Why ASX Consumer Discretionary Has Lagged the Market for 5 Years

1 hr ago

Only about one in four Americans with a will has reviewed it in the last five years, according to a 2024 Rocket Lawyer/YouGov survey reported by CNBC. That statistic lands differently in spring 2026, a season when families are navigating some of the most consequential estate planning conditions in recent memory. The federal estate tax exemption now sits at $15 million per individual, permanently increased under the One Big Beautiful Bill Act signed in July 2025. Graduation season, whether a grandchild finishing high school or a child completing a graduate degree, creates a natural inflection point. Wealth structures built years ago may no longer reflect a family’s current size, goals, or tax environment. This guide walks through six planning actions for US families with accumulated wealth during spring 2026: from documents that become legally urgent the moment a child turns 18, to 529 funding mechanics, to the coordination between financial and estate planners that most families neglect.

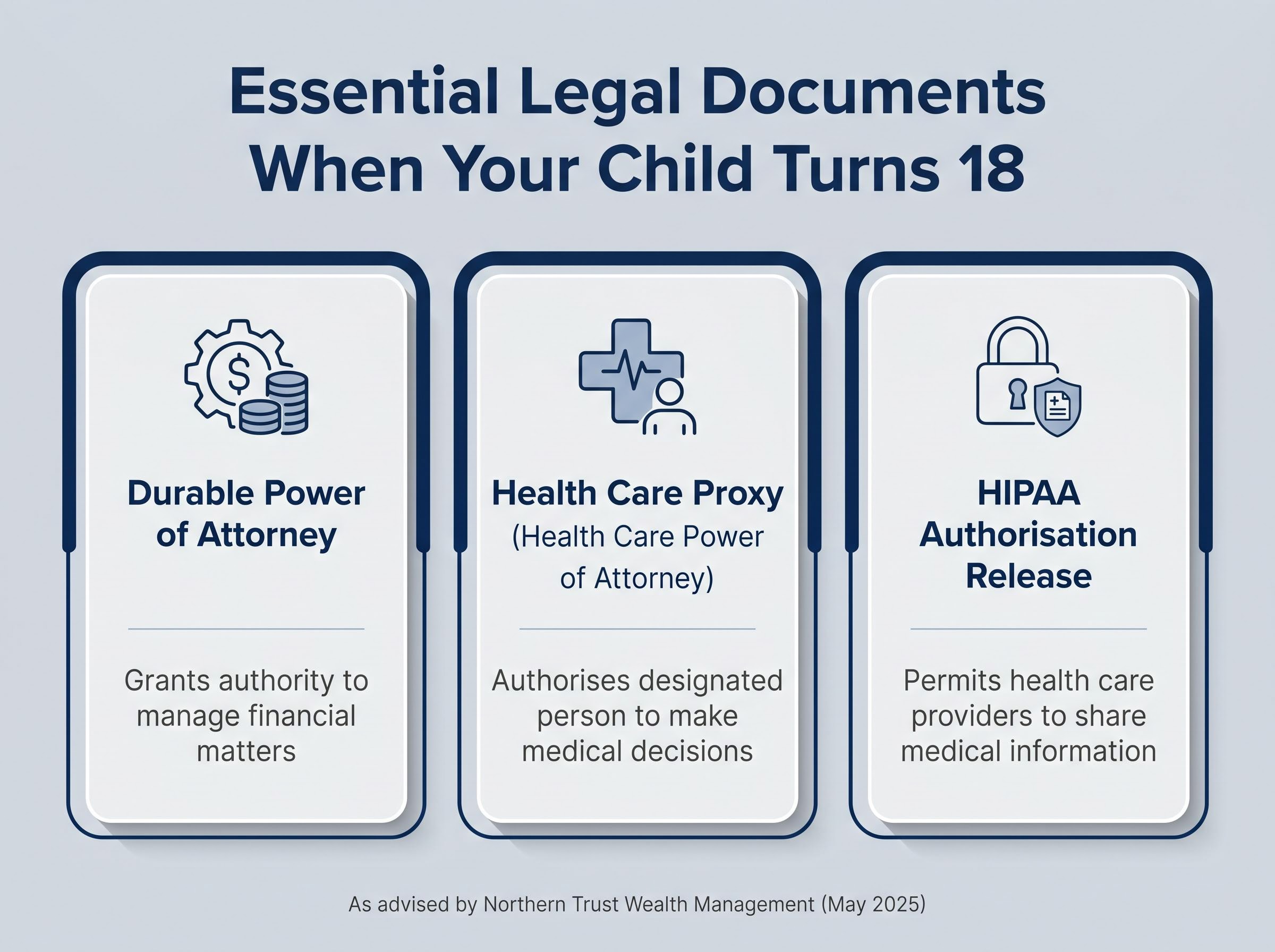

The moment a child turns 18, parental authority over medical decisions, financial accounts, and health information ends. This is true regardless of whether the child remains a dependent, lives at home, or has tuition paid by a parent. Without specific legal documents in place, a parent who needs to speak with a hospital, access a bank account, or make a medical decision on behalf of a college student has no standing to do so.

Three documents close that gap immediately:

Northern Trust Wealth Management (May 2025) advises high-net-worth families to align graduation milestones with updates to health care proxies, HIPAA releases, and durable powers of attorney for newly adult children.

Morgan Stanley Private Wealth Management notes that first jobs, equity compensation, and relocation, events that often accompany graduation, all carry tax and planning implications requiring updated legal documents. These are not estate planning abstractions. They are the documents a parent would need if their college student were hospitalised out of state on a Tuesday afternoon.

Wills and estate plans do not become outdated in a single dramatic event. They drift out of alignment through the accumulation of small changes: a new grandchild, a shifted beneficiary designation on a retirement account, a move to a different state, a changed relationship with a named executor.

