Are Rate Hikes Actually Bad for Stocks? What the Data Shows

2 hrs ago

A retiree who enters a bear market with two years of living expenses in cash never has to sell a single share of stock at a loss. One who enters fully invested in equities may be forced to liquidate at exactly the wrong moment, permanently shrinking the portfolio that needs to last 30 years. With stock market volatility persisting into 2026 and yields on cash and bonds still meaningfully above pre-2022 levels (money market funds yielding approximately 3.35-3.57%, five-year Treasuries near 4%), the retirement bucket strategy has become the dominant framework US financial planners use to protect portfolios from sequence-of-returns risk. Roughly 80% of CFP professionals recommend some version of it, and institutions from Vanguard to Charles Schwab have published their own refined models. This guide explains how to build each of the three buckets, what to put inside them, how to size them based on specific expenses and Social Security income, when to start the transition before retirement, and which bond choices to avoid in the conservative bucket.

Consider two retirees, each with a $1 million portfolio and identical 7% average annual returns over 20 years. The only difference: one retires into three strong opening years, the other into three poor ones. The retiree who draws down during early losses depletes the portfolio faster, because withdrawals compound against a shrinking base. The one who retires into early gains withdraws from a growing base, and the portfolio sustains itself far longer. Same average return, dramatically different outcome.

This is sequence-of-returns risk: the specific danger that withdrawals taken during a market downturn at the onset of retirement create a compounding negative effect on remaining assets. It is most damaging in the first five to ten years, when the portfolio is at its largest and withdrawals represent the smallest relative share. A bad sequence in those years can permanently impair a portfolio’s ability to recover.

Scott Bishop, CFP and co-founder of Presidio Wealth Partners, identifies this mechanism as the core motivation for shifting toward fixed income and cash in the years before retirement. The bucket strategy is the structural answer: by segregating assets into time-horizon-specific layers, a retiree is never forced to sell growth assets during a downturn.

The difference between a fully invested retiree and a bucketed retiree during a bear market:

Having liquid assets available during a bear market converts what could be a permanent portfolio impairment into a temporary paper loss. The bucket strategy exists to buy time for recovery.

The framework divides a retirement portfolio into three layers, each matched to a specific time horizon. Together, they form a system: Bucket 1 funds current spending, Bucket 2 replenishes Bucket 1, and Bucket 3 compounds over decades to sustain purchasing power.

