Why ASX Gold Stocks Fell 7% While Gold Futures Stayed Flat

38 mins ago

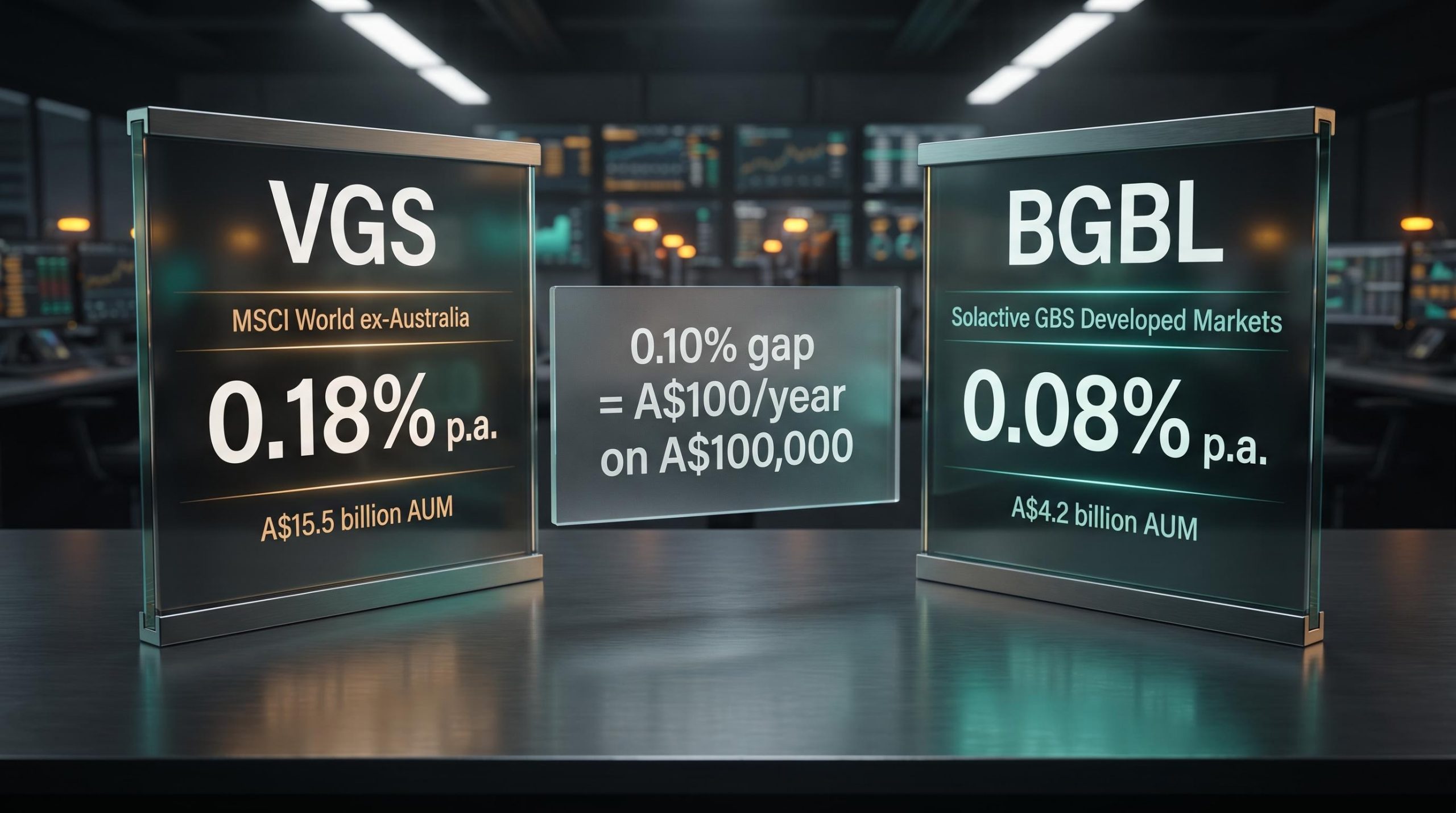

Vanguard is owned by its investors. It has no external shareholders. Its entire philosophy is built on returning economies of scale as lower fees. And yet its flagship international shares ETF, VGS, charges 0.18% per year, while Betashares’ BGBL offers near-identical developed market exposure for 0.08%.

That is a 0.10 percentage point gap from a manager whose ownership model is specifically designed to be the cheapest option. The assumption most Australian ETF investors carry, that Vanguard’s mutual structure means Vanguard is always the lowest-cost choice, is reasonable. It is also incomplete. The gap is not a failure of the model. It is a consequence of a cost the model was never designed to touch.

