Immuron Explained: the ASX Biotech Built on Revenue, Not Raises

2 hrs ago

Within two trading days of SpaceX listing on 12 June 2026, two of Australia’s most popular space-sector ETFs quietly transformed from diversified thematic funds into high-conviction SpaceX bets. Most investors holding them had no idea.

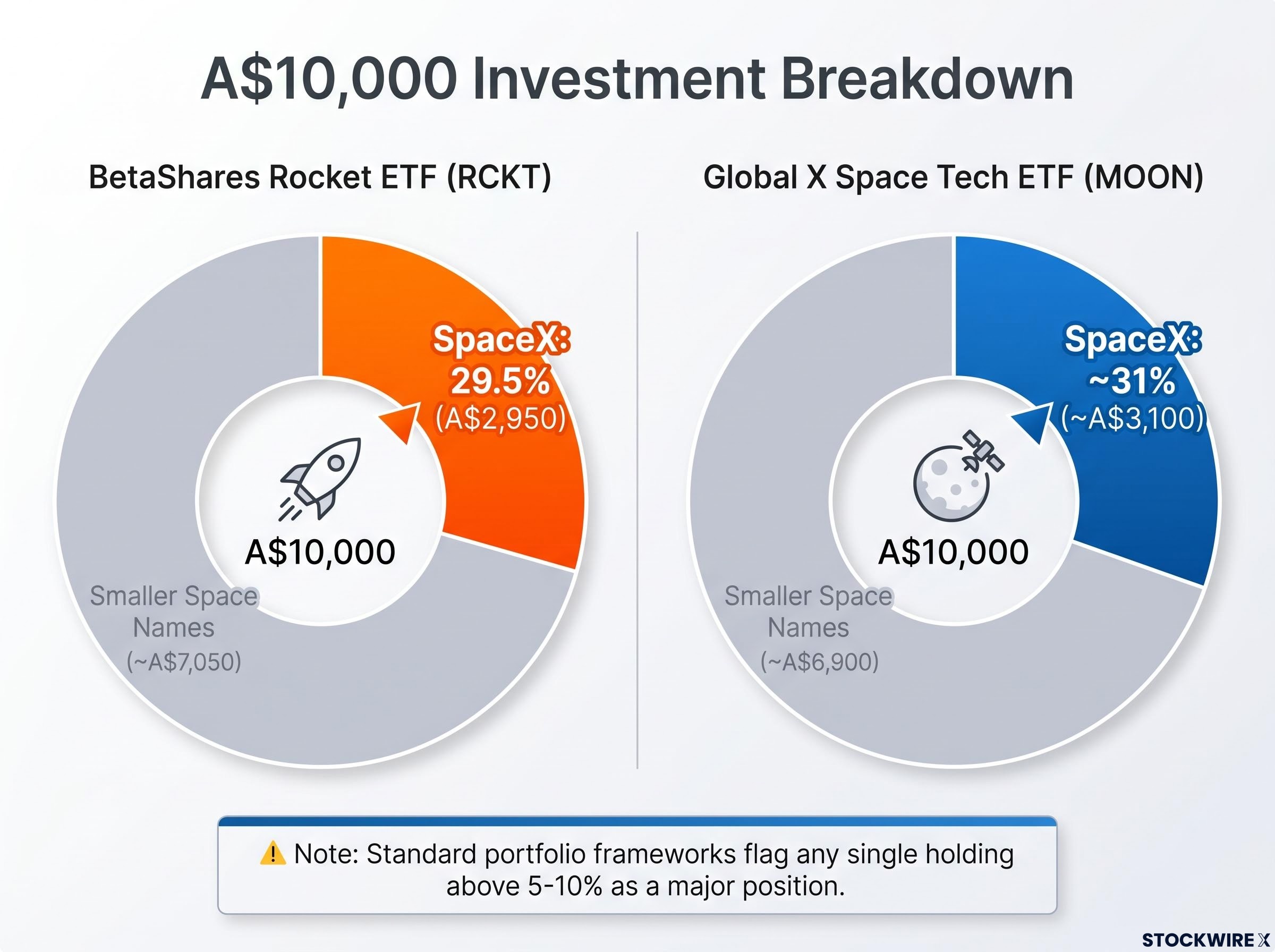

The BetaShares Rocket ETF (ASX: RCKT) and the Global X Space Tech ETF (ASX: MOON) now carry SpaceX as their single largest holding at approximately 29.5% and 31% respectively. For an investor with A$10,000 in either fund, around A$3,000 is now effectively SpaceX. That shift happened automatically, through index mechanics, without a single buy order from the investor.