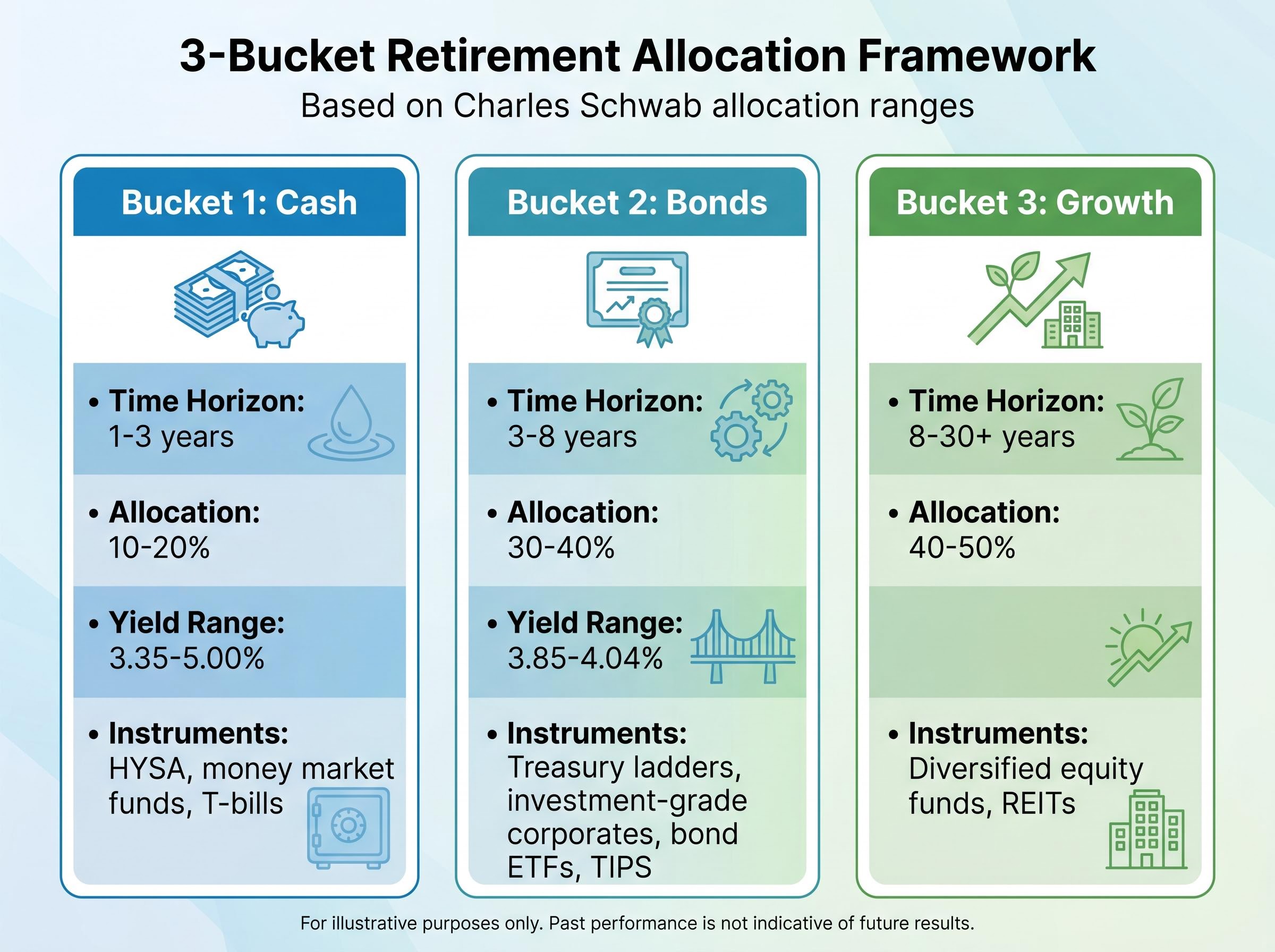

Charles Schwab’s published allocation ranges provide a useful baseline: approximately 10-20% of the total portfolio in Bucket 1, 30-40% in Bucket 2, and 40-50% in Bucket 3, with a minimum of one year of expenses in cash and more than eight years of expenses allocated to long-term growth.

| Bucket | Time Horizon | Instruments | Current Yield Range | Allocation (% of Portfolio) |

|---|---|---|---|---|

| Bucket 1: Cash | 1-3 years | HYSA, money market funds, T-bills | 3.35-5.00% | 10-20% |

| Bucket 2: Bonds | 3-8 years | Treasury ladders, investment-grade corporates, bond ETFs, TIPS | 3.85-4.04% | 30-40% |

| Bucket 3: Growth | 8-30+ years | Diversified equity funds, REITs | N/A (growth-focused) | 40-50% |

This is the spending account. It holds one to three years of living expenses in instruments that are fully liquid and carry minimal risk. The purpose is singular: fund retirement spending during market downturns without touching equities.

Appropriate instruments include high-yield savings accounts (FDIC-insured, with top institutions currently offering up to 4.21-5.00% as of May 2026), money market funds (Vanguard VMFXX at 3.57% seven-day SEC yield, Fidelity SPRXX at 3.35%), and three-month T-bills at 3.69%. Liquidity and capital preservation are the only criteria here; yield is a secondary benefit.

Bucket 2 is the replenishment engine. It holds three to eight years of expenses in fixed income instruments that generate income and mature on a schedule designed to refill Bucket 1 as it depletes.

Instruments include individual Treasury ladders (three-to-seven year maturities, with two-to-five year yields currently in the 3.88-4.04% range), investment-grade corporate bonds, short-to-intermediate bond ETFs (VGIT with a current yield of approximately 3.85%), and a roughly 20% TIPS allocation for inflation protection per Schwab guidance. Duration management matters here: holding bonds to maturity reduces mark-to-market volatility.

The growth engine holds everything remaining, typically 40-50% of the total portfolio. It is invested in diversified domestic and international equity funds and REITs, with a 20-to-30 year time horizon.

This bucket is what sustains purchasing power across a multi-decade retirement. It will experience drawdowns, and that is by design. The entire point of Buckets 1 and 2 is to ensure Bucket 3 never needs to be touched during those drawdowns.

