How ASX Triple Witching Works and Why Midday Is the Danger Zone

28 mins ago

In 2025, more than half of all newly launched ETFs were classified as derivative or options income products. JP Morgan’s own JEPI had grown to over $45 billion in assets, cementing the firm’s dominance in the covered call space. Yet on 19 March 2026, two of the firm’s newest funds, ROCQ and ROCY, went live with almost no fanfare, no distribution history, and a structural pitch that directly challenges the tax efficiency of its own flagship products.

Both funds are covered call ETFs built for taxable accounts. They target investors who want the income profile of JEPQ or JEPI but with distributions structured as return of capital rather than ordinary income. With both funds less than two months old and no confirmed yield data, many income-focused investors are trying to understand what they are actually buying, how the mechanics differ from the products they already own, and whether the tax advantage justifies committing capital to funds with no track record.

What follows is a full explanation of how ROCQ and ROCY work, why their call spread and FLEX options structure matters for taxes, how they compare to GPIQ, GPIX, JEPQ, and JEPI, and what trade-offs investors should weigh before allocating.

The shift started gaining momentum in 2023, when options income ETFs began attracting more new capital than traditional dividend ETFs such as SCHD and VIG. By 2025, the inflection was unmistakable: more than 50% of all newly launched ETFs were derivative or options income products.

Retail investors, not institutional buyers, have driven the bulk of this demand. That buyer profile shapes how these products are designed, priced, and distributed, favouring monthly income, accessible share prices, and simple narratives over institutional-grade complexity.

The debate around dividend investing vs total return sits directly beneath the covered call ETF appeal: investors drawn to JEPI and JEPQ are often optimising for income yield rather than compounding wealth, a preference that the ROC structure of ROCQ and ROCY does not fundamentally change, even if it improves the after-tax efficiency of each distribution.

JP Morgan sits at the centre of this wave. JEPI holds approximately $45.2 billion in assets; JEPQ holds approximately $37.5 billion. Both are among the largest ETFs launched in the past five years. Yet both distribute approximately 90% of their income as ordinary income through equity-linked notes (ELNs), a structure that creates a meaningful tax drag for investors holding them in taxable accounts.

Hamilton Reiner, the portfolio manager behind JEPI, JEPQ, and now ROCQ and ROCY, identified this tax inefficiency as an unaddressed gap in JP Morgan’s own product line. ROCQ and ROCY are the direct result: funds designed to deliver a similar income profile with a distribution structure intended to produce return of capital rather than ordinary income.

Three characteristics define this product cycle:

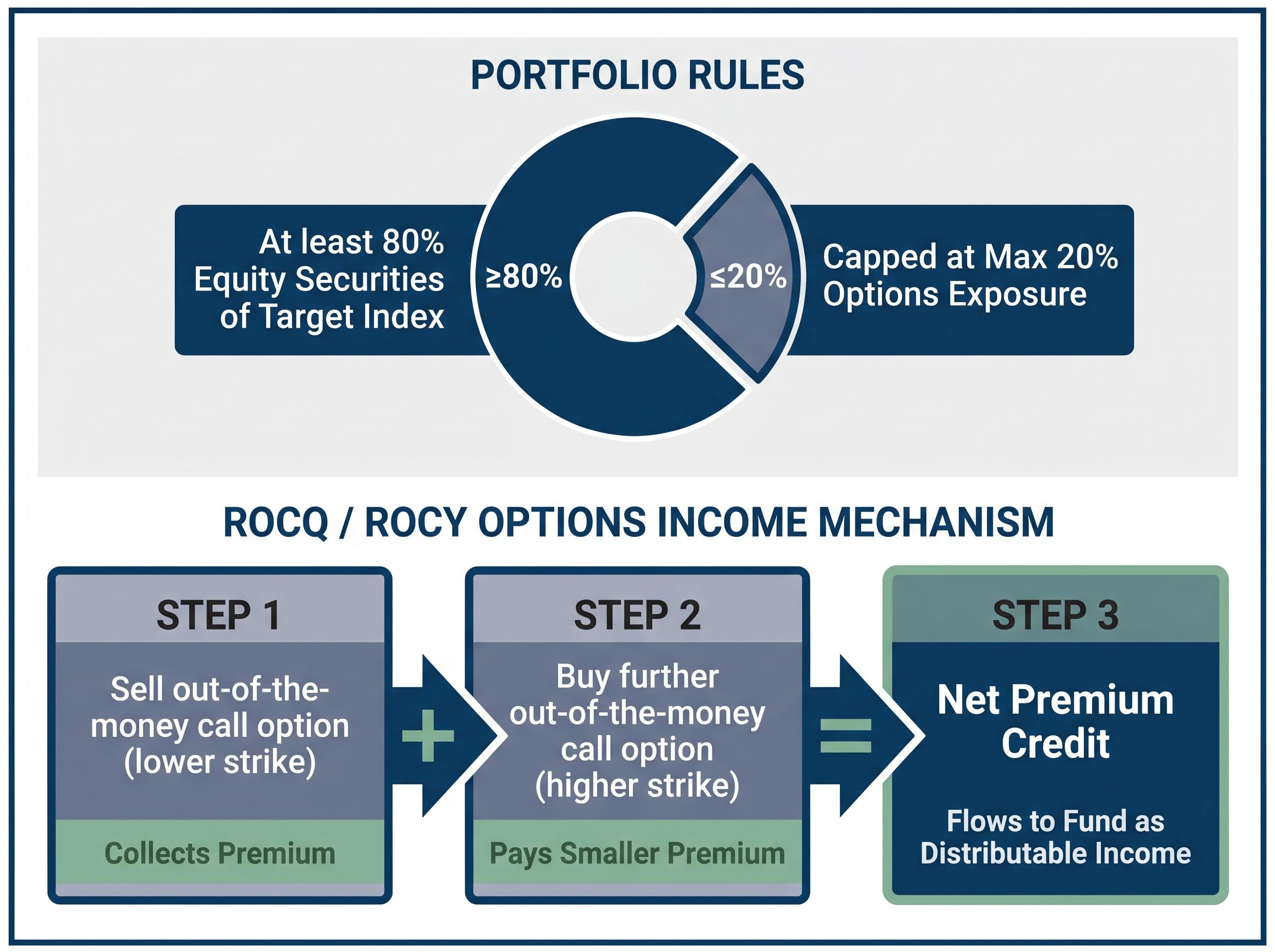

At the surface level, ROCQ and ROCY look familiar. Each fund holds a portfolio of equities tracking its target index (the Nasdaq 100 for ROCQ, the S&P 500 for ROCY) and layers an options strategy on top to generate income. At least 80% of each fund’s assets sit in equity securities of the target index, with options exposure capped at no more than 20% of net assets.

The income generation mechanism, however, is where the funds diverge from simpler covered call products. ROCQ and ROCY use a call spread strategy rather than writing plain covered calls against individual holdings. The mechanics follow three steps:

This structure caps the fund’s upside beyond the higher strike price but generates a net credit that forms the basis for distributions. Income sources for both funds include equity dividends from holdings, realised capital gains from portfolio turnover, and premiums from selling call spreads.

As of 3 May 2026, ROCQ held approximately $144.16 million in assets and ROCY held approximately $135.99 million, reflecting steady inflows in the weeks since launch.

The options used by ROCQ and ROCY are not standard listed contracts. Both funds use FLEX options, which are exchange-listed options traded and cleared through the CBOE with customisable strike prices and expiration dates. Unlike over-the-counter derivatives, FLEX options carry the counterparty risk protections of exchange clearing while allowing the portfolio manager to tailor strikes and expirations to the fund’s specific income and risk targets.

The Cboe FLEX options specifications confirm that all FLEX trades are cleared through the Options Clearing Corporation, eliminating bilateral counterparty exposure while preserving the strike and expiration customisation that distinguishes these contracts from standard listed options.

This is the same mechanism used by GPIQ, GPIX, and several other tax-oriented covered call ETFs, which is why these funds are grouped together for tax comparison purposes. The options are written against the index as a whole, not against individual stock holdings, and positions are reset periodically.

The tax problem is straightforward. JEPI and JEPQ generate their option income through equity-linked notes, and approximately 90% of those distributions are classified as ordinary income. For investors in higher income brackets holding these funds in taxable accounts, the effective after-tax yield is materially lower than the headline number.