The data suggests most families are carrying plans that predate at least one of these changes. The Rocket Lawyer/YouGov survey reported by CNBC in February 2024 found that only 26% of Americans with a will had reviewed or updated it in the last five years. A separate Caring.com 2024 study placed the figure even lower, at approximately 20%.

Professional organisations identify a consistent set of triggers that should prompt a formal review:

These triggers, drawn from guidance published by ACTEC and Fidelity Investments in 2024, apply year-round. Graduation season adds a distinct, time-sensitive layer.

When a child reaches 18 or 21, trust distribution standards may need to be revisited. 529 account beneficiary designations should be reviewed, particularly if a student is transitioning from undergraduate to graduate study or entering the workforce. Trustee and successor trustee appointments deserve a fresh look; the person named a decade ago may no longer be the right choice.

Norton Rose Fulbright (May 2024) recommends parents use high school and college graduation as natural checkpoints to review beneficiary designations, 529 plans, and trust provisions for newly adult children. These items are distinct from a general will review and often require coordination with an estate attorney rather than a simple self-review.

An outdated will is not a neutral document. It is an active instruction set that may direct assets to the wrong people, under the wrong conditions, with the wrong fiduciaries in place.

A 529 plan is a tax-advantaged savings account designed for education expenses. Contributions grow tax-free, and withdrawals used for qualified education costs (tuition, fees, room and board, books) are also tax-free at the federal level. The account owner, typically a parent or grandparent, retains full control over the funds, including the ability to change the beneficiary.

That control is what makes a 529 account unusually useful for estate planning. When a grandparent contributes to a 529, those funds leave the grandparent’s taxable estate while the grandparent retains the ability to redirect them. Future appreciation on those contributions is permanently outside the estate.

