Morningstar vs Markets: a 125-Point Gap in the US Rate Outlook

49 mins ago

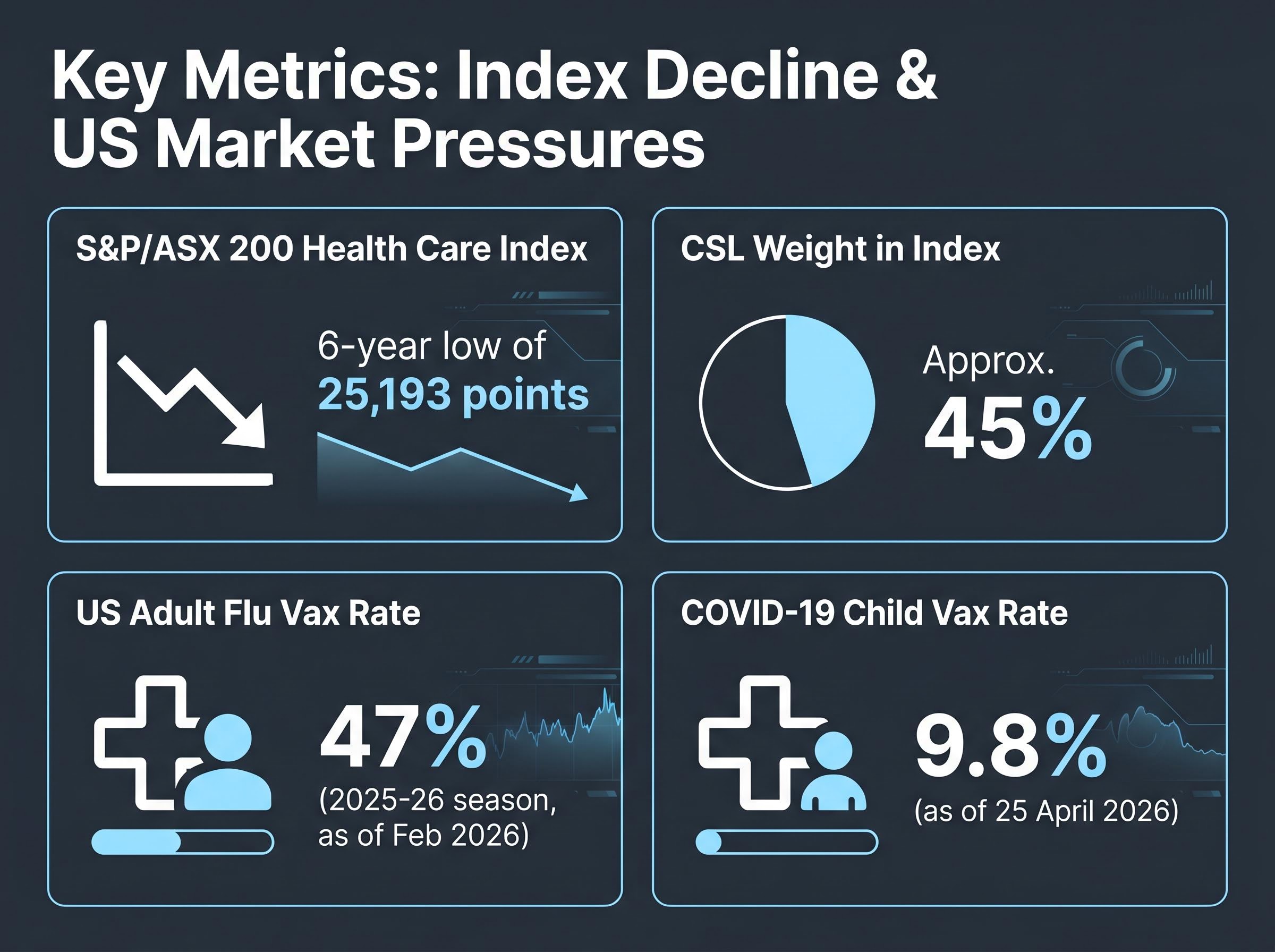

The S&P/ASX 200 Health Care Index has fallen to a six-year low of 25,193 points, making it the worst-performing segment of the entire ASX 200. That decline is not fully explained by interest rates or the Australian dollar.

