Crude Oil Surges Past $108 as Iran Strike Is Called Off

7 hrs ago

Australia’s most significant capital gains tax overhaul in nearly three decades landed on budget night, 12 May 2026, and it has already generated a wave of investor confusion, some of it based on misreading what the changes actually do. The 2026-27 Federal Budget replaces the familiar 50% CGT discount with an inflation-indexed cost base system, introduces a 30% minimum rate floor on net capital gains, and restricts negative gearing deductions for established residential property. Both reforms take effect from 1 July 2027.

For long-term holders of shares, property, and other capital assets, the changes alter the after-tax arithmetic that has underpinned portfolio planning since 1999. What follows is a precise breakdown of what changed, what did not change, why inflation indexation can actually work in long-term investors’ favour in certain scenarios, and what international evidence shows about how equity markets typically absorb capital gains rate changes.

The two components announced on budget night are designed to work as a single system, not two separate policies. The 30% minimum rate floor and the shift to inflation indexation interlock: one determines how the gain is calculated, the other sets the lowest rate at which that gain can be taxed.

The 50% CGT discount, introduced on 21 September 1999 under the Howard government, is abolished effective 1 July 2027. Under the current system, gains on assets held for more than 12 months are reduced by half, then taxed at the investor’s marginal income tax rate. The replacement system has two parts:

The announcement that the CGT discount abolished a policy framework in place since the Howard era also confirmed that SMSFs retain their existing one-third discount under the new regime, a carve-out with significant structural implications for investors deciding where to hold growth assets in the years ahead.

The 12-month holding period threshold is preserved. The fundamental qualifier for concessional treatment remains unchanged; what shifts is the nature of the concession itself.

The Australian Treasury’s 2026-27 budget tax reform page confirms that the replacement of the 50% CGT discount with an inflation-indexed system and the 30% minimum rate floor are designed to operate as an integrated package, with both measures taking effect from 1 July 2027.

| Feature | Current system (pre-2027) | New system (from 1 July 2027) | Impact on long-term holders |

|---|---|---|---|

| CGT discount method | Flat 50% discount on nominal gain | Inflation-indexed cost base (only real gain taxed) | Favours holders in high-inflation periods; less generous in low-inflation periods |

| Minimum rate | None (taxed at marginal rate after discount) | 30% floor on net capital gains | Binds low-income investors; less impact on higher earners |

| Holding period threshold | 12 months | 12 months (unchanged) | No change to qualifying period |

| Cost base treatment | Nominal (original purchase price) | CPI-adjusted (inflation removed from gain) | Reduces taxable gain for assets held through inflationary years |

The mechanics are straightforward in principle: before calculating the taxable capital gain, the original acquisition cost is adjusted upward by a CPI-linked inflation factor. The result is that only the gain above cumulative inflation is treated as taxable income. An asset that appreciated solely because of inflation would, under this system, generate zero taxable capital gain.