Here is the framework for understanding what actually drives Vanguard ETF fees, why a for-profit competitor can legitimately charge less for similar exposure, and how you can apply a concrete three-step check to any ETF comparison so you are evaluating real economics rather than brand reputation.

Vanguard operates under a mutual ownership structure that functions as a closed loop. The funds themselves own the management company, and investors in those funds own the funds. Because there are no outside shareholders extracting dividends or profits, the efficiencies that come with growing scale are passed back to investors through fee reductions rather than being distributed elsewhere. That is a structural reality, not a marketing claim.

The real-world impact is measurable. Vanguard announced one of the largest fee reduction programmes in its history, lowering costs across dozens of funds at an estimated annual revenue impact of US$350 million. The scale savings were returned to investors, precisely as the model intends.

But the model has a precise boundary. It governs costs Vanguard directly controls:

A Vanguard spokesperson has confirmed that index licensing fees vary across providers and are one of several factors the firm weighs when setting fund pricing. Morningstar Senior Manager Research analyst Zunjar Sanzgiri noted that the mutual model cannot guarantee the lowest fee in every situation, especially where MSCI benchmarks and similar legacy exposures come with structurally higher underlying costs.

What this means for you is direct: the Vanguard brand cannot serve as a shortcut for finding the cheapest product. You need to look at what the specific fund is actually paying for.

If you are working through your first ETF comparison, grounding yourself in ETF basics for Australian investors is worth the time: the mechanics of how units are created, how management fees are deducted, and how ASX-listed ETFs differ from unlisted managed funds all bear directly on what a TER figure actually represents.

When you open a Product Disclosure Statement (PDS), a document that sets out the key features and costs of a financial product, you see a single number: the total expense ratio (TER). That number already includes the licensing fee the fund pays to use its index. What it does not tell you is how that licensing fee is structured, and that structure determines whether the fund’s costs can fall as it grows or whether they are locked in place.

