An investor who bought Zip Co at $0.08 and held as the stock climbed past $14 had every reason to feel vindicated. The entry thesis was correct. The buy-now-pay-later wave was real. Yet many who rode the full cycle ended up with a fraction of what those who sold at $3 actually banked. The entry was identical; the outcome was not. Australian small-cap markets are structurally different from their large-cap counterparts in ways that make selling harder: thin liquidity, extreme price volatility, narrative-driven momentum, and the absence of institutional process for most retail participants. Across 2024 and 2025, behavioural finance research and commentary from ASX fund managers have increasingly identified the sell decision as the single most neglected element of investor process. What follows is an examination of why disciplined selling is so difficult, what the most effective Australian small-cap managers actually do, and how retail investors can build a structured exit approach before they ever place a buy order.

The buy obsession that quietly destroys small-cap returns

The pattern is familiar. Weeks of research go into finding the right stock: screening, reading annual reports, listening to management calls, mapping out the bull case. Then, at the moment of purchase, the exit plan amounts to something close to “I’ll know when it’s time.”

Ben Rundle of Hayborough Investment Partners frames this imbalance directly.

“The biggest mistakes in small caps come from not having an exit mapped out before you buy, letting a 3-bagger turn back into a 1-bagger because you fell in love with the story.”

Forager Funds CIO Steve Johnson has made a parallel observation. In the firm’s February 2025 quarterly report, Johnson noted that Forager’s best contributors share “one common thread: we sold when everyone else still wanted to buy,” having exited several small caps after outsized re-ratings, even when the stories still sounded compelling.

The distinction matters in terms of time-weighted returns: a 100% gain captured in 12 months is a fundamentally different outcome from the same gain over 36 months. Exit timing is itself a form of alpha generation. Professional managers maintain a continuous pipeline of new ideas, which creates structural pressure to redeploy capital. Most retail investors lack this pipeline, and without it, the default is to hold, waiting for a feeling rather than a signal.

When big ASX news breaks, our subscribers know first

Why the brain fights you when it is time to sell

The reluctance to sell is not a character flaw. It is a set of cognitive patterns that fire predictably at the moment of decision, and understanding them is the first step toward designing a process that overrides them.

Three psychological traps dominate:

- The disposition effect: Investors are systematically more likely to sell winners than losers, which is the opposite of what rational capital allocation requires. Profitable positions get cut to “lock in gains” while losing positions are held in hope of recovery.

- Loss aversion and anchoring: A stock down 60% from its purchase price feels like it still holds value because the purchase price serves as a psychological anchor. This is particularly destructive when a small-cap narrative deteriorates gradually rather than collapsing in a single event.

- Regret aversion: The mirror-image trap. Investors vividly imagine the pain of selling before a further 50% rally, even when the risk-reward has shifted materially against them. The possibility of future regret overrides the probability of current loss.

A 2024 working paper from UNSW and the University of Sydney, examining CHESS and brokerage data on Australian retail investors, found the disposition effect “especially pronounced in small-cap and speculative growth stocks,” where investors “anchor on peak prices and are reluctant to realise losses after large drawdowns.”

Peer-reviewed disposition effect research across retail markets confirms the bias is not only universal but intensifies in markets characterised by higher volatility and lower institutional participation, conditions that describe the ASX small-cap segment with particular precision.

The combined effect produces a paradox. Loss aversion and herding cause investors to hold during gradual deterioration, then sell in a panic at the worst moment after a sharp drawdown. The sell decision is made, but only after the damage is done.

The interaction between cognitive biases in volatile markets is rarely linear: loss aversion and herding do not fire in sequence but compound simultaneously, which is why retail investors who successfully resist panic selling in the first days of a drawdown often capitulate at precisely the point where the damage is irreversible.

Behavioural finance consultant Simon Russell has proposed a structural countermeasure: the implementation intention, a pre-written if-then rule designed before the emotional moment arrives.