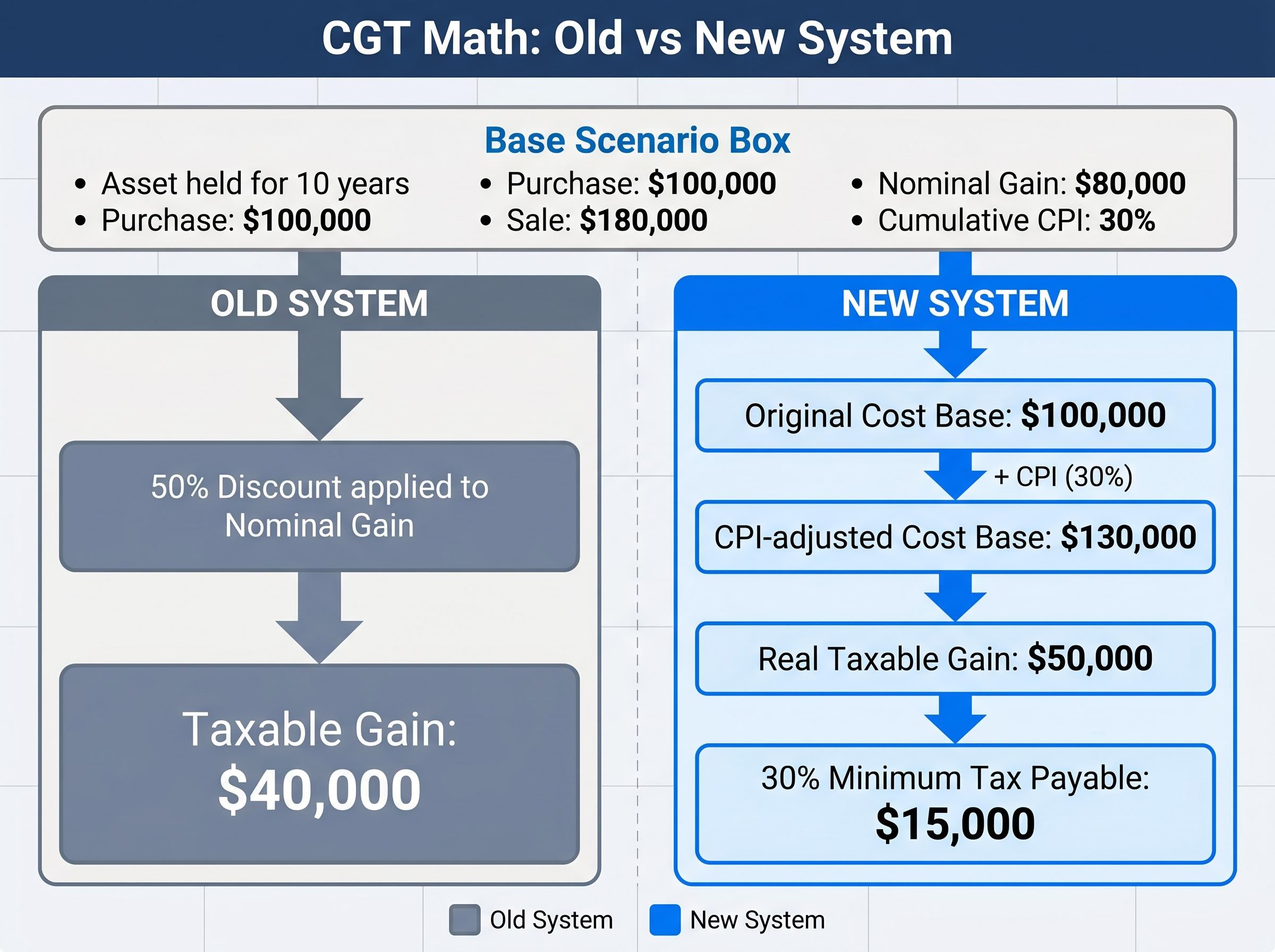

Consider a simplified illustrative calculation for an asset purchased for $100,000 and sold 10 years later for $180,000, assuming cumulative CPI inflation of 30% over that period:

Under the old 50% discount, the same asset would have produced a taxable gain of $40,000 (half of the $80,000 nominal gain). In this example, the new system produces a higher taxable gain ($50,000 versus $40,000). But if cumulative inflation were higher, say 40%, the indexed cost base rises to $140,000, reducing the taxable gain to $40,000, matching the old system’s outcome, and in even higher-inflation scenarios, the indexation method produces a lower taxable figure.

The relationship is clear: for assets with lower real returns relative to inflation, indexation can reduce the taxable gain more than the flat 50% discount. For assets with strong real appreciation, the old discount was more generous.

Pending guidance: The specific CPI series to be used and the precise calculation methodology have not yet been specified by Treasury or the Australian Taxation Office (ATO) as of mid-May 2026. Investors should treat illustrative calculations as directional rather than definitive until official guidance is released.

The negative gearing changes announced in the 2026 budget do not affect shares. They apply exclusively to established residential property acquired after 7:30pm AEST on 12 May 2026, and have no effect on leveraged equity strategies, margin lending arrangements, or share investment losses.

For equity investors: Negative gearing rules for shares and other non-residential assets are entirely unchanged by the 2026-27 budget. No action is required.

Under the pre-existing system, investors in residential property could deduct rental losses against all income streams, including wages and salary. The reform quarantines those losses for established residential property acquired after budget night: they can now only be offset against residential rental income or capital gains from residential property.

New residential property receives different treatment. Investors in newly built housing retain a choice between the old and new rules, a distinction designed to preserve construction incentives.

The boundary is precise:

| Asset type | Negative gearing (pre-budget) | Negative gearing (post-1 July 2027) |

|---|---|---|

| Shares and other equities | Losses deductible against all income | Unchanged |

| New residential property | Losses deductible against all income | Investor choice: old or new rules |

| Established residential property (acquired pre-budget night) | Losses deductible against all income | Unchanged (grandfathered) |

| Established residential property (acquired after 7:30pm AEST, 12 May 2026) | N/A | Losses quarantined to residential rental income or capital gains only |

The budget-night cut-off of 7:30pm AEST, 12 May 2026 follows standard Australian practice: prospective tax changes are applied from the moment of announcement to prevent forestalling transactions.