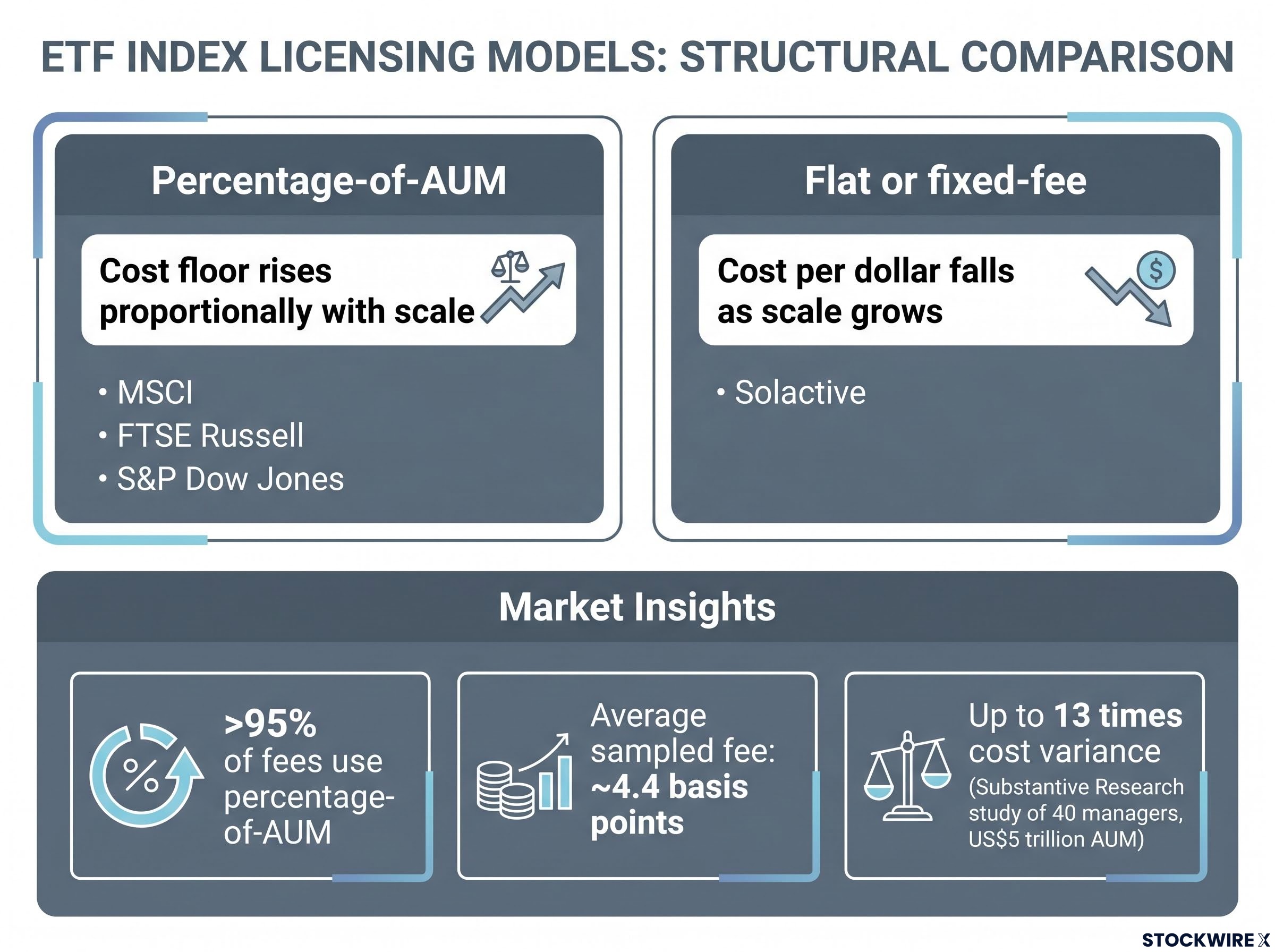

Every index ETF pays a fee to its index provider, the company that maintains the benchmark the fund tracks. How that fee is calculated varies dramatically.

| Attribute | Percentage-of-AUM licensing | Flat or fixed-fee licensing |

|---|---|---|

| How the fee is set | As a percentage of total assets under management | A mostly fixed amount, sometimes with negotiated tiers |

| How it behaves as AUM grows | Absolute cost rises proportionally; cost per dollar stays flat | Fixed cost spread over more dollars; cost per dollar falls |

| Major providers using this structure | MSCI, FTSE Russell, S&P Dow Jones | Solactive and newer entrants |

| Implication for the fund’s TER floor | Creates a cost floor that scale alone cannot breach | Scale directly lowers the effective licensing cost per investor |

More than 95% of licensing fees in examined samples are structured as percentage-of-AUM. Average licensing fees in sampled U.S. equity ETFs sit at approximately 4.4 basis points.

A study by Substantive Research covering 40 investment managers with a combined US$5 trillion in assets under management found that licensing costs for comparable index services can vary by as much as 13 times between the highest- and lowest-paying managers.

That dispersion is the reason two funds holding almost identical shares can carry materially different TERs. For you, the index provider name on the PDS becomes a meaningful signal. Seeing “MSCI” tells you something predictable about the cost floor the manager is working against before you even look at the fee.

Start with the two products side by side.

