3 ASX Sector ETFs That Returned Up to 136% in One Year

1 hr ago

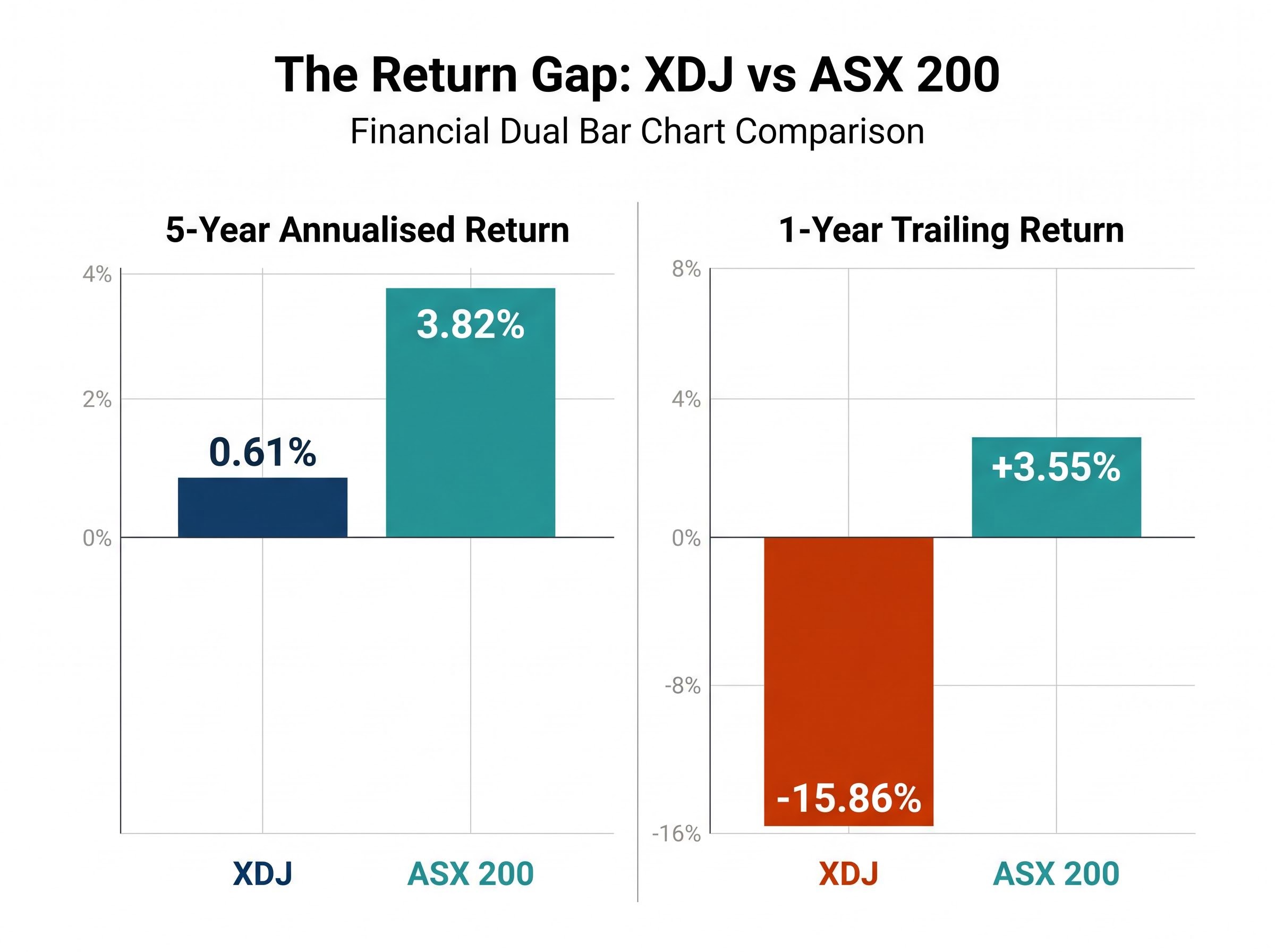

The ASX Consumer Discretionary sector has returned just 0.61% per year over the past five years. Over the same period, the broader ASX 200 returned 3.82% annually. For investors expecting household-name retailers and travel companies to deliver steady gains, that gap demands an explanation.

