British pharmaceutical heavyweights AstraZeneca and GSK entered the spring of 2026 facing similar global headwinds, yet their initial quarterly filings reveal entirely different commercial trajectories. April 2026 earnings reports dropped amid intense debate over US vaccine policy and shifting UK government pricing frameworks. These macroeconomic factors are forcing market participants to look closely at underlying portfolio resilience.

Analysing the AstraZeneca GSK financial results provides investors with immediate clarity on which corporation is currently executing its commercial strategy most effectively. This analysis unpacks the financial data, sector growth engines, and geopolitical risks shaping the outlook for both companies through the remainder of the year. The initial numbers demonstrate how therapeutic specialisation provides shelter from broader macroeconomic volatility.

Understanding these dynamics is necessary for navigating the healthcare sector in a high-rate environment.

Comparing First Quarter Revenue and Sector Leadership

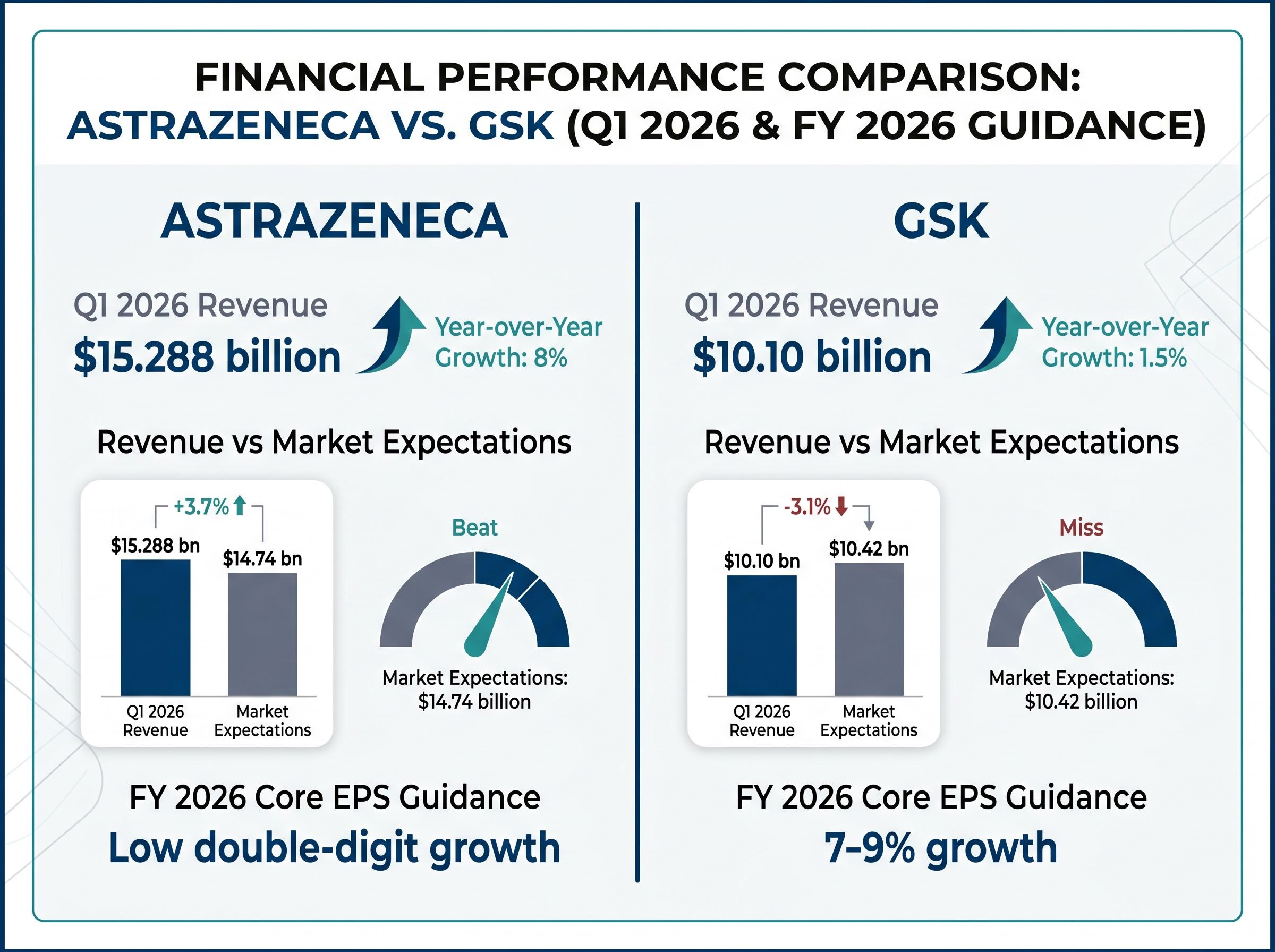

The aggregate revenue figures for the three months ending March 2026 establish a clear leader in top-line expansion. AstraZeneca reported $15.288 billion in total revenue, delivering an 8% year-over-year increase. This strong performance comfortably beat market expectations of $14.74 billion, highlighting the commercial efficiency of their current product mix.

Conversely, GSK reported a turnover of $10.10 billion for the quarter, representing a modest 1.5% overall increase. This result missed the $10.42 billion consensus forecast, reflecting softer performance in legacy product lines. These baseline figures provide investors with immediate clarity on how each firm is navigating shared macroeconomic challenges.

The gap in top-line growth reveals underlying differences in commercial momentum. Market analysts have adjusted their models accordingly, placing heavier weight on the corporations that demonstrate reliable earnings beats.

Both entities are simultaneously competing for operational advantages through tier-one pharmaceutical contracts, recently highlighted when GSK matched AstraZeneca by securing advanced quantitative lung imaging analytics to support clinical trial efficiency.

Management guidance points to continued divergence through the remainder of the fiscal period. AstraZeneca projects mid-to-high single-digit percentage growth in total revenue for the full year. GSK anticipates 3-5% turnover growth alongside 7-9% core EPS expansion.