While macro headwinds are real, including the Australian dollar at a four-year high of 71.3 US cents and two RBA rate rises already delivered in 2026, a separate structural risk has been building inside the US regulatory system. The Food and Drug Administration (FDA) is experiencing leadership instability at a scale that has disrupted approval timelines across multiple drug categories. Compounding that disruption, HHS Secretary Robert F. Kennedy Jr. has reshaped vaccine advisory processes in ways that carry direct commercial consequences for ASX-listed companies.

What follows is a clear-eyed account of how Washington’s regulatory dysfunction translates into specific, trackable risks for Australian biotech and healthcare investors, with practical indicators to monitor.

The FDA has lost more than 1,300 employees since 2025. That figure alone signals a staffing problem. The consequences, however, are more specific than a general slowdown.

Review categories most exposed to the personnel losses include:

These are the categories where the FDA’s remaining reviewers face the steepest knowledge gaps, and where submission backlogs have become most unpredictable. RealClearHealth reported in March 2026 that the dysfunction threatens the United States’ position as the global leader in biotech innovation.

The GAO oversight findings on FDA staffing confirm that overseeing food and drug safety has become materially harder as workforce reductions compound an already strained review system, with the proposed elimination of 3,500 FDA positions by HHS in 2025 identified as a direct threat to the agency’s operational capacity.

Boehringer Ingelheim’s zongertinib illustrates the new reality. The drug experienced documented delays before eventually receiving accelerated approval, a sequence that would have been unusual two years ago but now reflects the FDA’s erratic review cadence. BioPharma Dive has characterised the environment as one in which drugmakers are “guessing” at the agency’s trajectory, unable to model submission outcomes with confidence.

For smaller biotech companies, the loss of personnel with expertise in novel technologies has created a financing overhang. Investors are less willing to fund late-stage programmes when the approval timeline cannot be reliably estimated. Some firms moved clinical trials abroad during a turbulent 2025, seeking regulatory environments where review timelines remained predictable.

For any ASX biotech with a US market strategy, valuation multiples built on 12-18 month approval cycles may now be systematically mispriced.

Starpharma’s April 2026 FDA regulatory alignment for its DEP HER2 radioligand therapy candidate, confirmed through a formal Type C guidance meeting, demonstrates that structured pre-submission engagement can still yield predictable pathway outcomes even within the current review environment, though the process demands more explicit documentation than it did two years ago.

The policy concern is not abstract. Since taking the HHS Secretary role, Kennedy has taken specific actions that reshape the commercial environment for vaccine-focused companies:

The commercial signal is already visible. US adult influenza vaccination rates ran at 47% in the 2025-26 season as of February 2026, with the figure sitting at 43.9% as of January 2026. COVID-19 child vaccination rates stood at just 9.8% as of 25 April 2026.

CSL former CEO Dr Paul McKenzie acknowledged at the company’s October 2025 AGM that US influenza vaccination rates had declined more sharply than management anticipated, a rare admission that the regulatory and cultural environment was eating into forecast assumptions.

CSL represents approximately 45% of the S&P/ASX 200 Health Care Index. Deterioration in its vaccine franchise volumes is not a company-specific issue for investors holding index exposure. It is an index-level risk.

The Australian dollar’s 12% appreciation over the prior 12 months to 71.3 US cents compresses earnings when translated back to Australian dollars. Two RBA rate increases in 2026, with futures markets pricing a 76% probability of a further hike, weigh on growth-stock valuations. These are cyclical headwinds that investors understand and can model.