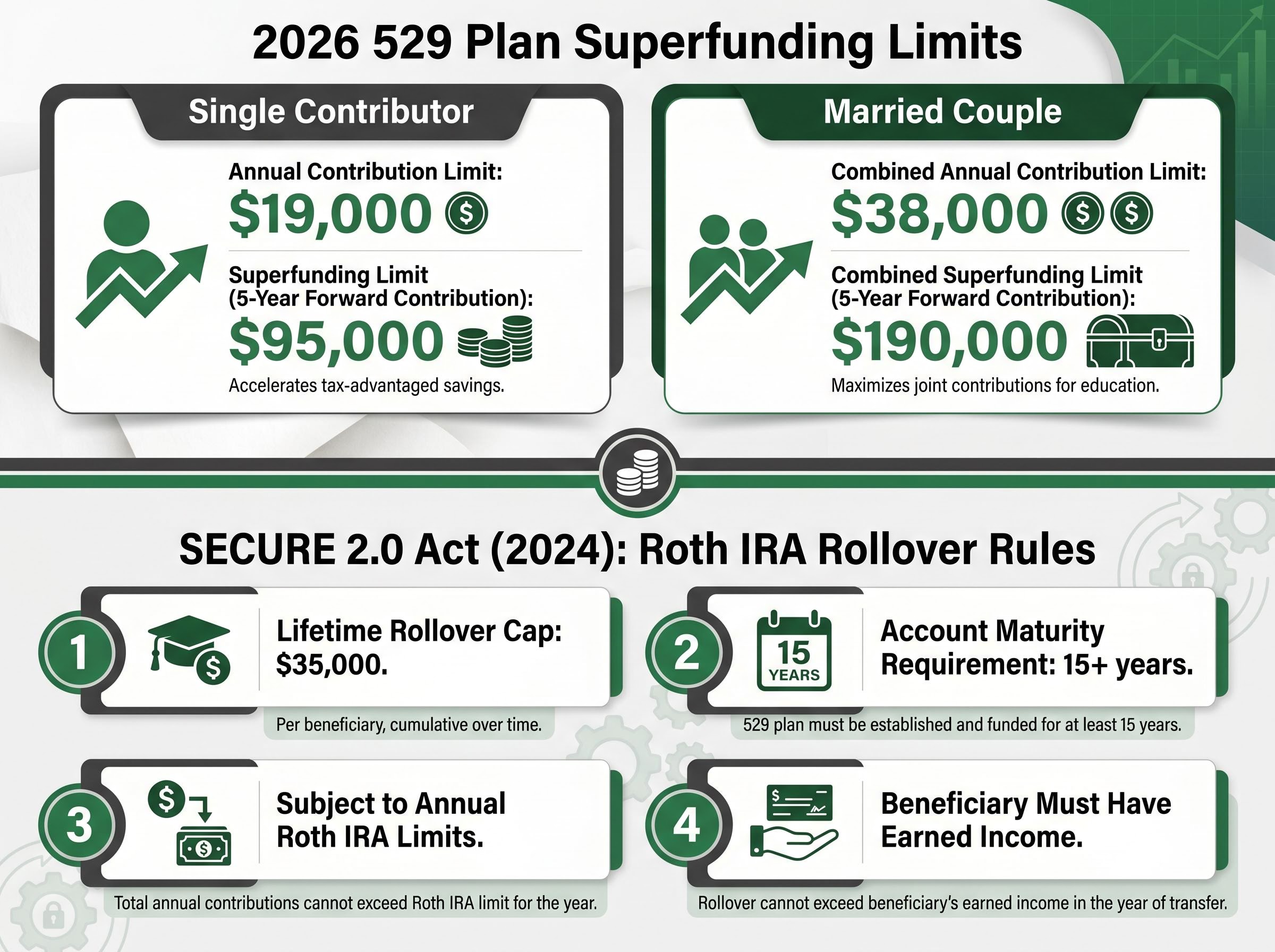

The mechanism that makes this especially powerful is superfunding, a five-year gift tax election that allows a contributor to front-load up to five years of annual gift tax exclusion contributions in a single year.

| Contributor Type | Annual Exclusion 2026 | Superfunding Limit 2026 |

|---|---|---|

| Single contributor | $19,000 per beneficiary | $95,000 per beneficiary |

| Married couple (gift splitting) | $38,000 per beneficiary | $190,000 per beneficiary |

J.P. Morgan Private Bank (2025) recommends superfunding for newborn grandchildren where liquidity allows, then smaller annual contributions as college approaches. Morningstar’s 2025 529 Landscape report suggests targeting roughly one-third of projected four-year costs as a savings benchmark, noting that front-loading is more efficient for affluent families given compounding. For context, the College Board reports average total cost of attendance for 2024-25 at $29,300 for public four-year in-state and $59,100 for private nonprofit four-year institutions.

