Why Governance and Communication Drive Post-IPO Value

7 hrs ago

Most investors, when they hear the word “pullback,” reach for a price chart. They scan for support levels, read a handful of broker notes, and start calculating whether this is the entry point they have been waiting for. That instinct is understandable. It is also the wrong place to start.

The market question, whether a pullback represents a buying opportunity, is the second question you should ask. The first is whether you are in a position to invest at all, given your specific income, your existing holdings, your time horizon, and your psychological wiring. Market pullbacks create time pressure and emotional noise that short-circuit systematic thinking. The investor who skips the personal audit is not acting on opportunity; they are acting on urgency.

By the end of this guide, you will have a concrete personal checklist to evaluate whether any market pullback is actually appropriate for your individual situation, before you touch a single price chart.

Here is the uncomfortable truth about investing during a market pullback: two investors looking at the same stock, at the same price, on the same day can reach opposite conclusions, and both can be right. The difference is not in what the market is doing. It is in what each investor’s circumstances allow.

The instinct to start with price action is almost universal, but it produces a specific error. It skips the only analytical step that is entirely within your control: an honest personal audit. Consider two investor archetypes:

Investor B is not slower. They are more disciplined. The self-assessment process is what separates genuine conviction from emotional urgency. A pullback is not inherently dangerous to buy into. Skipping the personal audit is what makes it dangerous. You may find, after completing the framework that follows, that you are well-positioned to act. Or you may find you are not. Both outcomes are equally valuable.

Your portfolio does not exist in isolation. It sits alongside your career, your income, and every financial commitment you have made for the next one to five years. Most investors assess their holdings as if employment income is a constant. It is not.

Career and income stability are material inputs into portfolio risk decisions. If your income is variable, contract-based, or tied to a cyclical industry, your risk capacity is lower than someone with a stable, salaried position, even if your portfolios are identical. This is the concept of correlated risk: when your income and your investments both move with the same economic cycle, a downturn hits you twice.

Income stability and risk tolerance are not abstract personality traits; they are concrete inputs determined by your time horizon, your career cyclicality, and your genuine ability to hold through a 20–30% portfolio drawdown without needing to sell, factors that a structured pre-investment assessment surfaces before any capital is committed.

“An investor in a cyclical industry who also holds a heavily equity-weighted portfolio faces compounded vulnerability during downturns.”

If your income moves with the economic cycle, your investment portfolio is already more correlated to a downturn than it appears on paper. Adding equity exposure during a pullback may feel like opportunity, but it is actually doubling down on the same underlying risk.

Before deploying any capital, separate your money into two pools:

Those facing variable or uncertain income should establish a meaningful cash reserve before taking on any further investment exposure. The size of that reserve matters, and until you have worked it out clearly, committing fresh capital to a pullback is premature.

Before you look outward at the opportunity, look inward at what you already own. Your current portfolio contains diagnostic information about whether adding to a position makes sense or quietly compounds a problem that already exists.

Existing portfolio concentration is as analytically important as evaluating the new opportunity itself. If you are already heavily weighted in a sector and that sector pulls back, adding further exposure is not diversifying risk. It is concentrating it.

Two portfolio states can both represent a form of risk, just in opposite directions.

| Dimension | Over-concentrated investor | Under-invested investor |

|---|---|---|

| Current exposure | Heavily weighted in one sector or position | Holding excess cash relative to long-term goals |

| Risk from adding | Compounds existing concentration | Low; adds diversification and growth exposure |

| Risk from not adding | Low; preserves balance | Misses compounding returns over time |

| Recommended action | Reassess before adding further exposure | A pullback may be a genuine deployment opportunity |