Regulatory disruption operates differently. A currency headwind reverses when the dollar weakens. An FDA that has lost institutional capacity in vaccine and gene therapy review does not rebuild that capacity when monetary conditions change.

| Risk type | Nature of risk | Expected resolution pathway |

|---|---|---|

| AUD/USD appreciation | Cyclical; compresses translated earnings | Reverses with currency cycle or RBA policy shift |

| RBA rate increases | Cyclical; raises discount rates for growth stocks | Reverses when rate cycle turns |

| FDA institutional capacity loss | Structural; impairs approval timelines for years | No clear resolution; requires sustained rehiring and institutional rebuilding |

| ACIP politicisation | Structural; disrupts vaccine recommendation pathway | Requires policy reversal or legislative reform; no automatic correction |

Research based on interviews with 16 biopharmaceutical investors across seed, venture, and private equity confirms that capital is already responding. Firms are restructuring portfolios away from US drug development and toward more mature assets and opportunities abroad, including China. Investors who treat the sector’s decline as purely macro-driven may re-enter on rate expectations alone, without recognising that the regulatory disruption is a separate variable entirely.

Telix Pharmaceuticals (ASX: TLX) has been the most publicly engaged with the changed FDA environment. In April 2025, the company issued a formal response acknowledging significant FDA changes while noting continued processing of applications. Its FY2025 results statement in February 2026 claimed alignment with the FDA on key issues for upcoming submissions.

Analyst commentary, however, identifies ongoing execution risks for Telix in 2026 despite its stated confidence. Stated alignment does not eliminate risk.

The information gap widens for smaller names. No specific statements from Immutep or Clarity Pharmaceuticals on FDA strategy changes have been identified in publicly available sources. That silence is itself a risk signal for investors who cannot assess how these companies are navigating the disruption.

Clinuvel provides a documented positive exception: an FDA update removed certain safety requirements for Scenesse, representing a favourable outcome. Isolated wins, however, do not change the sector trend.

Lumos Diagnostics’ FDA CLIA waiver for its FebriDx point-of-care test, secured in March 2026, represents the kind of isolated favourable outcome that mirrors Clinuvel’s Scenesse update: a specific regulatory win that expands addressable market materially but does not alter the broader review environment facing biotech and vaccine pipeline assets.

| Company (ASX code) | Documented FDA engagement | 12-month share price change |

|---|---|---|

| CSL (CSL) | AGM commentary on vaccination rates | Negative |

| Telix (TLX) | Yes; formal response and FY2025 alignment statement | Down ~45% |

| Clinuvel (CUV) | Yes; positive FDA update on Scenesse | Positive exception |

| Immutep (IMM) | Opaque; no public statements identified | Negative |

| Clarity (CU6) | Opaque; no public statements identified | Negative |

AusBiotech and Medicines Australia called in March 2026 for major government investment in life sciences to address structural challenges, signalling that industry bodies view the pressure as systemic rather than temporary. Companies with documented, specific FDA engagement strategies carry lower information risk. The quality of FDA communication in company announcements is a material due diligence variable, not a footnote.

The assumption that vaccine hesitancy is a public health story rather than an investment story does not survive contact with the commercial mechanics.