The historical concern with aggressive 529 funding was overfunding: what happens if the beneficiary does not use all the money? The SECURE 2.0 Act (Section 126, effective 2024) addressed this directly by allowing unused 529 funds to roll over into a Roth IRA for the beneficiary, subject to four conditions:

This provision removes the primary objection to contributing aggressively to a 529, making the account a genuine dual-purpose vehicle for education savings and estate reduction.

The SECURE 2.0 Section 126 rollover rules establish that unused 529 balances can move into a Roth IRA for the beneficiary, subject to the $35,000 lifetime cap and the requirement that the account has been open for at least 15 years, removing the longstanding overfunding objection that previously discouraged aggressive 529 contributions.

Through 2024 and into early 2025, a specific anxiety dominated estate planning conversations: the scheduled sunset of the Tax Cuts and Jobs Act provisions at the end of 2025, which would have roughly halved the federal estate tax exemption. Families accelerated gifting. Advisers urged action before the window closed.

That cliff did not arrive. The One Big Beautiful Bill Act (Public Law 119-21), signed on 4 July 2025, permanently extended and increased the exemption.

| Year | Basic Exclusion Per Individual | Authority |

|---|---|---|

| 2024 | $13.61 million | IRS Rev. Proc. 2023-34 |

| 2025 | $13.99 million | IRS Rev. Proc. 2024-40 |

| 2026 | $15.00 million | One Big Beautiful Bill Act (Public Law 119-21) |

The removal of the sunset eliminates one specific time pressure. It does not make lifetime gifting less valuable.

Future appreciation on gifted assets is permanently removed from the taxable estate regardless of exemption levels. The $19,000 annual gift tax exclusion compounds meaningfully over time for families with multiple beneficiaries. And for families who made large gifts under the higher exemptions in 2024 or 2025, IRS final regulations (TD 9884, issued 2019) confirm there will be no clawback.

The IRS anti-clawback regulations for prior gifts confirm that taxable gifts made under higher lifetime exemptions before any future exemption reduction will not be recaptured, a protection that applies to families who accelerated gifting strategies during the pre-OBBBA period of 2024 and early 2025.

IRS Treasury Decision 9884 confirms that gifts made under higher exemptions will not be recaptured if the exemption later decreases. For families who made accelerated gifts during the pre-OBBBA period, this assurance remains in effect.

Cerulli Associates’ 2025 report on US high-net-worth markets found that more than half of advisers serving ultra-high-net-worth clients cite intergenerational wealth transfer as their top planning priority for the next three years. The strategic window has not closed; it has stabilised. Families who paused planning while waiting for legislative clarity now have it.

The permanent exemption increase under the One Big Beautiful Bill Act resolves one legislative uncertainty, but affluent families monitoring the broader tax environment should note that unrealized capital gains tax proposals remain an active area of policy debate, with state-level experimentation underway and constitutional questions left open by the Supreme Court’s 2024 decision in Moore v. United States.

Past performance does not guarantee future results. Tax rules are subject to legislative change, and individual circumstances vary.

The most common failure in estate planning is not a poorly drafted will. It is a well-drafted will that says one thing while beneficiary designations on retirement accounts, life insurance policies, and 529 plans say another. Beneficiary designations override will instructions. A will that leaves everything to three children equally is meaningless if a retirement account still names an ex-spouse as primary beneficiary.

UBS Global Wealth Management (2025) identifies misalignment between investment strategy and estate structures as a recurring failure point, noting that clients with integrated advisory teams report higher satisfaction with wealth transfer plans.

