BlackRock Raises AI and Tech Decoupling to Top Risk Tier

2 hrs ago

Australia’s prudential regulator has put the financial sector on notice: artificial intelligence adoption is outpacing the governance frameworks designed to manage its risks, and the gap is no longer theoretical. On 30 April 2026, the Australian Prudential Regulation Authority (APRA) issued a formal letter to all regulated entities, setting out specific expectations across four domains after targeted supervisory engagement with large banks, insurers, and superannuation trustees conducted in late 2025. The letter arrived alongside parallel guidance from the Australian Securities and Investments Commission (ASIC), signalling a coordinated regulatory posture on AI governance across Australian financial services. What follows covers what APRA found, what it now expects from boards and accountable executives, why the cyber dimension deserves particular attention, and what the dual-regulator signal means for entities that have not yet formalised their AI governance frameworks.

APRA’s central finding is direct: across banking, insurance, and superannuation, AI adoption is advancing faster than the governance and risk management structures meant to contain it. The observation did not emerge from desk-based policy work. It came from targeted supervisory engagement with selected large entities in late 2025, giving the finding an evidence-based character that generic industry warnings lack.

The gap between expectation and practice is not hypothetical: documented AI governance failures already on APRA’s record include a superannuation fund that misclassified vulnerable members and a general insurer whose AI pricing model was deployed without independent validation, both attracting formal remediation requirements from the regulator.

APRA’s core regulatory finding: AI adoption across regulated financial institutions is outpacing the governance and risk management frameworks designed to manage its associated risks.

The scale of what sits behind that gap matters. APRA oversees institutions holding approximately $9.8 trillion in assets on behalf of Australian depositors, policyholders, and superannuation members. When the regulator responsible for that asset base issues a formal letter, dated 30 April 2026, applying to every entity under its supervision, the governance gap moves from an abstract observation to a material, sector-wide concern.

The letter sets out expectations across four specific domains, each tightening the accountability net around how regulated entities deploy and oversee AI systems:

Coverage from Clayton Utz (published 5 May 2026) and Norton Rose Fulbright (published in May 2026) characterised the letter as a shift from generalised guidance to targeted, AI-specific supervisory expectations. That distinction matters: these are not aspirational principles. APRA has framed them as defined expectations, and entities that fall short face the prospect of stronger supervisory action.

APRA’s formal AI letter to industry sets out binding expectations across governance, cyber security, supplier risk, and change management, making explicit that entities failing to meet those expectations face the prospect of escalated supervisory action.

| Domain | Key Expectation |

|---|---|

| Governance | Boards must demonstrate literacy on AI risk and establish accountability structures |

| Cyber and information security | Entities must address AI-specific cyber weaknesses already identified by supervisors |

| Supplier risk | Third-party AI provider dependencies must be assessed and managed |

| Change management and assurance | Accountability must extend across the full AI lifecycle, not only at deployment |

The practical implications run deeper than the four domains suggest at first reading. APRA expects entities to establish AI inventories, a foundational governance step that requires organisations to catalogue where and how AI systems operate across their businesses. Accountability must extend across the full AI lifecycle, from development and testing through deployment to ongoing monitoring, not merely at the point a system goes live.

Analysis from Corrs Chambers Westgarth (published 18 May 2026) highlighted a further expectation: entities should maintain fallback options where high reliance on AI systems has developed. That is a concrete operational resilience consideration, requiring organisations to stress-test what happens when an AI system fails or must be withdrawn at short notice.

Vendor concentration risk sits at the centre of the supplier risk expectation, with APRA finding that some regulated entities depend on a single AI provider across multiple critical functions simultaneously, lacking any adequate contingency planning for provider failure or disruption, a pattern that creates a single point of failure running across fraud detection, credit decisioning, and compliance monitoring at once.

Cyber and information security did not appear in the letter as a forward-looking risk category. APRA included it because supervisors observed specific weaknesses during their engagement with regulated entities in late 2025. The gap between AI adoption and cyber preparedness is already visible to the regulator.

