Why Vanguard ETF Fees Aren’t Always the Lowest on the ASX

6 hrs ago

A trade executes, and in the same instant it settles. No waiting period. No capital locked in a margin buffer. No counterparty risk accumulating overnight while a clearinghouse processes the paperwork. That is not a theoretical possibility; it is already running in pilot form within Australian markets in 2025, under a programme backed by the Reserve Bank of Australia (RBA).

The question is what happens when that capability scales across the entire market infrastructure, and what happens when the same technologies creating this efficiency also introduce risks that no single firm’s risk management framework can fully see. ASIC’s REP 835, released as Australia’s markets are being actively reshaped by distributed ledger technology (DLT), tokenised assets, and artificial intelligence (AI), is the formal mapping of that terrain.

After reading this, you will be able to distinguish between what these technologies genuinely change about how markets function, what specific risks ASIC has formally identified, and how Australia’s regulatory response is designed to let innovation and investor protection advance together rather than trade off against each other.

If your assumption is that fintech is just a faster version of existing infrastructure, that assumption needs correcting. What DLT, tokenised assets, and AI are doing is not making existing market functions run quicker. They are changing the structural features of how markets clear, settle, intermediate risk, and interact with you as a participant.

ASIC’s REP 835 frames these technologies as changing three things simultaneously: how markets clear and settle, how risk is intermediated between parties, and how both institutions and retail investors engage with financial markets. That is not an upgrade. It is a reconfiguration.

ASIC REP 835 frames these technologies as changing three things simultaneously: how markets clear and settle, how risk is intermediated between parties, and how both institutions and retail investors engage with financial markets.