“If the thesis is broken (earnings downgrade, management departure), then I will cut the position regardless of the share price.”

Writing down the exit process reduces emotional interference at the moment it matters most. The rule does the work so the investor does not have to.

What disciplined exit actually looks like: frameworks from Australian fund managers

No single exit rule is universal. What separates professional managers from reactive sellers is that their rules are pre-committed, specific, and acted upon consistently. The range of approaches spans valuation-based, catalyst-based, time-based, and thesis-break triggers.

The Perennial small-cap team’s “pre-mortem” discipline stands out as particularly actionable for retail investors: at the moment of purchase, write down three sell triggers covering thesis break, valuation stretch, and adverse capital allocation by management. The act of writing forces specificity that vague intention never achieves.

Staged profit-taking and wholesale exit approaches both appear across top-performing managers. Wilsons Advisory favours taking profits at +30%, +50%, and +100% from entry when liquidity permits, particularly after sharp one-day moves around results. NAOS Asset Management prefers a cleaner framework: sell when the key catalyst identified at purchase has been realised, even if it arrives earlier than expected. Both are valid; neither works without pre-commitment.

Luke Laretive of Seneca Financial Solutions captures the philosophical anchor: the team is “happy to leave the last 20-30% of potential upside to someone else” once the identified catalysts have played out.

| Manager / Firm | Trigger Type | Specific Rule |

|---|---|---|

| Ben Rundle, Hayborough | Position size / time | Trim above 7-8% of portfolio; reassess if catalyst not playing out within 18-24 months |

| Steve Johnson, Forager | Valuation re-rate | Sell into 30-50% earnings-surprise moves when PE bakes in bull case |

| Marcus Burns, Spheria | Valuation ceiling | Trim at intrinsic value or above 20x normalised earnings; exit when upside is less than 10% over 3 years |

| NAOS Asset Management | Catalyst realisation | Sell when identified catalyst (contract win, capital event) has been realised, even if early |

| Wilsons Advisory | Staged profit-taking | Take profits at +30%, +50%, +100% after sharp moves |

| Perennial | Pre-mortem triggers | Three written sell triggers at purchase: thesis break, valuation stretch, adverse capital allocation |

| Luke Laretive, Seneca | Catalyst completion | Exit once key catalysts are done; leave last 20-30% of upside to others |