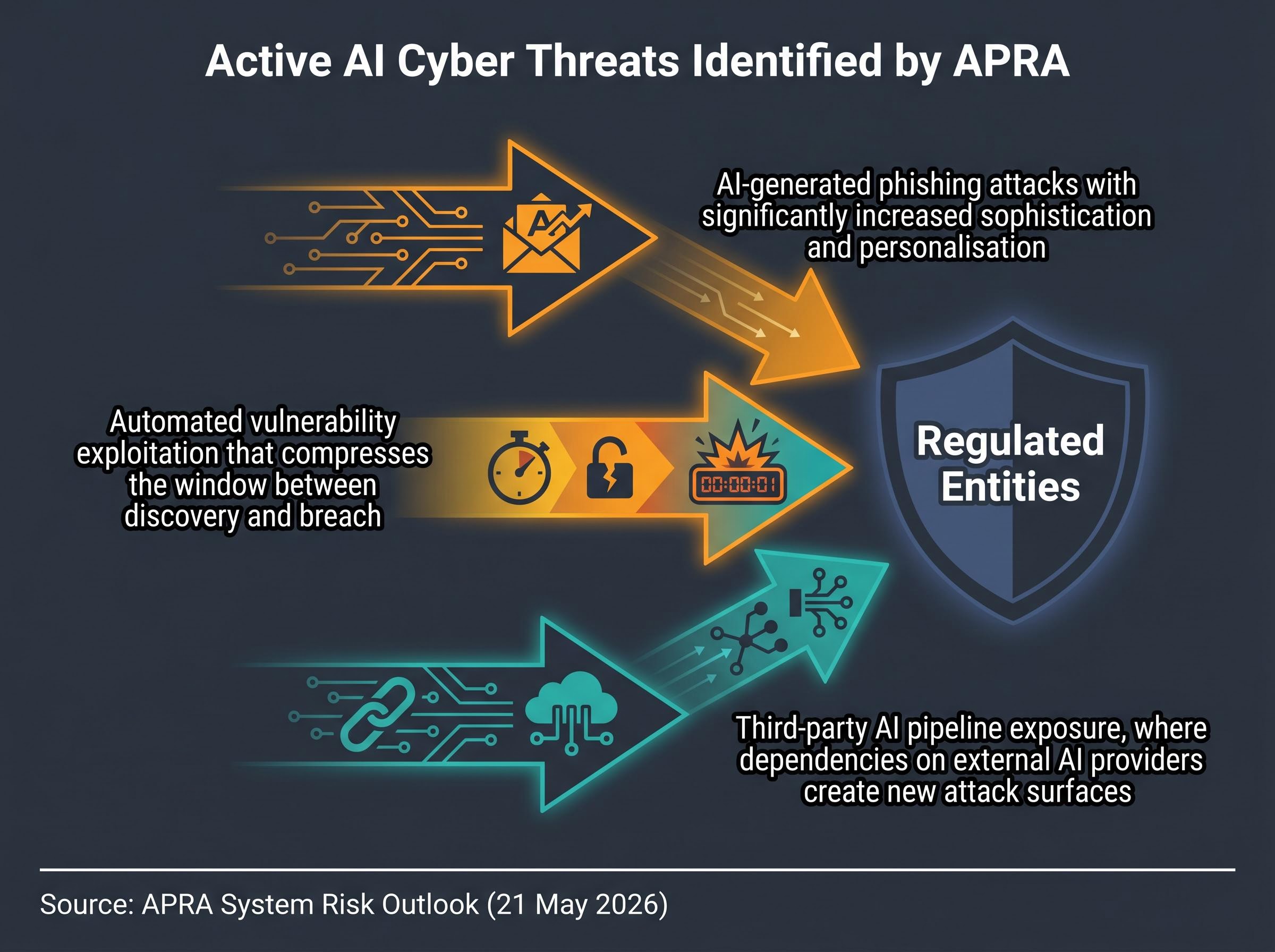

The broader threat environment reinforces the concern. APRA’s System Risk Outlook, published 21 May 2026, identifies AI-enhanced cyber sophistication as an active and evolving threat to regulated entities. The specific characteristics introduced by AI adoption include:

APRA System Risk Outlook (21 May 2026): Advanced AI models are contributing to an increasingly sophisticated cyber threat environment for Australian financial institutions, with AI-enhanced attacks identified as an active and evolving risk.