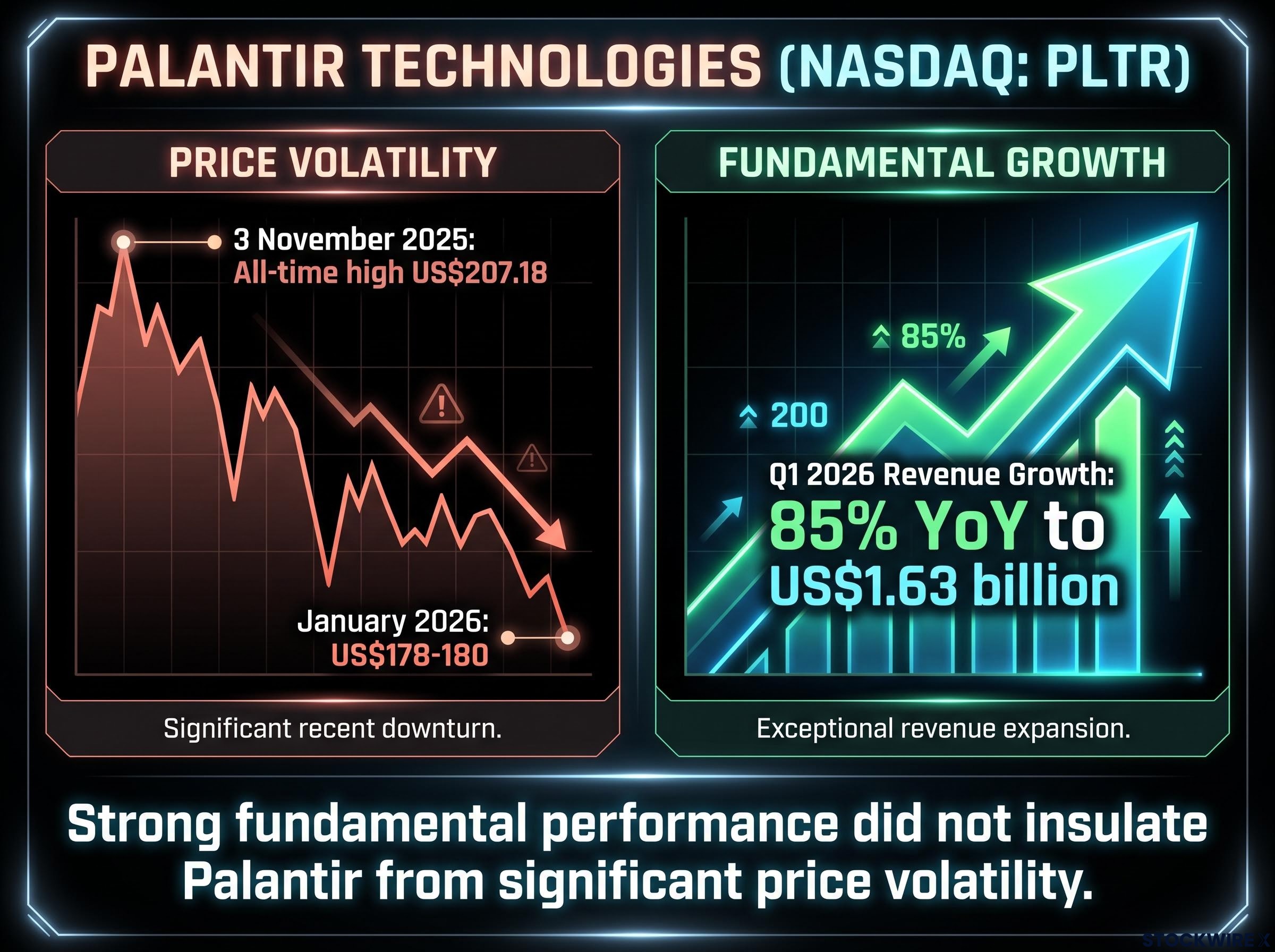

Palantir Technologies (NASDAQ: PLTR) offers a useful illustration. Around 3 November 2025, the stock recorded an all-time high closing price of US$207.18, propelled by strong investor appetite for its AI platform and a growing pipeline of government contracts. By January 2026, it had traded in the range of approximately US$178-180, and subsequent volatility continued, despite the company reporting Q1 2026 revenue growth of 85% year-over-year to US$1.63 billion.

Strong fundamental performance did not insulate Palantir from significant price volatility. Investors who bought at the momentum peak on FOMO grounds faced substantially depreciated positions even as the underlying business grew.

AI stock concentration illustrates the compounding vulnerability the article describes: when Broadcom reported disappointing results in June 2026, Marvell Technology fell more than 7% and Nvidia slipped nearly 1.1% on the same session, demonstrating how a single catalyst can simultaneously hit multiple positions in a portfolio already weighted toward one theme.

“The company is doing well” and “this is a good entry point for you specifically” are two separate questions. Your portfolio concentration determines which one matters more in your situation.

This is the question most investors skip, because FOMO does not feel like FOMO. It feels like analysis. It feels like a rational story forming in your head about why now is the right time.

The distinction matters. Genuine investment conviction is grounded in a thesis, a valuation framework, and a time horizon. FOMO is driven by social influence, past performance chasing, or the anxiety of watching other people make money while you sit on the sidelines. They produce identical feelings of urgency. They produce very different outcomes.

Genuine investment conviction treats permanent capital loss as the central risk to be managed, not short-term price volatility, which means the relevant question during a pullback is whether the business underpinning a position has deteriorated, not whether the share price has moved.

A diagnostic self-check can cut through the noise. Before acting during a pullback, ask yourself three questions in order:

“Would I be comfortable starting this position from scratch today, with no prior exposure to it at all?”

If you are averaging down on a declining position solely because the price is lower, without re-examining the underlying investment thesis, that is rationalisation, not discipline. Each purchase feels justified because the price is lower than the last one. But without a fundamental reassessment, you are compounding an existing error rather than improving your position.

Contracts for difference (CFDs, which are derivative contracts that let you speculate on price movements without owning the underlying asset), leveraged exchange-traded funds (ETFs), and short-dated options operate differently from standard equity positions. In some structures, losses can exceed your initial capital.

Before using any leveraged instrument during a pullback, you should be able to explain exactly how losses accumulate and at what point your exposure ends. If you cannot answer both questions with specificity, the instrument is not appropriate for your situation.

