The US industrial sector returned 17% in 2024 and 19% in 2025, outperforming several higher-profile segments of the equity market in consecutive years. Yet for many retail investors, “industrials” remains a vaguely understood label, somewhere between manufacturing plants and freight trains, without a clear picture of what the sector actually holds or how it behaves across economic cycles.

That knowledge gap matters now more than it has in years. The sector sits at the intersection of infrastructure bill deployment, defence budget expansion, manufacturing reshoring, and the green energy transition, four forces converging simultaneously in the US economy. This guide walks through every practical dimension of the investment decision: the vehicles available, the companies worth understanding, the cyclical risks that have historically punished poorly timed entries, and the structural trajectory that extends through the early 2030s.

What the industrial sector actually covers (and why it matters for US investors)

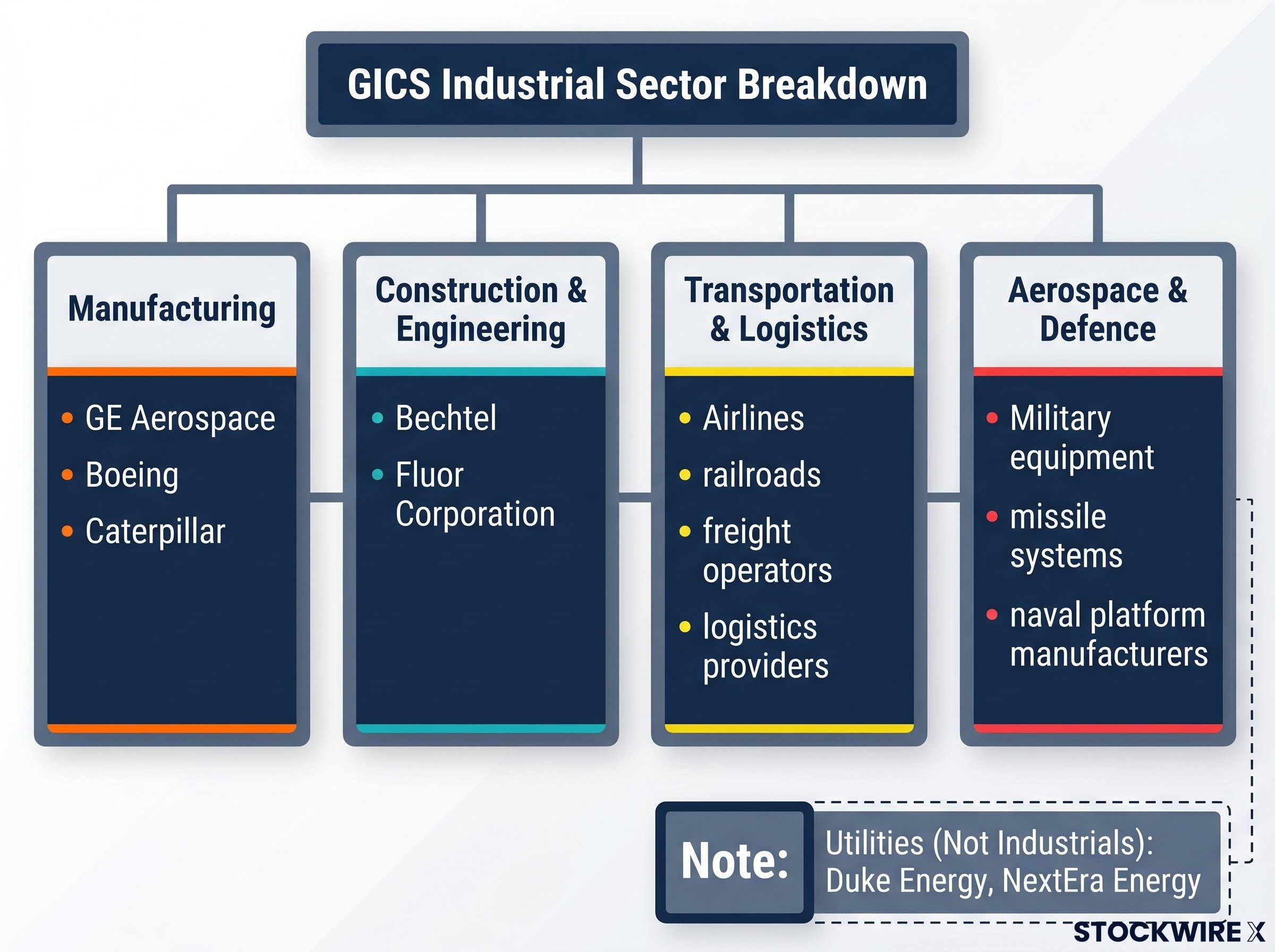

The industrial sector, as defined by the Global Industry Classification Standard (GICS), spans a far broader range of businesses than the word “industrial” might suggest. Its sub-sectors include:

The GICS sector definitions published by MSCI and S&P Global formally classify industrials across three broad groups: capital goods manufacturers, commercial and professional services firms, and transportation companies, a scope considerably wider than the colloquial use of the word industrial.