This article explains exactly how a SpaceX Australian ETF exposure of this magnitude came about, why early IPO pricing adds a layer of risk that direct stock buyers do not face in the same way, and what Australian investors currently holding or considering these funds should do now.

The numbers are blunt. BetaShares’ own holdings disclosure lists Space Exploration Technologies Corp at 29.5% of RCKT. Global X’s MOON carries SpaceX at approximately 31%. In both funds, the next-largest holding sits in single digits.

RCKT’s early risk profile included an annualised volatility estimate of approximately 28% and an analyst recommendation to cap the position at less than 5% of a portfolio, cautions that were published before SpaceX entered the fund and the concentration picture became materially more pronounced.

For context, SpaceX crossed the trillion-dollar valuation threshold at listing on 12 June 2026 and was added to RCKT effective 17 June 2026. Within a week, the fund’s composition had fundamentally changed.

| Fund | ASX Code | SpaceX Weight | Approx. SpaceX Exposure on A$10,000 |

|---|---|---|---|

| BetaShares Rocket ETF | RCKT | 29.5% | A$2,950 |

| Global X Space Tech ETF | MOON | ~31% | ~A$3,100 |

Many portfolio frameworks flag any single holding above 5-10% as a major position requiring explicit review. A 30% weight sits well beyond that threshold.

Fund performance is now driven predominantly by SpaceX’s returns and volatility rather than by the space sector as a theme. The remaining A$7,000 in a A$10,000 holding is spread across a long tail of smaller, often more speculative space names. Investors who have not checked their fund’s holdings page since early June may believe they hold a diversified space-sector basket. That description no longer fits either fund.

This outcome was not a surprise to anyone familiar with how these indices work. It was structurally inevitable. Three steps explain the chain.