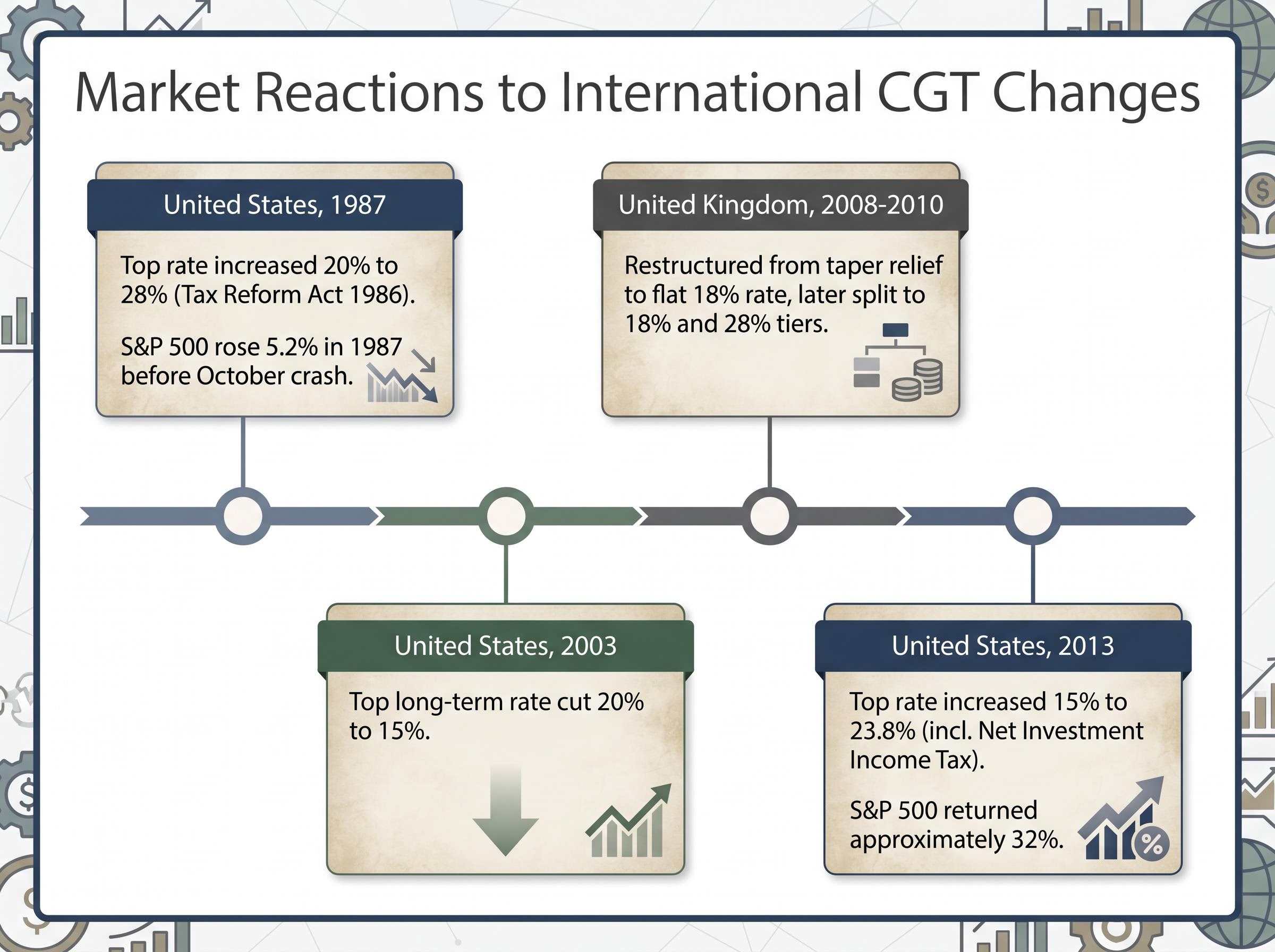

Investors anticipating a sustained equity selloff in response to CGT reform may want to examine what actually happened in comparable situations abroad. The international evidence base offers a counterintuitive pattern: capital gains rate changes, in both directions, have consistently failed to produce the dramatic equity market reactions that investors expected.

The structural reason is consistent across jurisdictions. Markets absorb CGT changes as investors recalculate expected after-tax returns and adjust participation accordingly. Some investors accelerate realisations ahead of rate increases; others defer. But the aggregate effect is a recalibration of after-tax return expectations, not a mass exit.

Higher effective CGT rates historically produce a lock-in effect on asset sales, where investors delay or forgo disposals rather than trigger a larger tax liability, and Stockspot modelling cited in the budget week analysis suggests a business founder selling a $1 million company could lose more than $225,000 in after-tax proceeds under the new regime compared with the current 50% discount system.