APRA Chair John Lonsdale has situated cyber risk within the regulator’s current supervisory priorities, reinforcing that this is not a secondary consideration. Entities that have not yet updated their cyber frameworks to account for AI-specific attack vectors are operating with a known gap that APRA has explicitly flagged.

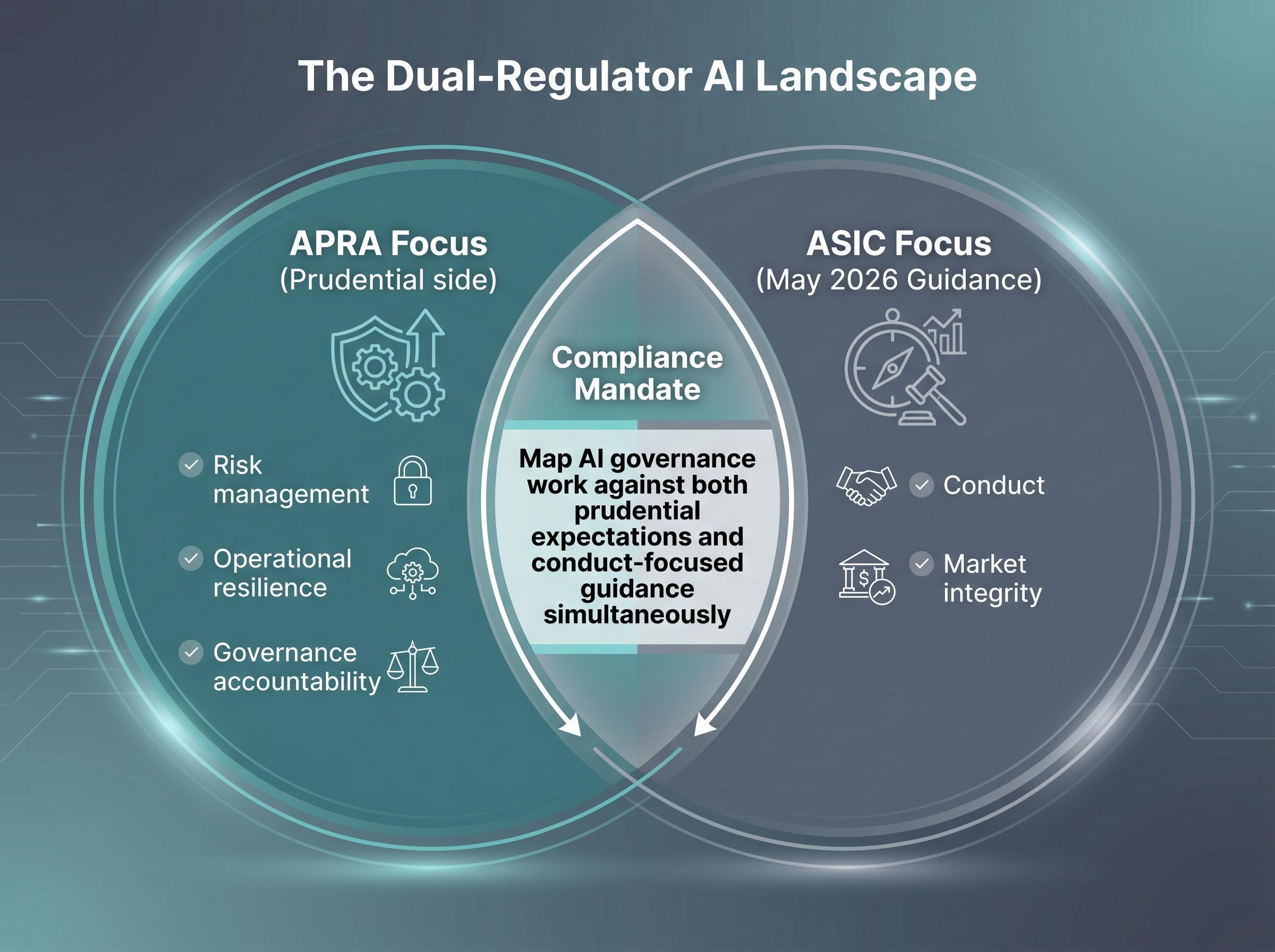

APRA did not act alone. ASIC issued parallel AI guidance in the same reporting period, as referenced in May 2026 coverage from Corrs Chambers Westgarth and other regulatory outlets. The two agencies’ simultaneous action creates a coordinated domestic regulatory posture that covers different but complementary dimensions.

APRA’s focus sits on the prudential side: risk management, operational resilience, and governance accountability. ASIC’s mandate addresses conduct and market integrity. Together, they cover the full spectrum of AI-related risk that a bank, insurer, or superannuation fund must manage.

For entities regulated by both authorities, and that includes most large financial institutions, AI governance frameworks must now satisfy two distinct but converging sets of expectations. The practical implications include:

The window for treating AI governance as a single-regulator compliance exercise has closed.

APRA’s letter does not leave the next steps ambiguous. The implied action sequence for regulated entities follows a clear priority order:

APRA’s escalation signal: The 30 April 2026 letter explicitly references the potential for stronger supervisory action against entities that do not meet the expectations it sets out.

APRA has also situated Australia’s approach within a broader international trend toward AI-specific governance in financial services, referenced directly in the letter. The next edition of APRA’s System Risk Outlook is expected toward the end of 2026, meaning AI governance will remain a supervisory visibility item through the remainder of the year.

Potential CPS amendments are already being discussed at the legislative level, with the Assistant Treasurer reportedly signalling that Australia’s current principles-based approach may not hold if governance gaps persist across the sector, meaning the April 2026 letter could represent the start of a longer arc of increasing regulatory intensity rather than a one-off supervisory moment.

The combination of a formal regulatory letter, parallel ASIC guidance, and an explicitly stated escalation pathway means the cost of delayed action has risen materially since 30 April 2026.