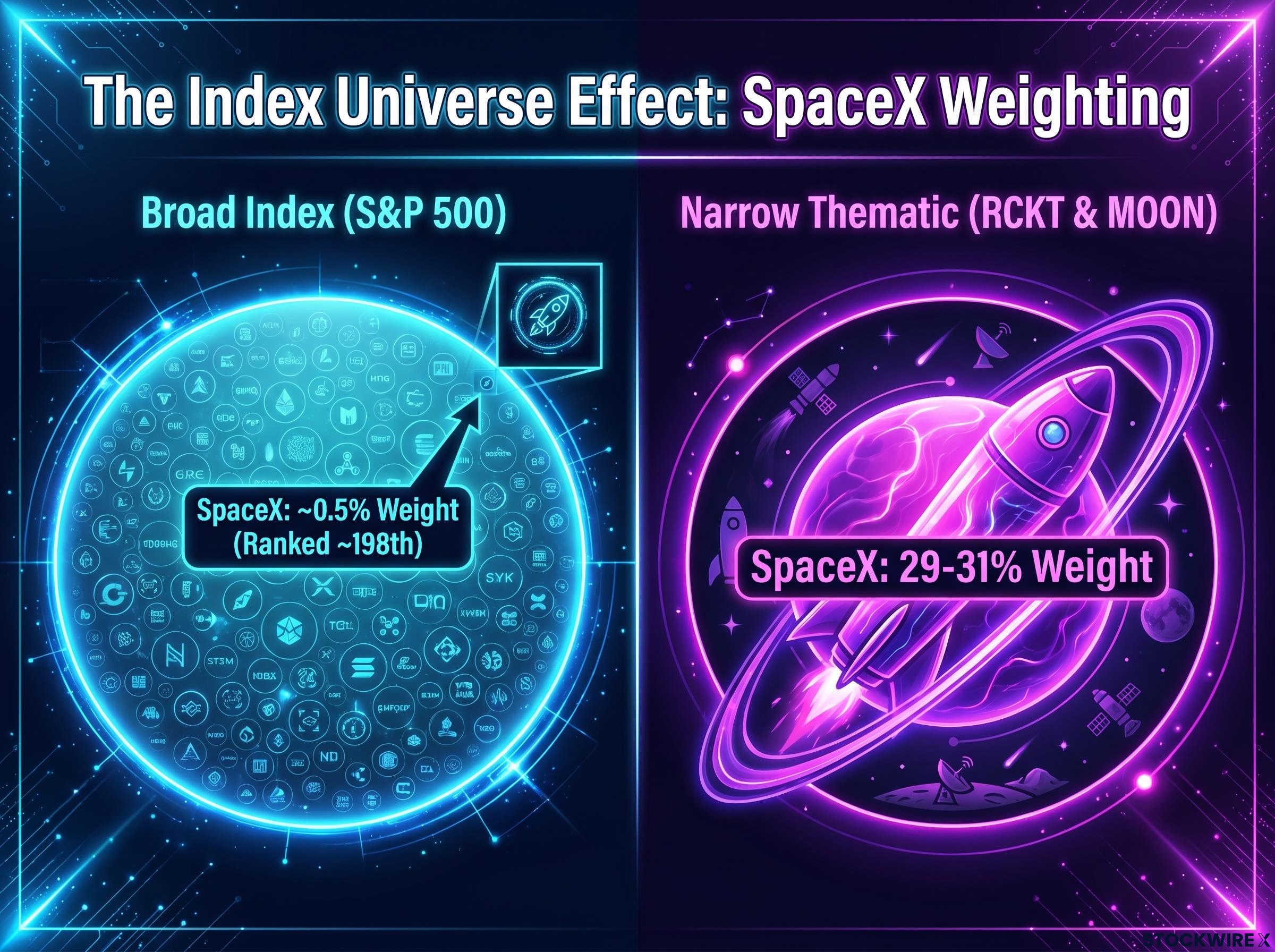

A trillion-dollar company entering a narrow thematic index instantly dominates because there is not enough breadth in the universe to dilute its weight. In a broad index with hundreds of names, SpaceX would be one of many. In a space-sector index with a handful of constituents, it becomes the fund.

SpaceX priced at US$135 per share on 12 June 2026. That figure appeared on screens as a straightforward market price. It was not.

Because insiders, including founders, did not sell heavily into the offering, the initial public float was estimated at approximately 5% of total shares outstanding. A thin order book, scarcity-driven upward pressure, and pent-up demand from investors who could not access the stock pre-IPO produced first-day price action that reflected available supply as much as it reflected fundamental value.

The cost basis at which RCKT and MOON built their SpaceX positions was set in this thin early market. That potential scarcity premium is now embedded in the fund’s effective entry price.

The scarcity premium at IPO is not a feature unique to SpaceX; prediction markets priced the debut above $2 trillion while analyst consensus sat closer to $1.5 trillion, and historical data across marquee listings including Facebook, Uber, and Snap show that the gap between listing-day sentiment and long-run fundamental value has consistently resolved against retail buyers who entered at the moment of peak excitement.

The same stock. Two entirely different risk exposures, determined by universe size and float-adjustment methodology.

Typical IPO lock-up expiries begin approximately 180 days post-IPO, with staged releases thereafter. For SpaceX, this means meaningful additional supply could begin entering the market around late 2026.

An ETF holder whose fund built its SpaceX position at early, float-compressed prices faces direct exposure to any normalisation of that scarcity premium as lock-up periods expire and supply conditions change.

The SpaceX inclusion is a specific case, but the underlying mechanic is general. Any future mega-cap debut in a sector with a dedicated thematic ETF will reproduce this dynamic.

Thematic ETFs track small, focused indices where market-cap weighting has almost no breadth to dilute a large new entrant. This is structurally different from broad indices. The Nasdaq 100, for example, imposes an approximately 15-day waiting period for new IPOs before they can be included. Investors in Nasdaq-100-tracking ETFs therefore had no immediate SpaceX exposure, while RCKT and MOON holders absorbed the full weight from the outset.