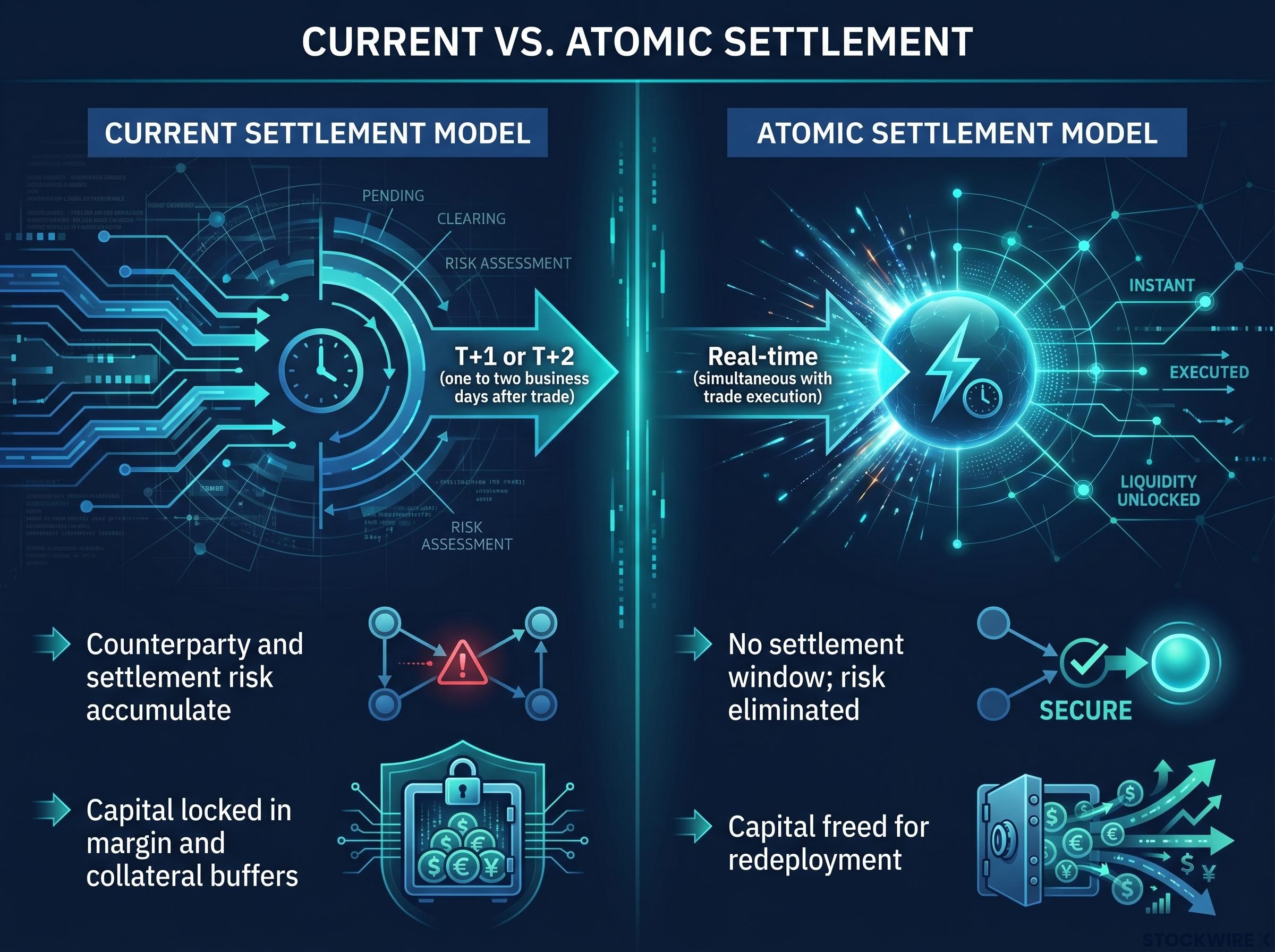

DLT and tokenised assets affect settlement mechanics and capital efficiency, not just record-keeping speed. The clearest expression of this is atomic settlement, which is the simultaneous, real-time exchange of assets and payment that eliminates the gap between trade execution and final settlement. Where a traditional settlement cycle leaves a window of hours or days during which counterparty risk accumulates, atomic settlement closes that window entirely.

The tokenised asset infrastructure taking shape under Project Acacia does not exist in a legal vacuum; crypto regulation in Australia has shifted from soft guidance to court-imposed penalties, with the Corporations Amendment (Digital Assets Framework) Act 2026 now introducing purpose-built licensing categories for digital asset and tokenised custody platforms for the first time.

The implications for capital efficiency are just as significant, and the next section walks through exactly how that works.

AI should not be understood solely as a trading algorithm. It operates across three distinct layers of the market stack simultaneously:

That three-layer penetration means AI’s influence on your experience as an investor is not abstract. It already shapes what you are shown on a platform, how risk is monitored on your behalf, and how trades around you are executed. All three layers are moving at once.

To understand why atomic settlement matters, you need to understand what it eliminates. In a conventional settlement model, a trade executes at one moment and settles at a later one, typically one or two business days afterwards. During that gap, both parties carry risk: the buyer might not deliver payment, or the seller might not deliver the asset. To manage that risk, capital gets locked into margin and collateral buffers.

Atomic settlement in plain terms: the asset and the payment change hands at the same instant, in real time. There is no gap between the trade and the final exchange. The settlement window, and all the risk that accumulates inside it, disappears.

The efficiency gain from this works in two distinct ways. The first is straightforward: less counterparty and settlement risk during a window that no longer exists. The second is the one that changes behaviour at scale. Capital previously trapped in margin and collateral buffers gets freed. That freed capital can be redeployed, which means atomic settlement has a compounding efficiency effect across the system, not just at the point of settlement.

| Feature | Current settlement model | Atomic settlement model |

|---|---|---|

| Timing | T+1 or T+2 (one to two business days after trade) | Real-time (simultaneous with trade execution) |

| Risk during settlement window | Counterparty and settlement risk accumulate | No settlement window; risk eliminated |

| Capital implications | Capital locked in margin and collateral buffers | Capital freed for redeployment |

This is not theoretical. Project Acacia was run jointly by the RBA and the Digital Finance Cooperative Research Centre (DFCRC) to investigate how digital money could function within wholesale tokenised asset markets. When ASIC extended regulatory relief to participants in that project in July 2025, it turned the abstract mechanics described above into a live, supervised test running inside Australia’s own financial system. The principles articulated in REP 835 are not waiting to be tried; they are already under examination.