Equity compounding mechanics explain why Bucket 3 tolerates decades of drawdown cycles without undermining a retirement portfolio: diversified equities have delivered approximately 7% real annual returns since 1802, and the second decade of a compounding investment generates nearly double the dollar gains of the first, making uninterrupted time in market the core structural argument for leaving growth assets untouched.

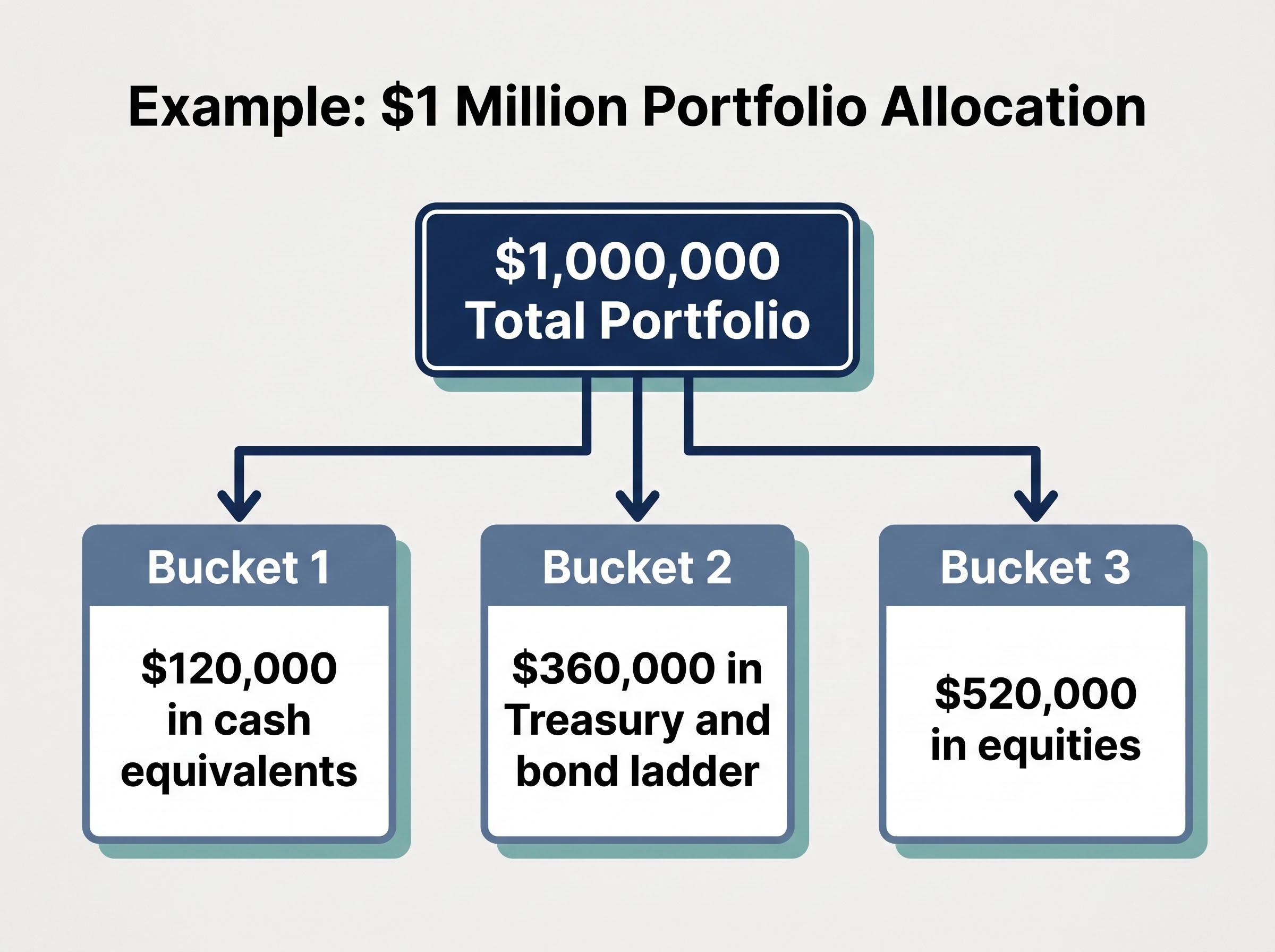

The single most common error in bucket construction is sizing based on total retirement expenses. The correct starting point is the income gap: total expected annual spending minus guaranteed income sources (Social Security, pension). This gap, not total expenses, is what the portfolio actually needs to cover.