The index rules govern what a fund holds and how concentrated it can become. Reading the Product Disclosure Statement (PDS), the document that sets out a fund’s investment strategy and rules, is not optional for thematic ETF investors.

Before purchasing or continuing to hold any thematic ETF, investors should be able to answer three questions from the PDS:

The structural explanation above converts into a specific sequence of actions for current holders.

For investors weighing whether to hold RCKT or MOON against buying SpaceX shares directly through an international broker, our dedicated guide to SpaceX access routes for Australian investors covers the brokerage requirements, currency conversion costs, and secondary market pricing risks that apply to each pathway.

A 15% RCKT allocation within a self-managed portfolio means over 4% of the total portfolio now sits in a single stock that listed six days ago.

Buying RCKT or MOON after SpaceX’s listing is a materially different proposition to buying either fund before June 2026. The new buyer is purchasing approximately 25-30% SpaceX at post-IPO prices that may include a scarcity premium, plus a basket of smaller speculative space names making up the remaining 70-75%.

These funds are now best described as tactical, high-beta satellite positions for investors who are explicitly comfortable with that SpaceX-dominant risk profile. They are not diversified space-sector core holdings.

Three signals that RCKT or MOON may still belong in a portfolio:

Future Nasdaq 100 inclusion, expected after expiry of the approximately 15-day waiting period, will give broad-index ETF investors their own SpaceX exposure. This may create unintended double-counting for investors holding both broad and thematic ETFs simultaneously.

The structural lesson travels well beyond a single IPO. Thematic ETF portfolios can change their fundamental character within days when a dominant sector player reaches public markets. The shift from “diversified space basket” to “SpaceX fund with extras” occurred within two trading sessions.

Any major IPO in a sector with a dedicated thematic ETF, whether in biotech, defence, or artificial intelligence, will reproduce this dynamic. The speed of transformation will always catch investors who are not monitoring holdings disclosures actively.

Thematic ETF concentration risk has played out repeatedly across the Australian market in 2026, with technology-themed funds falling by up to 25% during the same period that resources and energy ETFs delivered triple-digit returns, a pattern that illustrates how narrow thematic mandates amplify sector-specific drawdowns when leadership rotates.

Periodic review of fund composition is a basic discipline for any investor using thematic ETFs. The fund held last quarter may no longer resemble the fund held today.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. ETF composition and weightings are subject to change based on index rebalancing and market conditions.

SpaceX Australian ETF exposure refers to the indirect ownership of SpaceX shares through ASX-listed thematic funds. The BetaShares Rocket ETF (RCKT) and the Global X Space Tech ETF (MOON) are the two primary affected funds, now carrying SpaceX as their largest single holding at approximately 29.5% and 31% respectively.

SpaceX was automatically added to the Solactive Space Industry Index, which RCKT tracks, effective 17 June 2026 following its listing on 12 June 2026. Because thematic indices cover a narrow universe of stocks, SpaceX's trillion-dollar market capitalisation instantly dominated the index weighting, and the ETF managers built their positions ahead of the official inclusion date, meaning the weight appeared virtually overnight for retail holders.

For every A$10,000 invested in RCKT, approximately A$2,950 is now effectively SpaceX exposure; for MOON, the figure is approximately A$3,100. Investors should multiply their total holding value by the respective weight (29.5% for RCKT, 31% for MOON) to calculate their look-through SpaceX dollar exposure.

Investors should calculate their look-through SpaceX dollar exposure, assess whether that concentration is appropriate for their total portfolio and risk tolerance, check the current PDS for the operative weight cap and next quarterly rebalance date, and consider whether holding SpaceX directly through an international broker would give better control over position size and exit timing than holding it through the ETF.

The difference is entirely due to universe size and index methodology. In the S&P 500, SpaceX's weight is diluted across hundreds of constituents, ranking it approximately 198th at listing. In a narrow space-sector index with only a handful of stocks, the same market capitalisation has almost no breadth to dilute it, making SpaceX the dominant holding by a wide margin.