The ASIC regulatory relief for Project Acacia, granted in July 2025, turned the abstract mechanics of atomic settlement into a live, supervised test running inside Australia’s own financial system, with the principles articulated in REP 835 already under active examination rather than waiting to be tried.

The opportunity from financial market innovation is real, but understanding why it is real requires separating three distinct benefits, each with its own mechanism.

The first is capital and operational efficiency. Upgraded market infrastructure, from atomic settlement through to automated compliance monitoring, cuts the amount of capital tied down in settlement processes while also lowering the operational burden of surveillance and reporting. For market participants, those are quantifiable improvements, not aspirational ones.

The second is clearer regulatory pathways for new products. REP 835 treats it as a priority that firms can access well-structured routes to develop and bring to market new products, with regulatory engagement built in rather than bolted on afterwards. These pathways are not a single instrument. They are three distinct tools:

Each carries a different level of regulatory engagement and a different risk profile. Understanding the distinction matters if you are evaluating how any firm or product is navigating the regulatory environment.

The third is market competitiveness, and this is where a common assumption gets flipped. The argument in REP 835 is that without clear trial pathways, innovation does not stop. It either migrates to less-supervised jurisdictions or moves into domestic grey areas. Both outcomes reduce investor protection without stopping the underlying activity. Responsible innovation frameworks are therefore partly a defensive measure: they keep innovation visible and supervisable rather than driving it offshore or underground.

ASIC Commissioner Simone Constant has attributed the view that supporting responsible innovation enhances Australia’s market competitiveness while maintaining investor protections, framing ongoing public-private and global regulatory collaboration as beneficial to this objective.

That framing matters. ASIC’s approach is not simply permissive. It is structured around keeping innovation where regulators can see it.

The temptation is to bundle the risks from financial market innovation under a single heading. REP 835 resists that, and for good reason: the three risks it identifies operate through different mechanisms, affect different parties, and pose different supervisory challenges. A single regulatory response cannot address all three.

When multiple market participants rely on common external service providers, a failure at the provider level creates system-wide exposure. This is not the same as the operational risk any single firm manages internally. It is a supervisory gap: the risk is invisible to any individual firm’s risk framework because it sits at the infrastructure layer beneath them. REP 835 flags that this form of concentration risk can manifest at both the firm and the broader economic level, and no amount of internal risk management at the participant level is sufficient to address it on its own.

AI vendor concentration sits at the centre of APRA’s own systemic risk analysis, where the regulator formally identified single-provider dependencies across banking, insurance, and superannuation as a threat beyond the control of any individual institution, the same logic that underpins ASIC’s REP 835 flagging of shared infrastructure as a supervisory gap no firm-level risk framework can resolve.

Gamified and social trading platforms amplify risks for retail investors through a two-stage mechanism. The first stage is design: features such as streaks, notifications, leaderboards, and social feeds increase time-on-platform and trading frequency. The second stage is behaviour: those design choices produce impulsive trading, herd behaviour, and underweighting of risk, which in turn produce poor investor outcomes.

The regulatory implication is significant. Platform engineering is now a conduct issue within ASIC’s investor protection mandate, because decisions made by design teams have measurable effects on whether you act in your own financial interests.

Frontier AI adoption introduces three specific challenges that REP 835 highlights:

The third challenge is the most consequential. Existing accountability frameworks assume a human decision-maker who can explain their reasoning. When decisions are made by opaque AI systems, that assumption breaks, and the entire architecture of investor protection that depends on attributable responsibility comes under pressure. No jurisdiction has fully resolved this yet.

| Risk category | Mechanism | Who bears it | Supervisory challenge |

|---|---|---|---|

| Concentration risk | Multiple firms sharing common infrastructure providers | System-wide (not captured at firm level) | Invisible to individual firm risk frameworks; requires system-level supervision |

| Gamification and social trading | Platform design features driving impulsive trading behaviour | Retail investors | Platform engineering is now a conduct issue, not just a UX choice |

| Frontier AI | Synchronised AI behaviour, adversarial attacks, opaque decision-making | Market participants, supervisors, affected parties | Accountability frameworks assume a human who can explain their reasoning |

Understanding the risks and opportunities is one thing. Understanding how the regulatory architecture is designed to hold both simultaneously is what gives you the working model.