- Manufacturing: Companies producing aerospace components, heavy machinery, and electrical equipment, including GE Aerospace, Boeing, and Caterpillar

- Construction and engineering: Firms that design and build large-scale infrastructure, such as Bechtel and Fluor Corporation

- Transportation and logistics: Airlines, railroads, freight operators, and logistics providers

- Aerospace and defence: Military equipment, missile systems, and naval platform manufacturers

One common source of confusion involves utilities. Duke Energy and NextEra Energy are technically classified in the GICS Utilities sector, not Industrials, even though their operations overlap with infrastructure themes frequently discussed alongside industrial investments.

The April 2024 spin-off of GE Aerospace from the former General Electric conglomerate reshaped the sector’s composition. GE Vernova now trades separately, covering energy and renewables, while GE Aerospace offers concentrated aviation and defence exposure. Investors holding legacy industrials ETFs saw their underlying holdings shift as funds rebalanced.

The cyclical engine: how economic conditions drive industrial performance

The sector’s performance is tightly coupled to the broader economy. When GDP expands, corporations increase capital expenditure, which in turn drives demand for the machinery, engineering services, and transportation capacity that industrial companies provide. That positive feedback loop works in reverse during contractions, making industrials one of the more volatile sector allocations across a full economic cycle.

Interest rate trajectory plays a direct role in this dynamic. Easing rate cycles have historically favoured capital-goods and transportation names, as lower borrowing costs encourage the large capital investments these companies depend on. Prolonged higher rates compress valuations in capital-intensive segments by raising financing costs and discouraging expansion.

When big ASX news breaks, our subscribers know first

The investment vehicles available for industrial sector exposure

Four primary access points exist for US investors considering an industrials allocation, each suited to a different combination of knowledge, risk tolerance, and portfolio objective.

| Vehicle Type | Example | Diversification | Typical Cost | Best Suited For |

|---|---|---|---|---|

| ETF | XLI, VIS | Broad sector | Low (0.09-0.10% expense ratio) | Most retail investors seeking diversified exposure |

| Individual equities | CAT, BA, GE Aerospace | Single company | Brokerage commission only | Investors with company-level conviction |

| Mutual funds | Sector-benchmarked funds | Broad sector | Moderate (0.50-1.00% expense ratio) | Investors preferring active management |

| Industrial bonds | Issuer-specific corporate bonds | Single issuer | Varies by issue | Income-focused investors with credit analysis capability |