The bucket only needs to cover the gap between total expenses and guaranteed income. A retiree with $60,000 in annual expenses and $24,000 in Social Security income has a $36,000 income gap, not a $60,000 problem.

Here is the six-step setup process:

The refill conditions described above share the same mechanical logic as portfolio rebalancing triggers more broadly: Vanguard recommends a 5% drift threshold as the standard benchmark, and a Bucket 3 equity allocation that has grown well beyond its target after a multi-year rally is itself a signal that the bucket split requires attention.

Social Security timing functions as a sizing lever. Delaying claims to age 70 increases the guaranteed monthly benefit, shrinks the income gap, and allows more assets to remain in Bucket 3. Retirees with substantial Social Security or pension income may only need 6-12 months in Bucket 1 rather than two to three years, freeing capital for growth. Conservative retirees without significant fixed income sources may need up to three years in Bucket 1.

The CFPB retirement income planning guidance addresses Social Security claiming decisions, pension payout options, and guaranteed income sources, all of which directly affect how large a retiree’s income gap will be and, by extension, how much capital must be allocated to Buckets 1 and 2.

Tools such as Schwab’s bucket calculator, Fidelity’s retirement income planner, and Morningstar’s retirement tools support modelling of bucket sizes and refill scenarios.

The fastest way to undermine the bucket strategy is to reach for yield in the one bucket designed for stability. Flavio Landivar of Evensky and Katz / Foldes Wealth Management is direct on this point: the fixed income component of a pre-retiree’s portfolio should not be used as a vehicle for pursuing additional yield through lower-quality securities.

Flavio Landivar, Evensky and Katz / Foldes Wealth Management: The fixed income component of a pre-retiree’s portfolio should not be used as a vehicle for pursuing additional yield through lower-quality securities.

High-yield bonds carry elevated credit risk that defeats the purpose of a stability bucket. If Bucket 2 loses 10-15% during the same downturn that is depleting Bucket 1, the entire framework collapses. The retiree ends up needing to sell equities anyway.

Duration risk is the second threat. Longer-duration bonds carry more price sensitivity to interest rate changes. Morningstar analysis flags that a 50 basis point rate rise produces approximately 1-2% price decline on intermediate bond holdings. Manageable if held to maturity, but problematic if early liquidation is required.

Two structural approaches dominate professional guidance for Bucket 2:

Appropriate for Bucket 2:

Avoid in Bucket 2:

One exception: municipal bonds, with their tax-exempt status, are more appropriate in taxable accounts for investors in high-tax states, where the tax-equivalent yield may exceed comparable taxable alternatives.

The bucket strategy’s protective value is highest when it is already in place before a downturn occurs. Building it reactively during a bear market defeats its purpose entirely. Scott Bishop recommends beginning the transition two to three years before the target retirement date.

The logic is straightforward. Entering retirement already bucketed means a market downturn in year one does not force emergency cash raising. Entering fully invested means the first bear market triggers exactly the sequence-of-returns damage the strategy exists to prevent.

Here is a practical transition timeline:

The opportunity cost objection is predictable. Holding cash and bonds during a strong equity bull market feels costly. That cost is real, but the function is insurance against a specific catastrophic scenario. It is not a return-maximisation strategy.

Market correction positioning in the years immediately before retirement is where the bucket strategy and broader portfolio risk management intersect most directly: three independent valuation signals are currently elevated simultaneously, and holding short-duration Treasuries yielding more than the S&P 500 earnings yield provides a mathematically defensible case for the cash allocation a pre-retiree is building into Buckets 1 and 2 anyway.

Formulas such as “100 minus age” for bond allocation persist in popular financial guidance, but they are an inadequate substitute for individualised bucket sizing. Scott Bishop draws a distinction between risk tolerance (emotional comfort with volatility) and risk requirement (the level of risk actually needed to meet financial goals). Standard risk tolerance questionnaires often overstate risk appetite after periods of strong market performance, precisely when the greatest danger lies ahead.

Both Bishop and Landivar recommend that a financial plan, not an age-based formula, should drive pre-retirement asset allocation. The income gap calculation described earlier provides a more reliable foundation than any single rule of thumb.