ASIC’s stated aim in REP 835 is co-evolution: developing market infrastructure and regulation in parallel, rather than reacting to crises after they have occurred. This is an active policy choice with specific tools, not a passive posture of waiting to see what happens.

The response operates at two distinct layers:

These two layers serve different but complementary functions. Cross-border coordination shapes the international environment within which Australian markets operate. Domestic collaboration shapes how that environment is navigated at home. For you, if you operate within or adjacent to Australian financial markets, the rules you work under are being shaped simultaneously by both: local experimentation and global standard-setting are feeding each other.

REP 835’s co-evolution framework does not sit in isolation; ASIC’s regulatory modernisation programme has simultaneously been driving measurable operational change, eliminating approximately 45,000 paper-based submissions annually and expanding electronic lodgement options by 380%, giving you a clearer picture of how the regulator is reshaping its own infrastructure alongside the markets it supervises.

The “false choice” framing from REP 835 ties this together. Innovation and investor protection are not competing objectives. The report’s argument is that well-designed regulatory infrastructure, with clear trial pathways, supervised pilots, and cross-sector engagement, is what enables both simultaneously. Without that infrastructure, the practical outcome is less innovation under supervision, which produces worse outcomes on both dimensions.

The framework exists, and it is well designed. The hard questions are still open.

The opacity and explainability challenge in frontier AI remains unresolved globally, not just in Australia. The standards currently being set through IOSCO and FSB coordination are not finished products but active negotiations, and Australia’s participation in those negotiations matters precisely because the outcome will shape how accountability works across markets for decades.

Project Acacia’s work continues post-report, which tells you the co-evolution process is active, not concluded. The coming period is one where the quality of Australia’s regulatory co-design will determine whether the efficiency gains from DLT and tokenised assets are realised without creating new systemic vulnerabilities.

The way Australia handles these tensions over the coming decade will determine not just how innovative its markets become, but how trustworthy they remain.

For investors wanting to understand the commercial pressures shaping how frontier AI providers operate, our deep-dive into frontier AI business model risks examines the counterparty concentration dynamics that arise when a small number of providers dominate the infrastructure underpinning entire markets.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding regulatory developments and technology adoption are subject to change based on market developments and policy decisions.

Atomic settlement is the simultaneous, real-time exchange of an asset and its payment, eliminating the gap between trade execution and final settlement. Standard settlement models (T+1 or T+2) leave a window of hours or days during which counterparty risk accumulates and capital is locked in margin buffers; atomic settlement closes that window entirely.

ASIC REP 835 is a formal regulatory report mapping how distributed ledger technology, tokenised assets, and artificial intelligence are reshaping Australian financial markets. It identifies specific risks including infrastructure concentration, gamification conduct issues, and frontier AI explainability problems, alongside the frameworks designed to let innovation and investor protection advance together.

Project Acacia is a joint initiative between the Reserve Bank of Australia and the Digital Finance Cooperative Research Centre exploring how digital money functions within wholesale tokenised asset markets. ASIC granted regulatory relief to participants in July 2025, making it a live supervised test of atomic settlement mechanics inside Australia's own financial system.

Gamified platform features such as streaks, leaderboards, and social feeds increase trading frequency and drive impulsive behaviour, producing poor outcomes for retail investors. ASIC's REP 835 formally classifies platform engineering as a conduct issue, meaning design decisions by product teams now fall within ASIC's investor protection mandate.

Existing accountability frameworks assume a human decision-maker who can explain their reasoning; when opaque AI systems make decisions, that assumption breaks down. REP 835 flags this as a structurally unresolved challenge globally, because the entire architecture of investor protection depends on being able to attribute responsibility for decisions.