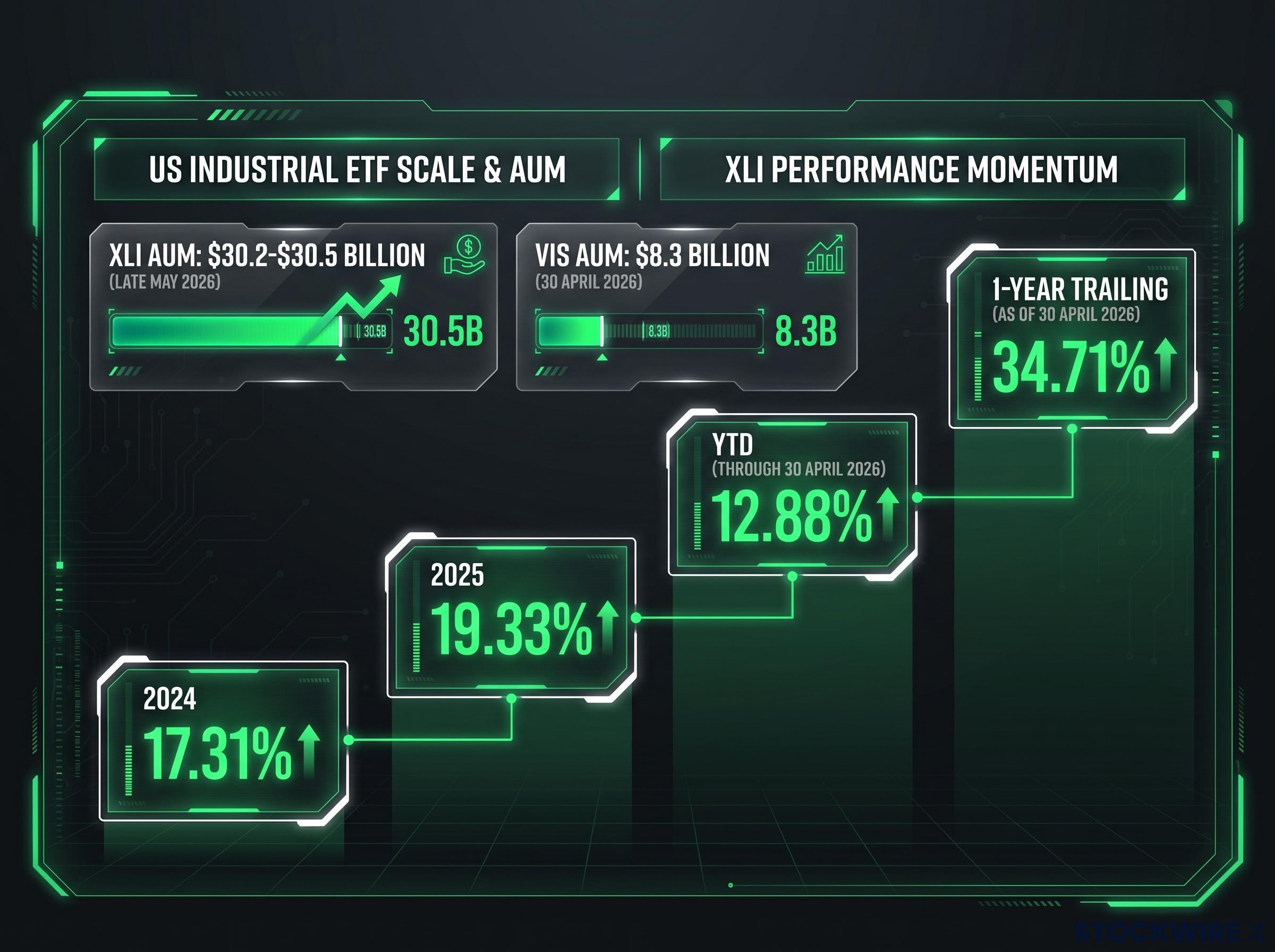

ETFs represent the most practical starting point for most retail investors. The Industrial Select Sector SPDR Fund (XLI) held approximately $30.2-$30.5 billion in assets under management as of late May 2026, making it one of the largest and most liquid US industrials ETFs. The Vanguard Industrials ETF (VIS) held total net assets of approximately $8.3 billion as of 30 April 2026, with particular alignment to US reshoring and infrastructure themes.

Investors approaching the industrials sector without a prior framework for vehicle selection, risk tolerance, or fee comparison will find that investing basics, including how to match an account type and cost structure to a specific goal, determine outcomes before any sector decision is made.

XLI’s track record illustrates the sector’s recent momentum: a full-year 2024 return of 17.31%, a full-year 2025 return of 19.33%, and a year-to-date return of 12.88% through 30 April 2026.

Individual equities offer concentrated exposure for investors with company-level conviction, while industrial bonds provide income with lower volatility, though they require credit analysis at the issuer level.

Key companies to know before investing in industrials

Not all industrial names carry the same risk profile. Understanding the meaningful differences between a clean cyclical play and a company carrying idiosyncratic risk determines whether an investor’s sector allocation behaves the way they expect.

- GE Aerospace: Following the April 2024 spin-off, the company provides concentrated commercial and military aviation exposure. Primary risk centres on engine production ramp timelines and aftermarket service demand cycles.

- Caterpillar: The cleaner cycle play on infrastructure and mining demand. Elevated order backlogs through 2024-2025 reflected ongoing infrastructure and mining spending, with some dealer inventory normalisation. Ongoing share repurchases and dividends reflected strong cash generation. Primary risk variables are interest rate sensitivity and commodity price fluctuations.

- Boeing: Carries the sector’s most prominent idiosyncratic risk.