The pattern across decades and jurisdictions: Markets recalibrate when capital gains rates change. They do not collapse. Investors adjust their after-tax return calculations and continue participating.

The Australian reforms were anticipated for several months before the May 2026 budget announcement, further reducing the potential for market surprise and front-loading any rational repositioning that institutional investors chose to make.

Investors exploring which parts of the market are structurally advantaged or disadvantaged by the shift away from the CGT discount will find our deep-dive into ASX sector rotation after the CGT reform covers how fully franked dividend payers including the major banks and miners carry a structural tailwind, while growth sectors such as technology and biotech face a derating of the tax premium embedded in their valuations.

The 30% floor is a single number, but its impact varies sharply depending on the taxpayer’s income bracket. Placing yourself accurately in the affected or unaffected population matters more than reacting to the headline rate.

Under the current system, a taxpayer with taxable income below approximately $45,000 faces a marginal rate of 19%. After the 50% discount, the effective CGT rate on a long-term gain could fall as low as 9.5%. The 30% floor eliminates that arithmetic entirely.

This reform specifically closes off a timing-based planning strategy: selling assets in years of low income (during career breaks, sabbaticals, or early retirement) to minimise capital gains tax. For retirees managing drawdown strategies around the tax-free threshold, the floor represents a genuine increase in effective rates.

For investors on the 45% marginal rate, the binding constraint was never the rate floor; it was the size of the taxable gain. Here, inflation indexation does the heavier work. An asset held for 15 years through periods of moderate-to-high inflation could see its indexed cost base substantially higher than the original purchase price, compressing the taxable gain.

Whether the net effect is better or worse than the old 50% discount depends on individual circumstances: the holding period, the inflation trajectory during that period, and the proportion of nominal appreciation attributable to real growth. No single answer applies across all taxpayers, and as of mid-May 2026, no official estimates of how many taxpayers are captured by the floor have been released.

The period between now and 1 July 2027 is a planning window. Several actions and decisions warrant attention before the new system commences:

For investors wanting to model the terminal wealth impact of the rate change on their specific holdings, our comprehensive walkthrough of CGT-efficient portfolio structures covers low-turnover ETF strategies, superannuation contribution sequencing, and buy-only rebalancing approaches that reduce realisation frequency before the 1 July 2027 transition deadline.

Equity investors and negative gearing: No action is required. The negative gearing changes do not apply to shares, margin lending, or any non-residential asset class.

The CGT reform is real and its mechanics matter. But the change is not uniformly punitive. Inflation indexation benefits long-term holders in many scenarios, particularly where a significant portion of an asset’s appreciation reflects inflation rather than real growth. The negative gearing restriction draws a precise boundary around established residential property and does not touch equity investors. International evidence from comparable rate changes in the US and UK suggests markets absorb these reforms through recalibration, not upheaval.

Genuine uncertainty remains. ATO implementation details on the CPI series and calculation methodology are pending. Investors with complex portfolios or large unrealised gains should seek professional tax advice rather than acting on general commentary.

The window between now and 1 July 2027 is a planning opportunity. Investors who understand the actual mechanics of the reform, rather than the headlines, are best placed to use it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Tax outcomes depend on individual circumstances, and the implementation details of these reforms remain subject to further ATO and Treasury guidance.

The 2026-27 Federal Budget abolishes the 50% CGT discount and replaces it with an inflation-indexed cost base system, meaning only real gains above cumulative CPI inflation are taxed. A 30% minimum rate floor on net capital gains for assets held more than 12 months is also introduced, with both measures taking effect from 1 July 2027.

Under the new system, the original purchase price of an asset is adjusted upward by a CPI-linked inflation factor before the taxable gain is calculated, so only the portion of appreciation above cumulative inflation is treated as income. For example, an asset bought for $100,000 with 30% cumulative inflation would have an adjusted cost base of $130,000, reducing the taxable gain accordingly.

No, the negative gearing restrictions announced in the 2026 budget apply exclusively to established residential property acquired after 7:30pm AEST on 12 May 2026, and have no effect on shares, margin lending, or any other non-residential asset class.

Low-income investors and those who strategically sell assets in low-income years are most affected, as the floor eliminates the ability to achieve effective CGT rates well below 30% through income timing. High-income earners on the 45% marginal rate may actually see a lower effective rate in some scenarios because inflation indexation reduces the taxable gain.

Investors should identify assets with large unrealised capital gains held more than 12 months, model after-tax outcomes under both the old and new systems, and consider whether crystallising gains before 1 July 2027 makes sense for their situation. Seeking licensed tax advice is strongly recommended, particularly for complex portfolios or large unrealised gains.