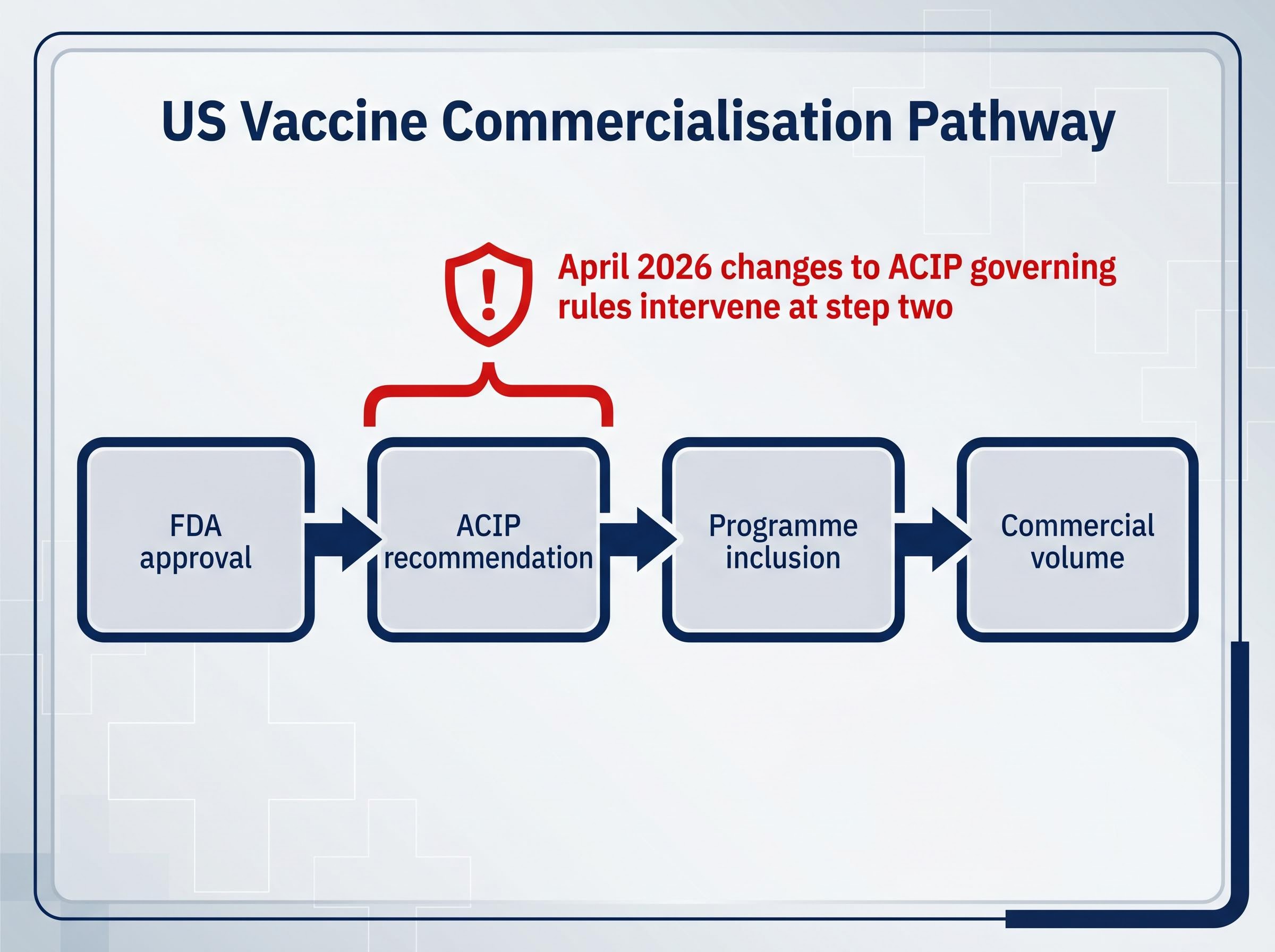

The US vaccine commercialisation pathway operates in four sequential steps:

RFK Jr.’s April 2026 changes to the ACIP’s governing rules intervene at step two. If a vaccine does not receive an ACIP recommendation, it is effectively locked out of the US public health purchasing system regardless of its FDA approval status.

The ACIP recommendation layer has become an independent variable with its own political risk dimension. Interviews with 16 biopharmaceutical investors confirm that vaccines are among the disproportionately affected categories, with reduced investment flowing into the space precisely because the recommendation pathway is now uncertain.

This risk extends well beyond pandemic-era vaccines. Influenza, RSV, and any novel infectious disease vaccine in development faces the same advisory committee uncertainty. Global vaccination rates are declining, providing a commercial volume backdrop that reinforces rather than offsets the US-specific policy disruption.

ASX investors holding companies with vaccine development pipelines should understand that FDA approval is now a necessary but no longer sufficient condition for US commercial success. This layer of risk is novel and may not yet be fully reflected in ASX biotech valuations.