| Attribute | VGS | BGBL |

|---|---|---|

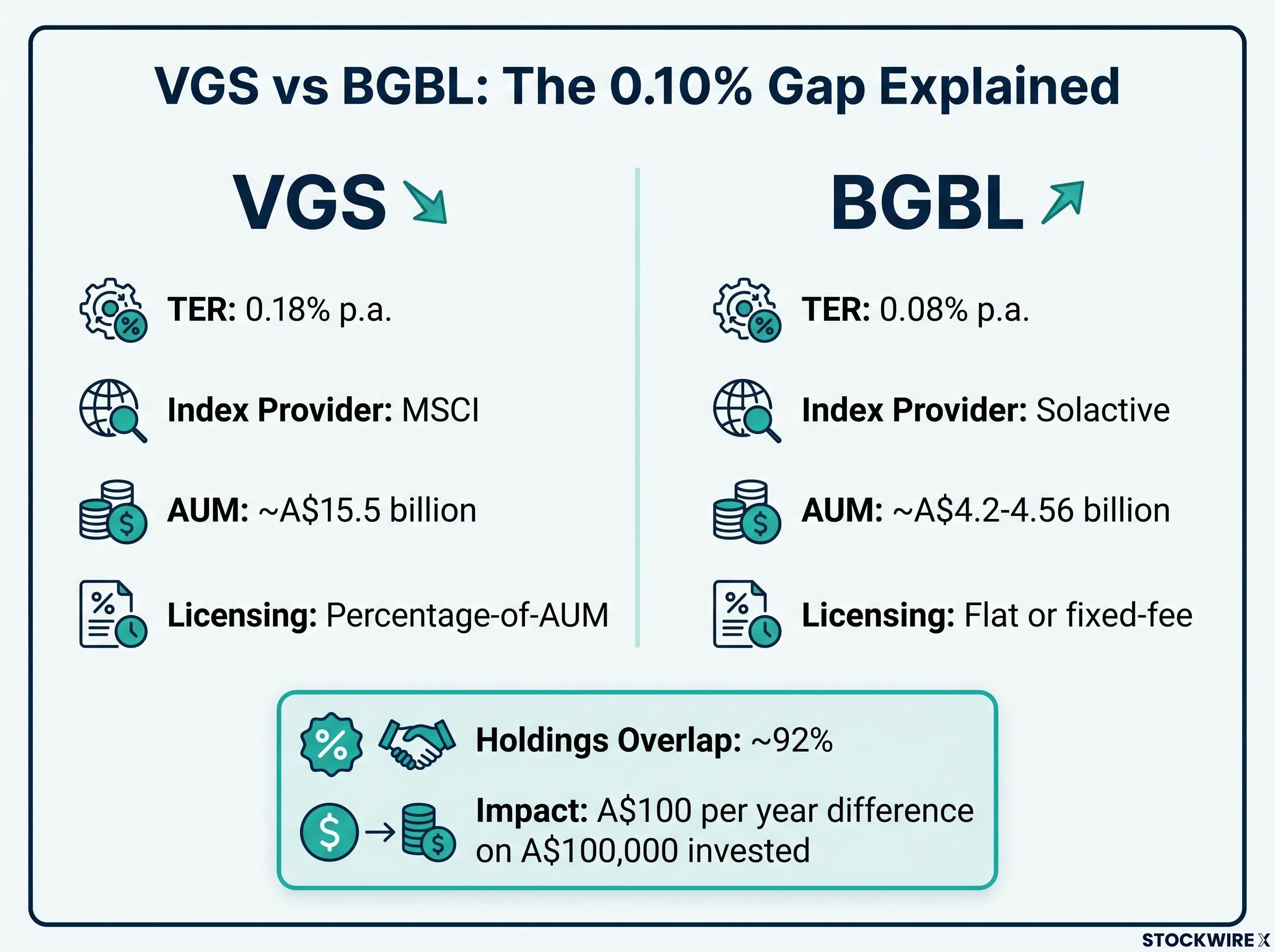

| Index tracked | MSCI World ex-Australia | Solactive GBS Developed Markets ex Australia Large & Mid Cap |

| Index provider | MSCI | Solactive |

| TER | 0.18% p.a. | 0.08% p.a. |

| AUM | Approximately A$15.5 billion | Approximately A$4.2-4.56 billion |

| Licensing structure | Percentage-of-AUM | Flat or fixed-fee |

The two products target comparable ground. Both indexes cover large- and mid-cap equities in developed markets outside Australia, both apply market-capitalisation weighting, and analyses of their holdings report approximately 92% overlap. Where the indexes diverge is in methodology: MSCI and Solactive apply different rules for classifying markets, selecting constituents, and managing corporate actions, producing modest variation in holdings rather than fundamentally different investment outcomes.

So where does the 0.10 percentage point gap come from?

VGS holds an MSCI licence under a percentage-of-AUM structure. That means every dollar of growth in the fund’s A$15.5 billion asset base brings a proportionally higher absolute licensing bill, setting a cost floor that Vanguard cannot undercut without renegotiating the contract terms entirely.

BGBL licences a Solactive index under a flat or fixed-fee arrangement. As the fund’s asset base expands, the licensing cost is spread across more investors, reducing the effective per-dollar charge. According to Morningstar analyst Zunjar Sanzgiri, Betashares runs BGBL profitably at its current A$4.2-4.56 billion in assets while charging 0.08%.

On A$100,000 invested, the 0.10 percentage point difference amounts to A$100 per year. Over a multi-decade investment horizon, that gap compounds into a meaningful drag on total returns.

For additional context, BlackRock’s iShares Core MSCI World ex Aus ESG ETF is priced at 0.09%, lower than VGS despite BlackRock being a for-profit manager. However, that product incorporates an ESG screen, so it is not a direct like-for-like comparison.

BGBL’s lower fee is not a loss-leader or a sign of lower quality. It reflects a structurally cheaper licensing arrangement that Betashares chose and Vanguard did not. That gap is unlikely to close unless the underlying licensing terms change.

The logic resolves cleanly once you separate the moving parts.

A for-profit manager that selects a flat-fee index provider and negotiates a cost-efficient licensing structure can offer a lower TER for similar exposure while still generating a profit. The licensing savings are large enough to undercut a mutual manager paying percentage-of-AUM fees even after the for-profit manager takes its margin.

This does not mean the mutual model is broken. It means the for-profit versus mutual distinction is a useful lens for understanding how a manager’s profits are allocated, but it is the wrong tool for predicting which specific product will be cheapest.

