A $2.1 trillion market is growing fast. Regulators at the Federal Reserve, the International Monetary Fund (IMF), the Bank for International Settlements (BIS), and the Office of Financial Research (OFR) are all watching it closely. The concern is not a wave of defaults. It is something quieter: a structural mismatch between when investors can ask for their money back and when that money can actually be returned.

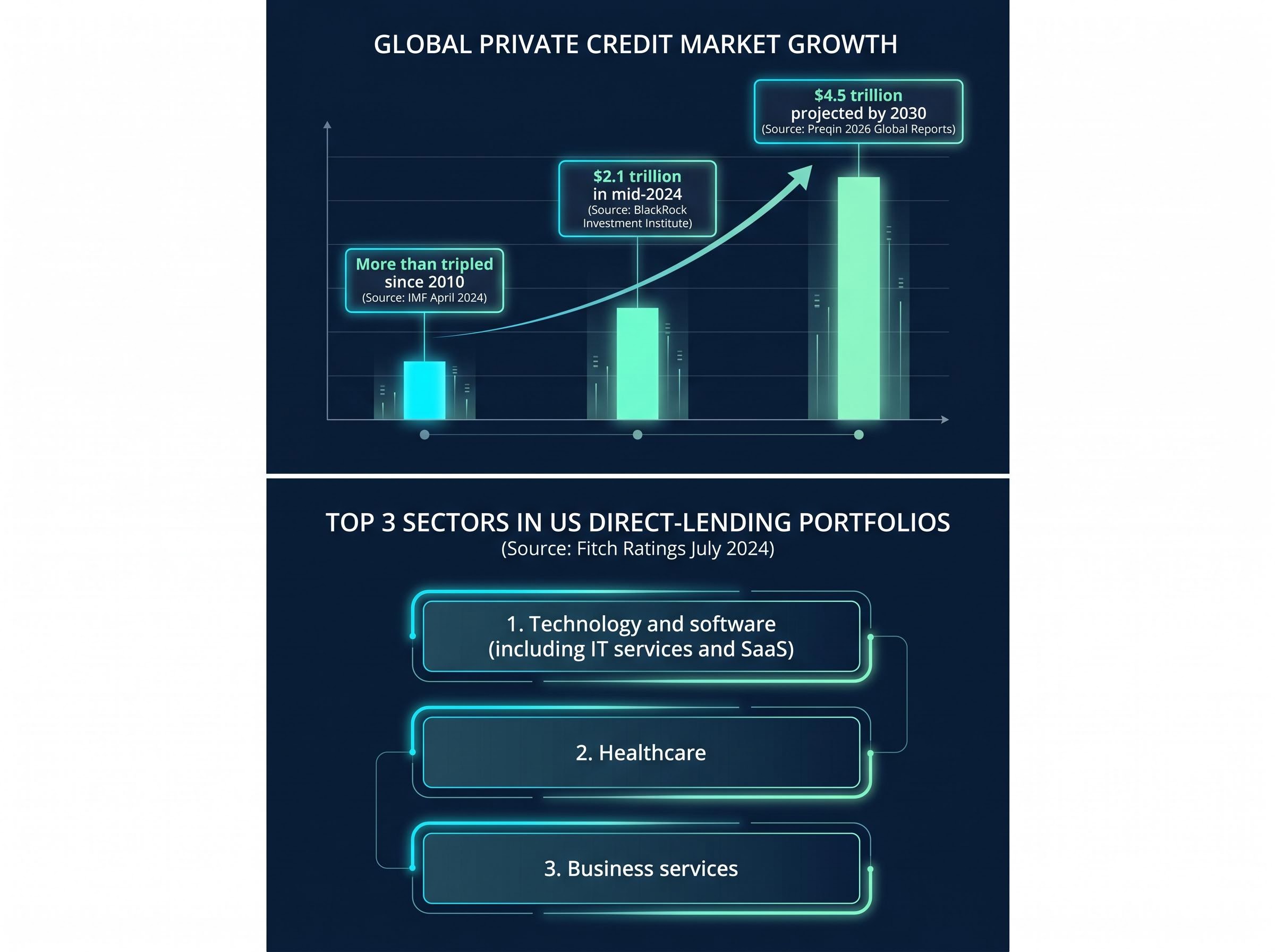

Private credit has more than tripled in size globally since 2010, with the United States as the dominant market. As semi-liquid vehicles and interval funds have brought this asset class to a broader investor base, the question of what happens during stress has moved from academic to urgent. Fisher Investments has identified this liquidity mismatch as the primary systemic concern, one that surpasses fears of outright catastrophic losses.