These forward-looking statements encode management’s confidence in their respective product pipelines. The guidance numbers reflect a broader industry pattern where capital is increasingly concentrated in top-performing assets.

| Company | Q1 2026 Revenue | Year-over-Year Growth | Market Expectations | FY 2026 Core EPS Guidance |

|---|---|---|---|---|

| AstraZeneca | $15.288 billion | 8% | $14.74 billion | Low double-digit growth |

| GSK | $10.10 billion | 1.5% | $10.42 billion | 7-9% growth |

When big ASX news breaks, our subscribers know first

Understanding the Margin Power of Oncology and Rare Diseases

Specialised medicines and cancer therapeutics offer stronger commercial resilience compared to general treatments due to their high barriers to entry and sustained pricing power. A clinical endpoint refers to a specific health outcome measured in a medical trial to determine if a treatment is effective. Treatments meeting these strict endpoints often secure exclusive market periods, insulating them from generic competition.

By understanding the underlying mechanics of specialty drug margins, investors can better evaluate why certain pharmaceutical stocks maintain their valuations even when broader product lines stagnate.

This structural advantage specifically propelled the first quarter gains for both firms. AstraZeneca saw a double-digit expansion in its cancer treatment division and a double-digit upward trajectory for rare medical conditions. These divisions remain the primary growth engines protecting the company from broader market volatility.

This rare disease commercial traction is highly prized by investors, as exclusive treatments for complex conditions frequently generate record royalty streams and sustain market dominance over multiple fiscal periods.

High-margin therapies generate outsized cash flows, supporting further research and development initiatives. GSK also relied heavily on this dynamic to support its earnings base. The firm experienced a massive surge in its oncology segment.

Specialty Medicines provided low double-digit growth for the corporation, keeping its overall revenue positive amid declines elsewhere. The data shows that specialty drug outperformance is an industry-wide requirement for top-line expansion.

AstraZeneca Oncology: Delivered double-digit growth through established high-margin cancer therapies. AstraZeneca Rare Diseases: Reached a double-digit growth trajectory based on exclusive treatment profiles. * GSK Specialty Medicines: Produced low double-digit overall expansion across the division.