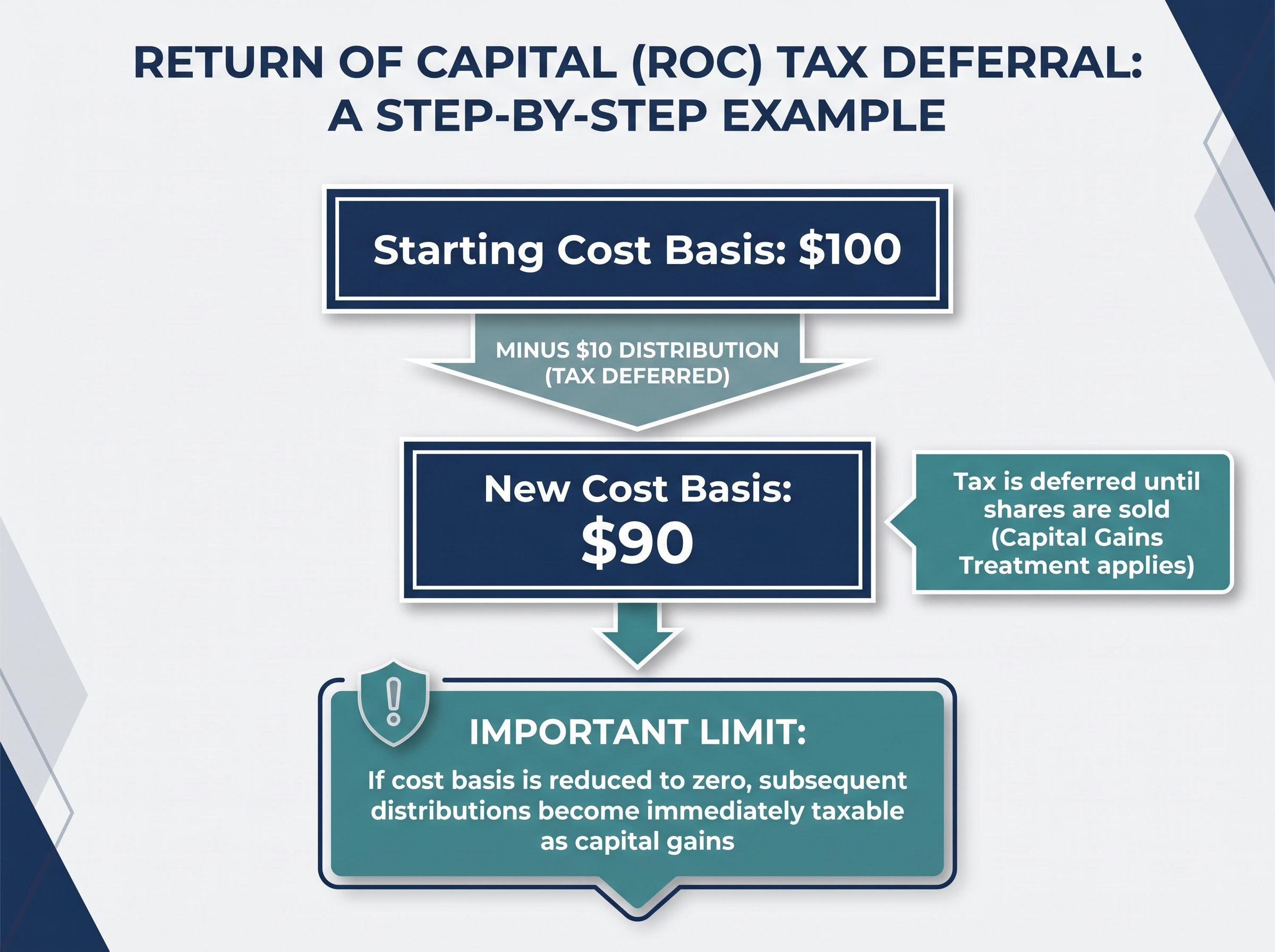

ROCQ and ROCY are designed to solve this by structuring distributions as return of capital (ROC). Under ROC treatment, distributions are not immediately taxable in the year received. Instead, they reduce the investor’s cost basis in the fund.

IRS Publication 550 nondividend distributions guidance specifies that distributions exceeding a shareholder’s cost basis are not taxable at receipt but reduce that basis to zero, with any excess then reported as a capital gain, providing the statutory foundation for the tax deferral benefit that ROCQ and ROCY are engineered to deliver.

A $10 distribution on shares with a $100 cost basis reduces the investor’s cost basis to $90. Tax is deferred until the shares are sold, at which point capital gains treatment applies (long-term if shares have been held for more than one year).

For taxable account holders, the difference between paying ordinary income tax rates annually and deferring liability as a capital gain can be substantial, particularly for investors in the highest marginal brackets.