Zip Co and the anatomy of a round-trip

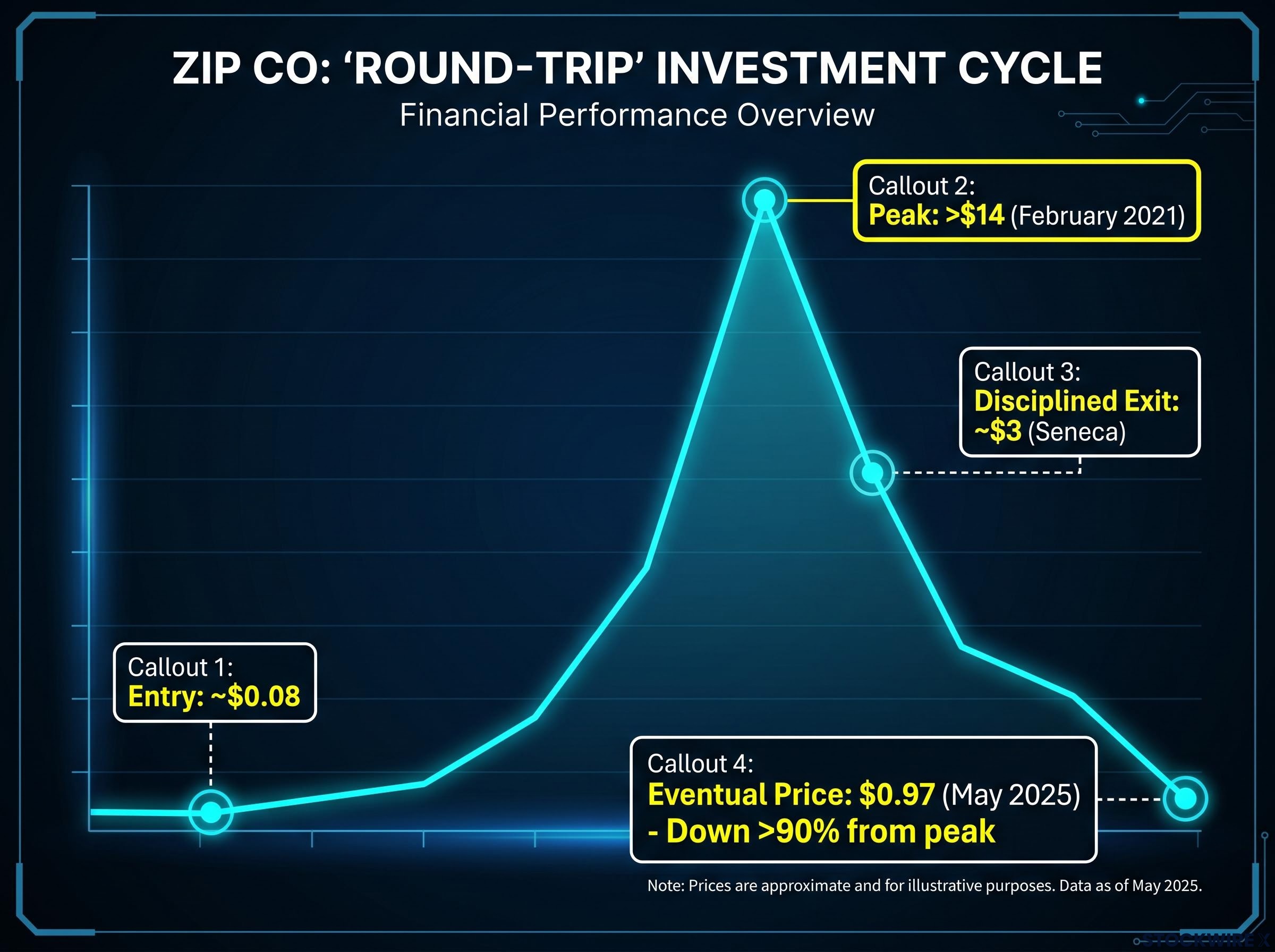

The arc is worth tracing in full. Early investors entered Zip Co around $0.08. The buy-now-pay-later narrative gathered force through 2020, and by February 2021 the stock had climbed past $14. Then it unwound. By 12 May 2025, Zip Co closed at $0.97, down more than 90% from its peak.

The entry thesis was sound. The sector was real, the growth was real, and the market validated the position for over a year. What separated outcomes was entirely the exit.

Seneca’s Luke Laretive has cited Zip as a case where selling discipline converted theoretical wealth into realised returns. Seneca entered at approximately $0.08 and exited around $3. The stock had peaked above $14 during the holding period, but the team had identified their catalysts, watched them play out, and sold. They left substantial upside on the table and still turned a correct entry into a confirmed multi-bagger.

Investors who held through the full cycle, waiting for the narrative to deliver more, watched the same entry point produce a fundamentally different result.

- Entry: approximately $0.08 for early investors

- Peak: above $14 in February 2021

- Disciplined exit window: around $3 (Seneca’s realised exit)

- Eventual price: $0.97 by May 2025

“BNPL names including Zip and Afterpay are reminders that when valuations detach from reality, having a pre-defined sell discipline is more important than finding the next hot theme,” Forager Funds noted in a 2024 review of past technology investments.

Zip is not an outlier. It is a template for how small-cap narratives inflate and deflate, and how identical entry points produce radically different outcomes depending solely on selling discipline.