What follows explains the mechanics of that mismatch, why software and SaaS (software-as-a-service) concentration inside private loan portfolios matters, how a private credit stress event could spill into public equity markets, and why the risk is currently contained but warrants close monitoring.

The $2.1 trillion market hiding in plain sight

The figure is striking on its own. According to the BlackRock Investment Institute, global private credit assets under management reached approximately $2.1 trillion as of mid-2024. Preqin’s 2026 Global Reports project that number will reach roughly $4.5 trillion by 2030.

The market exists because banks left a gap. After the Global Financial Crisis, regulatory pressure forced traditional lenders to retreat from middle-market lending. Private credit funds stepped in, becoming the dominant source of financing for sponsor-backed buyouts in the US. The IMF’s April 2024 Global Financial Stability Report confirmed private credit had more than tripled since 2010, with North America as the clear centre of gravity.

What distinguishes the composition of these portfolios from public loan and bond indices is sector concentration. According to Fitch Ratings, US direct-lending portfolios are “overweight” in technology compared with their public-market counterparts. The three sectors most heavily represented are:

- Technology and software (including IT services and SaaS)

- Healthcare

- Business services

Fitch Ratings (July 2024): “Technology, including software and IT services, represents a large share of new-issue volume for private credit funds,” with US direct-lending portfolios carrying meaningfully greater technology weight than public loan and bond indices.

Understanding this size and composition is the prerequisite. Without it, the risks that follow lack a foundation.

When big ASX news breaks, our subscribers know first

What liquidity mismatch actually means (and why it is not the same as default risk)

Most readers arrive at the topic of private credit risk with a straightforward assumption: the danger is that borrowers stop paying. That is default risk, and it is real, but it is not the structural concern keeping regulators up at night.

The deeper vulnerability is a timing problem. Some private credit vehicles, particularly interval funds and semi-liquid structures, allow investors to request redemptions on a periodic schedule (quarterly, for example). The underlying loans, however, cannot be sold quickly. They are bespoke, bilateral agreements with no active secondary market. This gap between investor liquidity expectations and asset liquidity reality is the mismatch.

The distinction matters because not all private credit vehicles carry this risk equally. Closed-end business development companies (BDCs), which are publicly listed entities that invest in private loans, do not offer frequent redemption windows and therefore face less redemption pressure. Interval funds and semi-liquid vehicles, which promise periodic liquidity while holding the same illiquid loans, are where the mismatch concentrates.

| Attribute | Closed-end BDCs | Interval / semi-liquid funds |

|---|---|---|

| Investor liquidity terms | Trade on exchange; no redemption window | Periodic redemption (quarterly or monthly) |

| Redemption flexibility | Sell on secondary market at market price | Submit redemption request to fund manager |

| Liquidity mismatch risk | Lower | Higher |

| Regulatory concern level | Moderate | Elevated |

The Federal Reserve’s April 2024 Financial Stability Report drew this distinction explicitly, noting that the liquidity concern is greater for interval funds and private credit funds offering periodic redemptions than for closed-end BDCs.

When redemptions spike: gates, queues, and the assets that get sold first

When redemption requests exceed available cash, a fund manager faces a binary decision: restrict withdrawals or liquidate something.

Restricting withdrawals means gating the fund, capping how much investors can take out in a given period. The Federal Reserve’s October 2024 report referenced gated redemptions in credit and real-estate funds as established precedent. Blackstone Real Estate Income Trust (BREIT) and Starwood Real Estate Income Trust (SREIT) both enforced redemption gates into 2024 after sustained withdrawal pressure, and regulators at the Fed and IMF cite these as structural analogues for private credit vehicles.