With the Reserve Bank of Australia (RBA) navigating a prolonged rate cycle and household budgets under sustained pressure, the forces weighing on this sector are not accidental. They are structural, and understanding them is a prerequisite before allocating capital to any stock in this space.

What follows is a breakdown of what the ASX Consumer Discretionary sector actually contains, why it has underperformed, how interest rates mechanically drive that underperformance, why comparing stocks within the sector is harder than it looks, and what three practical considerations should frame any investment decision here.

Under the Global Industry Classification Standard (GICS), the Consumer Discretionary sector carries code 2500. It groups companies that sell goods and services consumers want but do not strictly need: the purchases that get deferred or downsized when budgets tighten.

MSCI’s GICS framework organises publicly listed companies into 11 sectors, 25 industry groups, 74 industries, and 163 sub-industries using a standardised classification methodology co-developed with S&P Global, giving investors a consistent taxonomy for comparing companies across markets.

That definition sounds straightforward. In practice, it covers businesses with wildly different revenue drivers, customer bases, and economic sensitivities. The S&P/ASX 200 Consumer Discretionary Index (ticker: XDJ) is the benchmark that tracks these companies on the ASX, and its membership spans:

A consumer who books a holiday through Flight Centre and a consumer who replaces a couch through Nick Scali are both counted under the same sector label. That breadth is the first thing to understand: the index measures an average across businesses that rarely move in lockstep.

The headline figures are stark. According to the Rask Invest Research Team (published 27 May 2026), the XDJ has delivered an annualised return of just 0.61% over five years. The ASX 200, over the same period, returned 3.82% per year.

The five-year annualised return gap: 0.61% for the XDJ versus 3.82% for the ASX 200. A dollar invested in the broader market compounded meaningfully faster than one allocated to consumer discretionary names.

The more recent picture suggests the divergence has deepened rather than narrowed. Data from Market Index (approximately 26 May 2026) shows the XDJ’s one-year trailing return at approximately -15.86%, while the ASX 200 returned approximately +3.55% over the same period. The XDJ closed near 3,412.3; the ASX 200 stood near 8,658.

The consumer discretionary breadth deterioration visible in market-wide data from early May 2026 provides a granular illustration of the sector-level stress: seven consumer discretionary constituents hit fresh 52-week lows in a single week, even as the headline ASX 200 fell only modestly, exposing the gap between index-level readings and the actual performance of individual sector names.

| Metric | XDJ (Consumer Discretionary) | ASX 200 |

|---|---|---|

| 5-year annualised return | 0.61% | 3.82% |

| 1-year trailing return | -15.86% | +3.55% |

These figures cover a specific macro environment: a period of rising then elevated interest rates in Australia. That context matters, because it frames the underperformance as a cyclical story rather than a permanent structural verdict against the sector’s constituent businesses.