The shift APRA’s letter represents is not from silence to guidance. It is from guidance to expectation, with enforcement consequences attached. Board literacy, lifecycle accountability, and fallback planning are now defined regulatory requirements, not optional governance enhancements.

The stakes behind that shift are concrete: $9.8 trillion in assets, millions of superannuation members and policyholders, and a regulator that has committed its expectations to formal correspondence dated 30 April 2026. ASIC’s parallel action confirmed the signal in May 2026.

For every board member and accountable executive at an APRA-regulated entity, the risk calculus has changed. The question is no longer whether AI governance frameworks are needed. It is whether the ones in place will withstand supervisory scrutiny when APRA comes looking.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

APRA's AI governance framework sets expectations across four domains: board-level governance and accountability, cyber and information security, third-party supplier risk, and change management and assurance. These were formalised in a letter dated 30 April 2026 sent to all APRA-regulated entities.

APRA found that AI adoption across banking, insurance, and superannuation is outpacing the governance and risk management frameworks meant to contain it, with specific failures including a superannuation fund misclassifying vulnerable members and a general insurer deploying an AI pricing model without independent validation.

Regulated entities should establish a comprehensive AI inventory, assess board-level AI literacy gaps, audit third-party AI dependencies and maintain fallback options for high-reliance systems, and stress-test AI-related cyber controls against threat vectors APRA has explicitly identified.

APRA's System Risk Outlook published 21 May 2026 identifies AI-enhanced cyber threats as active and evolving risks, including highly personalised phishing attacks, automated vulnerability exploitation, and new attack surfaces created by third-party AI provider dependencies.

Large institutions regulated by both APRA and ASIC must now satisfy two distinct but converging sets of AI expectations: APRA's focus on prudential risk management and operational resilience, and ASIC's conduct and market integrity guidance, meaning AI governance frameworks must be architected to address both from inception rather than retrofitted.