The alternative, liquidation, creates its own problem. Private loans cannot be sold easily. The assets a manager can sell quickly are the liquid holdings it keeps as a buffer: public bonds and equities. The OFR’s March 2024 brief identified “sudden increases in margin calls or withdrawal requests that require selling more-liquid assets” as the core amplification channel. Fisher Investments has reported that, as of May 2026, investor redemption requests in some private vehicles have reportedly not been fulfilled promptly.

The danger, then, is not that borrowers default. It is that a fund’s structure forces it to sell the wrong assets at the wrong time.

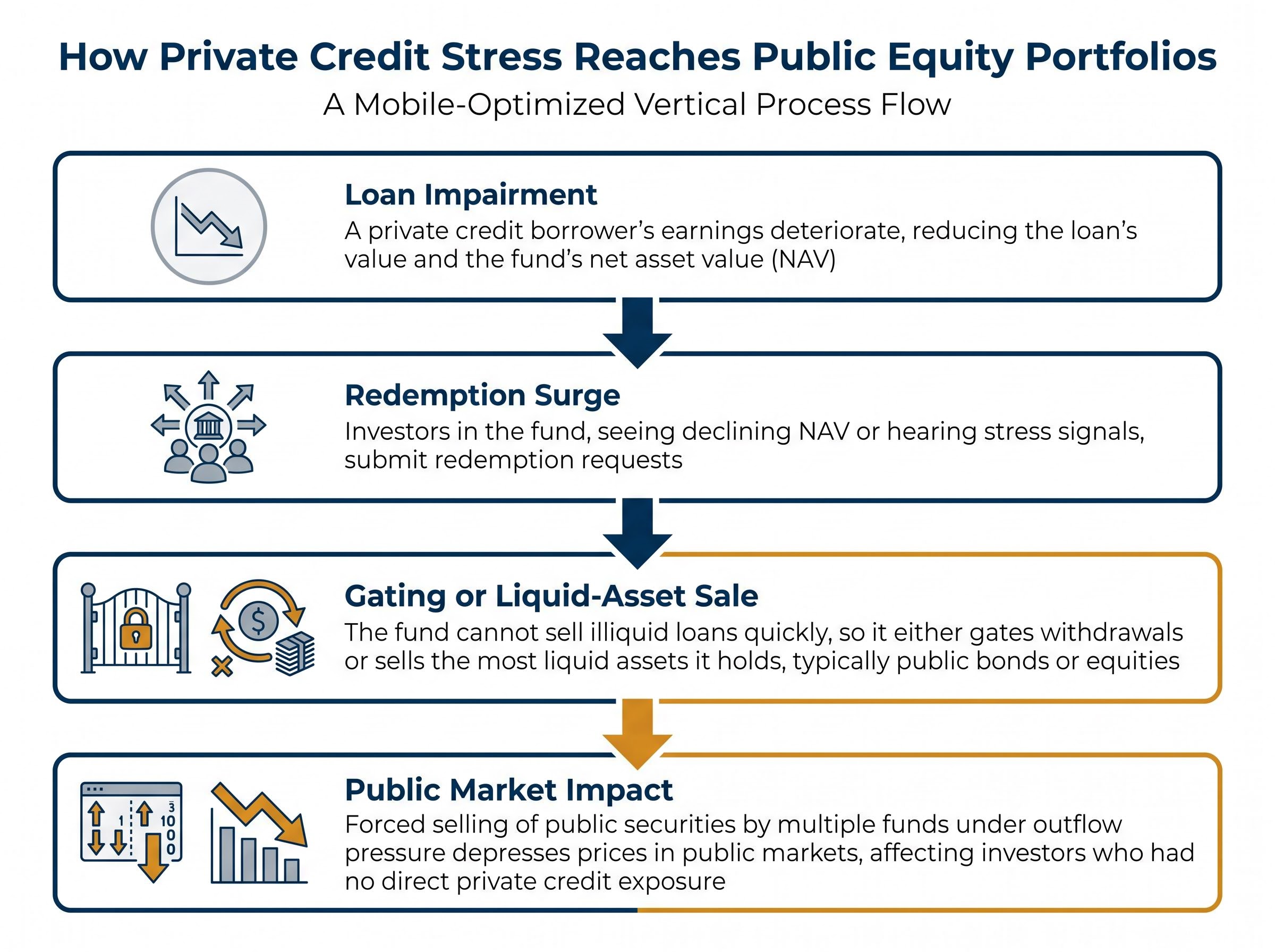

How private credit stress reaches your public equity portfolio

The connection between a private loan souring and a public stock falling is not intuitive. It requires following a four-step chain:

- Loan impairment: A private credit borrower’s earnings deteriorate, reducing the loan’s value and the fund’s net asset value (NAV).

- Redemption surge: Investors in the fund, seeing declining NAV or hearing stress signals, submit redemption requests.

- Gating or liquid-asset sale: The fund cannot sell illiquid loans quickly, so it either gates withdrawals or sells the most liquid assets it holds, typically public bonds or equities.

- Public market impact: Forced selling of public securities by multiple funds under outflow pressure depresses prices in public markets, affecting investors who had no direct private credit exposure.

This is not a speculative chain. The IMF’s April 2024 Global Financial Stability Report provided empirical evidence from past stress episodes showing that open-ended funds holding illiquid assets sold relatively more liquid assets first to meet redemptions. The BIS Quarterly Review from March 2024 corroborated this, documenting that during prior bouts of stress, funds holding illiquid assets disproportionately sold listed, more-liquid instruments first, and explicitly extrapolated this mechanism to private credit funds holding public securities as liquidity buffers.

As of mid-2026, no named US corporate private credit fund has publicly disclosed a stress episode in which private loan impairments directly forced selling of public equities. The structural conditions for it to occur, however, are strengthening as semi-liquid vehicles grow in prevalence. Fisher Investments has identified the possibility that holders of impaired private assets may be forced to liquidate liquid public assets to cover losses as the main systemic concern.

What regulators are actually watching

Four institutional bodies have flagged this mechanism in formal publications: the Federal Reserve (April and October 2024), the IMF (April 2024), the OFR (March 2024), and the Securities and Exchange Commission (SEC) (February 2024).

Their concern is forward-looking and structural, not reactive to a specific 2024-2025 crisis event. BREIT and SREIT remain the cases regulators cite most frequently as analogues for how private credit gating behaviour could operate at scale.

Why software and SaaS loans are the stress point inside private portfolios

The concentration of software and SaaS borrowers in private credit portfolios did not happen by accident. It followed a lending thesis that, until recently, appeared sound.

Private lenders gravitated toward sponsor-backed software buyouts because these companies exhibited three qualities that align with leveraged loan structures: stable annual recurring revenue (ARR), high customer retention rates, and predictable multi-year cash flows. For a lender structuring a five-to-seven-year loan, a borrower with 90%+ revenue renewal rates and contractual subscription income looked like an ideal credit.

The vulnerability sits inside that logic. According to Fisher Investments, many SaaS companies have operational lifespans of three to five years or shorter, while the loans extended to them carry equal or longer maturities. Capital can become tied up, or written off entirely, before a company runs its course.

Artificial intelligence is accelerating this dynamic. Goldman Sachs equity research from July 2024 highlighted that some legacy SaaS models face margin pressure and slower growth as AI-native competitors emerge, challenging highly leveraged capital structures. The divergence between software winners and losers is widening, and it is undermining the stable-ARR assumption at the core of private credit underwriting for these borrowers.

S&P Global Ratings (January 2025): Private credit portfolios heavily concentrated in software face “elevated risk from rapid technological disruption, including AI,” because underwriting often assumes stable recurring revenue and long customer lives.

The three core underwriting assumptions that AI disruption is now stress-testing:

- Stable ARR growth over the loan’s full term

- Durable customer retention across multi-year horizons

- Predictable cash flows sufficient to service leveraged capital structures

A BIS working paper from December 2024 added a systemic dimension: AI increases correlated default risk across technology sectors, meaning concentrated private lenders may face simultaneous impairment across multiple borrowers rather than isolated credit events. Filings from Ares Capital Corporation and Blue Owl Capital for 2024 disclosed isolated write-downs and non-accruals in software and technology-related loans, though both described overall credit quality as solid.