Narrow windows and illiquid markets: executing the exit when conditions allow

In ASX small caps, catalyst events create narrow windows that close within hours or days, not weeks. A takeover bid, a drill result, an earnings surprise, a regulatory approval: each produces a spike in both price and volume that may represent the only liquid exit opportunity for months.

Four catalyst types illustrate the pattern:

- Takeover and M&A announcements: ASX micro-cap takeover bids in 2024 produced 20-40% one-day spikes, according to a Stockhead review, with investors who sold into the first or second day of exuberance typically locking in better risk-adjusted outcomes than those who waited months for deal completion.

- Earnings surprises: Wilsons Advisory reported that ASX small-cap tech stocks posted 30-50% one-day moves during the 1H FY25 results season, and the firm used the post-result spike to reduce or exit positions where the re-rating left limited further upside.

- Drill results: Multiple junior explorers saw 100-200% intraday spikes on drill hits in 2024, only to give back the majority of gains over following weeks as enthusiasm faded. Investors with pre-defined exits (selling half at +100%) captured materially higher realised returns.

- Regulatory approvals: ASX small-cap biotech names surged 40-80% on TGA or FDA-related announcements in 2024, then retraced once the immediate catalyst passed. Managers interviewed by Livewire noted they “pre-commit to exit or heavily reduce positions into the approval rally,” recognising that both liquidity and sentiment are transient.

The liquidity trap compounds this. Some positions can only be exited during a brief spike in trading volume around a catalyst. Investors who wait for certainty may find themselves unable to sell without moving the price against themselves. A position sized for a liquid large cap but held in an illiquid small cap becomes a forced hold if the thesis deteriorates outside a catalyst window.

ASX small-cap illiquidity creates a specific asymmetry that compounds this problem: price moves during a catalyst window are often amplified by thin order books rather than genuine fundamental reassessment, which means the spike that represents the exit opportunity may be partly a liquidity artefact that disappears within days as order flow normalises.

Position sizing and exit planning are not separate decisions. They are two sides of a single judgement that must be made before the buy order is placed.

Selling is part of the thesis, not an afterthought

The argument reduces to a single principle: the decision to buy a small-cap stock is incomplete until the conditions for selling have been written down. Buying and selling are not sequential steps; they are a single integrated decision. The quality of the exit plan determines whether a correct fundamental thesis translates into a realised return.

A practical starting framework requires four elements documented at purchase:

- Catalyst identification and timeframe: What specific event is expected to close the valuation gap, and within what period? Rundle’s 18-24 month benchmark provides an anchor for reassessment if the catalyst has not materialised.

- Upside threshold for exit: At what valuation level does remaining upside become insufficient to justify continued holding? Burns’s framework of exiting when upside falls below 10% over three years offers a quantitative reference point.

- Thesis-break condition: What single development (earnings downgrade, management departure, regulatory failure) triggers an unconditional exit regardless of share price? Simon Russell’s implementation-intention structure, the pre-written if-then rule, provides the psychological mechanism that makes this work under pressure.

- Position sizing relative to liquidity: How large is this position relative to the stock’s average daily volume, and can it realistically be exited during a catalyst window without materially moving the price?

Thesis-break classification is harder in practice than in principle because narrative deterioration in small caps is rarely binary: a contract loss, a management departure, or a regulatory delay each represent different degrees of thesis impairment, and the discipline of sorting them into irrational overreaction, temporary setback, or structural disruption before acting prevents the most costly category error of selling a temporarily impaired business at its lowest point.

What separates professional from retail outcomes in Australian small caps is not stock-picking skill. It is the discipline to act on a pre-written plan at the moment when emotion is pulling in the opposite direction.

For investors who want to translate these sell-side disciplines into a complete portfolio framework, our comprehensive walkthrough of foundational investing strategies for Australian investors covers pre-commitment structures, ASX stock selection criteria, and the CGT implications of panic selling for both individual and SMSF investors, including how the 50% CGT discount changes the calculus on timing decisions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

—