Boeing’s regulatory situation: A January 2024 mid-air incident involving a 737 MAX 9 panel blowout triggered FAA production caps, delivery delays, cash-flow pressure, and management changes throughout 2024-2025. The episode illustrates how regulatory risk can create company-specific volatility that diverges sharply from broader sector performance.

Boeing’s challenges matter even for ETF investors. Because XLI and similar funds hold concentrated positions in large-cap industrials, stock-level risks in Boeing flow through to fund performance.

Construction, engineering, and defence: the less-discussed but structurally supported sub-sectors

Bechtel and Fluor Corporation provide exposure to the construction and engineering segment, where Infrastructure Investment and Jobs Act (IIJA) deployment timelines extend project visibility into 2026-2027. These names receive less attention than manufacturing giants but benefit directly from government-funded infrastructure programmes.

The defence manufacturing sub-sector is supported by multi-year US budget growth in aerospace, missiles, and naval platforms. Unlike private-sector cyclical demand, defence spending operates on multi-year procurement timelines that provide order visibility well beyond typical business cycles.

Understanding the risks that drive industrial sector cycles

The industrial sector’s cyclical character is its defining feature from a risk perspective. Because sector performance tracks GDP expansion and capital expenditure cycles closely, an economic contraction hits industrials harder and faster than defensive sectors such as utilities or consumer staples. That core cyclicality is the foundation, but five external variables amplify or dampen the cycle in ways investors can identify and monitor.

- Interest rates: A faster Federal Reserve easing path benefits capital-goods and transportation names by lowering borrowing costs for large capital projects. Prolonged higher rates compress valuations in capital-intensive segments.

- Commodity prices: Rising input costs squeeze margins for manufacturers, while elevated commodity prices simultaneously boost demand for mining and extraction equipment.

- Trade and tariff policy: Boeing and Caterpillar face headline risk from tariff escalation and retaliatory trade actions, given their significant international revenue exposure.

- Geopolitical conditions: Supply chain disruptions and regional conflict affect both demand patterns and input availability across transportation and manufacturing sub-sectors.

- Regulatory environment: Boeing’s FAA production cap situation demonstrates how regulatory developments can create idiosyncratic volatility within an otherwise macro-driven sector.

Tariff escalation affecting Boeing and Caterpillar operates through two channels simultaneously: direct cost increases on imported components and retaliatory measures from trading partners that close export markets, with the US average tariff rate now at approximately 9.6%, the highest level in roughly 80 years, creating a structural headwind that differs from the episodic trade disputes of prior cycles.

| Risk Factor | What Triggers It | Most Exposed Sub-Sectors |

|---|---|---|

| Economic contraction | GDP decline, falling business confidence | All sub-sectors, particularly capital goods |

| Rising interest rates | Fed tightening, persistent inflation | Construction, capital-intensive manufacturing |

| Commodity price swings | Supply disruptions, demand shifts | Heavy equipment, mining services |

| Tariff escalation | Trade policy changes, retaliatory measures | Aerospace exports, heavy equipment |

| Geopolitical disruption | Regional conflict, supply chain fractures | Transportation, logistics, defence |

| Regulatory action | Safety incidents, compliance failures | Aerospace manufacturing (e.g., Boeing) |

Structural offset: IIJA deployment was described as moving into its “middle innings” in early 2025, with increased bid activity for construction, engineering, machinery, and building materials extending visibility into 2026-2027. Government fiscal programmes provide multi-year order visibility that can partially cushion private-sector cyclical pressure.

Industrial sector losses during downturns are not random. They are structurally predictable and concentrated in identifiable conditions. An investor who can recognise those conditions in advance has meaningful tools to manage timing and position sizing.

For investors wanting to time an industrials allocation to the business cycle rather than entering on conviction alone, our dedicated guide to sector rotation strategy walks through each of the four cycle phases, the Relative Rotation Graph tools used to track real-time institutional flows, and the specific conditions under which cyclical sectors like industrials have historically led recoveries.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The long-term case: where the industrial sector is headed through the early 2030s

Three structural forces are operating simultaneously, and their convergence builds a long-term case that extends well beyond the current cycle.

- Industry 4.0 adoption: Integration of artificial intelligence, Internet of Things (IoT) connectivity, robotics, and digital twins is anticipated to drive operational efficiency gains and productivity improvements across the US manufacturing base through 2030. These technologies allow manufacturers to reduce waste, predict equipment failures, and optimise production in ways that compound over time.