Transatlantic Turbulence and the North American Vaccine Market

The North American market presents a more complex operating environment, characterised by political friction and public health scepticism. Changing state-level policies and residual Trump-era pricing pressures are actively dampening commercial forecasts for major manufacturers. The policy uncertainty impacting the pharmaceutical sector in the United States has forced a recalibration of short-term revenue expectations.

This transatlantic turbulence directly affects immunisation portfolios. GSK faces a projected low single-digit decline in its vaccines segment for the full year 2026. A federal court recently blocked a proposed vaccine overhaul, compounding the challenges of increasing public distrust in federal health guidance.

These political developments introduce a layer of volatility that is difficult to hedge against in traditional equity portfolios.

Market Commentary “US political uncertainty and growing public distrust of federal health guidance are actively suppressing vaccine uptake, creating a near-term revenue ceiling for companies heavily exposed to North American immunisation programmes,” noted industry analysts regarding the latest earnings data.

Despite these headwinds, specific inoculations continue to demonstrate exceptional commercial viability. North America remains the most lucrative healthcare market globally, making these regional political risks highly relevant for accurately pricing pharmaceutical equities in 2026.

Share prices have hit 24-year highs despite soft vaccine revenue, indicating complex market reactions to these headwinds. Investors appear willing to overlook isolated segment declines if the core specialty business remains intact.

For investors exploring how other major healthcare players are navigating similar operational headwinds, our detailed coverage of pharmaceutical margin pressures examines how strong top-line revenue beats can sometimes mask underlying gross margin contractions in the current macroeconomic environment.