The consequences of misunderstanding leveraged exposure can be severe. A widely reported 2020 case involving a Robinhood user illustrates this starkly: the individual was presented with a large negative balance of roughly US$730,000 and died by suicide, with his death linked to a fundamental misunderstanding of how his trading positions actually worked. While the precise figure varied across different reports at the time, the tragedy stands as a clear warning that complex instruments carry dangers reaching far beyond ordinary financial risk.

The most dangerous moment in a pullback is not when prices are falling. It is when a rational-sounding story forms in your head explaining why you should buy more right now. The diagnostic questions above cut through that story before it becomes an action.

If you have completed the self-assessment and concluded that you are in a position to act, the next question is how. The answer is not “pick the bottom.” No investor can reliably do that.

Spreading your capital deployment across multiple tranches removes the psychological burden of needing to call the market bottom precisely. Fixing your schedule or price triggers before any emotional pressure sets in means each purchase decision is grounded in logic rather than anxiety. The goal is not to optimise your entry price to the cent. It is to participate at a range of prices that average to a reasonable entry over time.

The critical word is “in advance.” These parameters must be set before emotional pressure to act takes hold, because they will not be set rationally once the pressure arrives.

Before deploying any capital into a pullback position, you need to lock in three specific parameters:

| Parameter | What to define | Example | What happens without it |

|---|---|---|---|

| Capital ceiling | Maximum total amount to deploy | No more than $10,000 across all tranches | Position grows without a logical stopping point |

| Adding triggers | Price levels, dates, or rebalancing signals | Add $2,500 at each 10% decline from initial purchase | Purchases become reactive and emotionally driven |

| Exit or pause conditions | Criteria for stopping further purchases | Pause if position exceeds 8% of portfolio or thesis changes | Averaging down becomes rationalisation with no end |

Without predefined rules, incremental averaging can devolve into a rationalisation for continuing to buy a declining asset with no logical stopping point. The pre-commitment framework is not about optimising your entry price. It is about ensuring that the decision to invest was made rationally, even if the market conditions at the time of each purchase are anything but rational.

A common misunderstanding about what financial advisers offer during volatile markets is that their usefulness centres on forecasting where prices go next. In practice, their greatest contribution during a pullback is helping you make better decisions, not more accurate predictions.

A good adviser functions as a behavioural circuit-breaker. When markets move sharply and media coverage intensifies, the temptation to act impulsively grows. Having someone who can structure the conversation and anchor it back to your underlying plan can prevent a hasty response from overriding a sound strategy. The value of slowing down a poor decision is often greater than the value of identifying a good one.

When you sit down with an adviser during a pullback, bring specific questions rather than passively receiving a market view:

When two people share finances, investment choices carry weight beyond any individual preference. Partners often hold different assumptions about acceptable risk, how long money can be tied up, or how much cash should be kept accessible, and those differences can pull decisions in conflicting directions without either person realising it. One partner may see a pullback as opportunity; the other may see it as a reason to preserve cash. Neither is wrong. But when those differing views are never openly discussed, the gap between them becomes a risk in its own right.

An adviser-facilitated conversation is a way to make those different assumptions explicit before a volatile market forces a rushed, poorly aligned decision. If you find yourself disagreeing with your financial plan during a period of market volatility, that is exactly when you need the plan most, not when you should abandon it.

A market pullback may be a genuine opportunity or a genuine risk. The difference depends entirely on your individual circumstances, not on market conditions alone.

Before you look at a price chart, work through this checklist:

The investor who applies this framework consistently across multiple market cycles builds the decision-making discipline that compounds over time. That discipline is separate from, and arguably more valuable than, any single investment return.

For investors who have completed the self-assessment and want a structural framework for channelling the urge to act during pullbacks without disrupting long-term compounding, our dedicated guide to core-satellite investing explains how separating a stable diversified core from a bounded satellite allocation creates a legitimate outlet for active participation, with pre-set criteria that interrupt the FOMO chain before a market reaction becomes a portfolio disruption.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The most common mistake is starting with price charts and broker notes rather than first completing a personal audit of income stability, portfolio concentration, and emotional state, because buying during a pullback without that self-assessment means acting on urgency rather than genuine conviction.

Separate your money into near-term capital (funds needed within a few years for property deposits, education, or emergencies) and long-term capital (retirement or wealth-building funds with a seven-year or longer horizon); only long-term capital should be considered for deployment into a pullback.

Concentration risk is the danger of having too much of your portfolio weighted toward a single sector or theme; adding further exposure to a sector that has already pulled back compounds that existing imbalance rather than diversifying it.

Ask yourself three questions: whether you would start the position from scratch today with no prior exposure, whether your investment thesis has changed or only the price has moved, and whether you are buying because your analysis supports it or simply because a lower price feels like a bargain.

You should define a total capital commitment ceiling (the maximum you will deploy under any scenario), specific price thresholds or a schedule for adding to the position, and clear exit or pause conditions such as a portfolio concentration limit or a change in the underlying investment thesis.