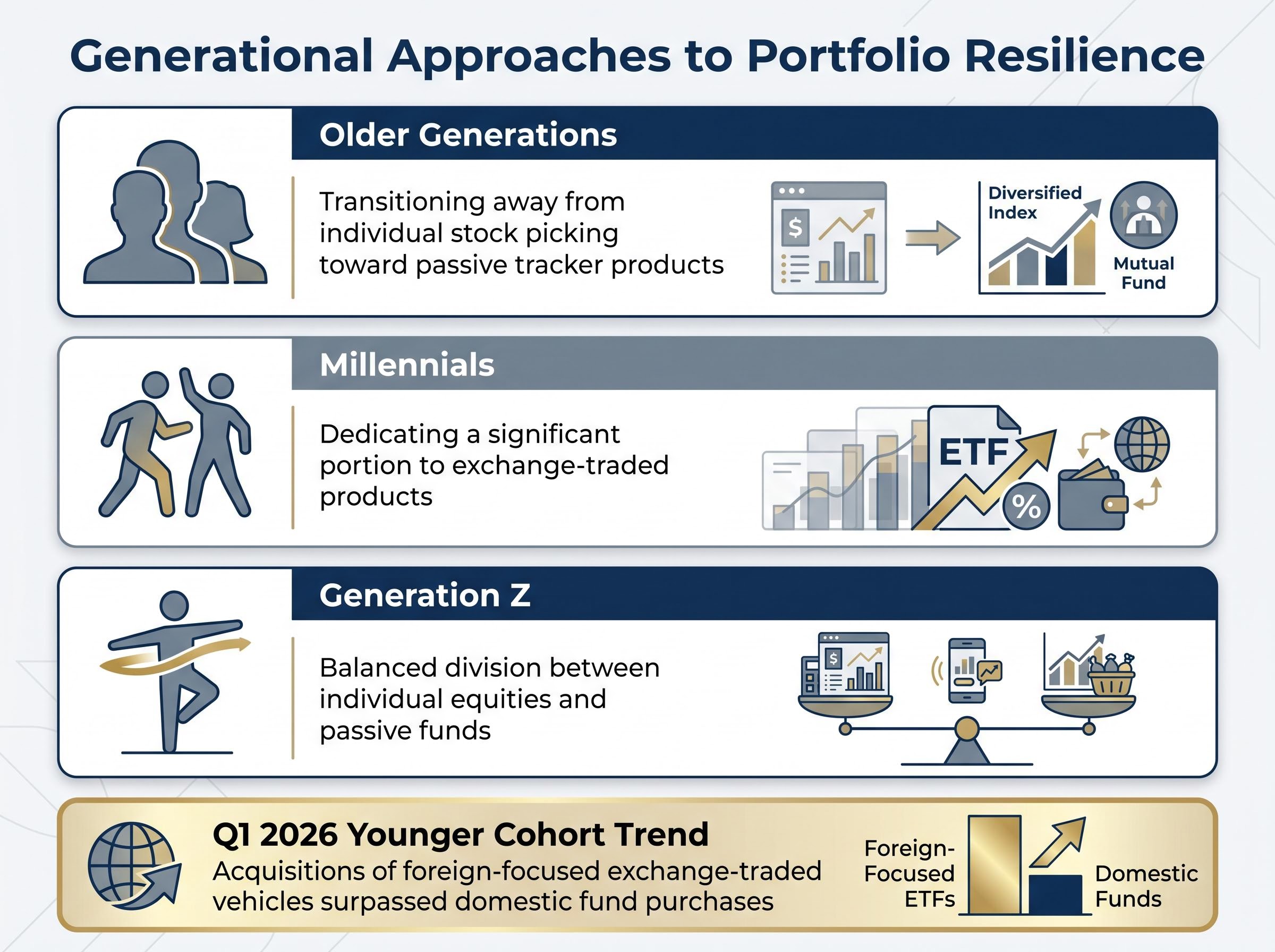

How Demographic Divides Shape Portfolio Resilience

Asset rotation patterns reveal distinct demographic divides in how Australian investors battle market volatility. Age now heavily dictates the chosen instruments for building portfolio resilience.

Older generations are increasingly transitioning away from individual stock picking. These participants are moving toward passive tracker products to insulate their capital from sudden domestic shocks. This approach minimises the need for constant portfolio monitoring during RBA announcements.

Younger demographics display entirely different structural preferences:

Millennial account holders now dedicate a significant portion of their portfolios to exchange-traded products. Generation Z participants maintain a balanced division between individual equities and passive funds. * Acquisitions of foreign-focused exchange-traded vehicles surpassed domestic fund purchases in Q1 2026 across both cohorts.

By observing how different generations build resilience, investors can audit their own portfolios for age-appropriate risk management. Younger traders lean into volatility with targeted allocations, while older investors construct broader safety nets.

The Migration to Overseas Equities

The most striking demographic consensus is the strategic move away from domestic exposure. Capturing foreign technology and healthcare opportunities serves as a functional hedge against local inflation.

However, navigating the current AI disruption in tech requires careful stock selection, as capital is rapidly migrating away from legacy software providers toward modern synthetic infrastructure.

When the RBA adjusts domestic borrowing costs, these international holdings often provide a buffer against the immediate local equity sell-off. The preference for overseas funds demonstrates an evolving understanding of geographic diversification. Australian retail capital is increasingly looking outward to bypass the limitations of domestic macroeconomic pressure.

Building Technological Defences for Volatile Trading Environments

The speed of the accelerated market requires a commensurate upgrade in personal wealth management technology. Wealth management firms are explicitly recommending digital-first strategies to combat the ongoing financial advice shortage.

Firms such as Obsidian Wealth are prioritising artificial intelligence integration for personalised trading strategies in 2026. By utilising AI, these platforms enforce strict risk management protocols that remove human hesitation from the execution process. This technology calculates optimal position sizing and executes defensive trades before a human operator can fully process a central bank press release.

Algorithmic assistance is rapidly becoming a necessity rather than a luxury to counter the speed of the modern market. Everyday investors can adopt these digital strategies by setting automated rebalancing parameters and strict stop-loss limits within their brokerage accounts.

Developing a balanced inflation investing strategy often involves using these precise algorithms to weigh short-term energy shocks against the long-term disinflationary forces of artificial intelligence.

The adoption of these tools transforms the overwhelming concept of high-speed trading into a manageable framework. The reader gains practical, forward-looking solutions to protect their wealth. By matching the market’s technological speed with personal algorithmic defences, retail participants can effectively navigate abrupt market fluctuations.

Redefining Portfolio Stability in the High-Speed Era

The March 2026 monetary policy adjustments confirmed a permanent shift in how markets digest macroeconomic developments. Hyper-sensitivity is no longer a temporary market anomaly; it is the established baseline for digital retail trading.

Market participants must acknowledge that traditional delayed reactions have been entirely replaced by instantaneous pricing mechanisms. Investors are encouraged to review their current asset allocation and digital toolsets to ensure they are adequately prepared for this accelerated reality. Adopting algorithmic risk management and diversifying through international exchange-traded products can help mitigate the whiplash of domestic policy shifts.

Formulating a resilient asset allocation strategy for this specific 2026 market shock requires understanding how these sudden yield changes impact both domestic fixed income and broader equity valuations.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.