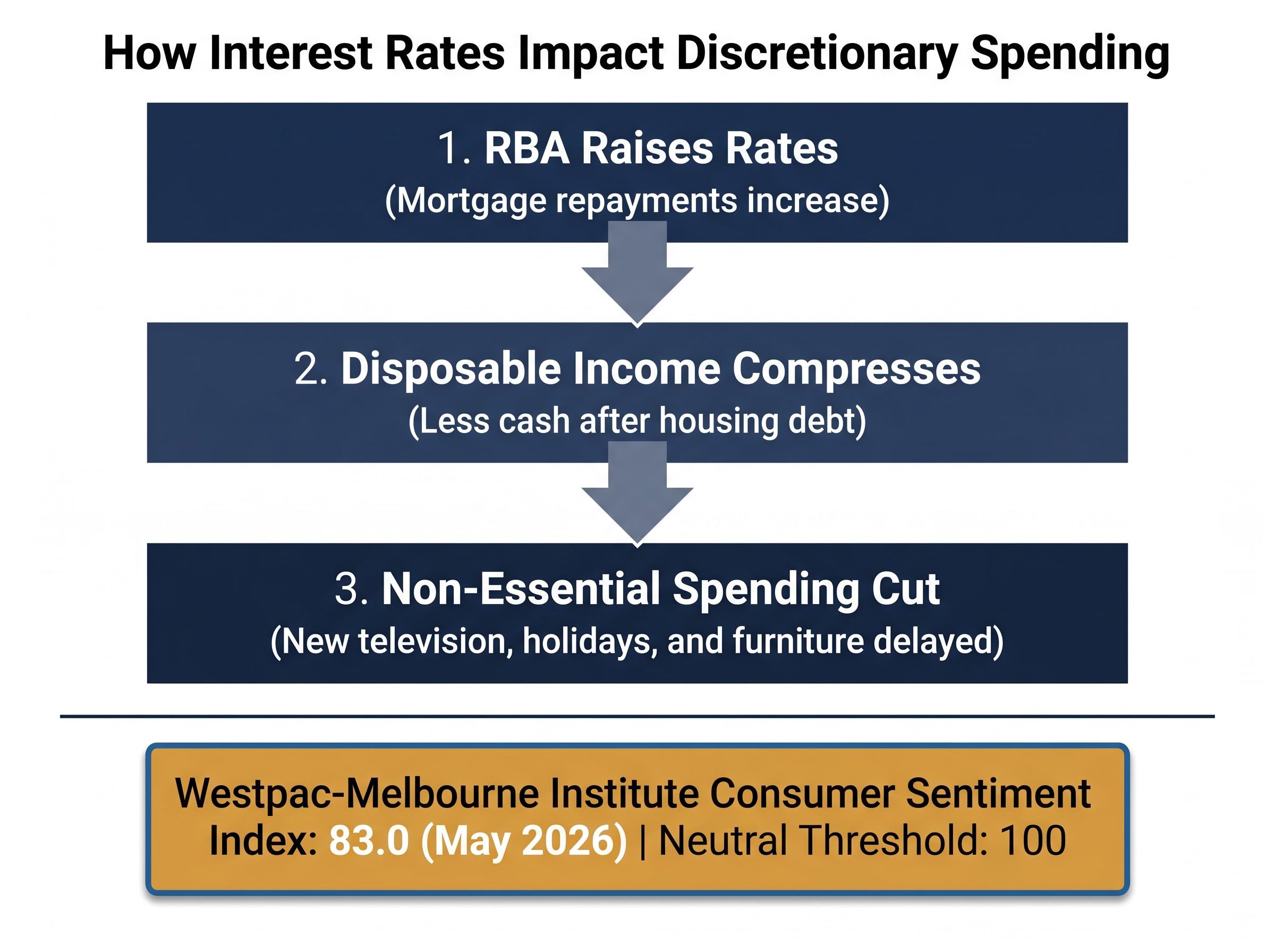

The connection between RBA rate decisions and consumer discretionary revenue is not abstract. It operates through a direct, three-step transmission chain that retail investors can track in real time:

This asymmetry is what separates Consumer Discretionary from sectors such as Consumer Staples or Healthcare. When budgets tighten, a household still buys groceries and fills prescriptions. The new laptop or the interstate flight is the line item that disappears.

The RBA tightening cycle has been notably aggressive by global standards, with the Fed, ECB, and Bank of England all holding rates steady during the same period that the RBA delivered three consecutive hikes, creating a policy divergence that amplified pressure on Australian household budgets relative to peers in other developed markets.

Consumer sentiment data reinforces this mechanism with current evidence. The Westpac-Melbourne Institute Consumer Sentiment Index rose to 83.0 in May 2026, up from 80.1 in April 2026, according to Trading Economics. The ANZ-Roy Morgan Consumer Confidence reading sat at 80.3 in April 2026.

The Westpac-Melbourne Institute Consumer Sentiment Index stood at 83.0 in May 2026, well below the neutral threshold of 100. Even a modest improvement from the prior month’s 80.1 leaves household confidence in firmly pessimistic territory.

Both indices sitting in the low-to-mid 80s represents depressed sentiment relative to a neutral reading of 100. Confidence affects spending even among households not directly exposed to higher mortgage costs: when the national mood is cautious, discretionary purchases get postponed. Consumer discretionary businesses tend to perform best during periods of lower interest rates, and the current readings explain why that recovery has not yet materialised.

Knowing that the sector has underperformed is useful. Acting on that knowledge is where the complexity begins.

Because GICS code 2500 spans retailers, leisure companies, media businesses, automotive distributors, and more, comparing one member against another using the same valuation metrics often produces misleading conclusions. A travel company with volatile, booking-dependent revenue and an electronics retailer with predictable seasonal cycles have fundamentally different cash flow profiles, margin structures, and risk exposures. Applying a single price-to-earnings threshold across both says little of analytical value.