Two limitations temper the appeal of this structure, and both deserve attention:

For taxable account holders in higher income brackets, the difference between ordinary income and deferred capital gains treatment may be worth more than any fee advantage. But investors should not build a tax strategy that depends entirely on ROC classification remaining permanent.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The table below compares the six most relevant funds across strategy type, expense ratio, distribution classification, assets under management, and yield.

| Fund | Strategy | Expense Ratio | Distribution Type | AUM / Yield |

|---|---|---|---|---|

| ROCQ | Nasdaq 100 call spreads (FLEX options) | 0.35% | Return of capital (intended) | ~$144M / ~10% projected |

| JEPQ | Nasdaq 100 ELN overlay | 0.35% | ~90% ordinary income | ~$37.5B / ~10.48% |

| GPIQ | Nasdaq premium income (FLEX options) | 0.29% | Return of capital (intended) | Not separately specified / comparable |

| ROCY | S&P 500 call spreads (FLEX options) | 0.35% | Return of capital (intended) | ~$136M / ~8% projected |

| JEPI | S&P 500 ELN overlay | 0.35% | ~90% ordinary income | ~$45.2B / ~8.29% |

| GPIX | S&P 500 premium income (FLEX options) | 0.29% | Return of capital (intended) | ~$3B / comparable |

Projected yields for ROCQ (approximately 10%) and ROCY (approximately 8%) are estimates based on comparable funds. Neither fund has yet published a confirmed distribution.

Two non-fee distinctions matter more than the expense ratio gap:

Leveraged covered call ETFs extend the same call-writing overlay logic to portfolios with 1.25x equity exposure, producing yields that can exceed 13% while maintaining a portfolio delta of approximately 0.92, a structural variation that some income investors find worth evaluating alongside the unleveraged, tax-oriented positioning of ROCQ and ROCY.

The comparison table gives investors the numbers. What it does not give them is a framework for deciding whether the structural differences between these funds actually matter for their specific situation.

Covered call strategies with upside caps tend to outperform pure index exposure in flat or declining markets. The premium income provides a cushion that total-return-only portfolios lack. The cost emerges in strong rallies.

When the underlying index rises sharply, say 5-10% in a single month, a call spread strategy captures only the width of the spread rather than the full index gain. The sold call limits participation above its strike, and the purchased call merely prevents unlimited loss on the short position. Hamilton Reiner’s management approach at JP Morgan is expected to produce conservative strike selection, which may reduce this drag relative to more aggressive covered call managers, but will not eliminate it.

Both ROCQ and ROCY posted year-to-date returns of approximately 5.16% as of late April 2026. No distribution history exists yet, so yield projections remain estimates until first payouts are confirmed. VIX levels affect option premiums directly: elevated volatility increases the income generated by the fund, while compressed volatility reduces it.

Implied volatility is the key input that determines how much premium a call spread strategy can generate in a given period: when VIX is elevated, ROCQ and ROCY collect wider net premium credits on each position reset, and when volatility is compressed, the income generation capacity of both funds contracts accordingly.

Investor profiles where ROCQ or ROCY fit well:

Situations where these funds are less suitable:

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

ROCQ and ROCY offer a genuinely differentiated structure relative to JEPQ and JEPI. The FLEX options framework, return of capital distribution intent, and call spread mechanics address a real gap: the ordinary income tax drag that costs taxable account holders a measurable portion of their yield every year. Against GPIQ and GPIX, the competition is tighter, with a 6-basis-point fee disadvantage as the primary differentiator.

The absence of any distribution history means yield projections remain estimates. Investors interested in these funds may benefit from treating the next one to two full tax years as a validation period, watching for first distribution announcements, 1099-DIV classification confirmation, and performance across at least one meaningful market drawdown.

For investors already holding JEPQ or JEPI in taxable accounts, the practical next step is not an immediate swap. Monitoring for tax-loss harvesting opportunities during down markets offers a way to transition gradually while capturing a tax benefit in the process.

ROCQ and ROCY are covered call ETFs launched by JP Morgan on 19 March 2026, designed for taxable account investors. ROCQ targets the Nasdaq 100 and ROCY targets the S&P 500, both using FLEX options call spread strategies intended to distribute income as return of capital rather than ordinary income.

JEPI and JEPQ generate option income through equity-linked notes, with approximately 90% of distributions classified as ordinary income and subject to higher tax rates. ROCQ and ROCY use FLEX options call spreads structured to produce return of capital distributions, deferring tax until the investor sells their shares.

No, ROC classification is confirmed annually via 1099-DIV forms and can shift from year to year. QYLD, another covered call ETF, previously classified distributions as return of capital before experiencing reclassification at tax time, illustrating the annual uncertainty inherent in this structure.

No. The return of capital tax deferral advantage that makes ROCQ and ROCY attractive provides no marginal benefit inside tax-advantaged accounts such as Roth IRAs or 401(k) plans, where distributions are already tax-free or tax-deferred.

All four funds use FLEX options and target return of capital distributions, making them structurally similar. The primary differentiator is the expense ratio: GPIQ and GPIX charge 0.29% versus 0.35% for ROCQ and ROCY, a 6-basis-point gap that amounts to approximately $60 per year on a $100,000 allocation.