The regulatory environment in Washington is neither stable nor predictable. It is, however, not entirely opaque. Specific signals can help investors distinguish between companies managing the disruption and those with unacknowledged exposure.

US policy signals to monitor:

Company-level disclosure signals to track in ASX announcements:

Geographic diversification of clinical programmes, exemplified by Nexsen’s parallel market entry strategy across the US, Asia-Pacific, and emerging markets for its StrepSure diagnostic, has emerged as a structural response to US regulatory uncertainty, giving companies revenue and approval optionality that reduces dependence on a single regulatory pathway.

CSL’s approximately 45% weighting in the index makes its disclosures the single most consequential data point for sector-level positioning. At the domestic level, AusBiotech and Medicines Australia’s March 2026 advocacy for government life sciences investment, alongside CSL and medical researchers’ January 2025 call to address the research funding crisis, may create opportunities that reduce some companies’ dependence on the US regulatory pathway over time.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The cyclical headwinds are reversible. If the Australian dollar weakens or the RBA shifts its rate trajectory over the next 12-36 months, the earnings translation and valuation compression pressures on ASX healthcare names will ease. The market may already be pricing some of that expectation into select names.

The structural risks carry no such timeline. FDA institutional capacity, once lost, takes years to rebuild. The politicisation of the ACIP recommendation process has no automatic correction mechanism and may persist regardless of which party holds power in Washington. The cultural shift in US vaccination behaviour, reinforced by institutional signals like the military’s policy change, does not reverse with an election cycle.

Capital is already migrating. The investor survey of 16 biopharmaceutical investors confirms portfolio restructuring away from US drug development, with some capital redirected toward China and other jurisdictions.

Capital migration away from unfavourable regulatory environments is not unique to the ASX; AstraZeneca’s decision to redirect substantial capital toward China rather than commit to UK infrastructure projects, despite active MHRA reforms, demonstrates that multinational capital allocation responds to regulatory credibility signals in ways that regulatory reform announcements alone cannot quickly reverse.

The ASX healthcare sector’s decline to a six-year low reflects a genuine, multi-layered deterioration. Investors who treat it as a simple mean-reversion opportunity without distinguishing the regulatory layer from the cyclical layer are accepting unpriced structural risk.

Past performance does not guarantee future results. Forward-looking statements regarding regulatory outcomes and sector recovery are speculative and subject to change based on policy developments and market conditions.

—

The S&P/ASX 200 Health Care Index has fallen to 25,193 points due to a combination of cyclical headwinds (a strong Australian dollar and RBA rate rises) and structural risks including FDA staffing losses of over 1,300 employees and policy changes under HHS Secretary RFK Jr. that have disrupted vaccine commercialisation pathways.

RFK Jr. has changed CDC vaccine advisory committee rules and presided over the elimination of the US military's annual flu vaccination requirement, meaning ASX companies with vaccine pipelines face a risk that FDA approval alone no longer guarantees access to the US public health purchasing system.

The Advisory Committee on Immunisation Practices (ACIP) issues formal recommendations that determine whether an FDA-approved vaccine is included in US federal and state purchasing programmes; following RFK Jr.'s April 2026 rule changes, this recommendation layer now carries independent political risk that can block commercial access even after regulatory approval.

CSL carries the greatest index-level exposure given its roughly 45% weighting in the S&P/ASX 200 Health Care Index and declining US influenza vaccination rates; Telix Pharmaceuticals (TLX) is also exposed, with its share price down approximately 45% over 12 months, while Immutep and Clarity Pharmaceuticals have provided no public commentary on how they are managing the disruption.

Investors should track ACIP meeting outcomes, HHS budget and FDA restructuring announcements, CDC seasonal vaccination rate data as a leading indicator for CSL revenue, and company-level ASX disclosures that include explicit FDA engagement language, revised submission timelines, or mention of clinical trial migration to non-US jurisdictions.