Where each bucket lives is as consequential as what it contains. The wrong placement compounds tax drag across a 20-to-30 year retirement horizon; the correct placement allows each bucket’s characteristics to align with each account type’s tax treatment.

| Bucket | Optimal Account Type | Tax Rationale |

|---|---|---|

| Bucket 1: Cash | Taxable accounts | Full liquidity without early withdrawal penalties; interest taxed as ordinary income but access is immediate |

| Bucket 2: Bonds | Tax-deferred (traditional IRA, 401k) | Bond interest (ordinary income) is sheltered from current taxation, allowing compounding within the account |

| Bucket 3: Equities | Roth accounts | Long-term capital gains and qualified withdrawals are tax-free, maximising after-tax value of highest-growth assets |

Municipal bonds are the one exception. Their tax-exempt status provides the most benefit in taxable accounts, particularly for investors in high-tax states. Placing munis inside a tax-deferred account wastes their primary advantage.

Withdrawal sequencing follows a logical order:

Refilling between buckets can trigger capital gains in taxable accounts. Coordinating refill timing, for instance selling equities to replenish Bucket 2 only after identifying tax-loss harvesting opportunities, improves overall efficiency. Fidelity’s tax-savvy withdrawal framework (fidelity.com/viewpoints/retirement/tax-savvy-withdrawals) provides detailed sequencing guidance.

A retiree who holds bonds in a Roth account and equities in a taxable account has the tax advantages of the strategy backwards. The placement decisions above ensure each bucket’s tax characteristics align with each account type’s treatment.

Even readers who understand the framework correctly can undermine it through implementation errors. These five mistakes appear consistently across professional guidance and retirement planning communities:

The choice between total return vs dividend income approaches within Bucket 3 carries meaningful long-term consequences: a total market portfolio returned 10.49% annualised from 2016-2025 versus 9.43% for a dividend-focused portfolio, a gap that compounds to roughly $116,000 in additional wealth on a $100,000 investment over 20 years and matters considerably when the bucket has a 20-to-30 year time horizon.

Most research supports one to three years maximum in cash for Bucket 1. Beyond that threshold, the insurance premium exceeds the risk it hedges, and the opportunity cost compounds significantly over a multi-decade retirement.

Schwab offers a useful guardrail: if Bucket 1 drops more than 20% below its target (due to higher-than-expected spending), reduce discretionary withdrawals until refilled. This type of spending flexibility is what distinguishes the bucket approach from rigid rule-based withdrawal methods, and it only works with consistent monitoring.

The strategy’s protective value is highest when it is already in place before a market downturn occurs. Building buckets reactively during a bear market misses the point entirely; the time to construct the framework is before it is needed.

Three decisions define the implementation:

The behavioural benefit is itself a return-enhancing feature. Knowing that two to three years of living expenses sit in cash, untouched by market movements, prevents the panic selling that destroys portfolios during downturns. The strategy does not just protect against sequence-of-returns risk; it protects against the retiree’s own worst instincts.

Tools including Schwab’s bucket calculator, Fidelity’s retirement income planner, and Morningstar’s retirement tools allow readers to model their own bucket sizes using the framework outlined above.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The retirement bucket strategy divides a portfolio into three time-horizon-specific layers: a cash bucket for current spending (1-3 years of expenses), a bond bucket for replenishment (3-8 years), and a growth bucket of equities for long-term wealth preservation, so retirees never need to sell stocks during a market downturn to cover living costs.

Most research and professional guidance supports holding one to three years of your income gap (total expenses minus guaranteed income like Social Security) in cash equivalents; holding five or more years in cash increases opportunity cost to the point where the insurance premium exceeds the risk it hedges.

Sequence-of-returns risk is the danger that withdrawals taken during a market downturn early in retirement compound negatively against a shrinking portfolio base, potentially causing permanent impairment even if long-term average returns are identical to a retiree who experiences early gains.

Financial planners including Scott Bishop of Presidio Wealth Partners recommend beginning the transition two to three years before your target retirement date, redirecting contributions into cash equivalents and funding the first bond ladder rungs so Buckets 1 and 2 are fully operational before the first withdrawal.

High-yield bonds and long-duration bond funds should be avoided in Bucket 2 because high-yield bonds carry credit risk that defeats the purpose of a stability bucket, and long-duration bonds are highly sensitive to interest rate changes, both of which can force equity sales if Bucket 2 loses value during the same downturn depleting Bucket 1.