The confusion comes from conflating three things that sound related but operate independently.

The fee gap between VGS and IVV illustrates the same licensing dynamic from another angle: IVV tracks the S&P 500 at 0.04% per annum, a 0.14 percentage point saving over VGS on a fund with even greater US equity concentration, which shows that index provider choice shapes the cost floor across the entire international equity ETF category, not just in the BGBL comparison.

This separation is worth keeping visible because it applies to every ETF comparison you will ever make, not just VGS versus BGBL.

| Concept | What it actually tells you about the fund |

|---|---|

| Ownership structure (mutual vs for-profit) | How profits on the manager’s own cost base are allocated |

| Product pricing (TER) | What you as an investor actually pay, inclusive of all costs |

| External contracts (index licences) | Can dominate product pricing regardless of the manager’s philosophy |

Morningstar analyst Zunjar Sanzgiri has noted that where a fund tracks a legacy benchmark carrying elevated licensing costs, the mutual ownership model provides no mechanism to absorb those external charges. The fact that Betashares operates BGBL profitably at 0.08% demonstrates that the lower fee is a function of licensing economics, not a subsidised offering.

The ownership model story is genuinely worth understanding. It should never substitute for reading the actual TER and understanding its components.

You can apply this three-step check to any ETF comparison. It takes under five minutes using publicly available PDS documents, and it will reliably surface fee gaps that brand reputation alone would have obscured.

The iShares ESG example illustrates why this comparability step matters: its 0.09% TER is lower than VGS, but the ESG screen makes it a different product, not a directly superior one. The approximately 92% overlap between VGS and BGBL is what sufficient comparability looks like in practice.

Vanguard’s mutual model delivers genuine benefits. It creates a structural incentive to pass scale savings back to investors on internally controllable costs, and it has a long track record of doing so. The US$350 million fee reduction cycle is evidence of that commitment, not just a talking point.

But holding VGS is a choice that carries a 0.10 percentage point annual cost relative to a comparable alternative. On A$100,000, that is A$100 per year. Over a 20-30 year investment horizon, that cost compounds in a way that is worth consciously accepting rather than accidentally overlooking.

Fee compounding over a 30-year horizon is where the abstract 0.10 percentage point difference becomes concrete: Morningstar research identifies ETF fees as a more reliable predictor of long-term relative returns than past performance or fund size, and modelling shows a sub-1% fee gap can compound into a terminal wealth difference exceeding $575,000 on an equivalent starting portfolio.

VGS remains a credible, liquid product with approximately A$15.5 billion in assets. Many Australian investors have chosen it knowingly, valuing tracking precision against the MSCI benchmark, brand trust, or the depth of liquidity that comes with a fund of that scale.

The most informed investors evaluate ownership philosophy and product economics separately. The Australian ETF market now offers enough genuine competition that those two evaluations rarely produce the same answer. This is a decision worth revisiting deliberately, not an oversight to feel anxious about. The right answer depends on how you weigh tracking precision, brand trust, and fee sensitivity in your own situation.

If the VGS versus BGBL comparison has prompted a broader review of your international exposure, building a core ASX ETF portfolio with clear domestic, international, and income allocations is the natural next step, and doing it with explicit fee discipline from the outset avoids the compounding cost that comes from restructuring later.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Vanguard's mutual ownership model only controls internally managed costs; when a fund licences a benchmark from MSCI under a percentage-of-AUM fee structure, that external cost creates a floor Vanguard cannot cut through scale alone, whereas Betashares chose a flat-fee Solactive licence for BGBL that becomes cheaper per dollar as assets grow.

An index licensing fee is the charge a fund pays to the company that maintains its benchmark, and it is already embedded in the TER you see on the PDS; the structure of that fee, whether it scales with assets or stays fixed, determines whether the fund's costs can fall as it grows or are locked in place.

VGS and BGBL have approximately 92% holdings overlap, as both track large- and mid-cap developed market equities outside Australia using market-capitalisation weighting, with modest differences arising from MSCI and Solactive applying different constituent selection and market classification rules.

On A$100,000 invested, the 0.10 percentage point annual gap costs A$100 per year, and Morningstar research shows that sub-1% fee differences can compound into terminal wealth gaps exceeding A$575,000 over a 30-year horizon on an equivalent starting portfolio.

Check the TER on each fund's PDS, identify the index provider as a signal of likely licensing structure (MSCI and FTSE Russell typically use percentage-of-AUM, Solactive more often uses flat fees), then verify both funds target similar markets, capitalisation ranges, and geographic scope before treating any fee gap as meaningful.