A coordinated review brings the estate attorney, financial adviser, and CPA into the same conversation. The four structures that should be examined together:

The ACTEC 2024-2025 podcast series emphasises that coordination between estate attorneys and financial advisers is the mechanism that prevents mismatches between estate documents and actual asset structures. The CFP Board (2024) similarly recommends that financial professionals collaborate with clients’ estate planning attorneys to ensure investment strategies, beneficiary designations, and cash-flow plans align with wills and trusts.

Morgan Stanley, UBS, and Northern Trust all explicitly identify graduation as an appropriate trigger for this joint review, particularly when it coincides with a child’s entry into the workforce, first equity compensation, or relocation. The ABA Real Property, Trust and Estate Law Section recommends annual or biennial joint reviews, with major life events in the younger generation triggering beneficiary, trustee, and distribution-standard reviews.

The procedural elements of estate planning, the documents, the account structures, the tax strategy, address what happens to wealth. A growing body of survey data suggests affluent families are spending more time on a different question: what the wealth is for.

The EY Global Wealth Research Report 2025 found that 64% of high-net-worth and ultra-high-net-worth respondents prioritised ensuring family members are financially prepared and educated over maximising inheritances. Over 40% of US wealthy investors want distributions tied to education, entrepreneurship, or impact goals.

This shift is producing specific structural changes. Families are adopting practical tools that embed values into the mechanics of wealth transfer:

Natixis Investment Managers (2025) reports increased adoption of values-based trusts incorporating incentives for education, philanthropy, or entrepreneurship. Fidelity Charitable’s 2025 Giving Report notes that many families now use DAFs as core elements of estate plans, naming children as successor advisors and integrating DAFs into revocable trust structures.

Graduation provides a natural entry point for conversations about financial values and the intent behind trusts and inheritances. These conversations do not require completing the legal documents first; they are a parallel track that makes the documents more meaningful.

Hamilton Lane’s 2025 Global Private Wealth Survey cited next-generation engagement and education as one of the top emerging client priorities in North America. The generational transition a graduation represents, moving from dependent to independent, is exactly the kind of moment families use to articulate what the wealth is for and what role the next generation will play in stewarding it.

Several conditions are converging at once. Newly adult children are crossing a legal threshold that creates immediate document needs. The estate tax environment, after years of uncertainty, has stabilised at a $15 million per-individual exemption with permanent status. 529 superfunding mechanics are well-established, and the SECURE 2.0 rollover provision has removed the historical overfunding objection. And the broader shift in how affluent families approach wealth transfer, toward purpose, preparation, and heir engagement, makes the values conversation easier than it has been in prior generations.

The concrete first step is straightforward: schedule a joint meeting with a financial planner and estate planning attorney before the summer, using the graduation itself as the scheduling anchor. The goal is not a complete overhaul. It is alignment, ensuring that every component of the family’s financial and legal plan is pointing in the same direction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Superfunding is a five-year gift tax election that lets a contributor front-load up to five years of annual gift tax exclusion contributions into a 529 plan in a single year. In 2026, this means a single contributor can contribute up to $95,000 per beneficiary, or $190,000 for a married couple using gift splitting, without triggering gift tax.

Once a child turns 18, parents lose automatic legal authority over their finances and medical decisions, so three documents are needed: a durable power of attorney for financial matters, a health care proxy for medical decisions, and a HIPAA authorisation release so providers can share health information with family members.

The federal estate tax exemption in 2026 is $15 million per individual, permanently increased under the One Big Beautiful Bill Act signed in July 2025, which resolved years of uncertainty around the scheduled sunset of the Tax Cuts and Jobs Act provisions.

Yes, under the SECURE 2.0 Act Section 126, effective 2024, unused 529 funds can be rolled into a Roth IRA for the beneficiary, subject to a $35,000 lifetime cap, a 15-year minimum account age, annual Roth IRA contribution limits, and an earned income requirement for the beneficiary.

Professional organisations including ACTEC and the ABA recommend annual or biennial reviews, with major life events such as marriage, divorce, birth of a child, relocation, or a child turning 18 or 21 triggering immediate review of beneficiary designations, trust provisions, and named fiduciaries.