Domestic Infrastructure Investment Under the Starmer Government

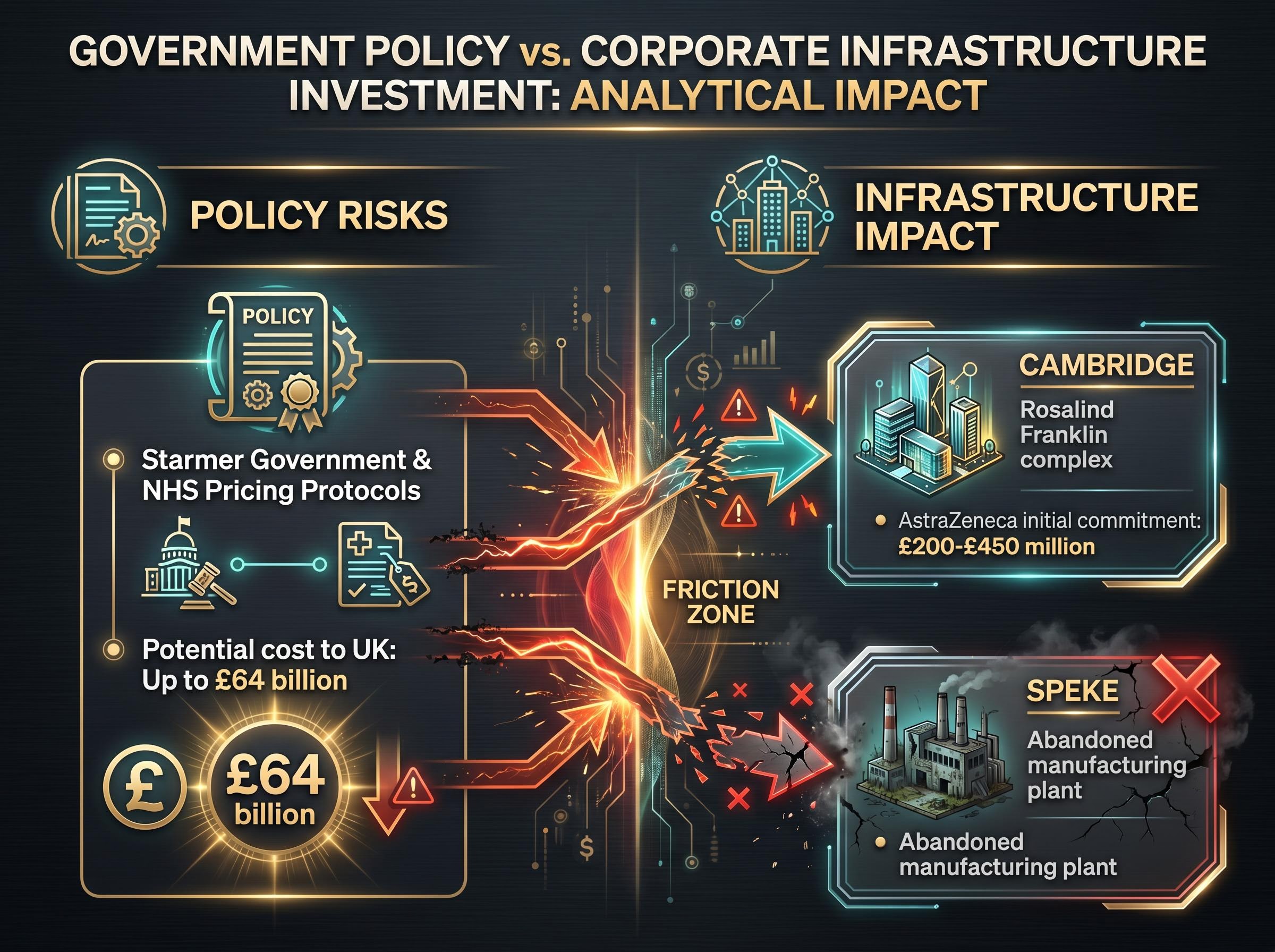

Capital expenditure decisions in the United Kingdom face a separate set of political headwinds. Domestic regulatory environments dictate corporate expansion strategies, and pharmaceutical leadership is currently hesitating on major facility investments. Critics warn of potentially complex government pricing deals that could cost the UK up to £64 billion, prompting firms to re-evaluate their domestic footprints.

The correlation between state backing and corporate expenditure has never been more apparent.

NHS Pricing Protocols and Industry Friction

The tension between industry leadership and the Starmer government regarding National Health Service pricing protocols is increasingly visible. AstraZeneca initially committed £200-£450 million toward infrastructure, including funds for the Rosalind Franklin complex in Cambridge. However, the fluctuating status of these investments indicates a deep unease with proposed regulatory frameworks.

Corporate boards are demanding clearer revenue pathways before committing significant capital to permanent infrastructure. This friction directly impacts domestic job creation and industrial capacity.

In response to these regional funding constraints, some healthcare developers are pivoting toward strategic clinical licensing models that replace heavy infrastructure spending with milestone payments and royalties from established global partners.

A previously planned manufacturing plant in Speke remains abandoned due to diminished state backing. Pharmaceutical firms are warning they may deliberately withhold investments if the government does not permit necessary drug price adjustments. Investors must monitor these policy battles closely, as they ultimately dictate future research capabilities and profit margins.

Diverging Analyst Forecasts and the Year Ahead

Financial analysts project clearly diverging paths for the two corporations based on the newly released financial data and geopolitical factors. AstraZeneca is widely regarded as the top pharmaceutical pick for 2026. Analysts project 7.2% sales growth and 11.2% profit growth for the company over the coming year.

This consensus view reflects confidence in the firm’s oncology pipeline and limited exposure to vaccine-related volatility.

In contrast, consensus views demonstrate a more cautious stance on the domestic rival. GSK frequently receives underweight ratings from analysts due to the ongoing challenges in its vaccine portfolio. However, some analysts maintain a hold rating based on the firm’s solid 3-5% sales growth fundamentals.

Recent Whalesbook analyst consensus reporting confirms this broader sentiment, showing that AstraZeneca retains moderate buy recommendations while its domestic rival increasingly faces reduce ratings from institutional observers.

The regulatory environment offers potential upside for both entities in the immediate future. Investors evaluating these equities must watch specific forward-looking metrics to determine whether the first-quarter trends will hold through the fiscal year.

- Pipeline Authorisations: The speed at which newly authorised medical treatments transition from clinical settings to commercial availability.

- Vaccine Revenue Stabilisation: Whether public health campaigns can arrest the low single-digit decline projected for North American immunisation portfolios.

- UK Policy Resolution: The outcome of ongoing negotiations regarding NHS pricing protocols and subsequent corporate infrastructure commitments.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.