Wesfarmers illustrates this challenge at the single-company level. It is classified under Consumer Discretionary, yet its operating portfolio includes:

Bunnings generates the majority of Wesfarmers’ operating profit and carries partial defensive characteristics; homeowners still repair leaking taps regardless of sentiment readings. Wesfarmers is often described as operating like a publicly traded private equity firm: acquiring businesses, utilising cash flows, reinvesting for growth, and divesting at a profit.

According to the Rask Invest Research Team (published 27 May 2026), Wesfarmers achieved average annual revenue growth of 9.2% over three years. Compare that with the sector’s 0.61% annualised index return over a broadly similar period, and the gap between the index story and the individual company story becomes clear.

That said, operational strength does not guarantee share price immunity. Wesfarmers’ share price declined 6.4% from the start of 2025, a reminder that even diversified, well-managed businesses remain exposed to broader sector sentiment and market conditions.

The mechanics above explain why the sector has underperformed. The question for retail investors is what to do with that understanding. Three considerations distil the analysis into a practical starting framework:

Familiarity bias in retail investing creates a specific risk in this sector: investors who regularly shop at consumer discretionary brands often conflate a positive customer experience with investment quality, inflating their confidence in multiples that can compress sharply when macro conditions shift, as Flight Centre’s price-to-sales ratio falling from 3.42x to 0.76x during the rate cycle illustrates.

Wesfarmers dividend yield: approximately 2.6% current versus a five-year average of approximately 3.4%. The gap reflects share price appreciation and dividend growth rather than a cut in distributions, but it signals a different entry point for income-focused investors.

Dividend yield serves as a basic valuation signal. More rigorous methods, such as discounted cash flow analysis or dividend discount models, are preferred for formal assessment.

The ASX Consumer Discretionary sector’s five-year underperformance, 0.61% annualised against the ASX 200’s 3.82%, is a direct function of the rate environment, not a reflection of broken businesses. The transmission chain from rate decisions to household wallets to retailer revenue is clear and trackable.

That same clarity, however, means the conditions for recovery are equally identifiable. Consumer sentiment indices remain in the low-to-mid 80s, below the neutral 100 threshold. Until rate conditions ease and household confidence returns, the sector-wide headwind persists.

The more productive approach is to examine individual businesses rather than the sector index. As the Wesfarmers example demonstrates, the gap between sector-wide data and company-level performance can be substantial. Investors who understand the macro mechanics and apply them to specific names, rather than making blanket sector calls, are better positioned to identify opportunities as the cycle turns.

ASX sector concentration in Financials and Materials, which together account for roughly 45% of the ASX 300, partly explains why the broader index returned approximately 8.62% annually over 15 years while the S&P 500 delivered 16.03% in Australian dollar terms over the same period, a structural gap that becomes relevant context when evaluating whether rotating within the ASX into consumer discretionary names is the most productive use of available capital.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The ASX Consumer Discretionary sector (GICS code 2500) groups companies that sell goods and services consumers want but do not strictly need, tracked by the S&P/ASX 200 Consumer Discretionary Index (XDJ). It includes businesses such as JB Hi-Fi, Harvey Norman, Flight Centre, Nick Scali, and Wesfarmers, which owns Bunnings, Kmart, Target, and Officeworks.

The sector's underperformance is largely driven by rising RBA interest rates compressing household disposable income, which causes consumers to cut non-essential spending first. Over five years, the XDJ returned just 0.61% annually versus 3.82% for the ASX 200, with the one-year trailing return sitting at approximately -15.86% as of May 2026.

When the RBA raises rates, variable mortgage repayments increase and household disposable income shrinks, causing consumers to defer non-essential purchases like electronics, furniture, and travel. This revenue reduction flows directly to consumer discretionary companies, while sectors like Consumer Staples and Healthcare are largely insulated because those purchases cannot easily be postponed.

The Westpac-Melbourne Institute Consumer Sentiment Index measures household confidence on a scale where 100 is neutral; a reading below 100 signals pessimism about spending. In May 2026, the index stood at 83.0, indicating that Australian consumers remain cautious, which continues to suppress discretionary spending even among households not directly affected by higher mortgage costs.

Comparing a stock's current dividend yield against its historical average can signal whether the entry point offers relative value for income-focused investors. For example, Wesfarmers currently yields approximately 2.6% versus a five-year average of approximately 3.4%, suggesting the share price has appreciated relative to distributions, which is a relevant consideration before buying for income.