Contained for now, but here is what would change that

As of May 2026, the risk remains primarily structural rather than acute. Fisher Investments observes limited signs of widespread distress, with only isolated instances of impaired private assets. The firm has described this area as a focus of significant internal research effort over roughly the prior year, framing it as a liquidity mismatch concern rather than a catastrophic loss scenario.

Fisher Investments (May 2026): The primary systemic concern around private credit is liquidity mismatch and spillover via forced sales of liquid assets, not immediate catastrophic credit losses.

Reuters reported in June 2024 that restructurings and amendments were rising among private credit lenders, with technology and software among stressed sectors, but no system-wide impairment had materialised.

Three specific conditions would shift this assessment from forward-looking concern to active risk:

- A broad deterioration in software and SaaS credit quality driven by AI displacement at scale, rather than isolated write-downs

- A sustained rise in redemption pressure across semi-liquid private credit vehicles, beyond individual fund-level events

- A significant increase in forced liquidation of public securities by private funds under outflow pressure

The market’s continued growth trajectory matters here. With private credit projected to reach $4.5 trillion globally by 2030 according to Preqin, even without a triggering event today, the systemic footprint of a future stress episode will be larger than anything seen in this asset class before. S&P Global Ratings noted in January 2025 that continued AUM growth was being driven by banks’ ongoing retreat and sustained M&A activity, both structural trends unlikely to reverse.

The next major ASX story will hit our subscribers first

The precise question investors should be asking about their private credit exposure

The systemic analysis translates into a specific diagnostic framework for individual portfolios. Four questions can determine whether this risk applies to a given investor’s holdings:

- Does the private credit vehicle in the portfolio offer periodic liquidity (interval fund, semi-liquid structure) while investing in illiquid long-dated loans?

- What percentage of the fund’s portfolio is held in liquid assets as a redemption buffer?

- What is the fund’s sector concentration in software, technology, and SaaS borrowers, and how does it compare with public credit indices?

- Has the manager disclosed how it is stress-testing its underwriting assumptions against AI-driven disruption in the software borrower base?

The first two questions identify whether the liquidity mismatch mechanism applies at all. The Federal Reserve’s April 2024 report confirmed that the risk concern is greater for interval funds and semi-liquid vehicles than for closed-end BDCs, making vehicle structure the first variable to check.

The third and fourth questions address concentration risk. Fitch Ratings flagged that US direct-lending portfolios carry greater technology weight than public indices, increasing idiosyncratic and disruption risk. Fisher Investments expects AI to benefit some software companies while rendering others obsolete, meaning outcomes across private loan portfolios will vary considerably rather than declining uniformly. The underwriting question is whether a given manager’s book is positioned for that dispersion or exposed to it.

The risk does not require catastrophic losses to affect investors. Even a liquidity crunch that forces a manager to sell public equities at depressed prices can create losses for investors who held no direct private credit exposure at all.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements regarding future market conditions and potential risk scenarios are speculative and subject to change based on market developments and regulatory actions.

The risk worth watching is the one that does not make headlines until it is too late

The private credit market’s primary vulnerability is not the dramatic default event that produces front-page coverage. It is a structural mismatch operating quietly inside fund vehicles that promise liquidity their underlying assets cannot deliver.

The mechanism is specific: loan impairment triggers redemptions, redemptions trigger liquid-asset sales, and liquid-asset sales transmit stress into public markets where investors may have assumed they had no private credit exposure. Software and SaaS concentration inside these portfolios adds a catalyst, as AI-driven disruption stress-tests the very underwriting assumptions that made these loans attractive.

The risk is currently contained. No system-wide impairment has materialised in the US corporate private credit market through mid-2026. But the market is growing, semi-liquid vehicles are proliferating, and the conditions for this mechanism to operate at scale are strengthening. Understanding the structural mechanism is the first step. The second is asking the right questions of any manager or vehicle with private credit exposure in a portfolio. The answers will determine whether this risk is one that belongs on a watchlist or in a portfolio review.

—