- Infrastructure modernisation and reshoring: US reshoring trends and CHIPS Act incentives are directing capital toward domestic industrial capacity. Construction, engineering, and equipment sub-sectors benefit directly from this shift in where manufacturing facilities are built and how they are supplied.

- Green energy transition: Clean energy infrastructure investment through 2030 is projected to be substantial, supported by federal policy incentives and private capital. Specific numerical forecasts vary by source, but the directional commitment of capital is well documented across industry and government analyses.

Defence manufacturing adds a fourth structural layer. US budget documents and industry analyses project multi-year growth in defence outlays, particularly in aerospace, missiles, and naval platforms.

Near-term catalysts versus decade-long structural forces

IIJA deployment and defence spending represent visible near-term drivers with project timelines extending through 2025-2027. Automation and green infrastructure operate on a longer arc, representing the decade-scale forces most likely to rerate the sector’s earnings power.

An investor with a 5-10 year horizon faces a different calculus than one making a tactical quarterly allocation. The structural tailwinds help distinguish between cyclical setbacks that could represent buying opportunities and fundamental deterioration worth avoiding.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Building an industrials position: practical steps and portfolio considerations for US investors

The decision to invest in industrials follows a specific sequence, and each step narrows the field of options.

- Determine investment horizon: A long-term allocation (5 years or more) aligns with structural tailwinds; a shorter tactical position depends more heavily on cycle timing and rate trajectory.

- Choose the vehicle: ETFs such as XLI (approximately $30.2-$30.5 billion AUM) and VIS (approximately $8.3 billion AUM) provide diversified exposure suited to most investors, while individual equities offer concentrated bets for those with company-level conviction.

- Assess sub-sector weighting: Spreading exposure across manufacturing, construction, defence, and transportation reduces single-sub-sector concentration risk.

- Evaluate geographic exposure: Some US industrials ETFs carry meaningful international revenue exposure through holdings in companies like Boeing and Caterpillar, which affects geopolitical risk even within a nominally “US” fund.

What to monitor after you invest

Post-investment monitoring determines whether to hold, add, or reduce exposure over time. The specific indicators to track include:

- Federal Reserve rate decisions: Rate trajectory directly affects capital-goods valuations and construction-driven demand

- Caterpillar and GE Aerospace quarterly earnings: Both are frequently cited as sector bellwethers whose guidance signals broader capital expenditure trends

- IIJA bid and award activity: Accelerating or decelerating project awards affect construction and engineering order visibility

- Trade policy headlines: Tariff developments create near-term volatility for export-oriented holdings

- Commodity price trends: Input cost movements affect margins across heavy equipment and manufacturing names

Industrials in 2026 and beyond: timing, conviction, and what the data suggests

Performance context: XLI delivered a trailing one-year return of 34.71% as of 30 April 2026. That figure makes the valuation question unavoidable for investors considering a new position today.

Back-to-back returns of 17.31% in 2024 and 19.33% in 2025, followed by 12.88% year-to-date through 30 April 2026, raise a legitimate question: how much upside has already been priced in? XLI’s AUM of approximately $30.2-$30.5 billion reflects sustained institutional and retail interest, confirming that capital has already moved into the sector.

Sector valuation divergence across the US market in 2026 runs deeper than index-level price-to-fair-value ratios suggest; Morningstar’s coverage data shows industrials sitting within a broader mosaic where small-caps carry an 18% discount and consumer defensives a 19% premium, context that sharpens the entry-timing calculus for any new industrials position.

The balanced assessment for a current allocation weighs three structural tailwinds against three active risks:

- Tailwind: IIJA and CHIPS Act deployment extending multi-year order visibility

- Tailwind: Defence budget growth supporting aerospace and naval manufacturing

- Tailwind: Industry 4.0 adoption and reshoring creating decade-scale demand

- Risk: Interest rate uncertainty and the possibility of a prolonged higher-rate environment

- Risk: Tariff escalation affecting Boeing, Caterpillar, and other export-exposed names

- Risk: Boeing’s idiosyncratic regulatory and production challenges affecting ETF-level returns

The sector’s structural tailwinds make a long-term position compelling for investors with the appropriate time horizon. Vehicle selection, sub-sector weighting, and position sizing relative to portfolio risk tolerance remain the variables that determine actual outcome. Recent performance provides context, not a guarantee, and entry timing relative to the economic cycle warrants careful consideration.

These statements are speculative and subject to change based on market developments and company performance.